hobo_018

Main Thesis & Background

The purpose of this article is to evaluate the PIMCO Municipal Income Fund II (NYSE:PML) as an investment option at its current market price. This fund’s objective is to invest at least 90% of its net assets in municipal bonds whose interest is exempt from regular federal income taxes and the fund invests at least 80% of its net assets in bonds that at the time of investment are investment grade quality (or bonds that are unrated but determined to be of comparable quality by PIMCO).

I initiated coverage on PML roughly two years ago and have always approached it cautiously. This was primarily due to the fund’s persistent premium to NAV – something that was on full display when I last reviewed it in June. I was starting to get bullish on munis as a whole, but I cautioned readers against buying PML as an option. In hindsight, that advice was well founded, with the fund sitting in bear market territory since that time:

Fund Performance (Seeking Alpha)

This type of move usually captures my attention and PML is no exception. On the backdrop of heavy losses and an income cut, this fund could continue to be an avoid for many investors. But for those with are able to withstand some short-term volatility, I see potential here. I think the yield, valuation, and muni exposure are all worth a buy on this weakness. I will use this review to explain why I recently purchased this fund, and some risks that should be considered.

The Short-Term News Is Bad, But Presents An Opportunity

Let’s begin with the news most investors are probably aware of after a turbulent trading week within the PIMCO muni family. This was the distribution cut announcement that was limited within the muni funds (the taxable CEFs were not impacted in this round of cuts). These income reductions were relatively expected to come, but the surprise was from how large they were:

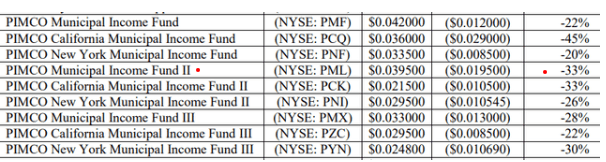

PIMCO Distribution Cuts (PIMCO)

PML in particular saw one of the largest cuts in terms of percent. So it may seem counter-intuitive to be buying a fund now with this recent track record.

In fairness, I would not fault someone for saying this is “not for me”. Buying after distribution cuts often brings its own challenges. But it can also be viewed as an opportunity due to panic selling – which I believe happened in a number of PIMCO’s muni CEFs. In the case of PML, the fund saw a more modest drop around 3% over the past week:

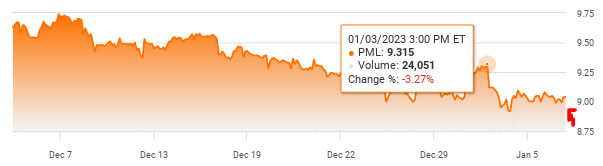

PML Price Action (Seeking Alpha)

So this doesn’t really scream “buy”. But it had been on the decline for a while and – importantly – its current yield is still over 5% even after the 33% income cut. When adjusted for tax savings this remains an attractive income stream:

| New Distribution | Current Share Price | Current Yield |

| $.0395/share | $9.04/share | 5.24% |

Source: PIMCO

My takeaway is two-fold. A distribution drop of this size is not inherently “good”, but we can surmise two key points from it. One, due to its size, I see it as a removal of a key headwind that made me cautious for all of 2022. I was anticipating a cut and subsequent share price decline and now that has happened. Can it happen again in the future? Of course. But I see the size of this one as large enough to limit the possibility of another any time soon. So this shores up my confidence in the short-term.

Two, on a tax-adjusted basis, a yield around 7% is not something to ignore. There are signs inflation has peaked and the Fed may be nearing the end of its rate hiking cycle. This tells me locking in yields of this level will be a move I don’t regret a year or two from now (and longer).

Valuation Story Is Now A Positive

Looking at PML in comparison to its sister funds from PIMCO brings about another important reason why I decided to buy this one last week. After Friday’s close, PML now sits with a premium just a hair about its par value:

Fund Metrics (PIMCO)

Investors may be asking – what is so great about that? On the surface, it may appear to be nothing. After all, there are a plethora of muni CEFs that trade at discounts to NAV, some of them quite large discounts. Further, simply buying (or selling) a fund based on premium/discount to NAV in isolation is not usually warranted. We have to dig deeper than that.

So let’s dig deeper. Of note, PML has a relative valuation edge over both its sister funds, the PIMCO Municipal Income Fund (PMF) and the PIMCO Municipal Income Fund III (PMX). While PMX is not too expensive either, PMF still clocks in near a 6% premium which I think is too rich considering the income cut:

| Fund | Current Premium to NAV |

| PML | 0.11% |

| PMX | 1.45% |

| PMF | 5.61% |

Source: PIMCO

As my followers know, I generally like to buy my muni funds at a discount. So asking what has changed here with PML is a fair question. The premise of it is that PML, while sitting at par, looks cheap compared to both its sister funds but also to its own short-term trading history. Over the past year, the fund has traditionally sat at a double-digit premium. So par value is quite a discount from those levels. Further, the fund has been trading at a single digit premium for a low percentage of the time and has never been at a cheaper valuation than where it sits today:

PML’s Premium Gap (PIMCO)

The conclusion I draw here is PML is finally at a reasonable level. It is “cheap”? Maybe not – that point is debatable. But I personally see these levels offering value in a fund that didn’t have it for a while long time. This supports me taking a bit of a gamble now after watching it for years.

Muni Credit Displays Quality

As we move in to 2023 it could be a year of challenges for both the bond and equity markets. The probability of a recession has increased and that will pressure revenue streams across corporate players and municipalities. This could lead to an increase in defaults or Chapter 9 filings this calendar year, especially if the recession hits sooner or harder than expected.

In this light, readers should manage expectations. I think bonds as a whole display plenty of value after last year’s drop. But that drop was not without merit and the risks should be considered before allocating too large a percentage of one’s assets to this space. Fortunately, I think munis are a good place for that allocation. While delinquencies or defaults may tick up, they should primarily be in the typical troubled sectors like private housing bonds – both assisted living and for profit education, as well as lower quality healthcare and transportation financings (think public transportation in hard hit cities that have still not recovered).

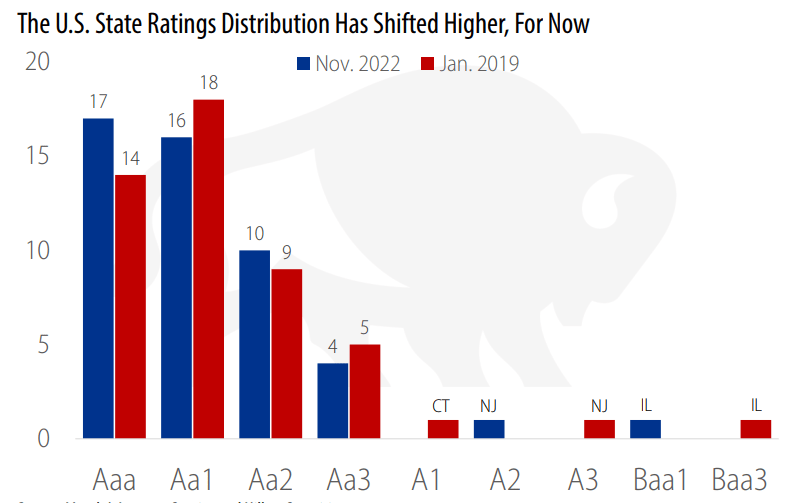

While those risks are evident, the good news is that munis as a whole display a strong credit backdrop. Are there areas to avoid? Yes. But for the most part the underlying bonds have strong ratings, have seen increased revenue streams in 2021 and 2022, and GO bonds (backed by state and local taxes) have low probabilities of default. This story is why credit ratings for U.S. states have actually shifted higher of the past few years, rather than lower, even with the headwind of a pandemic:

State Credit Ratings (Relevant To Muni Bonds) (Moody’s)

What I am doing here is illustrating why I choose munis over other credit areas when calculating where to put my cash. Quality is strong, yields are near historic highs, and the tax savings are enticing. This supports why I am looking at PML to begin with, as well as other CEF options within this space.

Now Let’s Talk Risks, Such As Chicago

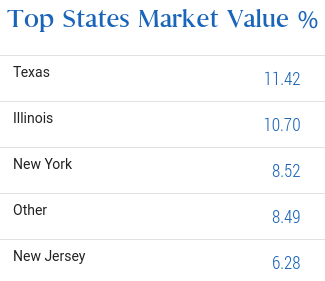

I have been laying the framework for why I like munis and PML. But this is not to suggest this is a risk-free option. I always spend time discussing the risks and “what could go wrong” with any investment thesis or recommendation. I am not a cheerleader or pumper for any stock, sector, or fund – I leave that role to others. In the case of PML, one risk that stands out in a big way is the Illinois exposure:

PML’s Top States (PIMCO)

As the second largest state allocation by weighting, this clearly means PML is exposed to this corner of the U.S. – and that isn’t really a good thing. It does offer some opportunity: as the lowest rated U.S. state the potential yields are higher. So risk-on investors in this space can be compensated for owning it. But the credit rating is lower for a reason (well, multiple reasons), and readers need to take that into account before deciding if this exposure is actually right for them.

Chief among those reasons is the poorly managed public pension fund of Chicago. This has been a sore spot for years, impacting the credit rating and forcing new tax levies across the city over time. Yet, leaders have simply not gotten the message to making meaningful changes. The debt owed by the city continues to rise in what I view as an unsustainable pace:

The Trouble With Illinois (Bloomberg)

There aren’t a lot of great things I can say about this city’s management. I’ve loved it as a tourist, but as an investor this city and state give me some pause. Fortunately, most of my other muni investments (listed in the disclosures section) are void of Illinois exposure. So I feel comfortable enough taking on a fund like PML with a 10-11% allocation here. But I won’t be rushing to amplify this positioning any time soon and I would urge readers to approach this state’s muni debt carefully.

Leverage and Duration Risks Remain

The final points are ones I have harped on many times in the past twelve months so I don’t want to dive into too much detail here. The fact is the Fed’s rate hike cycle is corresponding with investor concerns over economic growth. This has led to both higher short-term rates and a yield curve inversion, pressuring credit investors. This puts upward pressure on borrowing costs in the near term and limits investment opportunities at the longer end of the curve. The result is that long dated and highly leveraged CEFs have come under fire – and we have to look no further than PML to see that. The fund is way down over the past year and has seen an income cut. So the pain is clear.

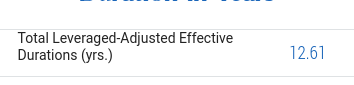

The problem is this story has not gone away. I think we have seen the worst of it, but PML is still highly leveraged and has a high duration metric:

Fund Leverage (PIMCO) Fund Duration (PIMCO)

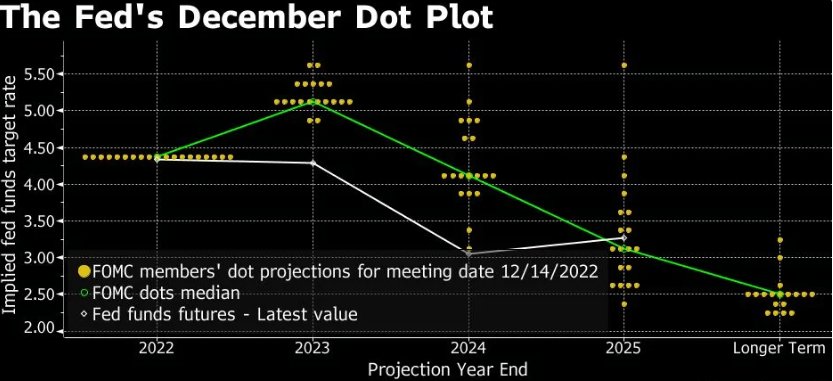

The issue here is the Fed is probably not done raising rates yet. So it would make sense to leave some liquidity on hand in case bond prices keep pushing lower. But the Fed’s most recent “Dot Plot” suggests we are nearing the end of the rate hike cycle. Further, the outlook suggests rates may be on the decline as we near 2024, which is sooner than I would have expected:

Fed Dot Plot (Federal Reserve)

Where I see this going is that bonds are going to be the place to be for the next few years. As rates decline, bonds will push higher, but we can’t wait for that to happen before buying in. It may be a little early to front-run a decline in rates since the next move is probably higher, but we are getting to peak levels near 5%. As we approach, hit, and begin to back off that level, the headwinds for bonds decrease materially. So I am using down days in Q1 and Q2 to add to my positions.

Bottom-line

PML has not had a great finish to 2022, nor a great start to 2023. I see this as an opportunity to buy a fund I have followed for years without pulling the trigger. It now sits right at par value, trades at a lower premium than the other two national muni funds from PIMCO, and sports an attractive yield despite a recent income cut. While risks such as Illinois’ exposure, high duration, and high leverage will all limit gains going forward, I see a positive risk-reward backdrop here. Therefore, I have initiated a position in PML, and I encourage readers to give the idea some thought at this time.

Be the first to comment