Sergey Dolgikh

A Quick Take On Paya Holdings

Paya Holdings (NASDAQ:PAYA) reported its Q3 financial results on November 4, 2022, beating revenue estimates and matching its earnings outlook.

The firm provides a range of integrated payment processing services for customers in the United States.

Optimistic investors may find PAYA an interesting bet, especially on its large B2B addressable market, but I don’t see a high net margin business here, and volume growth is under threat in 2023’s macroeconomic gloom.

So, I’m on Hold for PAYA in the near term, but the stock is worth putting on a watch list for future consideration.

Paya Holdings Overview

Atlanta, Georgia-based Paya Holdings was founded to provide payment processing capabilities to merchants and government agencies.

The firm is headed by Chief Executive Officer, Jeff Hack, who was previously EVP at First Data, and prior to that, COO at Morgan Stanley Smith Barney.

The company’s primary offerings include:

-

Credit and debit card

-

Automated clearing house (ACH)

-

Check payments

-

Integrations

Paya acquires customers through distribution partners and operates in two segments, Integrated Solutions and Payment Services.

Paya’s Market & Competition

According to a 2019 market research report, the market for payment processing services is expected to reach $62.3 billion by 2024.

This represents a forecast CAGR of 9.9% from 2019 to 2024.

The main drivers for this expected growth are a continued growth in the number of merchants seeking integrated payment processing solutions and the entrance of new market participants with new technology offerings.

Major competitive vendors include:

-

PayPal

-

Global Payments

-

Block

-

Wirecard

-

Visa

-

Jack Henry & Associates

-

Paysafe Group

-

Naspers Limited

-

Shift4 Payments

Paya’s Recent Financial Performance

-

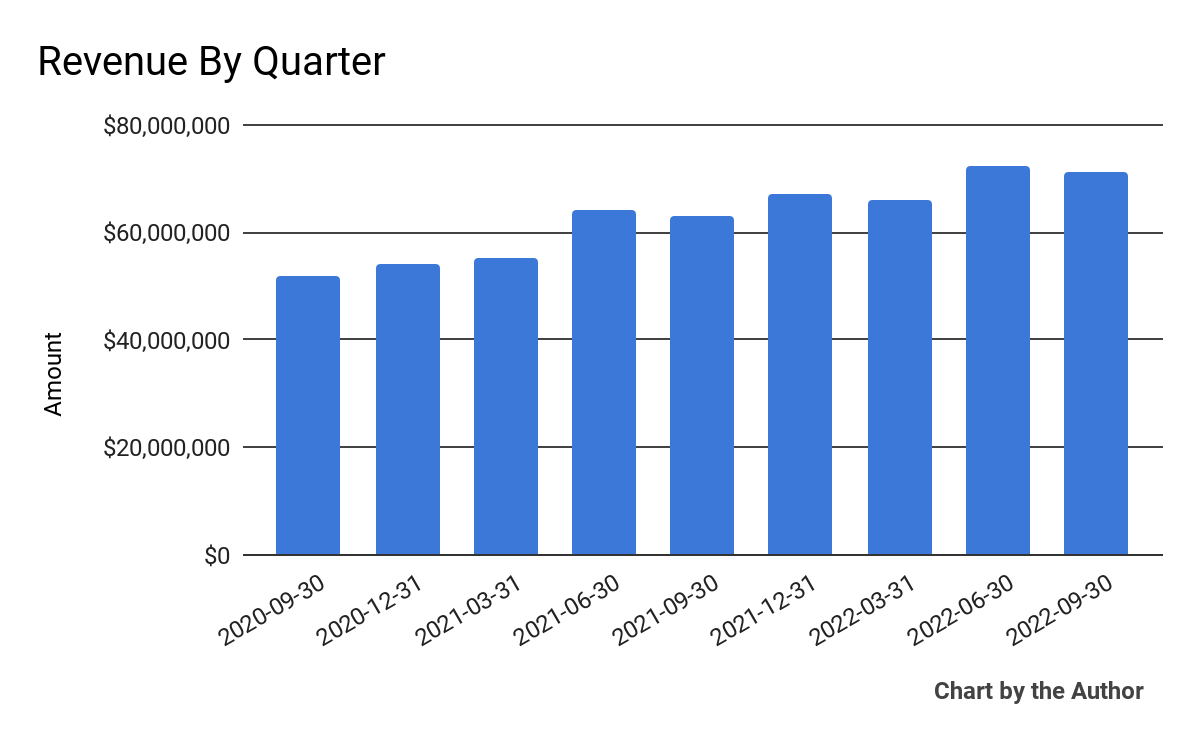

Total revenue by quarter has risen per the following chart:

9 Quarter Total Revenue (Financial Modeling Prep)

-

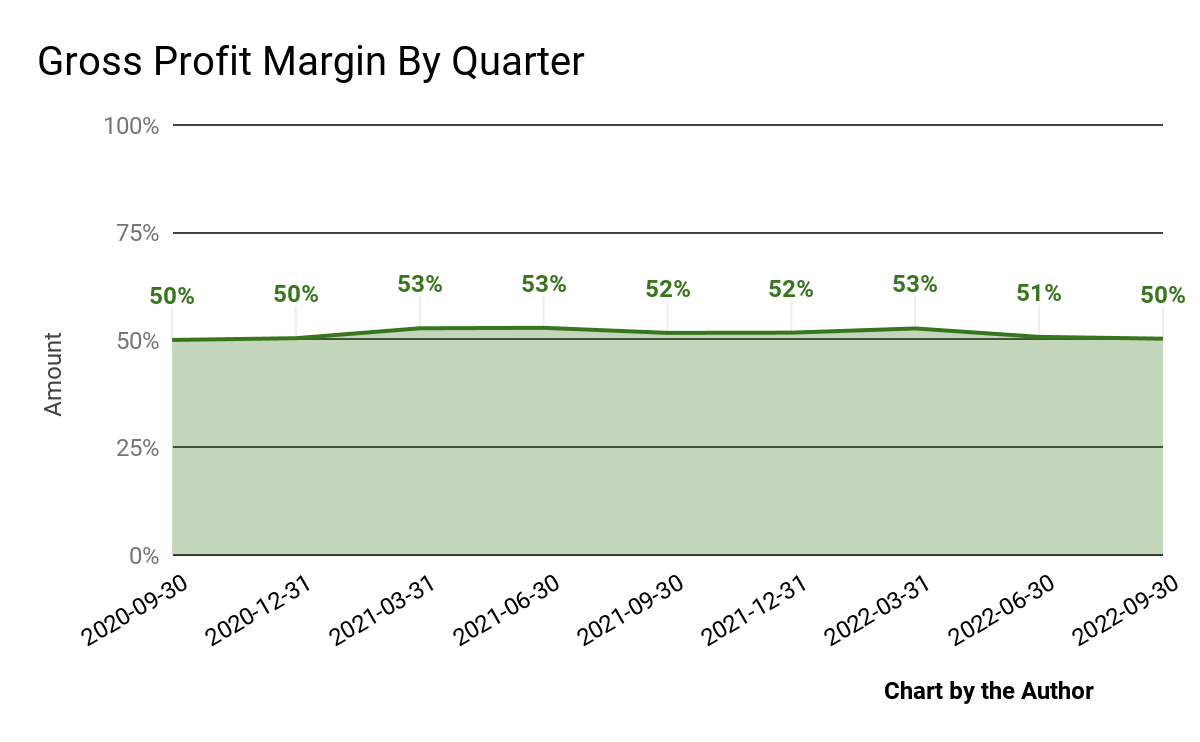

Gross profit margin by quarter has dropped slightly in recent quarters:

9 Quarter Gross Profit Margin (Financial Modeling Prep)

-

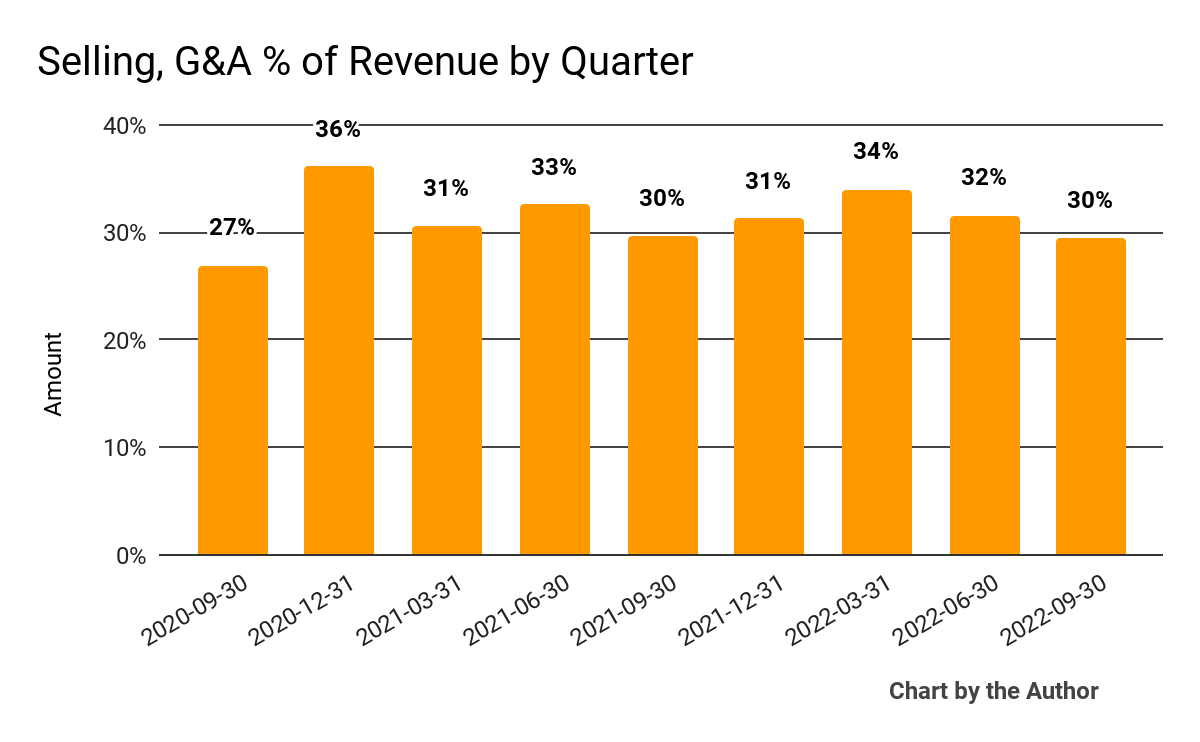

Selling, G&A expenses as a percentage of total revenue by quarter have varied within a tight range:

9 Quarter Selling, G&A % Of Revenue (Financial Modeling Prep)

-

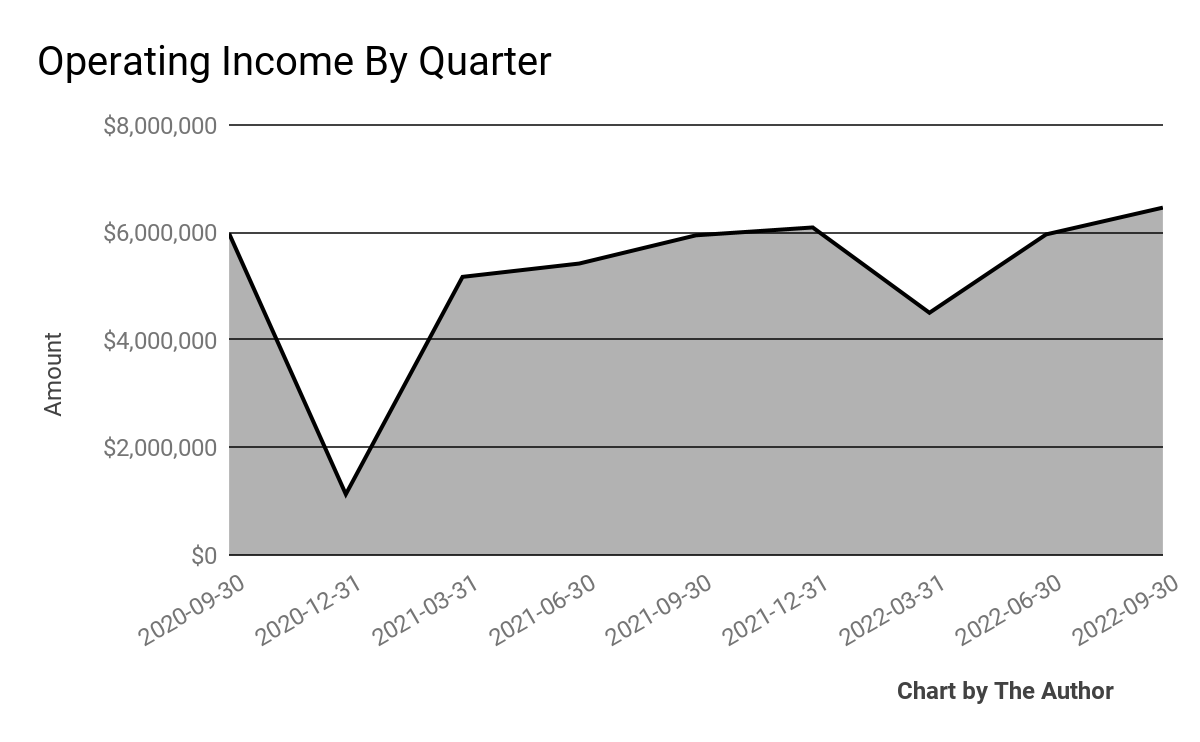

Operating income by quarter has exceeded $6 million in the most recent quarter:

9 Quarter Operating Income (Financial Modeling Prep)

-

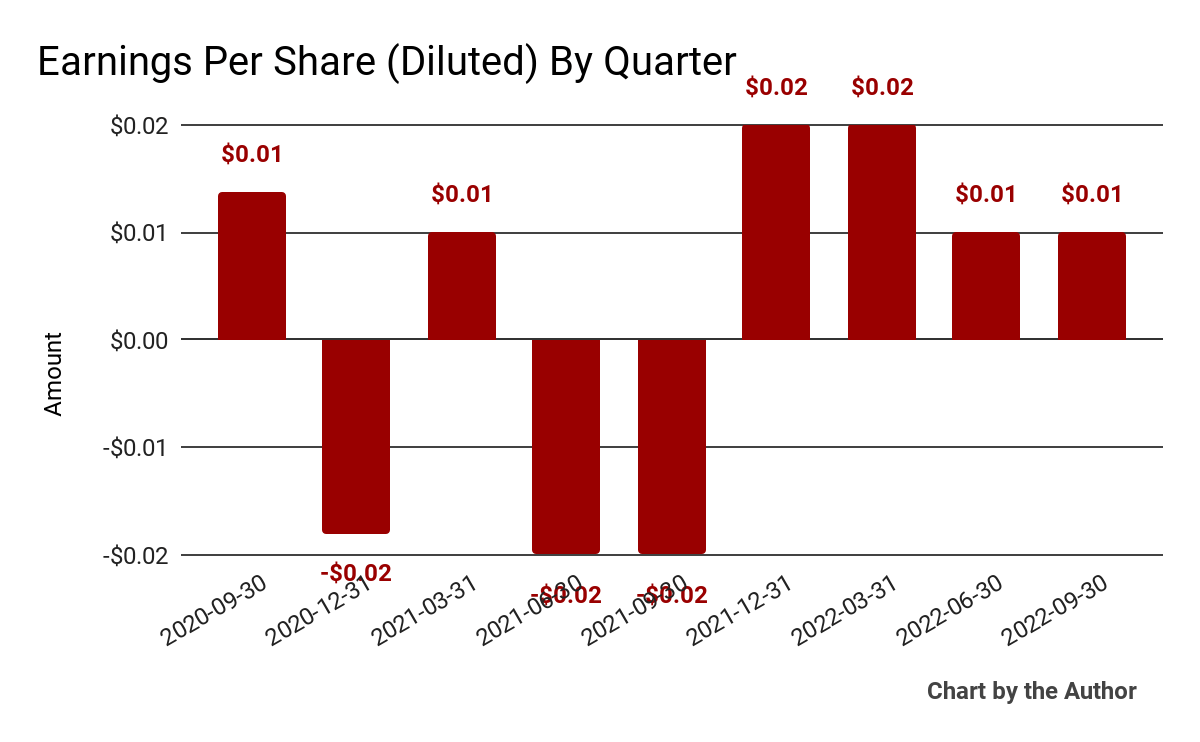

Earnings per share (Diluted) have fluctuated closely to breakeven:

9 Quarter Earnings Per Share (Financial Modeling Prep)

(All data in the above charts is GAAP)

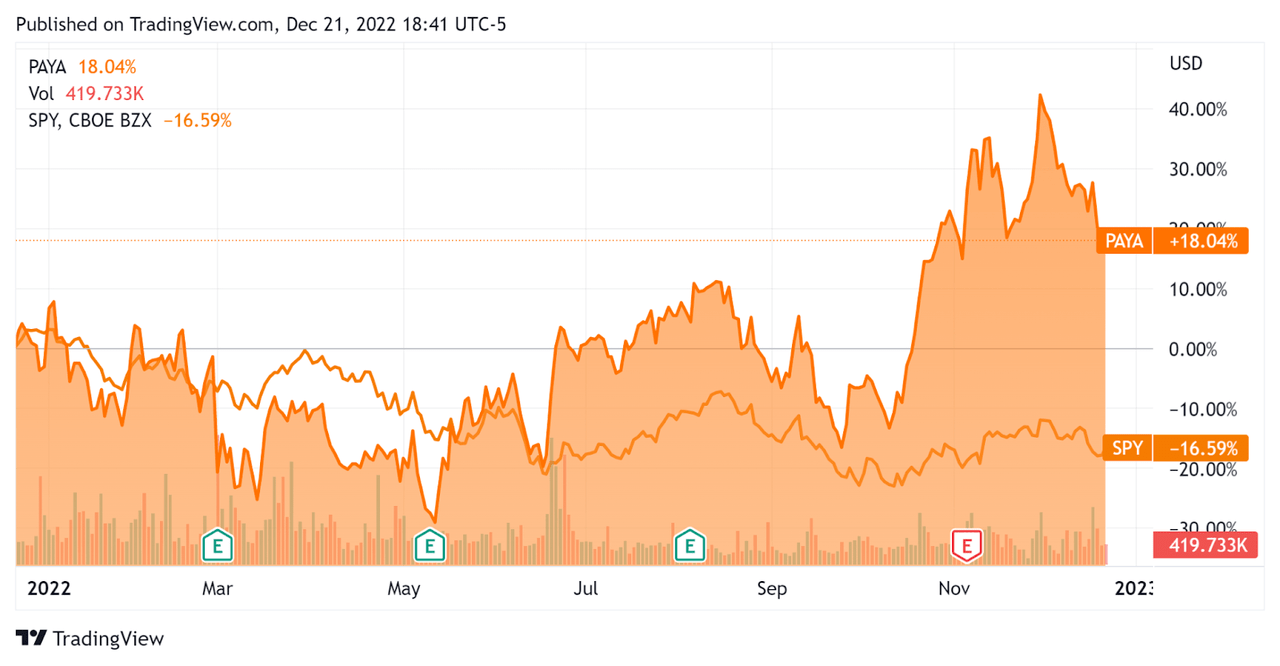

In the past 12 months, PAYA’s stock price has risen 18% vs. the U.S. S&P 500 Index’s drop of around 16.6%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Paya Holdings

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure (TTM) |

Amount |

|

Enterprise Value/Sales |

3.9 |

|

Enterprise Value/EBITDA |

19.3 |

|

Revenue Growth Rate |

17.2% |

|

Net Income Margin |

3.4% |

|

GAAP EBITDA % |

20.2% |

|

Market Capitalization |

$1,039,209,900 |

|

Enterprise Value |

$1,082,312,155 |

|

Operating Cash Flow |

$45,756,000 |

|

Earnings Per Share (Fully Diluted) |

$0.06 |

(Source – Financial Modeling Prep)

Commentary On Paya Holdings

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted the growth in payment volume, which rose by 14%.

The company saw improved results in its ‘high growth, underpenetrated and less cyclical end markets.’

The firm and its partners focus their efforts on the B2B, healthcare, not for profit and government market verticals.

Paya recently launched its citizen portal, for municipal government payment administration to its local citizenry.

As to its financial results, total revenue rose 13%, and adjusted EBITDA grew 14%.

While operating income ticked up sequentially, EPS was flat sequentially.

For the balance sheet, Paya finished the quarter with $158.7 million in cash, equivalents and trading asset securities, and $243.1 million in total debt.

Over the trailing twelve months, free cash flow was $38.6 million, of which capital expenditures accounted for $5.0 million.

Looking ahead, management raised the low end of its full-year 2022 guidance, with revenue expected to be $281.5 million at the midpoint of the range and adjusted EBITDA at $73.5 million at the midpoint.

Regarding valuation, the market is valuing PAYA at a much lower EV/EBITDA multiple as that of Shift4 Payments. Shift4 is growing revenue at about 3x that of PAYA.

The primary risk to the company’s outlook is the potential for a macroeconomic slowdown or recession in 2023, which would likely weigh on payment volume growth and revenue.

A potential upside catalyst to the stock could include a ‘short and shallow’ downturn in the first half of 2023.

In any event, while the firm is growing revenue, there isn’t a pattern of the benefit of that revenue growth dropping to the bottom line.

Despite the potential resilience of some of the company’s vertical focus characteristics, its gross margin mix variability can reduce the benefit of topline revenue growth, as management doesn’t ‘manage to gross margin percentage.’

While the firm has a strong enough balance sheet to get M&A deals done, and its pipeline is ‘solid’, management doesn’t appear to be in a hurry to make deals as they are probably waiting for valuations to fall further and for future economic conditions to come clearer into view.

Optimistic investors may find PAYA an interesting bet, especially on its B2B addressable market, but I don’t see a high net margin business here, and volume growth is under threat in 2023’s macroeconomic gloom.

I’m on Hold for PAYA in the near term, but the stock is worth putting on a watch list for future consideration.

Be the first to comment