Kameleon007

The overall office sector is down over 30% YTD and is the worst performing sector among all real estate investment trusts (“REITs”). Moreover, the outlook appears bleak at first glance. The list of companies downsizing physical spacing needs is long, and there is no shortage of headlines covering the industry’s current plight.

The increasing permanency of hybrid working arrangements lends credence to the secular threats facing many companies operating in the sector. Already, several companies have slashed dividends or announced intentions to do so in 2023.

This includes Douglas Emmett (DEI), who recently cut their dividend by 32%, as well as SL Green Realty (SLG), who reduced their payout by about 13%. Likewise, Vornado Realty Trust (VNO), also announced their intentions to right size their dividend in 2023 due to expectations of lower taxable income.

Investors, perhaps wisely, have fled the sector, which is resulting in lower valuations and an industry-wide pause on new projects.

With so much pessimism baked into the sector, there is what some might say “blood in the water.” And this is precisely why the sector is worth a second look by bottom-feeding investors. Valuations across the board have rarely been this low, even during the worst months of the COVID-19 pandemic. While opportunities abound, Piedmont Office Realty Trust (NYSE:PDM) at current trading levels presents one of the best long-term risk/reward prospects heading into 2023.

Sunbelt-Focused With Strong Tenant Base

About 65% of PDM’s annualized lease revenue (“ALR”) is generated in the Sunbelt region of the U.S. More specifically, Atlanta, Georgia and Dallas, Texas, themselves, accounted for about 45% of ALR as of September 30, 2022.

And looking ahead, the company is targeting a Sunbelt concentration of 70-75% of ALR by the end of 2023.

Elevated exposure to these high growth regions has enabled the company to capitalize on favorable inbound migration trends from both businesses and individuals.

According to the Dallas Observer, for example, Dallas had the fourth highest rate of inbound migration in 2021, with population growth that was nearly three times faster than the national average.

In addition, over 175 new corporate headquarters have moved to North Texas since 2010. Furthermore, the Dallas region presently hosts 22 Fortune 500 companies, including two Fortune 10 companies.

Return-to-office trends in Dallas also outperform benchmark averages. Currently, overall occupancy rates are at 53.7%, which is 550 basis points (“bps”) above the 10-city average of Kastle System’s Back To Work Barometer.

And with regards to Atlanta, the market is a national leader in absorption gains, with about 168K square feet (“SF”) of positive net absorption through Q3, which brings their YTD total through Q3 to 965K SF.

Furthermore, the region boasts of an unemployment rate that is below national averages, which is resulting in an economic surge, led by payroll growth in the professional/business services sectors.

These sectors are also the top industries served by PDM. Collectively, excluding government entities, they represent nearly 40% of total ALR.

Q3FY22 Investor Supplement – Summary Of Top Industries Served By PDM

Exposure to the Legal sector is particularly advantageous to PDM since the industry has one of the highest in-person occupancy rates, at about 65%.

The company’s overall tenant base is also comprised of credit-worthy tenants operating in industries that are generally more likely to favor in-person work. Two of their top tenants, for example, are both the State and City of New York, who together account for about 7% of total ALR.

Given the outbound migration experienced over the past two years due in part to the flexibility afforded by hybrid working arrangements, these two governmental tenants are among the least likely to endorse offsite work. This is for the sake of their own local economies.

Q3FY22 Investor Supplement – Summary Of PDM’s Top Tenants

Strong YTD Operating Performance

At the end of September 30, 2022, PDM’s leased occupancy rate stood at 86.8%. This is still down from the pre-pandemic benchmark, but it is up 90bps from the same period last year.

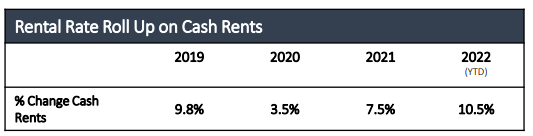

In addition, through nine months of the year, the company has completed over 150 leasing transactions totaling 1.7M SF, with cash roll ups of 10.5%. The positive leasing spread is impressive, considering the multitude of narratives surrounding collapsing demand for office space. Even more impressive is that current cash spreads are higher now than they were in 2019.

November 2022 Investor Presentation – % Change In Cash Rents By Year From 2019 To 2022

Average lease terms also continue to hold firm at about 6 years. If offices were truly facing an existential crisis, it’s unlikely tenants would be committing themselves to long-range leases.

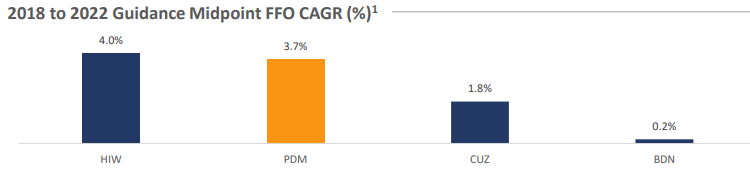

As the robust leasing activity continues, PDM is still delivering on their strong track record of growth in core funds from operations (“FFO”). From 2012 through 2022, for example, core FFO guidance has grown at a compound rate of 3.5%, with 3.7% growth from 2018 to 2022. This outpaces the growth rates of related peers, Cousins Properties (CUZ) and Brandywine Realty Trust (BDN) and is just shy of the growth rate reported by Highwoods Properties (HIW).

November 2022 Investor Presentation – Comparative Summary Of FFO Growth From 2018 To 2022

Prime Beneficiary Of Tenants Seeking Quality Office Space

In future periods, more offices are likely to close or be converted to alternative uses. Further downsizing is also likely by those seeking to attract and retain talent or to minimize costs in a challenging operating environment.

Among the first casualties of these secular threats would be owners of lower quality properties in unappealing locations. These would be primarily Class B and C properties.

Class A properties, however, are likely to benefit at their expense, as those tenants that do still need space will likely increasingly turn to the highest quality properties in desirable locations with enticing amenities.

Over the longer-term, these higher quality properties are likely to be in short-supply due to the current pullback in sector investment. This will be supportive of both rents and occupancy. The Sunbelt region of the U.S., in particular, is likely to remain a prime beneficiary due to favorable economic tailwinds.

Numerous Levers For Future Growth

As it is, rents in PDM’s portfolio are already 5-10% below market rates. And in their most recent trophy acquisition, 1180 Peachtree Street in Atlanta, GA, rents are currently 20% below market values. This is also the case with a separate value-add acquisition at 999 Peachtree Street.

Capturing the embedded upside is also possible due to their smaller lease and tenant size. This provides PDM with greater negotiating power at the time of renewal.

One example of this in action is their recent renewal of Ryan LLC, a top 20 tenant that was recently renewed at double-digit spreads. This heavily skewed their overall reported Q3 cash rollups, which came in at a topline 33.1%. But excluding the Ryan renewal, the roll-up would have been 9.9%.

In addition to the embedded mark-up opportunities, PDM also has attractive leasing opportunities that are primarily concentrated in the Sunbelt region. 71% of available vacancy, for example, is in the Sunbelt, with 60% of their 2023 expirations also located in the region.

Moreover, of their total leases up for extension in 2023, just one is over 100K SF. The remaining expirations average just 8K SF. Again, the smaller space size has typically provided greater leverage to PDM in negotiations. So spreads are likely to hold up at healthy levels in the new year as these renewals are completed.

Anchored By A Largely Unburdened Balance Sheet

Furthermore, since 2020, PDM has been relocating more of their portfolio from the northern regions of the country to the Sunbelt. Most recently, they disposed of two properties in Massachusetts and used the proceeds for deleveraging purposes.

The added liquidity, which now includes the full +$600M availability on their revolver, could now be used to fund further opportunistic acquisitions, similar to their recent trophy acquisition of 1180 Peachtree Street.

With ample liquidity that is further supported by a manageable debt profile, PDM has a well-positioned and credit-worthy balance sheet that should provide comfort to investors.

And for income investors, their current dividend payout represents just 42% of core FFO, which signifies a high degree of safety, considering the sector average is about 65%.

The Bottom Line

PDM owns a portfolio of Class A properties occupied by credit-worthy tenants with a weighted average remaining lease term of over 5 years. As a pivotal operator in one of the most attractive markets in the country, Atlanta, GA, the company is poised to capitalize on any turnaround in sentiment surrounding offices.

Recently, the company disposed of two properties in Cambridge, MA, for total proceeds of +$160M. Together, these two properties represented about 2.4% of ALR as of September 30, 2022. Assuming that is a fair estimate of their share of total accrual-basis portfolio NOI, one can reasonably surmise that the disposition was completed at an implied cap rate of 5.1%.

For perspective, PDM is currently trading at an implied cap rate of about 10%, which appears way out of line, considering their recent disposition cap rate. In addition, their current implied rate is well below real-estate research firm, CBRE’s, forecasted rates of 5%-6% for 2023.

Even at an implied cap rate of between 7% and 9%, PDM would have an estimated target price between $13/share and $22/share. That would represent upside of over 40% on the low end and a whopping 145% return on the high end.

While some would scoff at that upside potential, it’s worth noting that at those prices, shares would command a forward multiple of FFO of just 6.5x and 11.0x.

At the high end, that would still be less than the 12.6x multiple they commanded at the end of 2019. And this return potential excludes the returns from the dividend payouts, which are currently yielding over 9.5% at current pricing.

For bottom-feeding investors, the upside in PDM is simply too lucrative to miss out on.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Top 2023 Pick competition, which runs through December 25. This competition is open to all users and contributors; click here to find out more and submit your article today!

Be the first to comment