bymuratdeniz

PDC Energy (NASDAQ:PDCE) is projected to generate $1.075 billion in free cash flow in 2023 at current strip, before the potential impact of cash income taxes. It put more than expected towards share repurchases in 2022, while declaring a smaller special dividend than I had anticipated. If that focus continues, PDC may end 2023 with a share count in the low-80 millions.

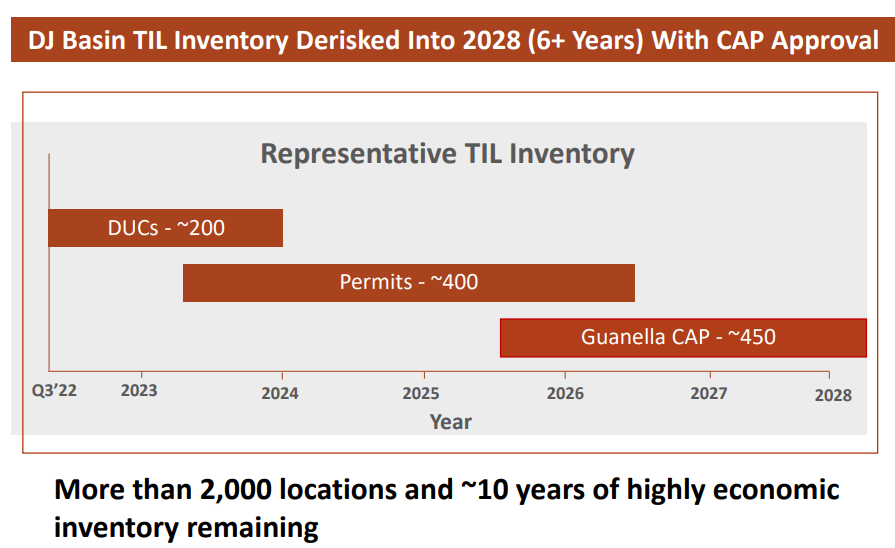

PDC received approval for its Guanella Comprehensive Area Plan [CAP] and now has line of sight for DJ Basin development activities into 2028. With that approval, I now estimate PDC’s value at $75 to $81 per share in a long-term $70 WTI oil environment.

Return Of Capital To Shareholders

PDC announced a $0.65 per share special dividend in December 2022 in addition to its regular quarterly dividend of $0.35 per share. It appears to be focusing more on share repurchases than dividends though.

PDC has committed to returning 60+% of free cash flow (after base dividends) to shareholders. It had previously forecasted $675 million to $725 million in share repurchases during 2022, which would leave close to $2 per share for special dividends assuming $1 billion in total returns to shareholders (including approximately $125 million for base dividends).

PDC ended up spending approximately $820 million on share repurchases in 2022 to repurchase approximately 12.1 million shares. Thus approximately 82% of its total 2022 return of capital to shareholders went to share repurchases and 18% went to dividends compared to its prior forecast for approximately 70% to share repurchases and 30% to dividends.

Regulatory Approvals

PDC Energy received unanimous approval of its Guanella CAP in December 2022 from the Colorado Oil and Gas Conservation Commission [COGCC]. This was a major boost for PDC as the Guanella CAP involves approximately 450 wells, which would be around three years’ worth of DJ Basin development inventory.

PDC indicates that it now has a line of sight into its DJ Basin turn-in-line inventory that lasts into 2028 at current activity levels. PDC’s DUCs, permits and Guanella CAP cover a bit over half of its roughly 2,000 remaining identified DJ Basin locations.

PDC’s DJ Basin Inventory (pdce.com)

2023 Outlook

I am modeling PDC’s 2023 production at 255,000 BOEPD, including 83,000 barrels of oil production per day. PDC expects modest production growth in 2023 from 2H 2022 levels. PDC’s production growth compared to full year 2022 would be higher due to the Great Western acquisition that closed in May 2022.

Current strip for 2023 is now around high-$70s WTI oil along with Henry Hub natural gas prices that are a bit over $3. At those commodity prices, PDC is projected to generate $3.432 billion in revenues before hedges. PDC’s 2023 hedges have around negative $100 million in estimated value at current strip.

PDC’s hedges (not including basis hedges) cover approximately 52% of its projected 2023 oil production and around 32% of its projected 2023 natural gas production.

|

Barrels/Mcf |

$ Per Barrel/Mcf (Realized) |

$ Million |

|

|

Oil (Barrels) |

30,295,000 |

$77.00 |

$2,333 |

|

NGLs (Barrels) |

27,309,300 |

$25.00 |

$683 |

|

Natural Gas [MCF] |

212,824,200 |

$2.00 |

$426 |

|

Hedge Value |

-$100 |

||

|

Total Revenue |

$3,342 |

PDC’s capex budget for 2023 is estimated at $1.4 billion. This is a roughly 10% increase from 2022 (at $1.075 billion plus $200 million for a full year of Great Western capex).

|

$ Million |

|

|

Lease Operating Expense |

$279 |

|

Transportation, Gathering and Processing |

$130 |

|

Production Taxes |

$258 |

|

Cash G&A |

$135 |

|

Cash Interest |

$65 |

|

Capital Expenditures |

$1,400 |

|

Total Expenses |

$2,267 |

This leads to a projection that PDC can generate $1.075 billion in free cash flow in 2023 before potential cash income taxes.

Share Count

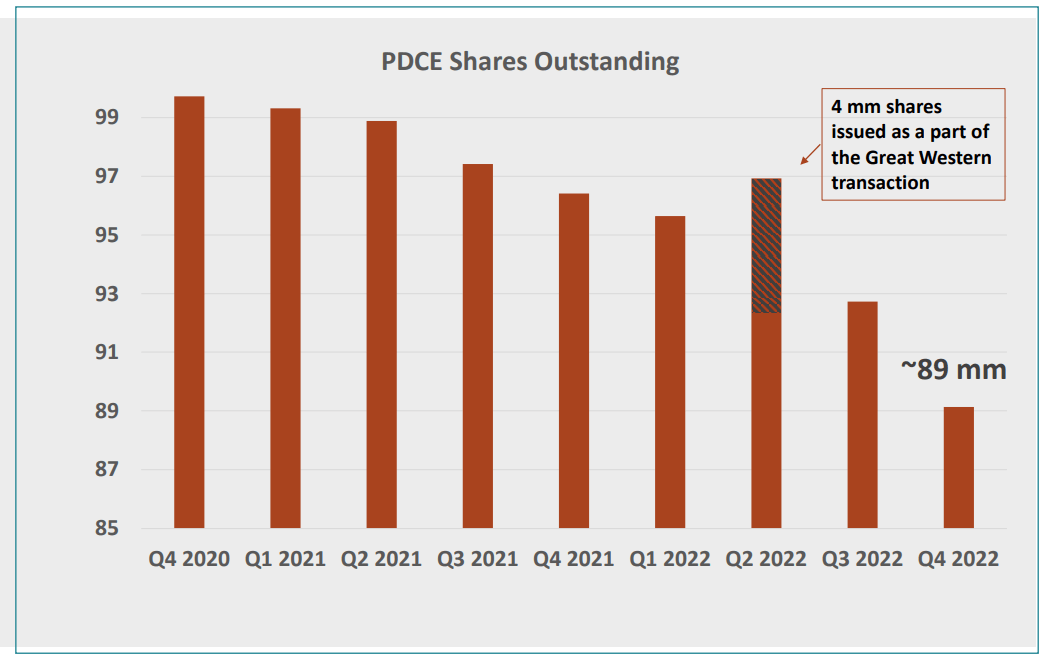

PDC’s aggressive share repurchases have reduced its outstanding share count to approximately 89 million at the end of 2022, down from nearly 100 million at the end of 2020. This reduction comes despite PDC issuing approximately 4 million shares for its Great Western acquisition.

PDC’s Outstanding Shares (pdce.com)

Although PDC’s share repurchases may slow in 2023 due to reduced free cash flow compared to 2022, it can probably end 2023 with a share count in the low-80 millions.

Notes On Valuation

I now estimate PDC’s value at $75 to $81 per share in a long-term $70 WTI oil and $4.00 Henry Hub gas scenario. This includes the expected effects of PDC’s share repurchases in 2023, reducing its share count to the low-80 millions. PDC’s estimated value has been improved by the approval of the Guanella CAP, which gives it a line of sight for DJ Basin development activity in 2028. The approval of various CAPs also shows that companies are figuring out how to design projects to meet Colorado’s updated requirements.

Conclusion

PDC is projected to generate around $1.075 billion in free cash flow in 2023 at current strip before the impact of cash income taxes. Much of that free cash flow is likely to go towards share repurchases. PDC aims to put 60+% of its free cash flow (after its base dividend) toward share repurchases and special dividends. It made the decision to focus mainly on share repurchases during 2022, reducing its outstanding share count to around 89 million by the end of the year.

PDC got unanimous approval for its Guanella CAP, giving it line of sight for DJ Basin development activities into 2028. I now estimate that PDC is worth around $75 to $81 per share in a long-term $70 WTI oil and $4.00 Henry Hub gas environment.

Be the first to comment