grinvalds

My focus for early 2023: pick out winning rebound plays in the tech sector that are strongly aligned to the “growth at a reasonable price” trade. Many very high-quality software companies experienced precipitous falls in stock price last year, and once market volatility around interest rates and macro softening starts to subside and investors begin to take on risk again, these companies should see a healthy recovery.

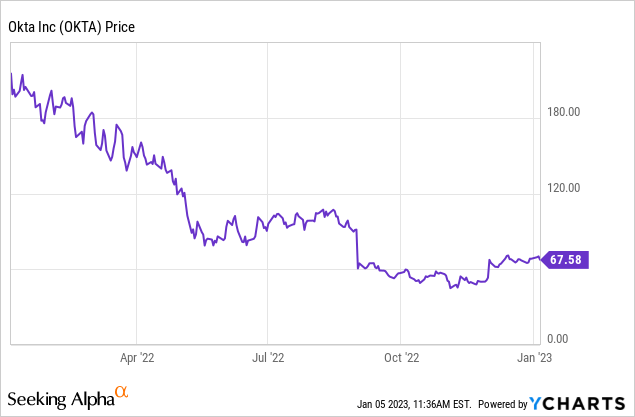

This is especially true of stocks like Okta (NASDAQ:OKTA), which have fallen far from being a Wall Street favorite and now have plenty of “valuation rope” to move higher. Okta, for investors who are unfamiliar with the name, is the premier software brand in single sign-on – which is how many corporate employees access internal applications and websites. Down more than 65% over the past year, Okta has nevertheless continued to deliver strong earnings, demonstrating both rapid growth despite its large scale as well as progress toward meaningful profitability.

Owing to the steep decline in Okta shares, plus the company’s ability to sustain impressive growth rates even after it moves past comping the acquisition of Auth0 in Q2 last year, I am upgrading Okta to strong buy. I additionally think the company’s above-breakeven pro forma profitability is a strong distinguisher in a relatively more risk-averse market.

Here is my full bullish thesis for Okta:

- Despite its massive scale, Okta is still able to grow at an incredible pace. Once most companies reach a $1.5-$2.0 billion revenue scale, their growth typically slows down to the high teens or 20% range. Okta, meanwhile, is still managing to grow ~35-40% y/y on an organic basis. This is a reflection of both the company’s strong execution plus the attractiveness of the IAM market.

- Huge $80 billion TAM. Okta estimates its total addressable market at $80 billion, which means its current revenue scale is only about ~2% penetrated. It’s also the clear market leader here, with competitors like OneLogin and Duo Security being smaller and lesser-known entities.

- Horizontal product. Okta is a true “horizontal” software company whose product is applicable to companies of any size in any industry.

- Recurring revenue and high net retention rates. All of Okta’s business is in recurring subscriptions; in addition, the company’s seat-based pricing plus its multiple modules lend themselves nicely to its >120% net revenue retention rates. In short, Okta has a very stable subscription revenue base that is a powerful growth engine from within the current install base.

- Profitable bones. Okta has achieved above-breakeven pro forma operating margins, on top of positive free cash flow. The company’s tendency to upsell aggressively into its client base also gives it excellent operating leverage.

From a valuation perspective: at current share prices just below $68, Okta trades at a market cap of $10.86 billion. After we net off the $2.47 billion of cash and $2.20 billion of debt from Okta’s most recent balance sheet, the company’s resulting enterprise value is $10.59 billion.

Meanwhile, for FY24 (the fiscal year for Okta ending in January 2024), Wall Street has a consensus revenue expectation of $2.16 billion, representing 18% y/y growth. Considering Okta is currently clocking in at a mid-30s growth rate in both billings and revenue, I think the implied deceleration here is rather sharp. Nevertheless, taking consensus at face value, Okta trades at just a 4.9x EV/FY24 revenue multiple. Recall that during its pandemic heights, Okta traded at a high-teens multiple – and though I don’t think Okta will ever scale those heights again, I do think Okta’s combination of strong top-line growth plus margin accretion call for at least a high single-digit multiple.

My price target on Okta is at 8x EV/FY24 revenue, representing a $112 price target (where Okta traded last May, and representing ~65% upside to current levels). I recommend that you buy this fantastic software name while it’s still trading cheaply.

Q3 download

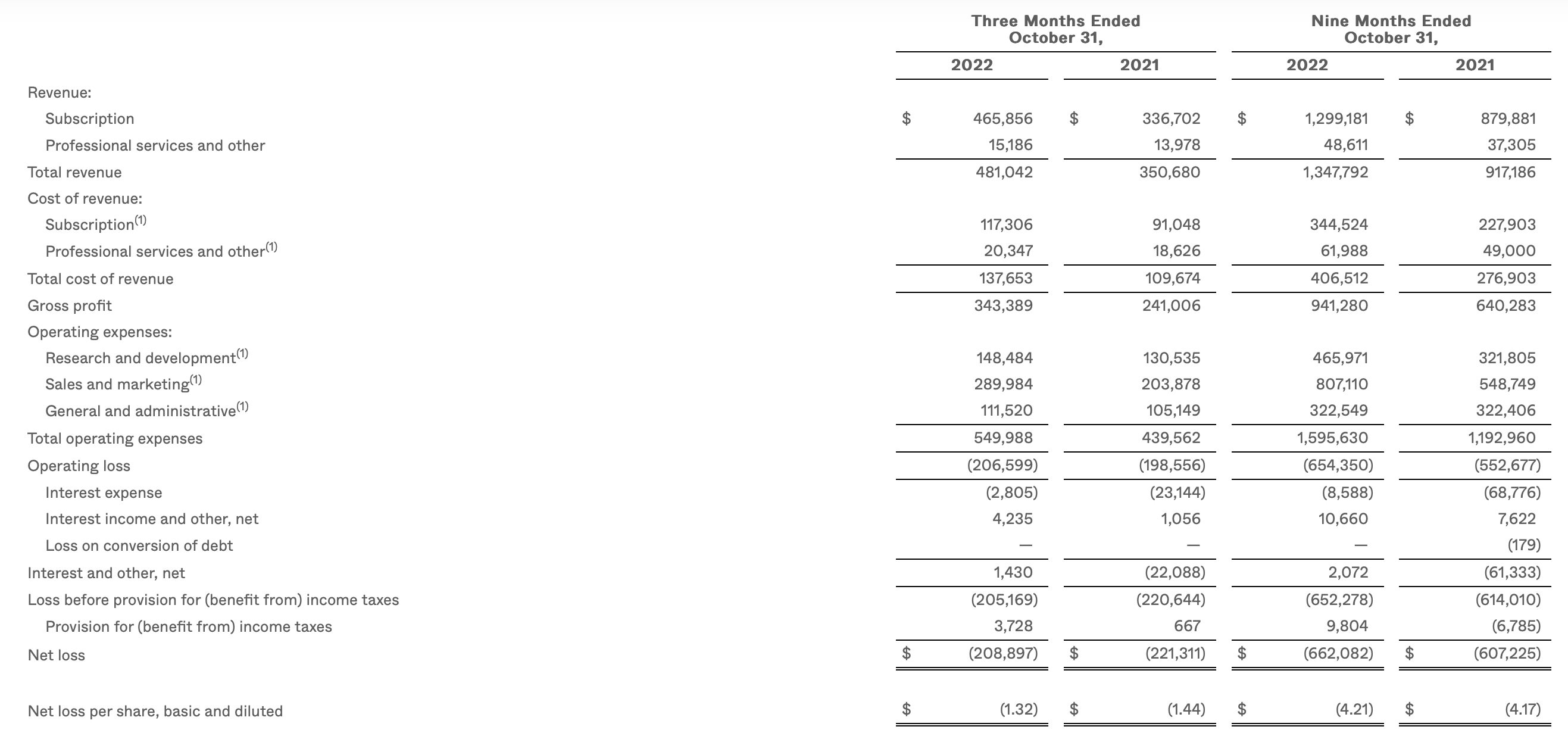

Let’s now go through Okta’s latest Q3 results in greater detail. The Q3 earnings summary is shown below:

Okta Q3 results (Okta Q3 earnings release)

Okta’s revenue grew 37% y/y to $481.0 million, beating Wall Street’s expectations of $465.3 million (+33% y/y) by a strong four-point margin. Note that earnings beats in the back half of 2022 have been fewer and farther between, especially for tech names. Also note that Okta’s reported growth is now entirely organic, as the company has comped the Q2 acquisition of Auth0 last year.

The company added 650 net-new customers in the quarter, bringing its total customer base to over 17K, up 22% y/y. Management also noted especially strong performance in the public sector, which grew 65% y/y helped by a large federal agency deal covering tens of thousands of employees.

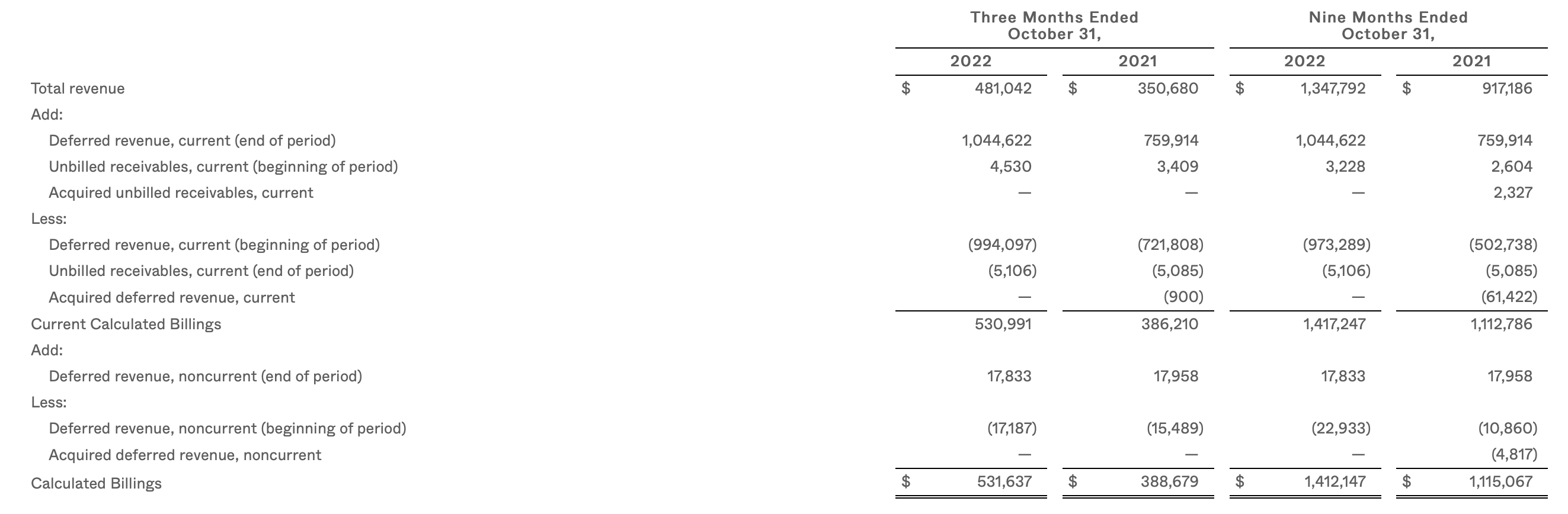

Okta also continued to build up its deferred revenue backlog, with billings of $531.7 million growing 37% y/y, on pace with revenue growth. As seasoned software investors are aware, billings represents a better way to look at a company’s longer-term growth trajectory, as it captures deals signed in the quarter that will be recognized as revenue in future quarters. Okta’s 37% y/y billings growth rate, to me, makes it seem unlikely that revenue growth will decelerate to the mid-teens in FY24 as implied by consensus estimates.

Okta billings (Okta Q3 earnings release)

Now to be fair, Okta’s FY24 preview also does bake in revenue deceleration to the high teens – driven both by anticipation of macro headwinds plus turnover from the company’s sales leadership change. Per CFO Brett Tighe’s remarks on the Q3 earnings call:

From a revenue perspective, we are factoring in the execution challenges we faced this year, the go-to-market leadership transition and the growing uncertainties of the macroeconomic environment. We estimate total revenue to be in the range of $2.130 billion to $2.145 billion or growth of 16% to 17%.

While we had initially planned on providing an update on our long-term targets, we believe it’s prudent to wait and revisit this once we have increased visibility and confidence in the macro environment, new global field operations leadership in place and have made more progress on the integration.”

I’d say at the very least, however, that estimates are now fully de-risked and Okta has set a pretty low bar for itself to cross in FY24.

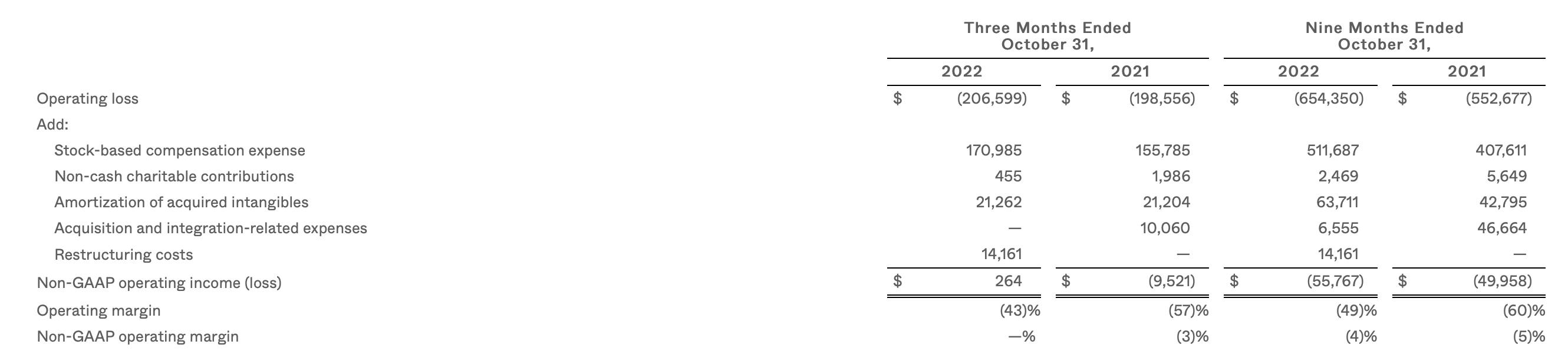

From a profitability perspective, the company achieved a breakeven pro forma operating margin in Q3, up three points from -3% in the prior-year Q3. This was helped by two points of pro forma gross margin gains, as well as spend reduction actions that the company implemented in Q3.

Okta margins (Okta Q3 earnings release)

Looking ahead to FY24, the company expects pro forma operating margins to tick up to the “low single digits”, and Okta also expects to deliver a “meaningful” boost to free cash flow.

Key takeaways

Growth at scale, a sticky and expandable product that is applicable to all industries, a path toward boosting profitability, and a very modest valuation: these are all the key reasons to be invested in Okta. Stay long here.

Be the first to comment