Michael Vi

In less than a month Palantir (NYSE:PLTR) will submit its earnings card for the second-quarter, which, if the company executed well against its growth targets, could potentially be a catalyst for a the initiation of a new up-leg in shares of Palantir. I last covered Palantir in June While I expect Palantir’s second-quarter revenues to slightly exceed the firm’s Q2’22 guidance, the company will likely have made further progress regarding its customer monetization rate, especially in the commercial business where all of the firm’s momentum is right now. I believe Palantir will submit a solid earnings card in August and the firm could sail past low earnings expectations.

Palantir’s Q2’22: Guidance versus expectations

For the second-quarter, Palantir has said it expects to see base case revenues of $470M and adjusted operating margins of 20%. The revenue guidance implies 5.3% quarter over quarter growth, but revenues could come in better than expected if the company on-boarded a good amount of new paying clients in the commercial business. I anticipate revenues between $470-475M as the second-quarter likely saw improving customer monetization as well as a decent number of customer net-adds.

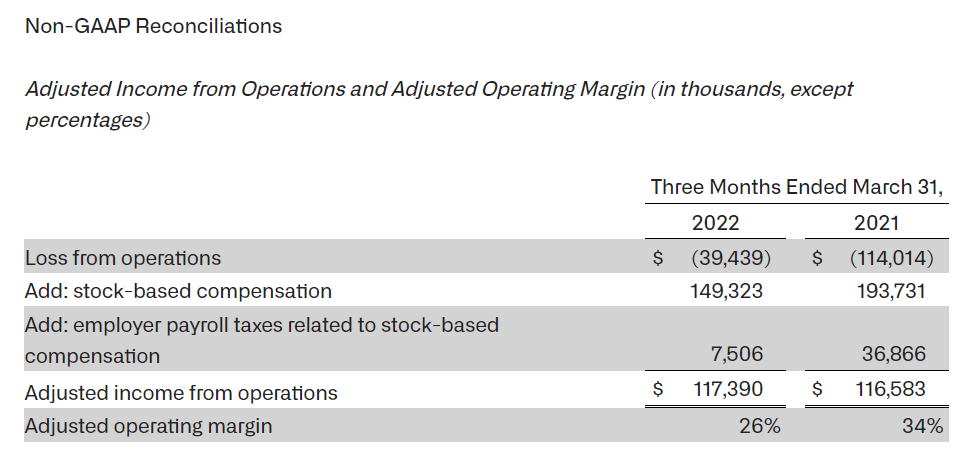

Regarding adjusted operating margins, Palantir historically submitted margin expectations that were low relative to actual results. In Q1’22, Palantir guided for Q2’22 adjusted operating margins of 23% while actual margins were 26% and FY 2021 guidance regarding margins was also conservative. For this reason, I expect Palantir to report slightly better adjusted operating margins, between 22-24% for Q2’22, in part because I expect strong net retention rates as well as continual increases in customer product spend.

Palantir

Customer monetization could make a difference for Palantir

While new customer net-adds are an important way to broaden its revenue base, it is key for Palantir to optimize revenue generation from its existing client book.

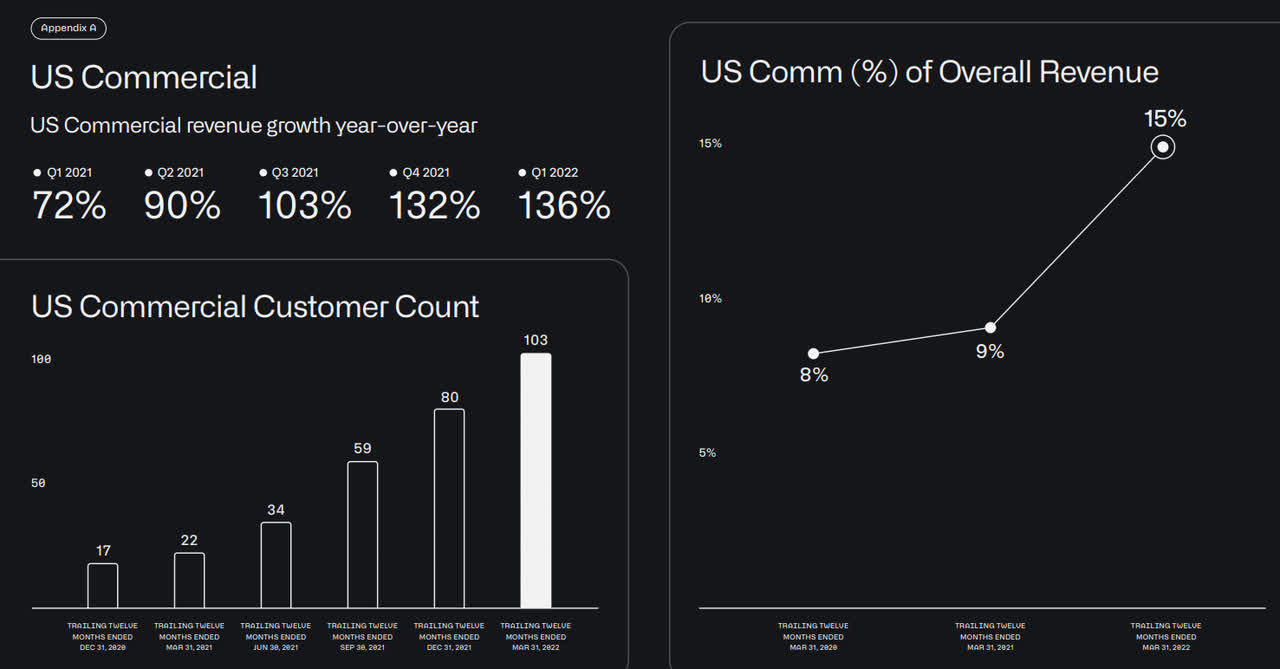

Palantir’s commercial revenue growth accelerated for the fifth straight quarter in Q1’22 and the firm added 37 net new customers in this segment, after tripling the commercial customer count in FY 2021. Palantir serviced 184 commercial customers at the end of Q1’22, showing 207% year over year growth. Across Palantir’s government and commercial businesses, the company had 40 customer net-adds in Q’22 and this momentum is likely to have persisted in the second-quarter.

Palantir

My expectations for Palantir’s Q2’22 are:

- 136-140% year over year US commercial revenue growth, sixth straight quarter of top line acceleration

- A total customer count across government and private enterprise segments exceeding 300, for the first time ever, implying a customer net-add of at least 23 accounts

- Commercial customer count exceeding 200, for the first time ever, implying at least 16 net-adds in Q2’22

- Average revenue per top twenty customer growing from $45M to $47M, showing 4.4% quarter over quarter growth, driven by US commercial momentum

- Continual quarter over quarter growth in ACV (average account value) and billings

Average revenue for the largest 20 customers grew 24% year over year to $45M in Q1’22 and I believe that Palantir could really surprise here for the second-quarter due to clients having shown a willingness to increase spending on Palantir’s products and services. Anything that indicates improving monetization (higher average product spend, large number of customer net-adds and growing net retention) could push shares of Palantir into a new up-leg, but a sizable revenue beat could also achieve this.

Low EPS expectations

In each of the last two quarters Palantir’s actual EPS was 50% below its expected EPS: $.02 per-share compared to $.04 per-share — meaning the software analytics company under-performed estimates in two quarters in a row. In each case, shares of Palantir plunged after the earnings card was delivered, with investors taking out their frustration on Palantir’s shares.

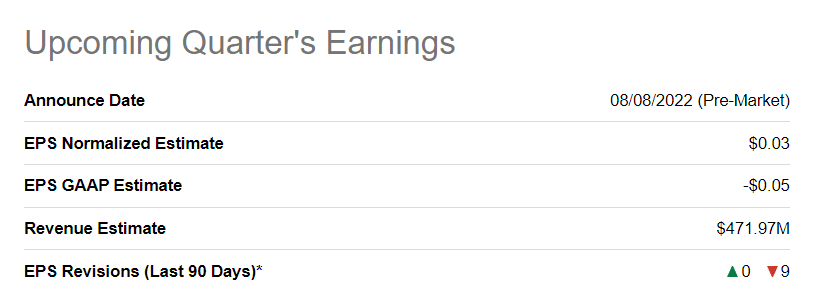

For the second-quarter, the prediction is for Palantir to have EPS of $.03 and predictions have fallen nine times in the last 90 days, meaning the market doesn’t expect much from Palantir. An earnings beat in August, potentially driven by improving customer monetization in the commercial business, could create some desperately needed upside momentum for Palantir.

Seeking Alpha

New U.S. Army Contract Win

Just before the end of the second-quarter, Palantir announced that it was one of two companies that was awarded a U.S. Army contract to build a prototype for TITAN, which stands for Tactical Intelligence Targeting Access Node. TITAN is a system that consolidates a large amount of data to assist long range precision targeting missions. With more and more sensor data to sift through, the U.S. Army is going to draw on artificial intelligence and machine learning capabilities for threat identification and tracking… and Palantir stands ready to support the effort. The Army contract will last through 2023 and is worth $36M. The most recent contract win comes after Palantir was awarded a $53.9M contract increase by the U.S. Space Systems Command at the end of May which brought the SSC contract value to $175.4M. Contracts like these are the reason why I believe Palantir could reasonably see an acceleration of revenue growth in the non-commercial business as well going forward.

Risks with Palantir

The two biggest risks for Palantir are a slowdown in revenue growth, especially in the U.S. commercial business which is driving the company’s entire financial performance right now, and shareholder dilution related to Palantir’s high levels of stock based compensation.

What would change my mind about Palantir is if the firm’s second-quarter earnings showed deteriorating metrics in customer monetization rates, a drop-off in customer net-adds or declining average revenue per customer.

Final thoughts

Palantir has been on a wild ride lately and it hasn’t been a good one. Shares of the software analytics company are in a long term down-trend and have skidded below $10 in July. To get Palantir to move into an up-leg, the software analytics company will have to deliver substantive business improvements in August… a sizable EPS beat, growing average revenues per customer (better monetization) and the on-boarding of a large number of new clients in the commercial business could do the trick for Palantir. I expect the company to confirm its 30% revenue growth target for FY 2022 while operating margins are likely going to come in better than expected, like they did in the past!

Be the first to comment