Maskot

Main Thesis & Background

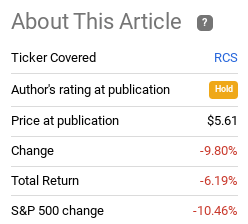

The purpose of this article is to evaluate the PIMCO Strategic Income Fund (NYSE:RCS) as an investment option at its current market price. RCS is a closed-end fund whose objective is “to generate a level of income that’s higher than that generated by high-quality, intermediate-term U.S. debt securities. Its secondary objective is capital appreciation”.

I covered RCS last summer and continued to view it cautiously. The fund’s potential wasn’t enough to get me past the premium to buy-in and I stayed on the sidelines. In hindsight, I must say I was proven correct on this front:

Fund Performance (Seeking Alpha)

With the new year underway, I thought it was time to review RCS once more to see if an upgrade (or downgrade) makes sense. Unfortunately, I still don’t see a buy case for this one. While the high yield will support the share price and limits the downside risk, the broader macro-environment and the high premium to NAV put me off. Thus, I will keep the “hold” rating in place, and explain why in detail below.

It Is Time To Consider Bonds More Broadly

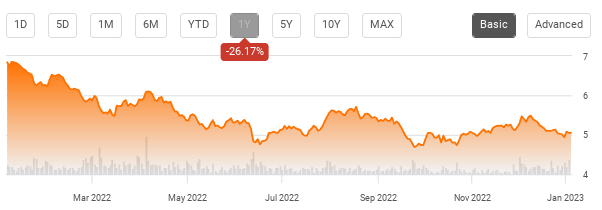

To start I will take a moment to reflect on why I am even giving RCS any attention. The simple fact is that I like to review most asset classes and funds that I cover when we begin a fresh year, but the reality this time around is there is more to it. The backstory is that 2022 was a terrible year for bonds, and CEFs that hold them. RCS was not an exception to this trend. While it only lost 6% since my August review, the story over the past year was worse:

RCS – 1-Year Performance (Seeking Alpha)

These types of drops always cause me to reflect. Such large swings can indicate it is time to build a contrarian position – and that very well may be true for bonds as a whole (and perhaps RCS by extension).

To understand why, let us consider history. Last year was an unusual time for a number of reasons. Thinking strictly of performance, we rarely see such large drops for stocks or bonds as a whole, and hardly ever in tandem! But that is precisely what happened in 2022 – making it an anomaly in historical terms:

Historical Market Performance (World Bank)

The conclusion I draw here is that stocks and bonds both look ripe for a turnaround. History supports this – although very real risks remain on the horizon. For me, bonds may actually offer the better value now if one does expect more market volatility. If stocks come under pressure, bonds may revert back to their typical inverse correlation. Last year can repeat for sure, I will not be blind to this risk. But history suggests that bonds tend to fare well when stocks decline. If one is pessimistic about stocks in early 2023, then bonds could very well be the answer.

RCS Offers Income, But So Do Many Options

Expanding on the discussion above, we have to remember that bonds and other income-generation products are myriad in number. Investors have a lot of options, which is a good thing. So we have the luxury of being bullish on bonds while still being critical of whether RCS does or does not offer value.

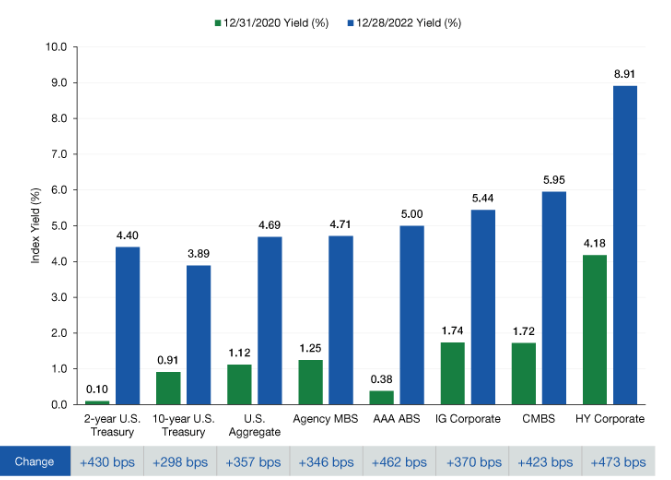

I will dig into the merits of RCS specifically in this review. But before I do so what I want to convey is this isn’t an “RCS or nothing” market. On the surface RCS looks like a great income/yield play. This alone may pique investor interest. But before we get carried away on this fund’s potential, readers should recognize that yields are up dramatically across the board to start the year. If we compare the end of 2020 with the end of 2022, we see that income-oriented investors finally have the upper-hand:

1-Year Yield Differentials (Lord Abbett)

The point I am making is that RCS looks great as an income play on the surface. The fund’s yield sits at 12% – a level that is hard to ignore. But I would temper any enthusiasm for this with two points. One, as the graphic above shows, yields are up across the board so yield alone is not a major differentiator right now. Two, RCS’ yield may very well come under pressure, given its most recent UNII metrics:

UNII Metrics (PIMCO)

The good news is RCS survived the latest round of distribution cuts from PIMCO that were announced this week. The bad news I imagine this is only a temporary reprieve. RCS is likely to see some income pressure in the year ahead and the broader uptick in yields across the credit market suggests this CEF is not one investors need to rush into anytime soon.

I Like The MBS Holdings, But Yield Curve A Headwind For Leverage

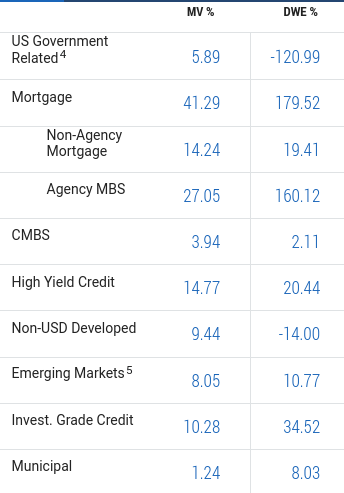

The next question readers may have is why RCS could see an income cut. In this vein, RCS has a bit of a push-pull backdrop. Working in its favor is the heavy allotment of MBS exposure. At over 41% of total fund holdings, this is clearly a fund for those who want to own mortgage debt:

RCS’ Holdings (PIMCO)

In my personal view I actually like this exposure. MBS as a sector seemingly fared poorly in 2022 with a decline, but it was smaller than other riskier debt sectors. In addition, I think there is a real potential for gains in 2023. With the 30-year mortgage rate in the 6.5% – 7.0% range, prepayments and refinancings are going to remain low for the time being. This means the yield offered by those debt securities is less at risk of going away – which is a shift in dynamic from the last few years when rates declined and homeowners rushed to refinance. Investors can lock in current yields that should stay reasonably constant, which are also backed by good credit scores and few delinquencies. So this exposure is an overall positive for RCS, in my view.

This begs the question – what is the problem? The problem for me has to do with leveraged plays in general. This doesn’t matter in the fund buys high yield, MBS, or munis – leverage is going to continue to be a major headline risk in early 2023.

The reason for this is the yield curve remains stuck in an inverted position:

Yield Curve (Bloomberg)

I have discussed this at length in numerous prior reviews so I will keep it short here. But the general takeaway is that an inverted yield curve means that opportunities to invest short-term liquidity into longer-dated positions is limited. So fund managers are borrowing at rates that are rising (thank you, Fed) but have fewer options when it comes to deploying that cash at an advantageous yield spread.

What this does is make me cautious on all leveraged CEFs at the moment. I have to be entirely convinced for other reasons that any such play is the right move in this environment. While I continue to own some leverage, I will be extremely careful with new buys and RCS’ MBS exposure is not enough to make me overlook some of the other issues facing the fund.

Premium Keeps Making Fund A Non-Starter

I will now dig into the key reason why RCS is not on my buy list, despite some underlying positives with the MBS sector. Ultimately, I would be a bull on many fixed-income sectors now – such as corporates, munis, and MBS. And RCS holds many of these assets. But I don’t want to own this exposure at any price. And that is precisely why RCS doesn’t pass the muster for me.

To understand why, consider that the premium to buy RCS on the open market is over 14% the fund’s underlying value. This is expensive by most measures:

Current Valuation (PIMCO)

Suffice to say I am a value driven investor and this fund lacks value. Despite falling into bear market territory, it still sits at a premium well above my comfort zone. For that reason alone, RCS would probably not make it on my buy list until the premium falls to (at least) single digits.

Duration Is Being Managed Properly

So far in this review I have taken a fairly negative tone for RCS. This could make me lean towards “sell” in my rating. However, these are a couple aspects that lead me to believe downside risk is mitigated in the short-term. Chief among them was the yield that I highlighted earlier. At 12%, RCS can afford a distribution cut and still pump out an attractive yield. So that gives the fund some merit straightaway.

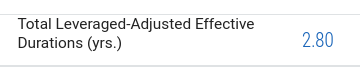

In addition, the duration level of the fund is quite low, especially compared to other PIMCO CEF offerings. At under 3 years, this fund does not have a tremendous amount of interest rate risk:

Duration (PIMCO)

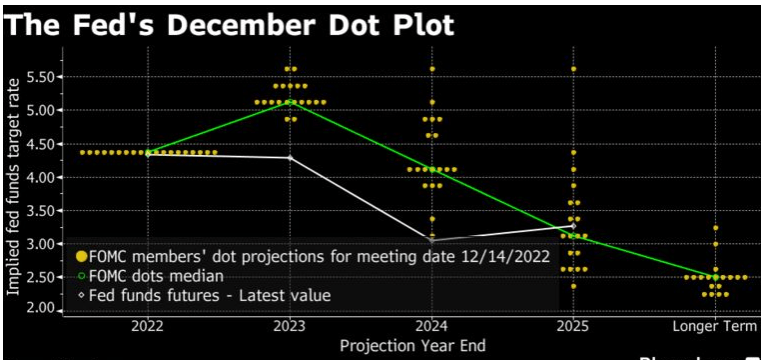

The reason this is a positive is because interest rates remain set to keep rising. Despite market beliefs (or perhaps hopes) that the Fed is going to pump the brakes, the Fed’s “Dot Plot” suggests a continued path higher to the 5% mark:

Fed Dot Plot (Federal Reserve)

The conclusion I have is the Fed is not done hiking, but it is close. They (Fed members) don’t see light at the end of the tunnel yet with inflation, but they are not anticipating going over 5% in their benchmark rate to get there. This means investors can start to ladder into the bond market as rates are near “peak” level. Do we want to go all in now? Absolutely not. But the income opportunity out there in the market today is enough to start positions.

RCS is not my preferred choice to do so, that should be clear. But a managed duration portfolio with rates set to go higher still is one reason why I think there is some merit to keeping an eye on it. For those who are interested in MBS and don’t mind a high premium to NAV, this option could make sense.

Bottom-line

RCS continues to illustrate a mixed bag. The positives are the high yield and the MBS exposure. This is an area – both agency and non-agency – that I think readers should consider in 2023. The supply of new issues should fall this year with higher mortgage rates. It will bring fewer new securities to the market and the higher rates have also eliminated the potential for refinancing (keeping yields constant). This is critical because the Fed continues to taper its MBS holdings, so providing a couple of tailwinds to offset the Fed is important.

However, headwinds remain. RCS is facing an income shortage that could lead to be distribution cut. Further, the premium to NAV is simply too high in this environment. This has limited the attractiveness of this fund in the past and it continues to do so today. Therefore, I believe “hold” continues to make sense, and I would suggest readers approach this fund carefully at this time.

Be the first to comment