MF3d

Power Integrations (NASDAQ:POWI) just published its fourth quarter results, and it was not pretty at all. The company had already warned investors that results were going to be weak, but it is still painful for investors to see that revenues were down 22% sequentially to $125 million. This is in line with the company’s previous guidance, but it is still a very meaningful decline and shows the depth of the downturn in the semiconductor industry. Even worse, the company expects a further sequential decline in the March quarter as end demand continues to be soft and distribution inventories remain elevated.

Perhaps no segment illustrates the severity of the downturn better than the consumer category, which is dominated by appliances, which was down more than 30% with weakness across all categories. This was despite the company gaining share across many competitors in appliances.

Still, despite the severity of the downturn, there are also some positives. The company sounds a lot more optimistic about the second half of the year, and it has a history of investing heavily during downturns in order to gain market share and outperform during the economic rebound. During the earnings call the company specifically mentioned seeing strong growth in home and building automation, renewables like solar and wind, and power grid products like high voltage DC transmission. They are seeing particularly strong activity in EVs, and also in new appliance designs. The company did caution that some of these design wins, especially in longer design cycle products like EVs, won’t turn into revenue overnight.

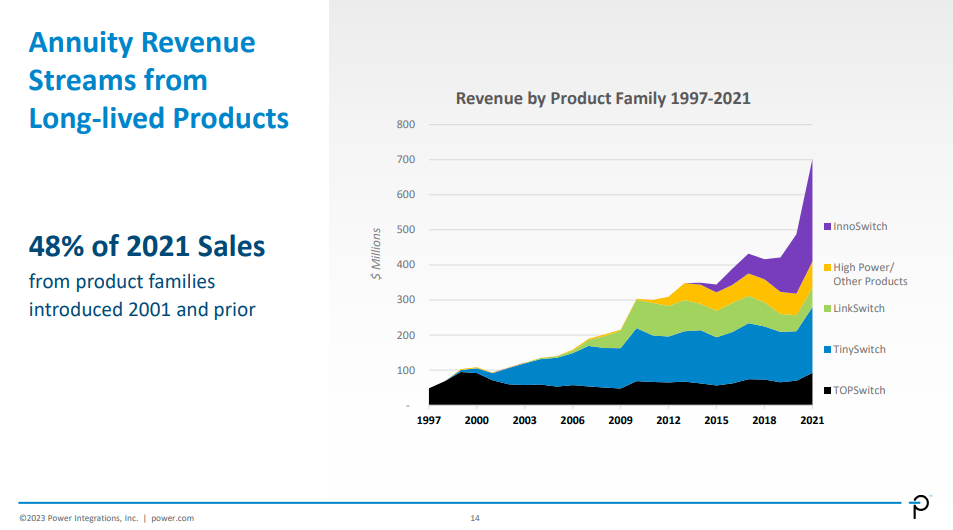

One thing that makes analog devices like the one power integrations manufactures special, is that they have very long lives. All of these design wins and market share gains the company is talking about are likely to stick for a long time. One interesting statistic is that 48% of 2021 sales were from product families introduced in 2001 or before. This is one of the reasons why we are so optimistic that the new opportunities will be additive to the company’s revenue and that it will soon be delivering new records once this downturn is over.

Power Integrations Investor Presentation

The key message is therefore that the downturn is an opportunity for the company to gain market share because they are investing for the future, and that they are likely to come out stronger on the other side. The company is guiding for revenues to bottom in the March quarter, followed by sequential growth in the June quarter.

Financials

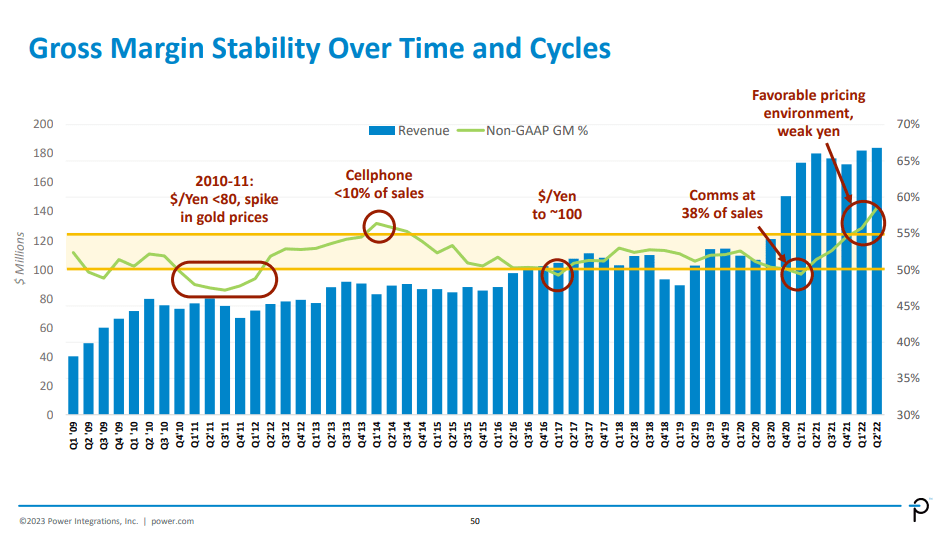

Non-GAAP gross margin was a little disappointing at 54.7% compared to the company’s previous guide of 56% to 56.5%. Compared to the previous quarter, gross margin was down about three percentage points. The company attributed this to mix and the impact of lower production volumes. Non-GAAP operating margin for the quarter was 22.5% and non-GAAP earnings of $0.48 per diluted share. Still, it is worth looking at the big picture, and how resilient gross margins have been even during downturns, rarely going below 50%. In recent periods the weak yen has proven a tailwind.

Power Integrations Investor Presentation

Growth

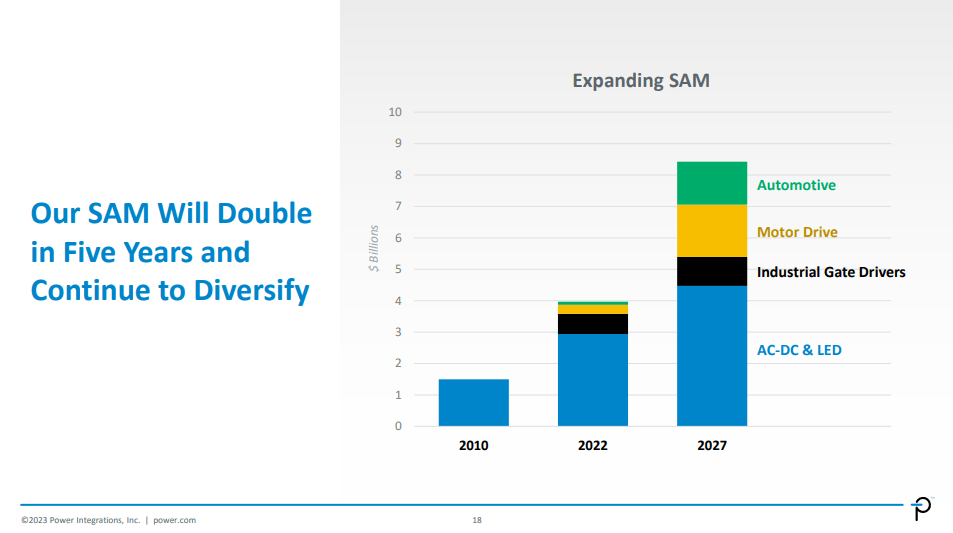

As part of the big picture, it is also worth remembering that during the company’s recent analyst day, they shared plans to double serviceable addressable market over the next several years. They also plan to expand the portfolio of GaN products to address a wider range of applications. Particularly in brush-less DC motors and EVs, each of which the company expects will be a $1 billion opportunity by 2027.

Power Integrations Investor Presentation

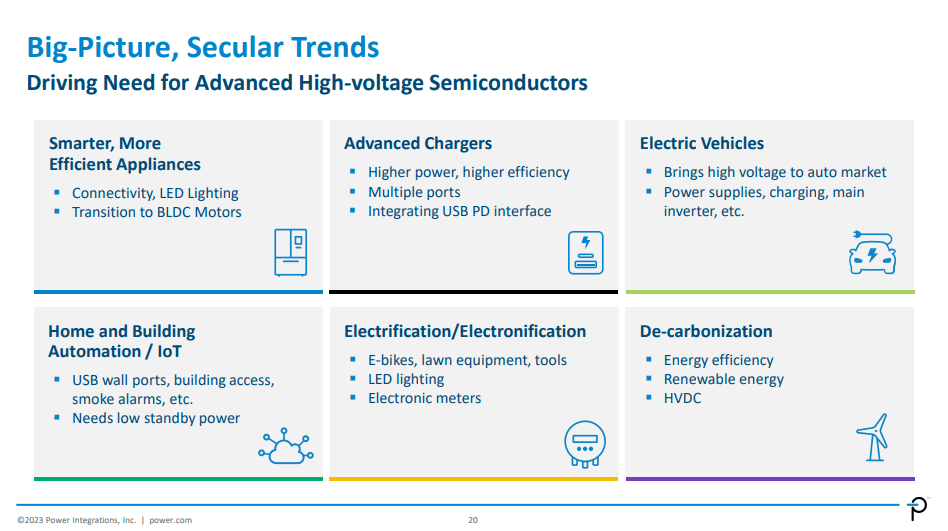

The company made some progress towards this vision during the quarter, by winning five new automotive designs in Q4. It now has more than three dozen designs in production servicing about fifteen end customers. Both of these figures are on track to increase significantly, with as many as 20 new programs already scheduled to enter production this year and many more in the pipeline. The slide below summarizes nicely the several secular tail winds the company should benefit from in the coming years.

Power Integrations Investor Presentation

Guidance

Power Integrations expects revenues for the March quarter to be $105 million, plus or minus $5 million, and for channel inventories to continue to come down. Non-GAAP gross margin for Q1 is guided to be approximately 53.5%, driven again by lower manufacturing volumes and a less favorable end market mix. These are not great numbers, but it is worth remembering that this could be close to the bottom of the downturn, and that the company sound optimistic they should start coming out of it soon.

Valuation

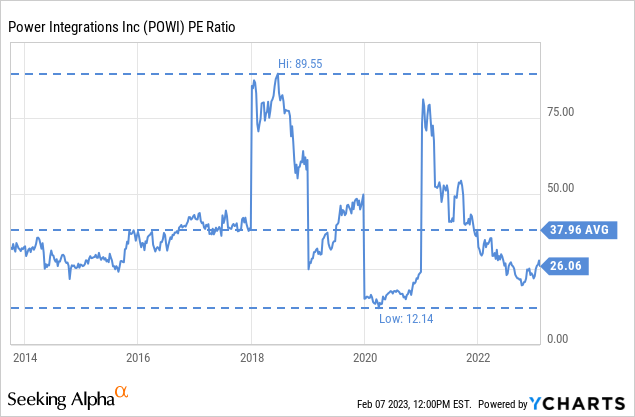

Shares have somewhat recovered since our last article on the company. Still, we still believe there is some value left in the shares. On a trailing twelve months basis, POWI stock’s price/earnings ratio is still considerably below the ten year average.

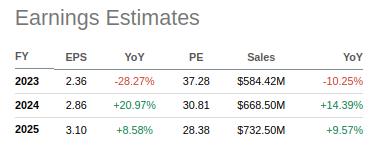

On a forward basis shares look more expensive as 2023 is expected to be a difficult year for the company. The forward p/e is ~37x, and ~30x based on 2024 estimates. No doubt that these are not cheap multiples, but the long term growth opportunity at Power Integrations appears intact. We also believe the company will perform very well coming out of the downturn, as it has been gaining share.

Seeking Alpha

Risks

The biggest risk we see for Power Integrations is a severe recession which would make the current downturn even worse. This risk is mitigated by a very strong balance sheet with a net cash position, and very high profit margins. It is also worth noting that the valuation reflects high expectations of revenue growth in the future, and if growth disappoints shares could drop significantly.

Conclusion

Results for Power Integration’s fourth quarter were not pretty, and neither were guidance. The company is still in the middle of a severe downturn. There are some positives, however, such as the company gaining share and reporting several design wins. We therefore believe investors should look past the current weakness. The long-term growth prospects at Power Integrations appear intact, and that gives us hope that the company will outperform coming out of the downturn.

Be the first to comment