Kevin Dietsch

Palantir Technologies Inc. (NYSE:PLTR) surprised the bulls and bears and most Wall Street analysts as it reported its first-ever GAAP profitable quarter. Moreover, CEO Alex Karp reiterated the company’s commitment to maintaining its GAAP profitability for 2023, which likely sent the bears scurrying for cover.

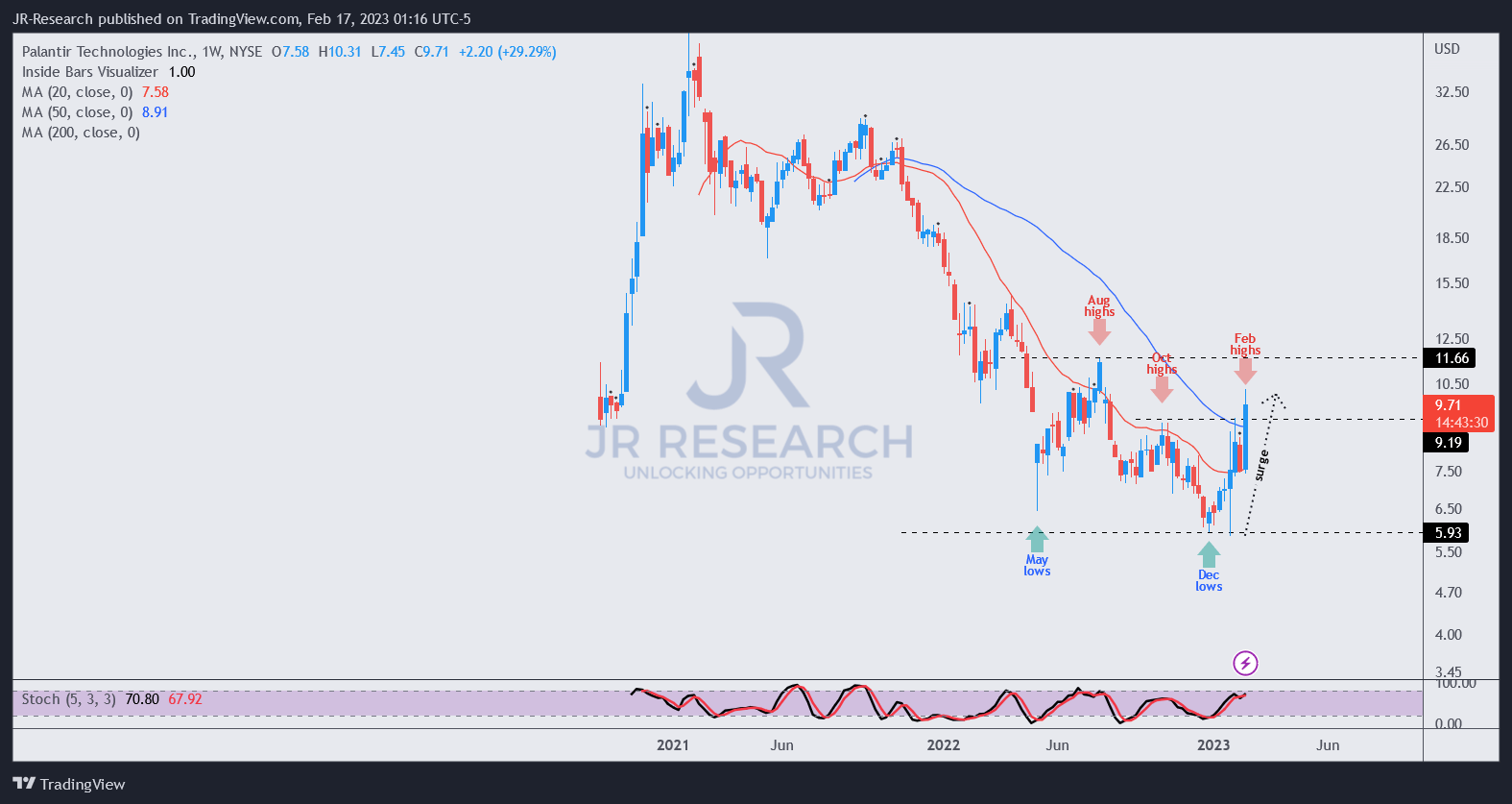

Accordingly, PLTR has significantly outperformed the S&P 500 (SPX) (SPY) since forming its lows in December. It posted a price-performance gain of nearly 75%, demonstrating the power of its highly attractive reward-to-risk proposition at its 2022 bottom.

However, with the significant surge from its previous lows, PLTR is no longer reasonably valued. At an NTM EBITDA of 34.2x, or NTM adjusted P/E of 48x, we believe the optimism over the potential of maintaining its GAAP profitability has been reflected.

As such, investors must be extra vigilant to avoid chasing the recent momentum spike, even though greedy buyers chasing AI-hype trains could push PLTR up further in the near term.

However, we explained in our previous article that Palantir is not just another AI-hype company. Instead, it has defined its competitive edge over time with its government customers, particularly the US government. Therefore, Palantir’s capability to shape further AI progress built on top of its AI operating system shouldn’t be understated.

Karp even stressed the significance of Palantir’s systems as its customers are keen on watching Palantir achieve sustainable profitability, given the mission-critical nature of Palantir’s system deployments in their business. He added:

The people whose lives depend on our product have been very dependent on us and want to know that our financial stability now and in the future is guaranteed. So this [GAAP profitability] has been much more of a priority to get us to this place. (Palantir FQ4’22 earnings call)

So, the naysayers who believe that Palantir will fade away when the AI hype normalizes subsequently need to consider their thesis carefully.

Karp accentuated that Palantir has been spending the “last 5 years building core infrastructure for powering and training AI algorithms.” As such, the company has a strong foundation with its customers, particularly when “Palantir’s clients are mostly regulated, and this requires specific considerations for the use of AI.”

Investors need to bear in mind just how important Karp’s commentary on regulating the at-scale deployment of AI is, which is what Palantir’s government and commercial AI platforms are designed for. Hence, Palantir remains well-perched in the catbird seat, with AI taking centerstage moving forward.

Keen investors have had a front-row seat watching how challenging Google (GOOGL) and Microsoft (MSFT) have struggled with their advanced AI models for broad adoption. Their models have been ridiculed with allegations of misinformation/biases/inaccuracy/hallucination, etc.

As such, with the proliferation of “AI in everything,” we believe Palantir’s proven systems will likely set it further apart from even its closest peers, with its proprietary technology “not available anywhere else.”

Notwithstanding, investors need to note that the company’s FY23 outlook suggests a further slowdown in topline growth, mitigated by its commitment to GAAP profitability.

Hence, we believe investors need to assess the company’s ability to remain on its profitable path, as bears will likely be lurking in the hallway, waiting to pounce on any signs of weakness.

PLTR price chart (weekly) (TradingView)

With the surge in PLTR over the past two months, investors who missed buying earlier need to exercise vigilance and patience now.

The market will likely assess the growth cadence of its commercial and government business, which has continued to slow, as highlighted in its outlook.

Moreover, with the Fed likely to tune up its hawkishness, given the strength of the economy and persistent inflationary pressures, a further upward re-rating of PLTR’s growth premium might not be sustainable.

Hence, waiting for a steeper pullback to add more positions could be the more prudent move instead of joining the recent buyers now.

Rating: Hold (Revised from Buy).

Be the first to comment