Chris Whitehead/DigitalVision via Getty Images

Main thesis

Procter & Gamble (NYSE:PG) is the world’s largest consumer goods corporation, which is an undisputed leader in many segments. Thanks to the concentration of a huge number of brands specializing in different segments, the company has practically no major competitors. Procter & Gamble ramps sales, raises selling prices, and focuses on cost control to help the company grow organically.

I believe that the in the current situation, the corporation proves its business strength and relatively wide moats. However, the market is totally aware of this and gives a completely fair valuation. Thus, the upside and downside are limited.

Position in the industry

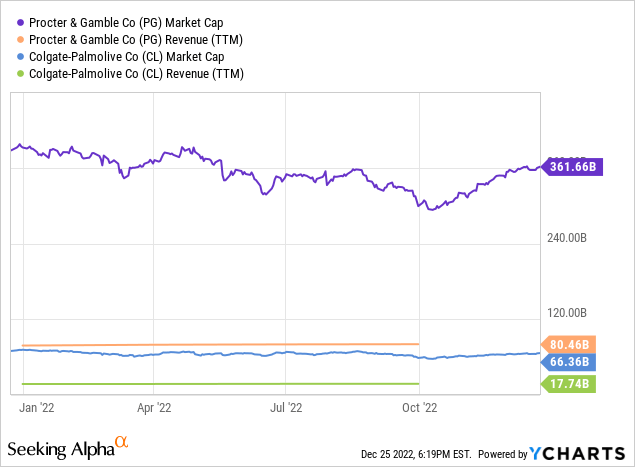

P&G-owned brands have a significant market share. More specifically, 36% in fabric & home care; 30% in baby, fem & family care; 18% in beauty care; 20% in health care, and 47% in the grooming sector. Thus, the company practically has no serious competitors. Colgate-Palmolive (CL) is one of the only P&G competitors, whose products are presented in more than one segment. It successfully develops lines of products for the home, oral hygiene, and body care but their sizes are just not comparable.

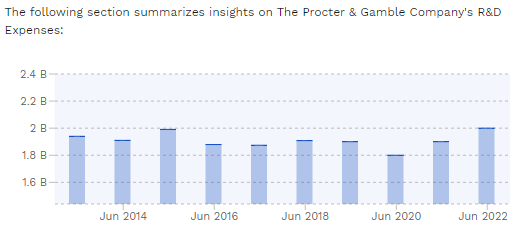

The company’s strategy is that when entering a new market or in order to regain its positions, P&G seeks to constantly raise the bar of its products, which makes the brands stronger than those of competitors. Marketing also plays a big role. PG is one of the largest advertisers in the world with about 10% of its revenue annually spent on marketing. It stimulates sales through brand awareness, helps to enter new markets, and allows the company to charge higher prices than unadvertised brands. Procter & Gamble has a $2 billion R&D budget to respond to changing consumer packaging and product preferences.

Finbox

PG continues to focus on cash efficiency and cost savings and sees this as a key driver of long-term growth. According to the company, each expense item is checked. The company has gone through a series of restructurings in the past, including a reduction in the number of brands (from 170 to 65) and product categories.

No recession fears here

Consumer staples products are non-cyclical, so demand for them is more stable even during periods of recession than for consumer cyclical goods. Also, the main part of the company’s products is all-weather, so sales do not change seasonally, with the exception of some health products. P&G products are and will be used by 5 billion people around the world, despite the economic turmoil. Thus, the company has a fairly predictable revenue structure.

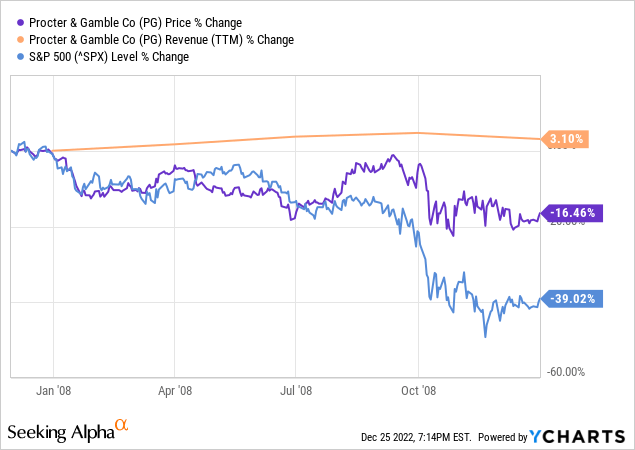

If we consider the performance during periods of economic crisis, then in 2008, PG shares fell by 16%, while S&P 500 dropped by 38%. At the same time, FY2008 revenue grew 9% compared to the last year before falling just 3.4% in FY2009.

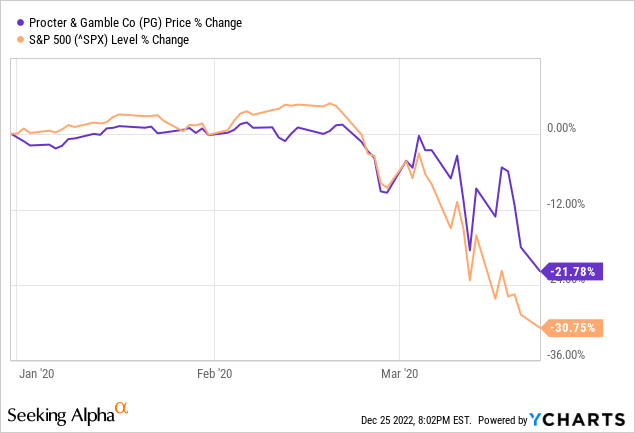

In 2020 (January-March), Procter & Gamble shares fell by 21.8%, S&P 500 dropped by 30.7%.

In addition, after general market crashes, P&G stock recovers faster than the S&P 500. It took Procter & Gamble 2 years and 2 months to return to 2007 prices, the S&P 500 index took more than 4 years. After falling in March 2020, PG recovered in 4 months, while S&P 500 did it in 5.

Payout to shareholders

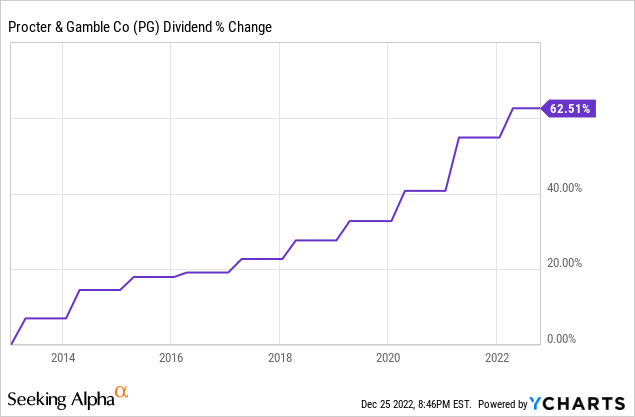

The company has paid regular quarterly dividends since its founding in 1890 and has increased them annually for 65 consecutive years.

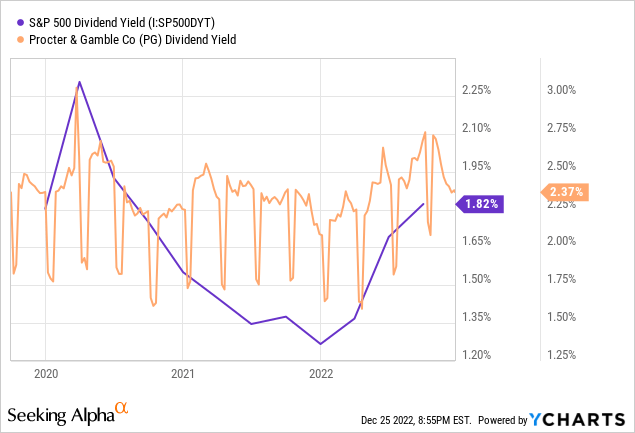

Dividend payments have been growing at a CAGR of 4.5%, which is below the industry’s average of 6.5%.The payout ratio is 60%, which will allow the company to continue to increase dividends without any problems even if earnings would fall. Procter & Gamble’s dividend yield has declined to 2.4% over the past 3 years due to rising stock prices but remains well above the S&P 500’s average return of 1.7% and in line with the industry average value.

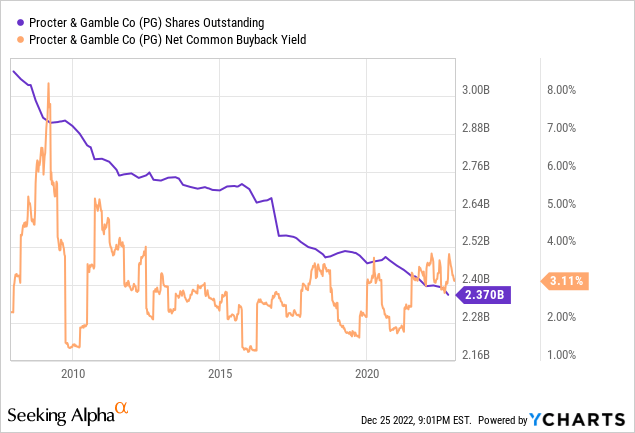

Over the past 15 years, the number of shares outstanding has decreased by 23%. That’s not Apple (AAPL)-like, but still very solid, considering that the net buyback yield is 3.11% now.

Growth rates

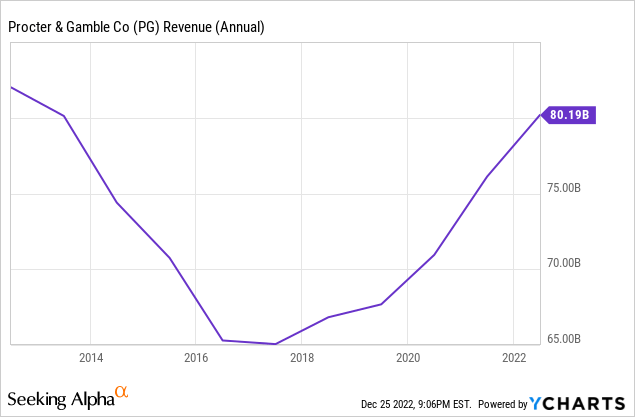

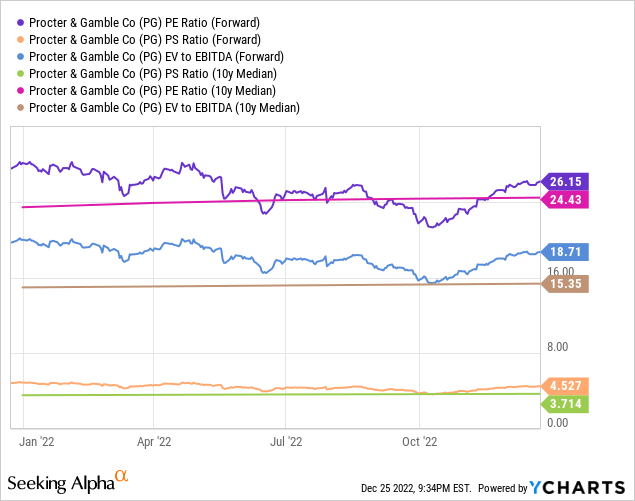

In 2012, the company’s revenue reached $82 billion, after which it began to decline.

Procter & Gamble was gradually losing the market due to a very large number of its own brands competing with each other, which formed a kind of sales cannibalization effect, and the inability to focus on the development of the most promising areas. When the number of brands reached 170, the company announced its intention to sell or retire up to 100 of its brands. Thus, P&G sold the battery company Duracell to Berkshire Hathaway (BRK.A)(BRK.B) for $2.9 billion. In 2016, P&G sold 43 beauty brands to Coty (COTY) for $12.5 billion and soap brands to Unilever.

Currently, Procter & Gamble has 65 brands in its portfolio and the company manages to carry out successful marketing campaigns and regain lost ground in the market. Since 2017 revenue has been growing, but it’s just too slow as the CAGR has only reached 3.5%.

P&G Ventures is developing new products and constantly innovating, but due to a very high base, these improvements won’t help the company to grow faster.

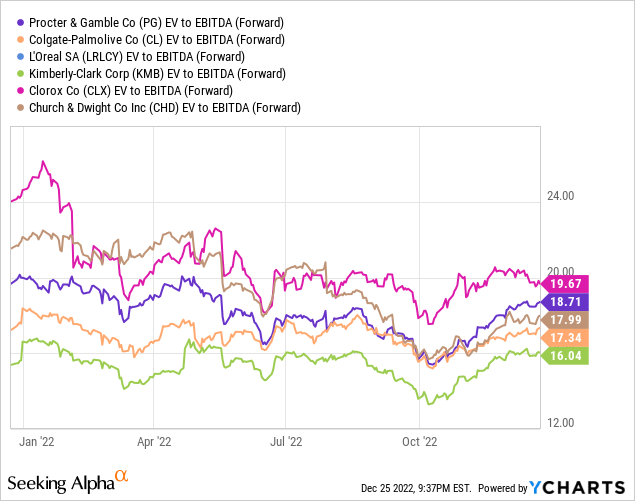

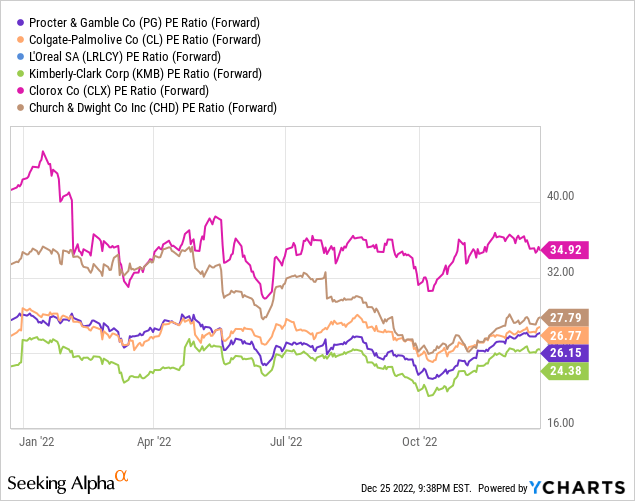

Valuations

Forward P/E, P/S, and EV/EBITDA multiples are not that far from the medians given P&G’s position in the industry.

Compared to peers, Procter & Gamble doesn’t look too expensive either. Just fairly priced.

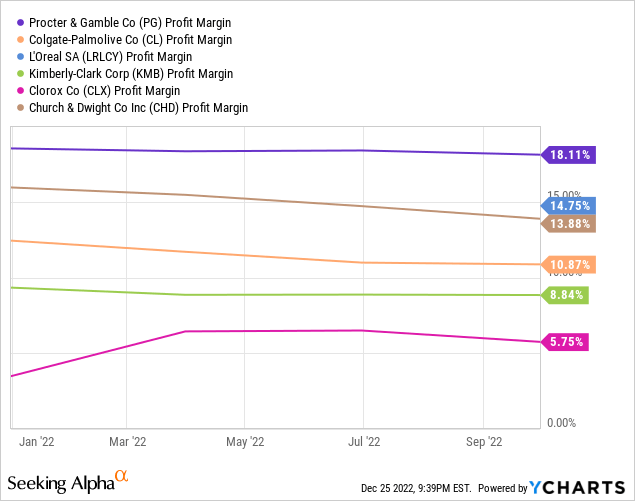

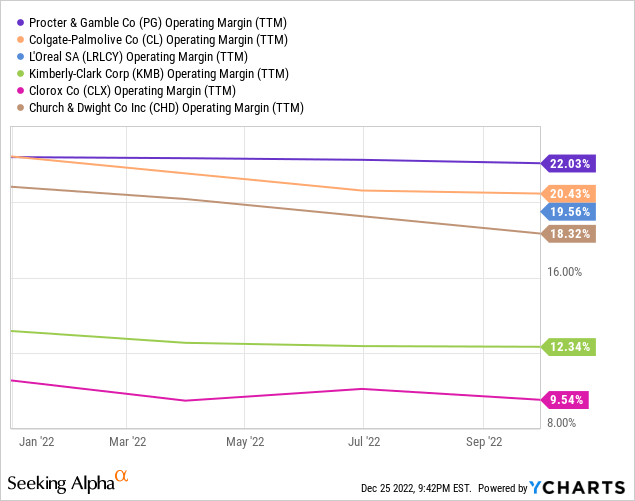

The premium valuation is mainly driven by P&G’s higher profitability.

Conclusions

The company does an excellent job of expanding and gradually increasing the once-lost market share. The scale can be considered the main advantage over competitors. Procter & Gamble Co is one of the best conservative blue chips in the US market and an excellent safe haven in case of economic shocks.

The company’s revenue is growing at a slow pace, but the company is still a leader in many segments and this is unlikely to change in the next 40-50 years. I believe that the company is ideally valued by the market, and the upside or downside potential is very limited.

Be the first to comment