Joe Raedle/Getty Images News

This article was prepared by Shahmi Anas in collaboration with Dilantha De Silva.

When Peloton Interactive, Inc. (NASDAQ:PTON) stock plummeted to $30 last February, we thought that investors should ignore PTON despite rumors of a potential deal by a tech giant to acquire the company. With stocks suffering this year due to a myriad of macroeconomic and geopolitical concerns, Peloton stock has continued to lose ground, not surprisingly. There’s no denying that Peloton, a true pandemic winner, looks attractive on paper with its tech-friendly product offering. For this reason, we will revisit our thesis for Peloton to identify any potential inflection points.

Rough Workout for Peloton Since Early 2021

Peloton Interactive has seen share prices take a dramatic nosedive ever since peaking at an all-time high of over $160 in January 2021. The company found itself on the right side of the COVID-19 pandemic, with people having no choice but to spend a considerable amount of time within the confinement of their homes. This resulted in Peloton witnessing exponential growth on the back of a demand surge for home exercise equipment. However, the company took on more than it could handle, and this bled into serious reputational damage as downstream supply chain failures started to emerge. Customers started complaining of delays and missed deliveries, and to add salt to Peloton’s wounds, an incident involving an accidental death of a child on a Peloton treadmill pushed the company to recall and halt the sale of bikes temporarily.

With vaccines widely available and gyms reopening, Peloton has struggled to sustain the hyper-growth it experienced. It would not be a harsh judgment to state that Peloton misinterpreted the pandemic bubble to be the new normal. During the stages of its demand surge, the company invested heavily in excess capacity to enter new verticals such as fitness equipment for hotels and spas, and today, finds itself grappling with serious working capital problems as most of its cash is tied up in inventory.

Measures to Revive Fundamentals in Place Under New Leadership

Peloton Interactive’s overall fundamentals paint a concerning picture. Based on its most recent earnings release for Q3 2022, free cash flow came to -$746.7 million, compared to -$204 million in Q3 2021. Moreover, revenue has continued to fall (24% decline year-on-year in Q3 2022, and 15% quarter-over-quarter), along with widening bottom-line losses. Over the first three quarters of fiscal 2022, the company has reported a $1.5 billion loss from operations compared to net income from operations of $114 million during the comparable period of fiscal 2021.

Peloton’s business is a sum of multiple parts. Along with the exercise hardware, the company also sells an ongoing subscription service that unlocks content and features for its hardware. Connected-fitness subscribers (who own both the hardware and the associated subscription services) get automatic access to Peloton’s exercise app. The company has now repositioned itself strategically under the management of new CEO Barry McCarthy with the exercise app available for separate download even for those who do not own Peloton hardware. Peloton hopes to be able to upsell hardware and hardware-associated subscription services over time to app subscribers, who can enroll for a very affordable fee of $12.99 a month + taxes, compared to the hardware-associated subscription of $44 + taxes. In its Q3 2022 letter to shareholders, McCarthy stated Peloton’s management was “rethinking the value proposition” of their digital apps to drive marketing funnel growth. The company has also introduced a Fitness-as-a-Service program, a rental program that combines the cost of connected fitness hardware and all-access subscription service into one low monthly fee.

The most recent segmental numbers of the business also help to understand the direction the company is moving in. Peloton’s connected fitness products revenue (i.e., hardware exercise equipment) fell 42% year-on-year in Q3 2022, and 25% quarter-on-quarter owing to declining demand after the pandemic bubble. Gross profit of connected fitness products over the same period fell drastically by 123% year-on-year and 233% quarter-on-quarter, owing to big-time price reductions of hardware equipment to boost sales. On the other hand, subscription-based revenue saw impressive YoY growth of 55% in Q3 2022, with gross profit also up by 63%. With a shift in the business model, these numbers give hope that Peloton is not done yet although there is a long way to go to come out of the woods.

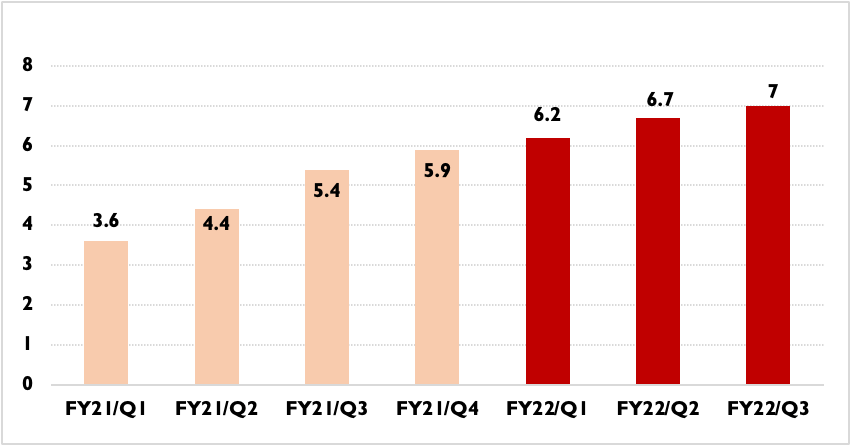

Ever since going public, the total member base of Peloton has seen steady growth every quarter, which is expected to continue in the future, albeit at a slower pace (see exhibit 1). On top of this, Peloton has always maintained a remarkably low subscriber churn rate. In Q3 2022, the company saw net average monthly churn stay more or less the same compared to the previous quarter (0.79% vs. 0.75%).

Exhibit 1: Peloton total members

Company filings

Peloton has also managed to raise $750 million in debt in order to manage its cash flow issues. As highlighted in his letter to shareholders, this was one of McCarthy’s priorities, where he laid out a target to achieve positive free cash flow in the fiscal year 2023. To further expand on this, initiatives such as cost savings of $550 million along with a plan to improve the run rate of the $1.4 billion inventory levels are what the management has planned to devote much of their efforts in the short run.

Takeaway: Should Peloton Investors Cut Losses or Double Down?

With share prices still heading downwards and currently alternating back and forth between single and double digits, we believe Peloton stock has the potential to attract the attention of growth investors to its turnaround plans as it presents itself as an undervalued stock. With the focus now shifting to a subscription-based business model that has given some early promises, we would not be surprised if current shareholders double down at these prices in the hopes of seeing better prices in the coming years.

With the global connected fitness industry expected to grow, the recently adopted refined strategies could open up doors for the company to capitalize and possibly get ahead of the competition. The company’s cash constrictions have also temporarily eased up with the recent influx of $750 million, giving Peloton some breathing space to account for any upcoming losses and infuse stagnant working capital.

As mentioned earlier, the biggest underlying issues with Peloton are its idling hardware inventory worth $1.4 billion and negative free cash flow. Peloton, in our opinion, needs to find ways to spur demand for its exercise equipment to come out of these challenges, which is no doubt going to be an uphill ride considering more people are now returning to gyms, and stiff competition is also emerging in the connected fitness market. One way to deal with this is to funnel app and rental subscribers to buying hardware, and to do this, Peloton will have to offer them at reduced prices as they are doing today. This, in turn, will continue to put pressure on the profit margins of the company. As growth investors, we are wary of investing in companies that find it difficult to expand profit margins in the long run, and for now, we do not see how Peloton could sustainably address the current challenges without shooting itself in the foot.

Despite some improvements in Peloton’s story and our expectations for the long run, we will remain on the sidelines for now until we have a clearer picture of Peloton’s turnaround story. That being said, we do not plan to wait until it’s too late to act, so stay tuned for our next article on Peloton.

Be the first to comment