Michael Vi/iStock Editorial via Getty Images

All eyes will be on Palantir (NYSE:PLTR) when it reports fiscal fourth quarter results after market close on Monday. Investors will be keenly watching how spending cuts by enterprises across the globe affect the software stalwart’s sales in its upcoming results. But in addition to tracking the headline financial figure, investors might want to also keep a close eye on its customer additions, billings value, segment financials and its management’s outlook for the year ahead. These items, combined, will provide us with a holistic view of Palantir’s near-term prospects and are likely going to influence where its shares head next. Let’s take a closer look to gain a better understanding of it all.

Gauging Operating Performance

I’d like to start by saying that we’re in the midst of macroeconomic turmoil. Companies are slashing their discretionary spending to weather the recessionary environment, and Palantir’s customers might be doing the same. So, we’ve to pay particularly close attention to Palantir’s operational and financial performance to assess how adversely has its business been affected or if it’s business as usual for them.

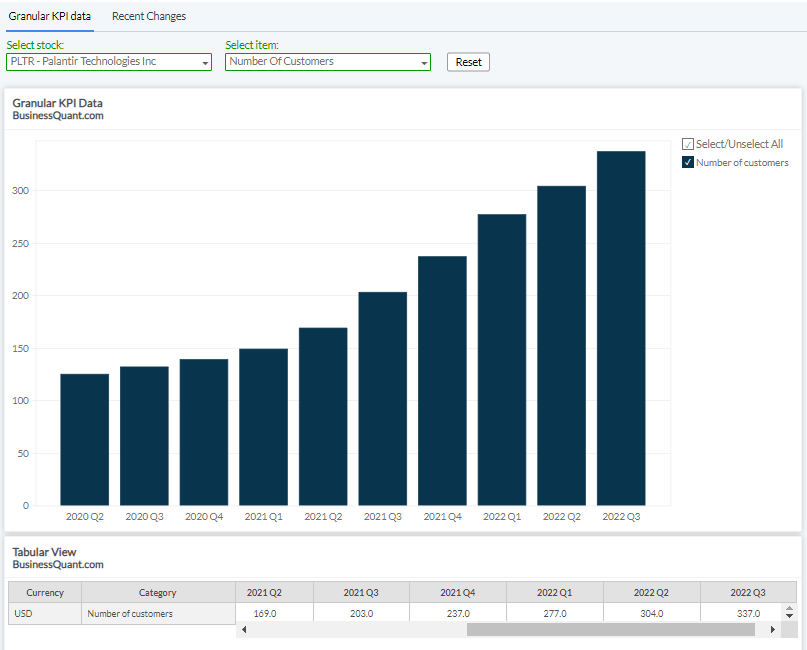

We can start by tracking Palantir’s customer count. The company has made a number of concerted decisions to grow its footprint in the commercial space over the last 2 years, which involves undertaking steps such as expanding their direct sales team, moving away from an upfront payment model and adopting a recurring fee model, as well as giving teaser access to major enterprises for free. The proof is in the pudding – Palantir’s customer count has skyrocketed.

BusinessQuant.com

But this will be a testing quarter for Palantir. If its pool of potential customers is treating the company’s platforms as a non-essential, then they’re likely to defer their orders, and we’re likely to see Palantir’s customer count stagnate for the time being at least. But if its platforms are truly a value-add for its existing and potential customers, then we’re likely to see its customer count grow in spite of the tumultuous macroeconomic situation. I’m optimistic about Palantir’s capabilities, so I believe the latter scenario will play out nicely and Palantir will bag another 20-30 customers during Q4.

Another key item to watch would be its billings value. This will indicate how Palantir’s new and existing customers are using its platforms. If they’re cutting back on Palantir’s billings, then its platforms are probably being classified as non-essential spending, and it will come across as bad news for the company’s shareholders. But, as I said earlier, I’m optimistic about how Palantir adds value for its customers, so I expect its billings to grow during Q4 as well. Worst case scenario, in my opinion, is that Palantir’s pace of billings growth could moderate, but I do not expect the metric to decline in value anytime soon.

BusinessQuant.com

But with that said, let’s now shift attention to Palantir’s financials.

Financial Expectations

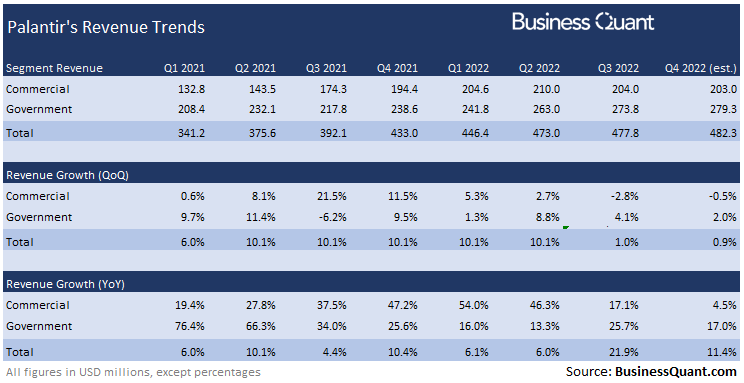

It’s worth noting that Palantir classifies its revenue in two reportable segments, namely Government and Commercial. The latter segment caters to non-government enterprises across the globe of all scales and sizes, and the segment accounted for approximately 43% of Palantir’s total sales last quarter. The company has been expanding its sales function over the last 6-8 quarters, which bolstered its commercial revenue in the said time frame.

BusinessQuant.com

However, the ground reality now is that we’re in a recessionary environment and enterprises across the globe are cutting back on discretionary spending in order to survive this economic downturn. Since Palantir isn’t decoupled from the macroeconomic environment, I believe its commercial revenue is going to see a minor contraction of 0.5% on a sequential basis and its revenue figure is going to come in at roughly $203 million.

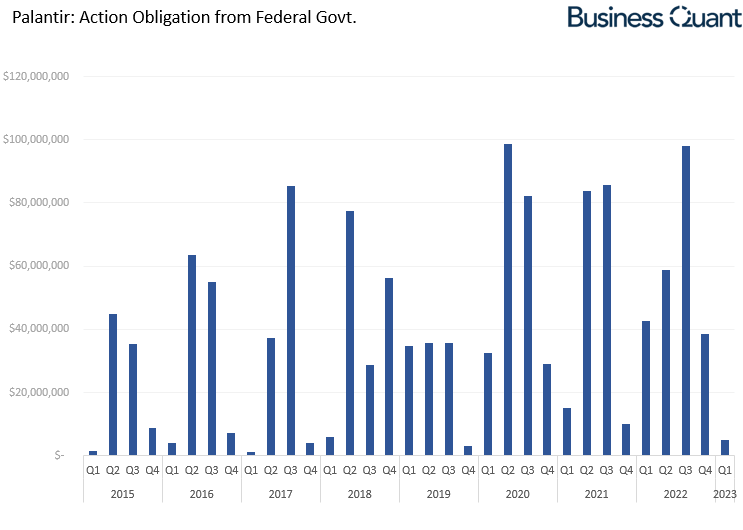

Next, Palantir’s government division comprises of sales to government agencies, be it domestic or international, and it contributed approximately 57% towards the company’s total sales last quarter. This segment has been consistently growing sales, in spite of all the bearish narratives floating around in the rumor verse. I’ve maintained in prior articles that Palantir’s strong presence in the government division, earns it praise, credit and referrals for other government divisions. Since there hasn’t been any major catalyst to change the status quo, I expect the trend to continue in Q4 as well.

Note in the chart below how Palantir has scored a good number of orders from US government agencies during Q4. Granted, the figure is down sequentially, but it’s much higher than the levels typically seen in Q4’s of prior years. So, I’m optimistic about Palantir’s government business and expect its revenue to grow north of 11% on a year-over-year basis during Q4, with its revenue coming in around $279.3 million.

BusinessQuant.com, FPDS database

This brings us to a company-wide revenue estimate of $482.3 million. Coincidentally, my estimate is within the Street’s consensus range that’s currently spanning from $472.5 million to $515.7 million at the time of this writing.

BusinessQuant.com

With that said, investors must also pay close attention to Palantir management’s revenue outlook for the year ahead. This is going to be particularly important because Palantir is considered to be a high-growth stock in investing circles. If the company can keep up with its pace of revenue growth, or accelerate it, while the macroeconomic conditions remain tumultuous, it’ll inspire long-term investors and the stock is likely to rally shortly after. But if the management hints of a slowdown in its growth momentum, then investors are likely to reconsider their investment thesis and the company’s shares may be subdued in the subsequent weeks. So, revenue guidance is going to be another key item in Palantir’s Q4 earnings report.

Investors Takeaway

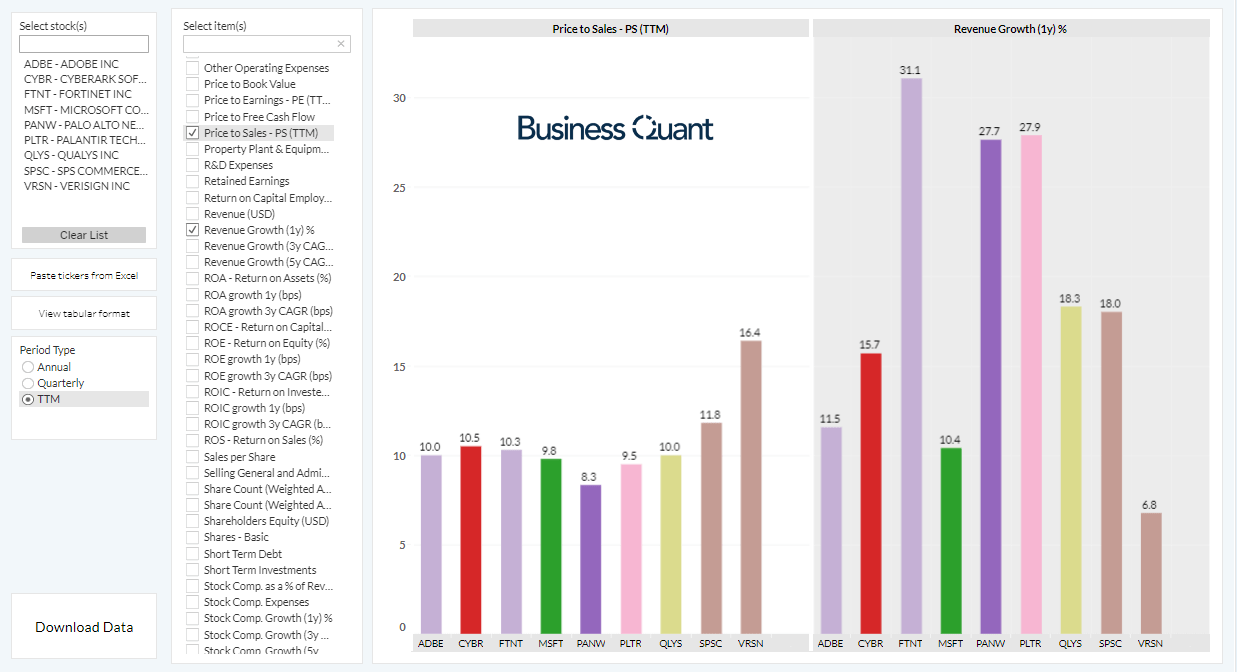

It’s worth noting that Palantir’s shares are down nearly 40% over the last year, which has, arguably, pushed it into the oversold territory. For instance, the stock is currently trading at 9.5-times its trailing twelve-month sales. This figure may seem huge in isolation, but it’s actually quite attractive when comparing with industry peers. Most of the other prominent software infrastructure companies are either trading at even higher multiples, or their pace of revenue growth is relatively much lower. So, I’m bullish on Palantir at current levels and believe it makes for a good buying opportunity for investors with a multi-year time horizon.

BusinessQuant.com

As far as Q4 is concerned, investors may want to keep close tabs on Palantir’s segment financials, management’s revenue outlook for the year ahead, its customer count and its billings growth. These items will better highlight Palantir’s near-term growth prospects and dictate the investors’ sentiment pertaining to the company in the coming weeks. Good Luck!

Be the first to comment