constantgardener/E+ via Getty Images

Note: all dollar values in this article are in Canadian dollars.

Pembina Pipeline Corporation (NYSE:PBA) wrapped up a successful 2022. The company is set to generate approximately $3.65 billion in Adjusted EBITDA, 6.3% above 2021’s $3.43 billion and 5.8% above management’s initial guidance of $3.45 billion.

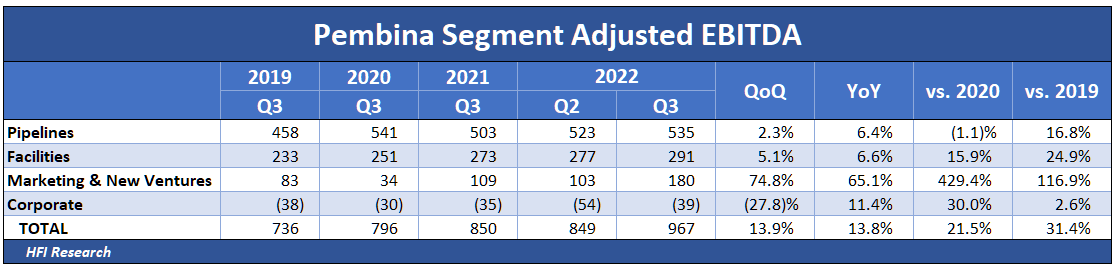

Its most recently reported third quarter results beat analyst Adjusted EBITDA expectations, reporting $682 million of Adjusted EBITDA versus consensus expectations of $674 million. Third-quarter Adjusted EBITDA grew by 14% from the previous year, and Adjusted EBITDA increased in every operating segment, as shown below.

Pembina, HFI Research

Pembina Pipeline Corporation management also raised full-year 2022 guidance for the third time in as many quarters.

Throughout 2022, PBA’s outperformance was driven by its commodity price exposure, which enabled its marketing division to profit from increasing oil, natural gas, and NGL prices and wide price differentials. Pipeline segment Adjusted EBITDA also outperformed due to higher rates that were attributable to inflation escalators in PBA’s service contracts.

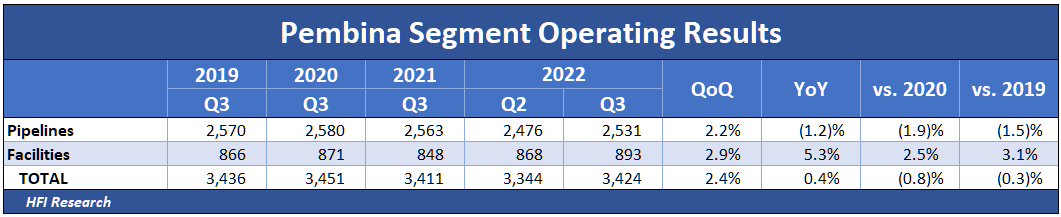

Volume performance was less impressive than its financial performance. Third-quarter pipeline throughput volumes fell by 1.2%, primarily due to declining volumes on PBA’s Ruby and Nipisi Pipelines. The Facilities segment registered a stronger performance, growing volumes by 5.3% from year-ago levels.

Pembina, HFI Research

On the capital allocation front, in November, PBA increased its dividend by 3.6% over the prior year. As of the end of the third quarter, it had repurchased 6.3 million shares for $288 million and was on its way to meeting management’s $350 million repurchase target for 2022.

PBA also achieved a significant operating milestone in the third quarter with the closing of its PGI natural gas processing joint venture. The joint venture is 60% owned by PBA and 40% owned by KKR & Co. (KKR).

Looking ahead to 2023, PBA’s throughput volumes are set to improve, as its Ruby and Nipisi pipelines won’t be a drag as they were in 2022. In fact, PBA’s Nipisi pipeline could turn from an operational headwind to a tailwind. Management is considering reactivating the pipeline to service the rapidly growing Clearwater play.

Unfortunately, the benefit PBA gains from higher volumes will likely be offset by weaker results from its marketing division amid anticipated lower commodity prices in 2023. Overall, we’re expecting low-single-digit Adjusted EBITDA growth from 2022 levels.

The Most Conservative Canadian Midstream Alternative

Pembina Pipeline Corporation benefits from its exposure to growing oil and natural gas production in the Western Canadian Sedimentary Basin (WCSB), with a dominant midstream presence in the Montney and Duvernay plays. Its PGI natural gas processing joint venture possesses significant operating leverage, so it can increase processing volumes with minimal incremental capex. It also has multiple growth projects underway, including its Empress Cogen Facility, Peace Pipeline expansion projects, and its fourth fractionator at its Redwater NGL complex. PBA’s Cedar LNG facility—which is now in the planning phase—could expand the reach of its system by integrating natural gas export capabilities.

PBA is managed more conservatively than its larger peers, Enbridge (ENB) and TC Energy (TRP). ENB and TRP have net debt levels that exceed their Adjusted EBITDA by 4.5-times, which is on the high side for large North American midstream operations.

While it is generally accepted that Canadian midstream majors can run with higher debt loads due to their entrenched market positions, their leverage could pose a problem over the long term if the billions of dollars they spend annually on growth capex don’t generate attractive returns on capital. Both TRP and ENB outspend organic cash flow to invest in projects that offer returns on capital in the mid-to-high single digits.

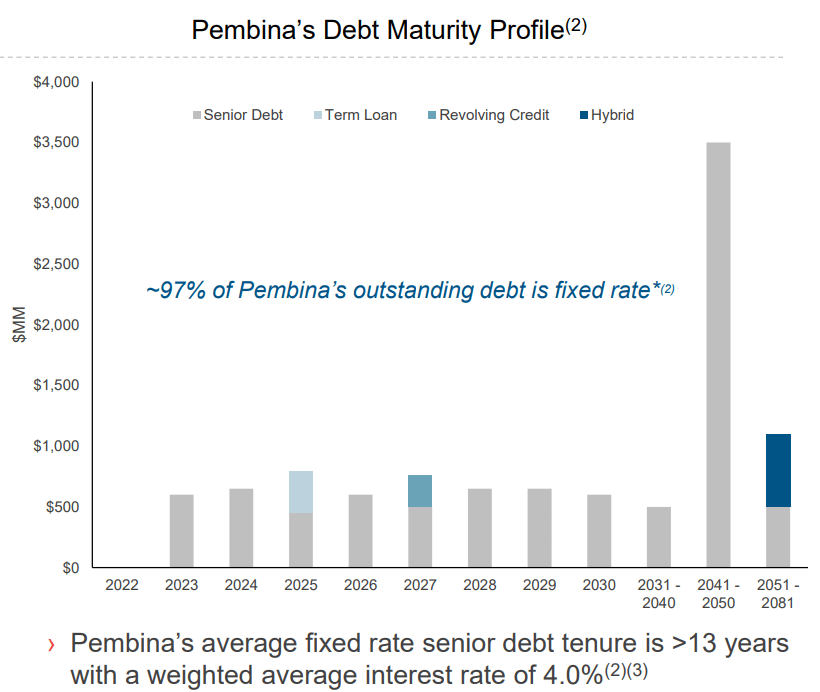

By contrast, PBA’s leverage ratio for the past four quarters is a far more conservative 3.5-times. It has a manageable maturity schedule, as shown below. It also has a lower cost of debt than its peers, with a weighted-average interest rate of 4.0%.

Pembina

Source: PBA December 2022 Investor Presentation.

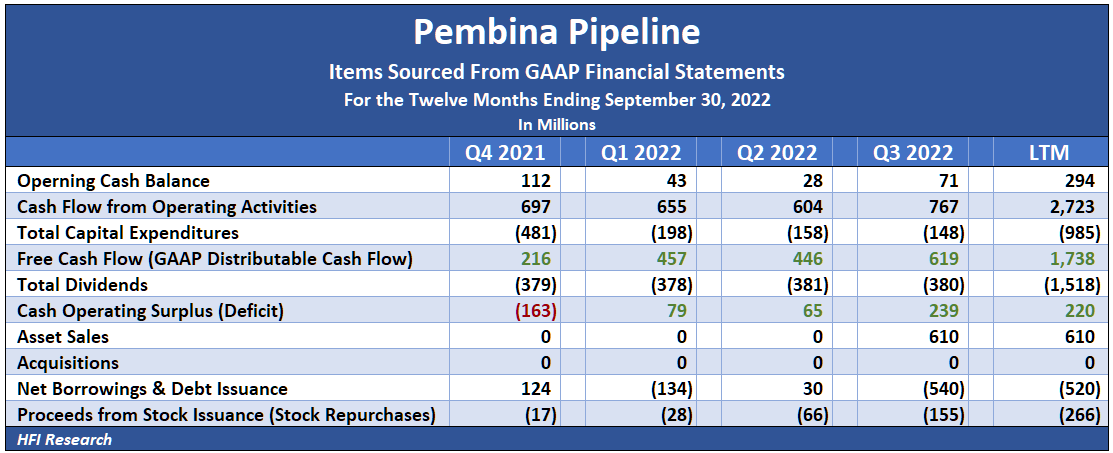

Unlike TRP and ENB, PBA has generated a cash flow surplus over the past few quarters, which it allocated to repurchasing shares and paying down debt.

HFI Research

PBA’s Shares Trade at Fair Value

Over the next few years, we expect PBA to generate low-to-mid single-digit growth. We expect its dividend to increase at a similar rate. Shareholders should note that in 2023, the company will convert to paying its dividends quarterly instead of monthly.

We expect PBA to maintain its conservative financial profile, with its leverage ratio remaining well below 4.0-times.

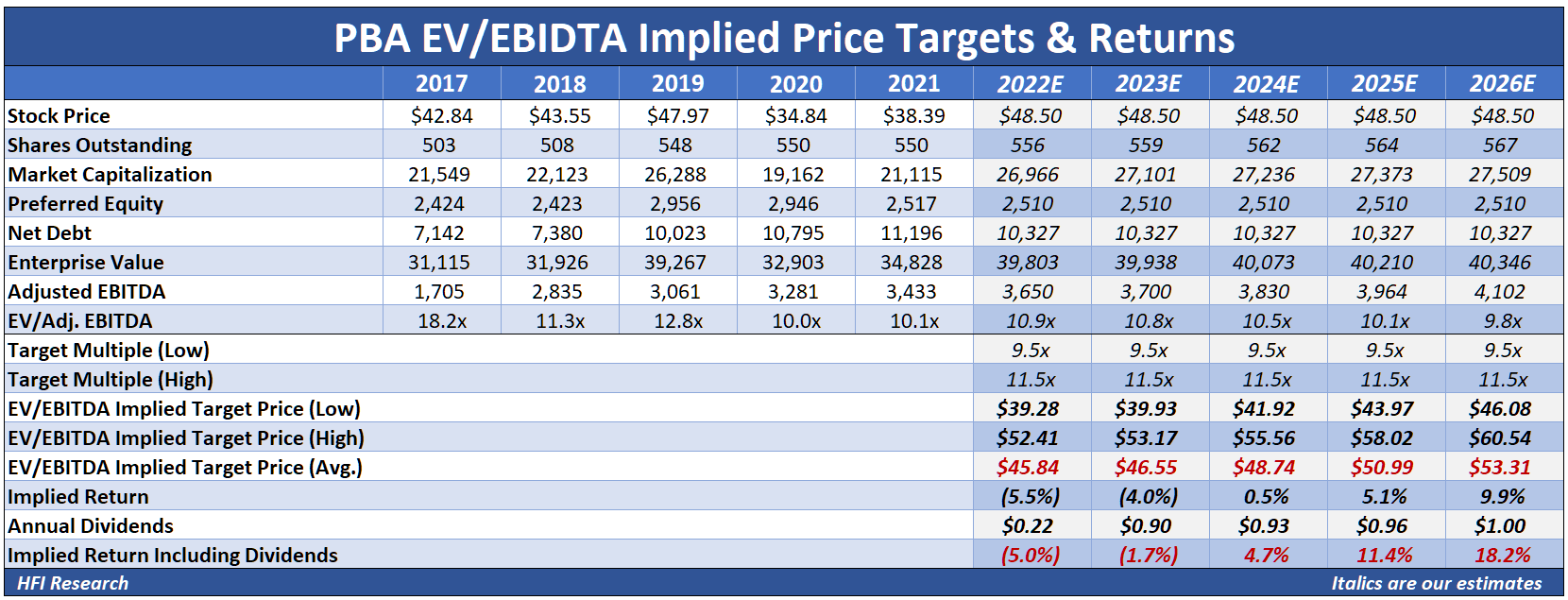

Our EV/EBITDA valuation implies that the shares are trading in the range of value. Over the next four years, our valuation implies PBA shares have 18.2% total return upside. While this is lower than the upside potential of TRP, it is also lower risk from both operational and financial perspectives.

HFI Research

With Pembina Pipeline Corporation shares trading at fair value, we would argue that dividends offer a better way to return capital than repurchases.

Due to Pembina Pipeline Corporation’s financial strength, operational stability, high-quality management, and exposure to production growth, its equity is as safe as ENB and safer than TRP. The tradeoff for PBA’s stability is a lower dividend rate. PBA shares trade at a 5.6% dividend yield, while ENB and TRP shares both trade at a 6.4% and 6.3% dividend yield, respectively.

Conclusion

Owners of Pembina Pipeline Corporation equity can sleep well knowing their equity and dividend is among the safest in North American midstream. Its peer TRP is at risk of overextending itself from its overspending, as we reported here. ENB offers a higher yield, but it also fails to cover its dividend with free cash flow, pursues aggressive growth at middling returns, and takes on a growing debt load quarter after quarter. Its equity value and dividend are, therefore, at modestly higher risk.

By contrast, Pembina Pipeline Corporation’s dividend is well covered by free cash flow. With a much more conservative financial profile, we believe income-seeking equity investors who prize safety above all else should go with Pembina Pipeline Corporation for the long term.

Be the first to comment