golibtolibov

ON Semiconductor (NASDAQ:ON) (ONSemi) provides products for an industry that is still expanding and where technology advancement plays a major role in equipment replacement. The company recently landed two important deals one with KIA Corporation and the other with Ampt.

The deal with KIA means ONSemi will be supplying traction inverters for the KIA EV6 GT electric vehicle. The modules provided by ONSemi will lower the weight and increase efficiency. The traction inverters will improve both the range and performance of KIA’s top EVs.

The press release also mentions that ONSemi will continue to cooperate with Hyundai/KIA for upcoming high-performance EVS based on the Global Module Platform (GMP). The GMP was developed by Hyundai and is also being used by KIA.

Considering how governments are pushing the manufacture of EVs all around the globe I believe the potential for products ONSemi manufactures in this sector is enormous.

The deal with Ampt, considered the world’s number one DC optimizer company by Business Wire, gives ONSemi the supply of a component Ampt uses in its string DC optimizers. The CEO of Ampt told Business Wire that they chose ONSemi for their product performance but also for their capability to scale production to meet Ampt’s high demand for string optimizers.

ONSemi is continuing the expansion of its client base and it’s holding on to most of the increase in earnings. The TTM EBITDA shows the company tripled its earnings from 2020. I’m not suggesting they’ll do it again over the next two years.

But the company seems to have a lot of factors in its favor, and it appears to be increasing profitability.

Industry Trend

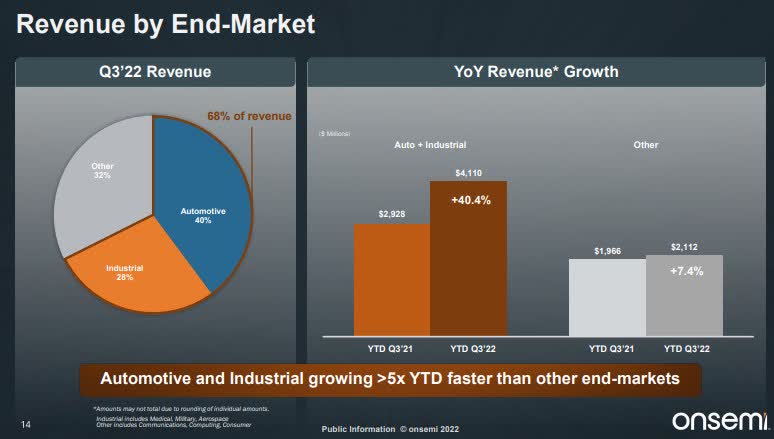

The industry demand for semiconductors is on the rise according to ONSemi and would be verified by the increase in revenue experienced by the company. In the latest quarterly investor presentation, they see most of that growth coming from the industrial and automotive end markets.

OnSemi

I see ONSemi as well positioned to take advantage of the growth of automotive and industrial end markets. The company has products of a high standard and the capability to scale up production to meet the demand of its customers.

The company’s latest two deals come from those end markets. However, there is also another sector that ONSemi caters to and that’s 5G. Presumably, the 5G products that ONSemi manufactures are in the industry end-market.

And that means they are including the growth potential from 5G in their report. However, ResearchAndMarkets issued a report on the 5G industry, and they estimate that the sector will grow from $5.06 billion in 2022 to $17.75 billion by 2027.

As ONSemi’s report is from Q3 2022 I doubt they would have had those numbers factored into their growth forecast.

Electric Vehicle Growth

This is the most important revenue source for ONSemi at the moment and accounts for 40% of revenue, as per their report. So, where is the EV market heading? And how has it expanded in recent years?

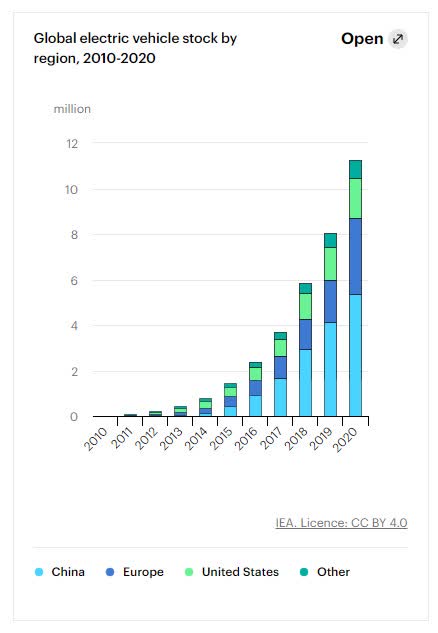

According to data from the IEA, the U.S. 2020 saw 1.8 million registered electric vehicles, the number includes plug-in hybrids and fuel cell cars. That number is more than 3 times the number of vehicles in 2016. However, the growth is even stronger in the EU and China.

IEA

In Europe, EV registrations stand at 3.3 million, in 2016 the number of EVs was 0.6 million. In China, the number of registered EVs has gone from 0.9 million in 2016 to 5.4 million in 2020. I really don’t see this trend changing anytime soon.

Many countries in Europe, and around the world, have mandated all vehicles should be zero emissions for a set date in the future. Although it still remains to be seen if those mandates still stand when the time comes.

For sure, there doesn’t seem to be much pushback from either side of the political spectrum in European countries and China of course is very likely to continue its policy. So, I see a huge potential in this sector for a company like ONSemi.

Photovoltaic Power

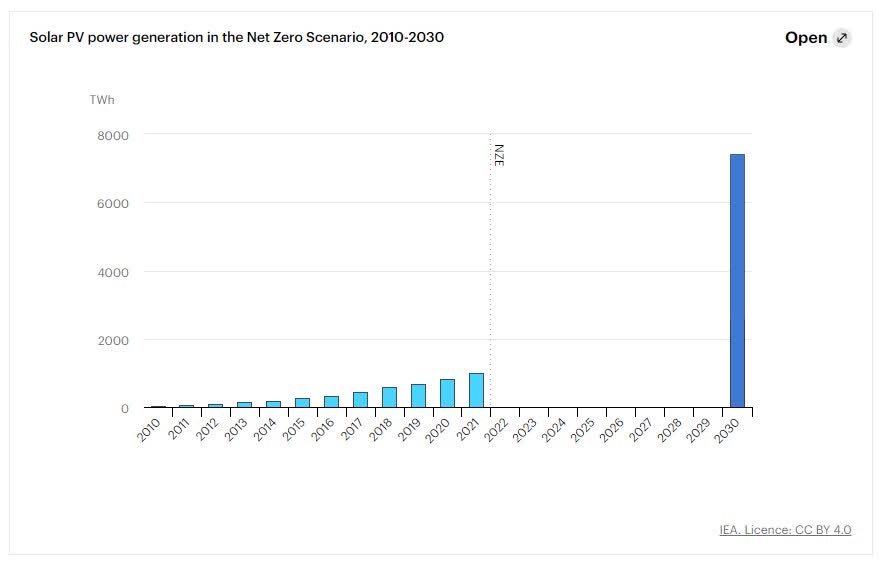

Photovoltaic power generation is another sector with a lot of expansion potential where ONSemi is a player. The IEA reports that photovoltaic power generation grew by 22% in 2021. The agency also sees solar photovoltaic energy as becoming the cheapest option for renewable energy generation.

Some countries are also subsidizing homeowners to install photovoltaic panels on their rooftops. Which has increased PV production and sales in many European countries. However, to get to the established net-zero target for 2030, the IEA estimates the PV generation growth would need to be 25% per year.

IEA

That seems a tall order, considering the growth for 2021 was 22% and it made PV power generation the second fastest-growing technology after wind power. However, given that so many governments are pushing renewable energy production, I feel it’s likely that the growth rate of PV power reaches 25% or close.

ONSemi Fundamentals

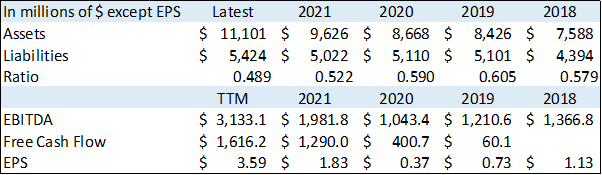

The thing I like the most about ONSemi’s fundamentals is the spectacular earnings growth. Earnings, as measured by EBITDA, have gone from $1.043 billion in 2020 to $3.3 billion TTM. This was helped by a great gross profit margin of 49.3%, which has been steadily growing since 2020 Q4 when it was 34.4%

Seeking Alpha

EPS has also been growing steadily and reached a TTM of $3.59 from $1.13 in 2018. The liabilities to assets ratio is also solid at 0.489 and can be seen as trending lower since 2018 when it was 0.579. It doesn’t compare so well to its peers:

Liabilities to assets ratio

However, I can be satisfied, as in absolute terms it’s low and above all, it has been decreasing over the past 5 years. Free cash flow is also high and has been trending higher since 2019. The company has a long runway in case of an adverse market event.

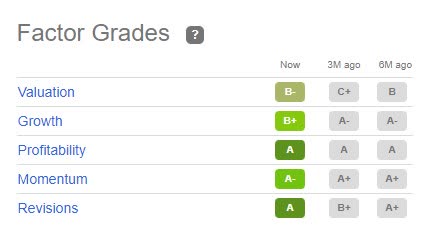

Quant Rating

The Quant rating for ONSemi is a strong buy and I fully agree. Of the 5 factors involved in the rating 2 have improved, 2 have decreased, and one has remained stable from 3 months ago. Profitability and momentum have an A and A-. Those factors are the ones that stand out to me also.

Seeking Alpha

ONSemi Technicals

The medium-term outlook from my technical viewpoint is positive. The weekly chart shows the stock price is in a bullish trend. The current bullish trend started in mid-October when price action broke above the Ichimoku cloud.

Since then, the stock price has proceeded to print higher highs and lows and remain above the cloud. The two-week dip of price action below the cloud is not a break into bearish territory. That’s because the system was not completed by a follow-through of the lagging line (green line).

The RSI is also beginning to show upward momentum as it is currently above 50, and about to cross above its moving average. There was a large increase in volume for the week of June 13, 2022. However, short volume is only at 6.06%.

TradingView

The day chart is a little concerning and may leave room for some downside price action. The stock price is currently below the cloud and is testing the resistance level at the bottom of the cloud. For the short-term bullish trend to return we would need to see price break above the cloud.

Along with the price above the cloud, the other components would need to turn bullish also for confirmation. While the RSI is already giving a signal of bullish momentum having crossed the 50 level and above its moving average.

TradingView

Conclusion

I see a very healthy company with EBITDA growth having tripled since 2020, along with an almost ten-fold increase in EPS since 2020. And the free cash flow gives the company plenty of margin to weather a major storm.

The developments in the semiconductor industry show potential for strong growth in the demand for the company’s products. It also seems well-placed to cover those demands and scale up production when needed.

I see this stock reaching $85, even if there is a slowdown in the economy overall. The increase in demand for 5G and EVs in my opinion would offset that downfall.

Be the first to comment