Dzmitry Dzemidovich

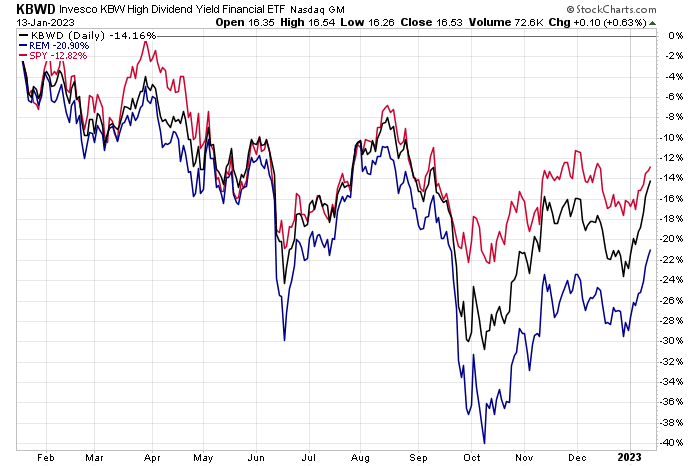

Mortgage REITs have been a tempting place to park some cash to earn a high yield lately with a big drop in equity pricing within the space. While high dividend financials have fallen roughly in line with the S&P 500 over the last year, as measured by the Invesco KBW High Dividend Yield Financial ETF (KBWD), the iShares Mortgage Real Estate ETF (REM) is down massively from 12 months ago – even when including dividends.

One REIT in KBWD has endured volatility, but shares have been on the mend lately. Is there more upside in Orchid Island Capital (NYSE:ORC)? Let’s take a look.

Mortgage REITs Surging Back, But Still Underperforming SPY

Stockcharts.com

According to CFRA Research, Orchid Island Capital a specialty finance company, invests in residential mortgage-backed securities (RMBS) in the United States. The company’s RMBS is backed by single-family residential mortgage loans, referred to as Agency RMBS. Its portfolio includes traditional pass-through Agency RMBS, such as mortgage pass-through certificates and collateralized mortgage obligations; and structured Agency RMBS comprising interest-only securities, inverse interest-only securities, and principal-only securities.

The Florida-based $401 million market cap Mortgage Real Estate Investment Trust (REITs) industry company within the Financials sector has steeply negative trailing 12-month GAAP earnings but pays a high 16.0% dividend yield, according to The Wall Street Journal. Seven percent of the float is short.

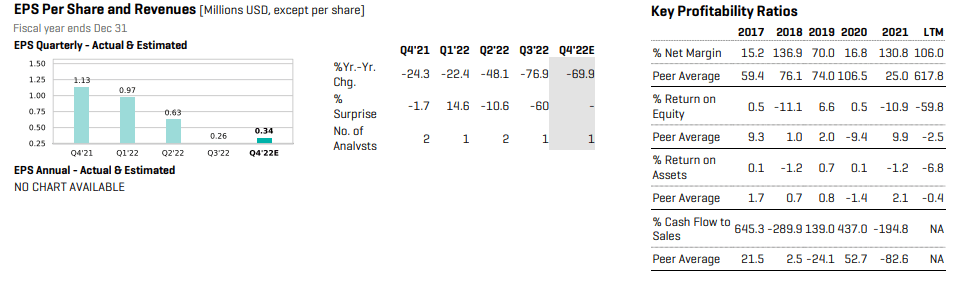

Last week, the firm estimated that its book value rose 4.5% in Q4, and that growth has been reflected in a recent rise in this small-cap’s stock price. It’s not all good news, however, as ORC reported a major EPS loss (GAAP) back in October as wider credit spreads and ongoing Fed rate hikes dinged the real estate market and ORC’s business operations. Moreover, as the Fed mulls selling off its MBS portfolio, that could negatively impact ORC too.

On valuation, the mortgage REIT is expected to report a massive 70% decline in earnings from a year ago in its upcoming quarterly report. With operating earnings summing to $2.20 from Q1 2022 through Q4 2022, the operating P/E is less than 6, which is attractive. What is not ideal, though, is that future profits will likely be much worse given the recession ongoing in real estate.

ORC: Earnings Outlook & Key Profitability Ratios

CFRA Research

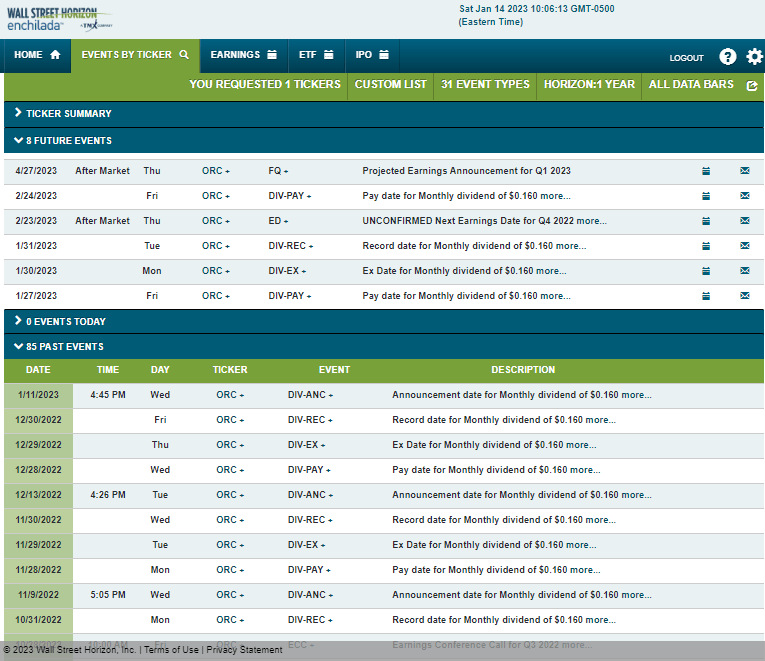

Looking ahead, corporate event data from Wall Street Horizon show an unconfirmed Q4 2022 earnings date of Thursday, February 23 AMC. A dividend ex-date of Monday, Jan 30 also takes place. No other volatility catalysts are expected.

Corporate Event Calendar

Wall Street Horizon

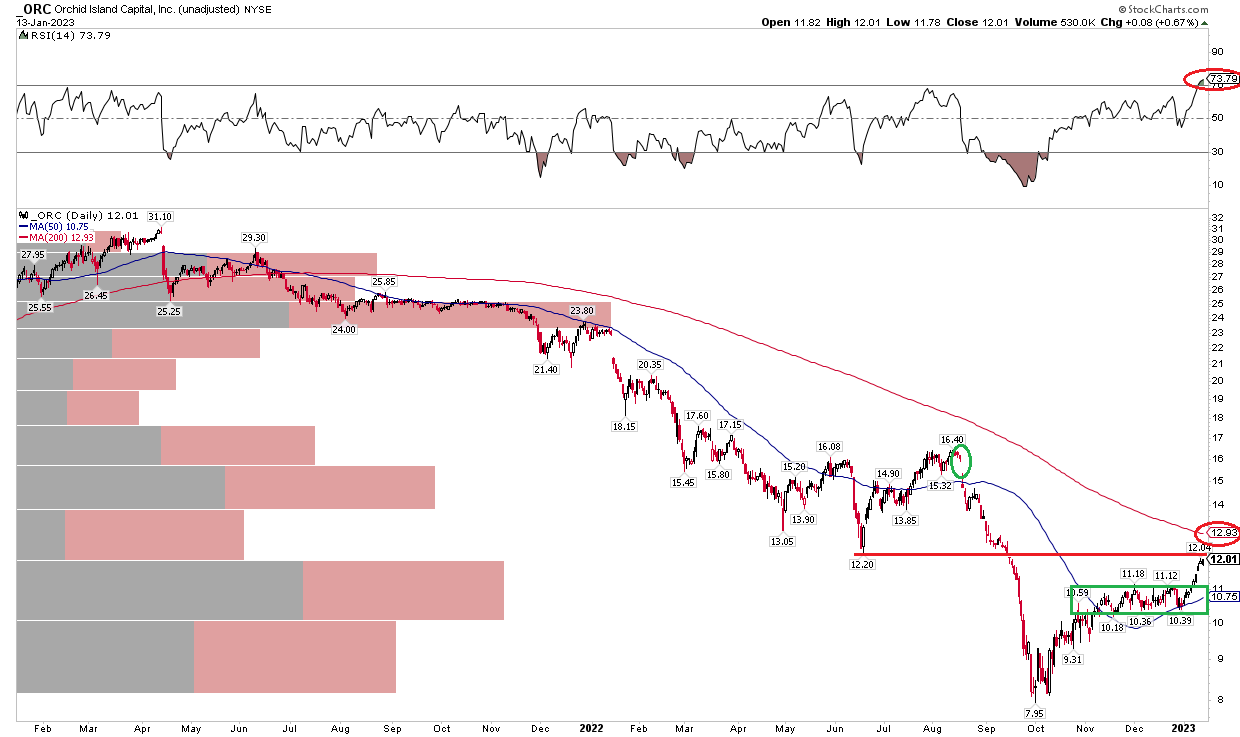

The Technical Take

With shares beaten down, but off the lows, what does the chart say about where ORC could go? I see capped upside for a few reasons. First, notice in the graph below that shares have risen back to the key $12.20 spot. That level was a low from June 2022.

Also, the stock ranged from the low $10s to the low $11s in November and December – with a bullish breakout from that zone, a measured move price target to the near $12.20 also hits here. Finally, notice that the stock is just now approaching its falling 200-day moving average, so that is another reason the bears could resume control.

Moreover, take a look at the high RSI at the top of the chart. Momentum has surged, while broader price action remains bearish. So perhaps the upside move is getting long in the tooth. I would be a seller here on this strength.

ORC: Shares Rally Into Resistance

Stockcharts.com

The Bottom Line

With a shaky housing market and declining operating profits, I would take profits on ORC longs. The chart also shows that we are now entering a resistance zone.

Be the first to comment