Win McNamee/Getty Images News

The stock market has risen dramatically off the October lows, and despite all of the hawkish comments from Fed officials, the stock market has pushed higher since the middle of October. Jay Powell is taking no chances with the blackout period quickly approaching for the December FOMC meeting. He will speak on November 30 at the Brookings Institution about the labor market and the economic outlook.

This Wednesday may be another one of those moments when Jay Powell has a chance to reset market expectations as he did back at Jackson Hole in late August. In July and August, markets ran sharply higher, easing financial conditions. Now Jay Powell finds himself in a similar spot, with the S&P 500 moving sharply, implied volatility levels falling, and financial conditions easing.

The Fed transmits its monetary policy through forward guidance, quantitative tightening, and interest rates. Together these factors help to either tighten or loosen financial conditions. Immediately following his Jackson Hole speech, financial conditions tightened considerably, but since the October CPI report, financial conditions have eased dramatically.

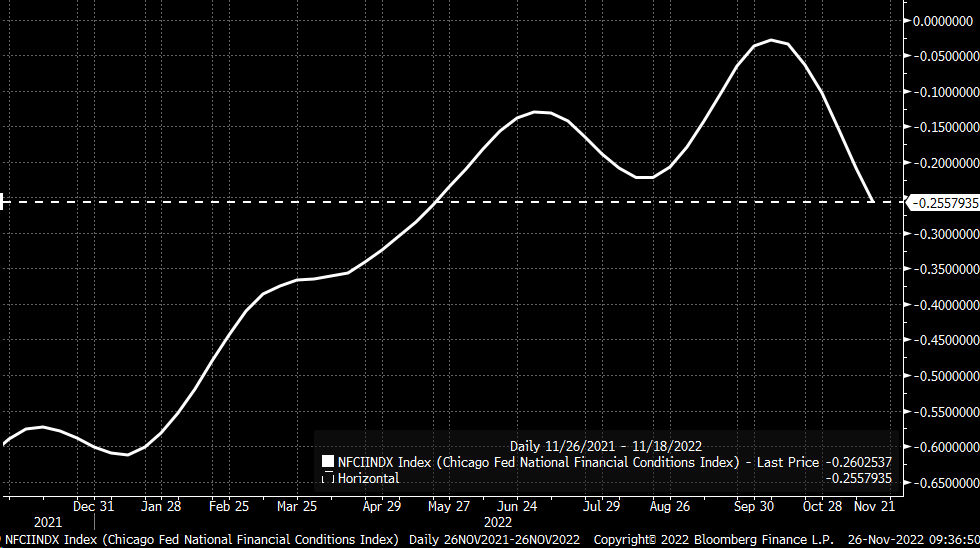

It is a problem for Powell because easing financial conditions work to undo much of the tightening the Fed has done over the past several months. The Chicago Feds National Financial Conditions Index recently dropped to levels not seen since May 20, when the Fed’s Funds rate was just 75 to 100 bps.

Bloomberg

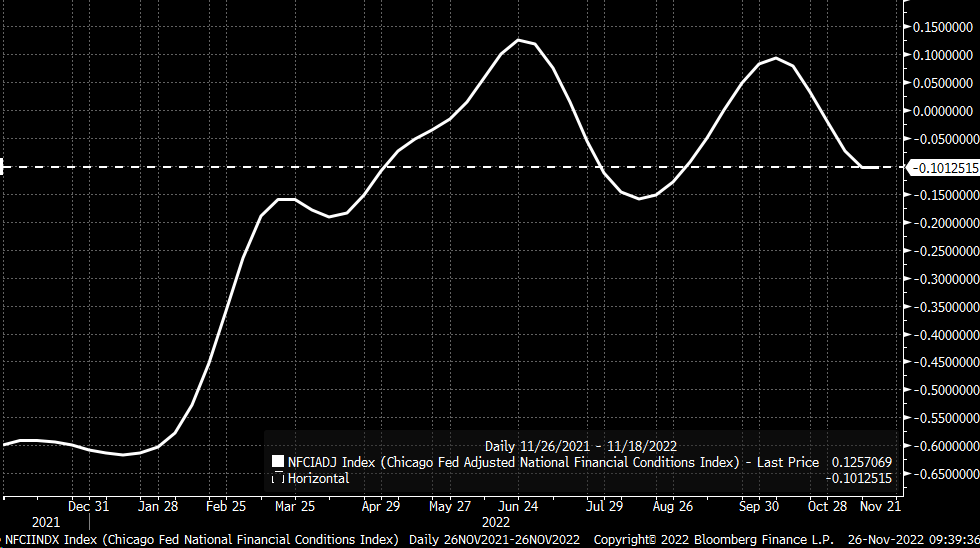

Meanwhile, the adjusted national financial conditions index fell back to levels not seen since September 2, when the Fed’s Funds rate was 2.25 to 2.5% versus its current 3.75 to 4% rate.

Bloomberg

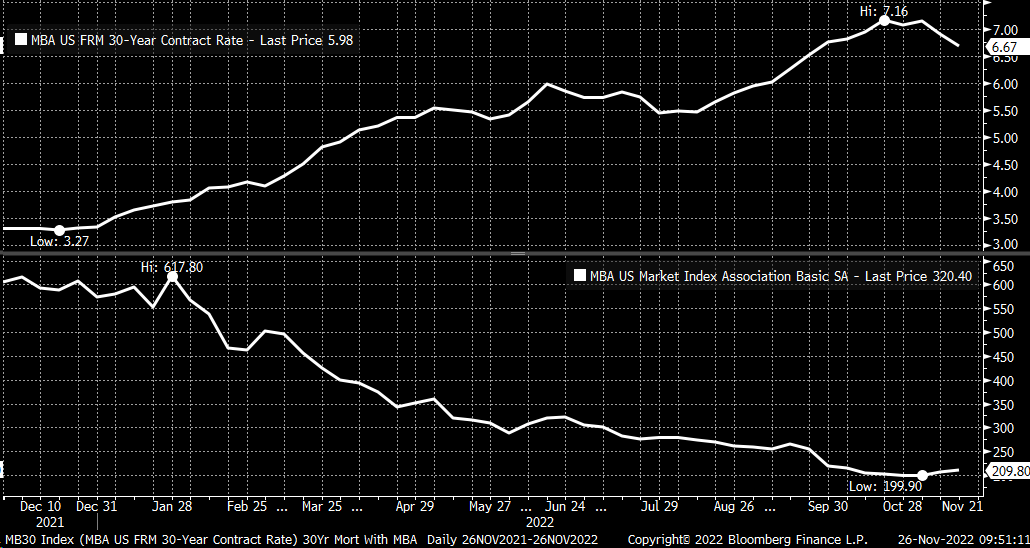

The easing of these financial conditions has real-world effects because the 30-year average national mortgage rate has fallen from 7.16% on October 21 to 6.67% as of November 18. While rates are still high relative to where they may have been 6 to 9 months ago, the falling rate has increased mortgage applications over the past couple of weeks. Should financial conditions in the economy continue to ease, mortgages would likely continue to fall, leading to mortgage applications rising further.

Bloomberg

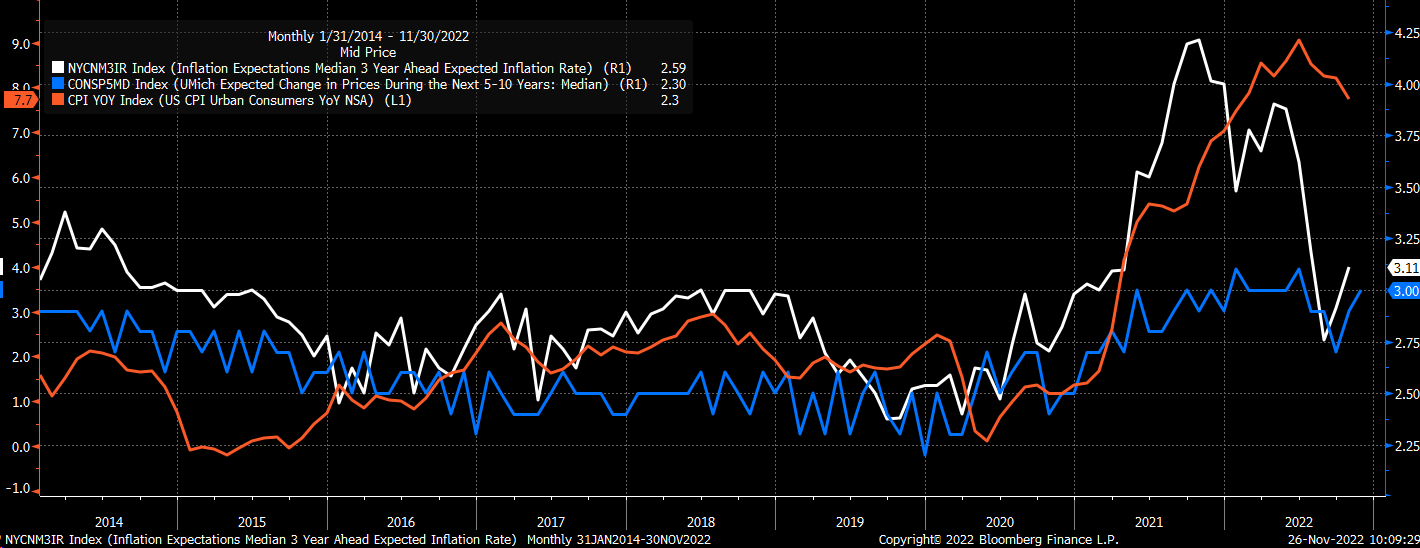

Over this same time, consumer inflation expectations, as measured by the NY Federal Reserve with a 3-year outlook, have increased to 3.11% from 2.76% in August. Meanwhile, the University of Michigan’s 5 to 10-year inflation expectations outlook has risen to 3% from 2.7% in September. Rising consumer expectations could indicate that overall inflation may begin to rise again.

Bloomberg

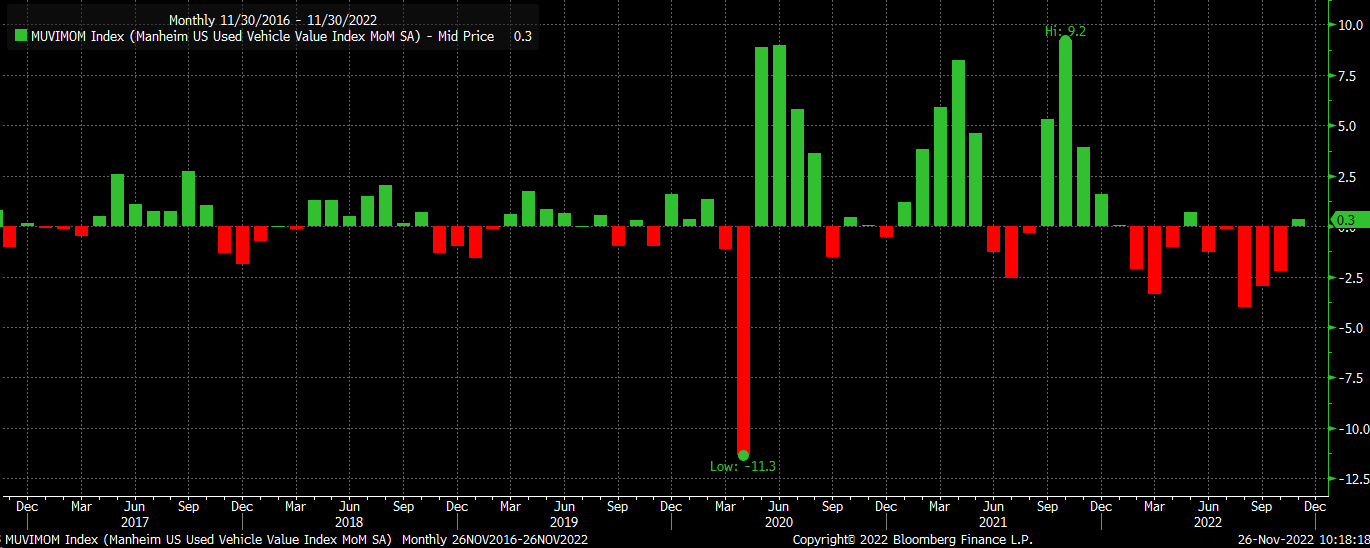

For example, after months of falling, the Manheim Used Auto Index has increased for the first time since June.

Bloomberg

These are just minor samples, but they also show why the Fed can’t let financial conditions continue to ease and need them to tighten again back to October levels and then require them to stay there. On top of that, while jobless claims have started to rise, the number of job openings compared to the number of people unemployed is still very high, at nearly a 2-to-1 ratio. It is still significantly higher than where the value stood before the pandemic at roughly 1.25.

Bloomberg

It is why Powell needs to push back against the recent trends in the market of lower rates, a weaker dollar, lower implied volatility, and higher stock prices. He needs financial conditions to tighten, and he needs them to stay that way to avoid further easing and the undoing of everything the Fed has accomplished this year.

The first step in regaining control was the Fed minutes. Some investors appeared to completely miss the point of the Fed minutes, instead focusing on the known “known” of slower pace of rate hikes. The critical piece of the Fed minutes emphasized that rates were going higher than previously noted at the September FOMC meeting. Meanwhile, the Fed is willing to risk recession if it means beating inflation. Reading the Fed minutes and listening to Fed officials, it seems that rates are destined to exceed 5%.

It seems that rates will get above 5% in 2023. The next step is for Powell to come out and forcefully push back against the recent easing that has taken place by emphasizing the minutes and telling the markets the Fed’s job is far from over and that rates will go much higher until their mission is complete.

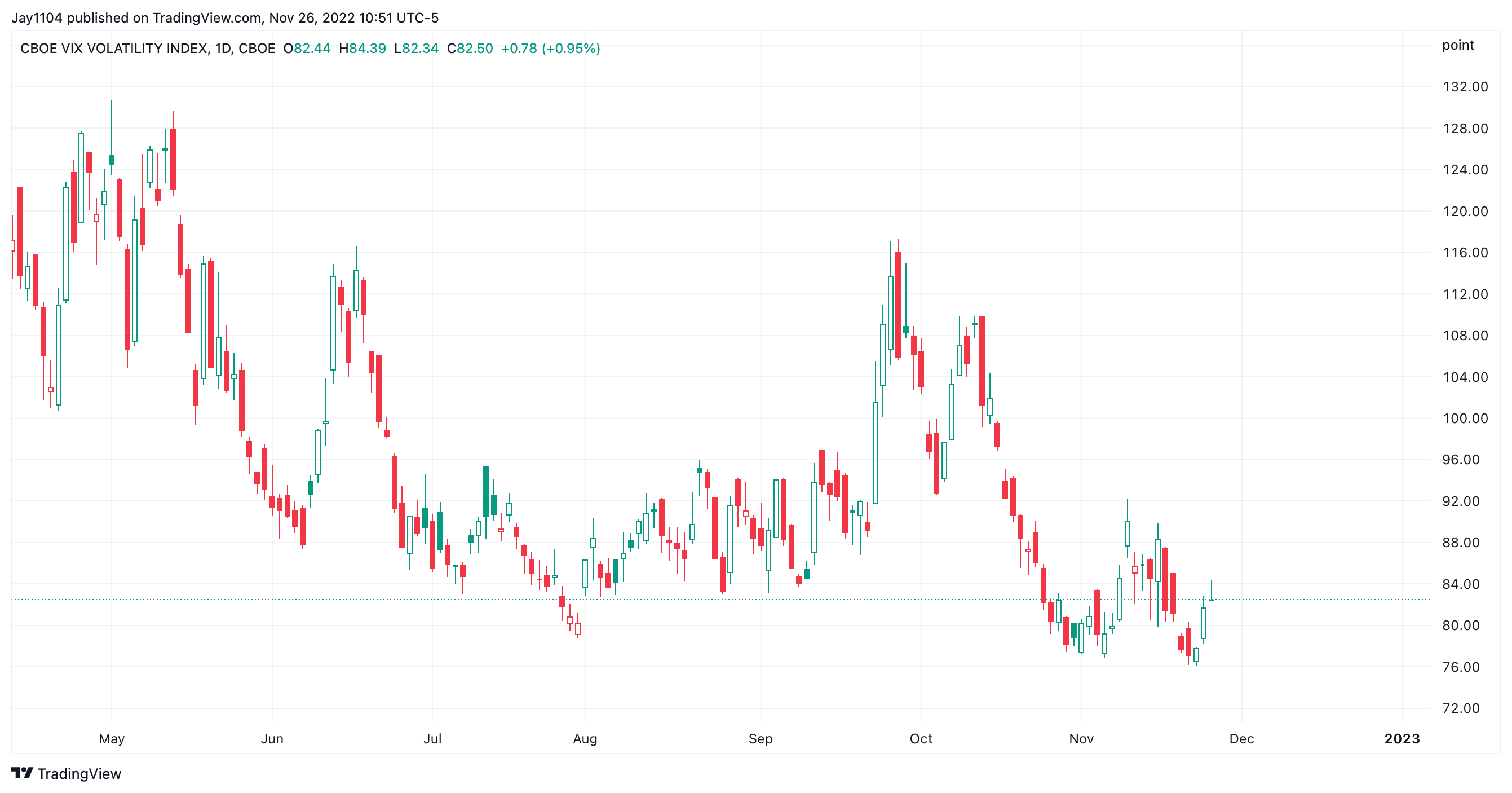

The VIX index has melted since peaking on October 12, dropping from roughly 33 to Friday’s closing value of 20.5. Meanwhile, the S&P 500 has risen from 3,577 to 4,026 over that same time.

But there are signs of market expectations shifting, with the implied volatility of the VIX starting to creep higher, as measured by the VVIX. It is also exceptionally cheap to buy protection and put hedges in place. Since November 22, the VVIX has started to move higher, the first signs of rising implied volatility, and traders are looking to put hedges in place.

TradingView

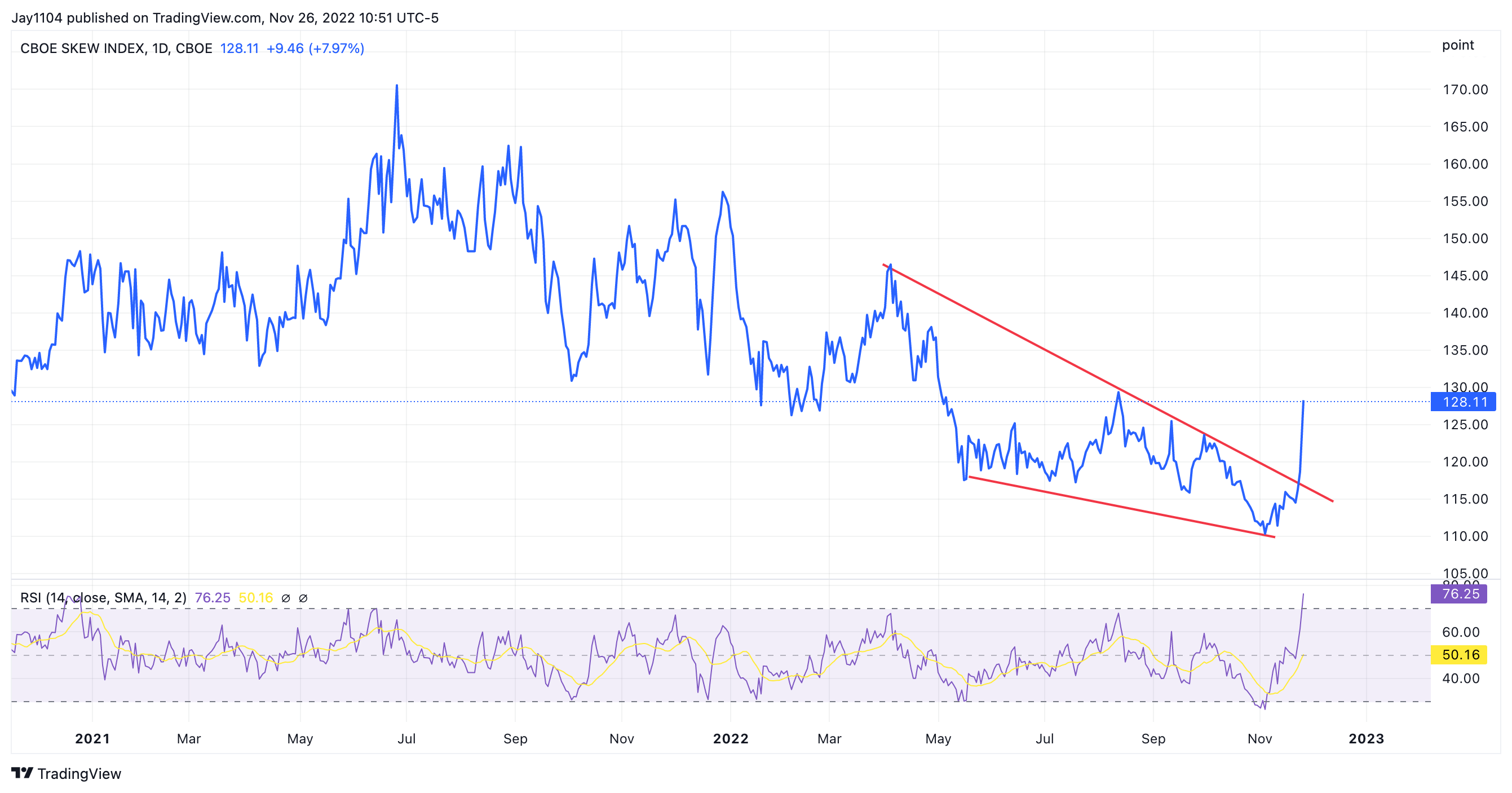

That view is confirmed by the SKEW index, which is now starting to rise after months of dropping. The SKEW index measures out-of-the-money S&P 500 options and is a measure of tail risk. The rising SKEW index is a sign of investors looking to put hedges in places, and why not, given how cheap it is, based on the low VVIX level.

TradingView

Also, the dollar index has fallen to a critical zone of support that, if breached, could lead to even further declines in the dollar. It would be a massive negative for Powell, as a weakening dollar would increase commodity prices and result in import prices starting to rise again. While the Fed doesn’t focus or comment on the dollar, Powell knows that he needs the dollar to strengthen to get financial conditions to tighten further.

TradingView

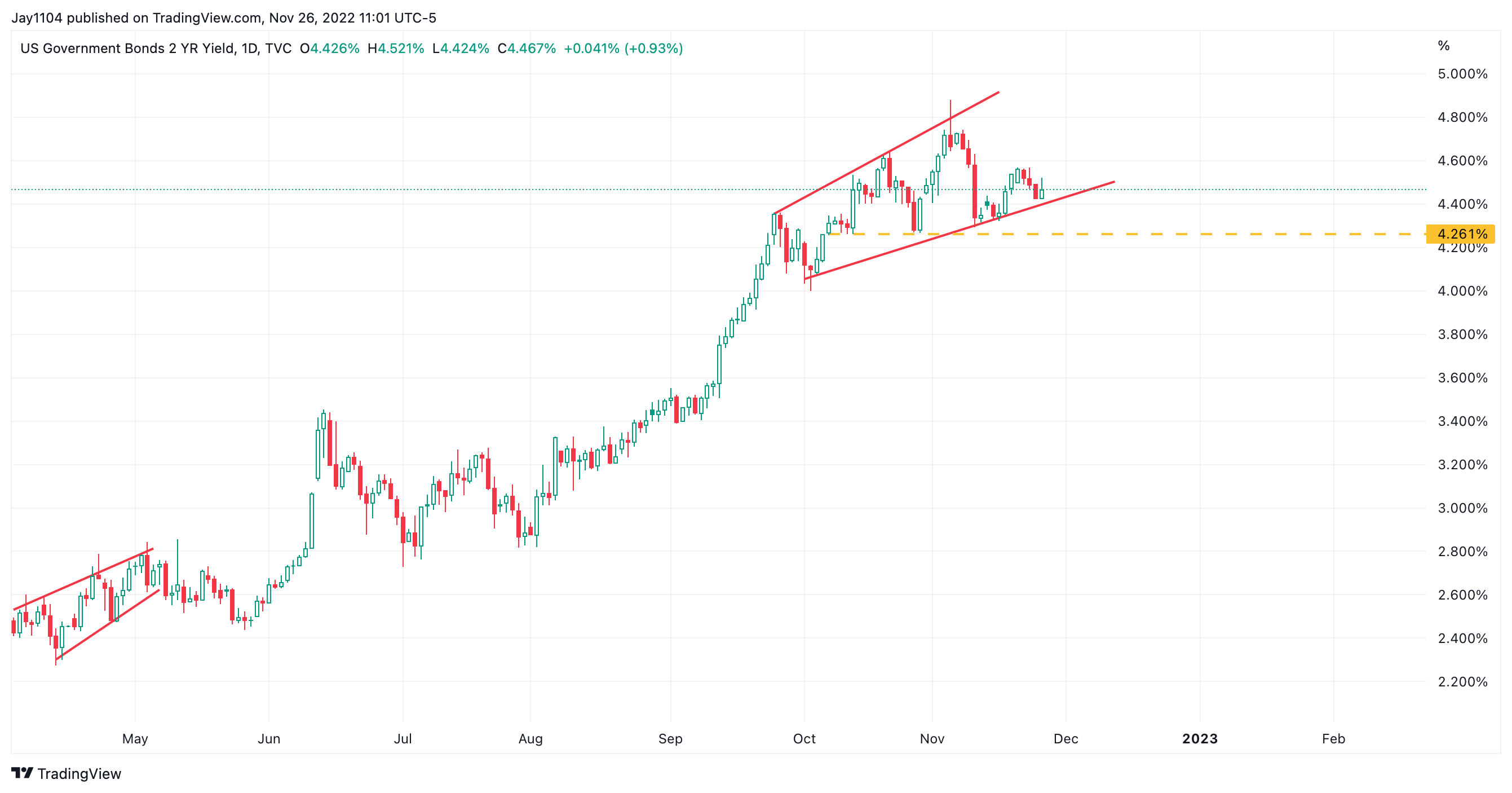

What Powell can do, though, is to move the dollar higher, and he can comment on where rates are likely heading, and he needs to do everything in his power to convince the market that rates are heading north of 5% to help push the 2-year rate higher. The 2-year rate can’t afford to drop below 4.25% because if that happens, it could drop to 4% or even lower, back into the 3% region. The higher he can get the 2-year to move, the more likely the entire curve moves higher with it and the stronger the dollar gets.

TradingView

He also needs to give the market something to worry about, invoking the fear required to push the VIX higher and, as a result, push stock prices down. Falling implied volatility and rising stock prices ease financial conditions. Again, to successfully get financial conditions to tighten, stock prices need to fall, and implied volatility needs to increase.

It is a critical moment for Powell, similar to the Jackson Hole speech. He needs to double down on that speech and tell investors that the labor market is too tight, inflation is too high, and that he will do whatever it takes to get inflation back to its 2% target, no exceptions.

It is a make-or-break moment for Powell because he risks losing control of the markets and his battle on inflation.

Be the first to comment