Ignatiev

Article Thesis

Nvidia Corporation (NASDAQ:NVDA) has just reported its most recent quarterly results. Profits were below expectations, but overall, results were more or less in line with what the market had anticipated, as Nvidia had pre-announced some of its results not too long ago.

The company’s guidance for the current quarter is much worse than expected, however. Nvidia is clearly feeling hefty pressure from the current crypto winter, and it seems questionable to pay $170 or more per share of Nvidia in the current environment.

Q2 Was Worse Than Expected

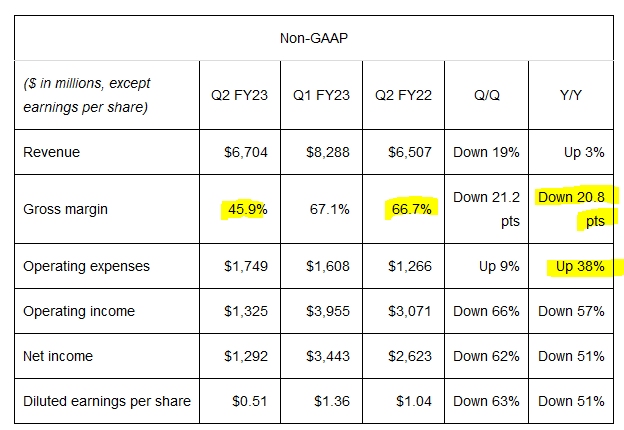

Nvidia had pre-announced its revenue results for the second quarter earlier, thus there was no major surprise there – analysts adjusted their models accordingly, and Nvidia met the consensus estimate:

Seeking Alpha

But the company nevertheless missed estimates, as margin compression was worse than expected. In fact, Nvidia saw its gross margin drop massively, showcased by the following table:

Seeking Alpha

The company’s gross margin dropped from a very attractive 67% to a much less attractive 46% over the last year, almost being cut in half. A 46% gross margin isn’t disastrous in absolute terms, but the hefty margin drop naturally has a huge impact on Nvidia’s profitability.

Nvidia was widely regarded as a high-end semiconductor company that was able to generate very strong margins due to its excellent product quality. But at least for now, that has apparently ended, as its gross margin is far lower than what we have gotten used to in recent years.

At the same time, Nvidia also saw its operating expenses explode upwards. This includes research and development, sales, but also administrative costs. While Nvidia was able to grow its revenue by 3% year over year, operating expenses somehow rose by almost 40% – or around 13x as much as the company’s revenue. That is pretty bad, and it is not clear why that happened. Higher R&D expenses aren’t bad per se, at least if those result in strong products that improve the longer-term growth outlook.

But for a growth company like Nvidia, investors generally want to see operating leverage, meaning operating expenses grow less than revenue and gross profit, as this allows a company to grow its profits faster than its sales. The complete opposite of that happened here, as gross margins dropped severely while operating costs rose much more than Nvidia’s sales and gross profit. The steep profit decline of more than 50% is the logical consequence of that ill-timed increase in Nvidia’s operating expenses.

With earnings per share at $0.50 for the quarter, Nvidia’s EPS is running at a $2 annual rate. That will most likely drop even further in Q3, as indicated by the pretty weak forward guidance (more on that later). Profits are now back at the level seen in early 2020 when earnings per share were in the $0.50 range as well. It’s important to note that Nvidia was trading at as low as $50 back then, whereas Nvidia is trading at $170 right here — or more than 80x the Q2 earnings run rate.

These are Nvidia’s non-GAAP results, where items such as share-based compensation are already backed out. GAAP profitability was even worse, as GAAP earnings per share came in at $0.26 — or around $1 annualized, for a 170x earnings multiple. That’s quite expensive for a company with a 3% top-line growth rate.

Nvidia’s Forward Guidance Is Horrendous

I want to note first that I do believe that Nvidia is a quality company with a positive long-term outlook, thanks to its strong position in growth markets such as AI, autonomous driving, etc. I also want to note that I have been a bull on Nvidia in the past, and shares are up since my last bullish article. But when the facts change and the underlying performance is much worse than previously thought, then it makes sense to reflect one’s formerly bullish stance.

Nvidia’s guidance for the current quarter, Q3, was very bad. The company is forecasting revenues of $5.9 billion for the period, which is not only $1 billion or 15% below the current consensus estimate, but which also indicates a revenue decline of 16.9% versus last year’s Q3 revenue of $7.1 billion. That is comparable to Intel’s (INTC) revenue decline during the most recent quarter, as Intel reported a drop of 17.3% in its top line for the period. In other words, Nvidia is forecasting a revenue drop that is comparable to the one Intel has just reported — the huge difference is that Nvidia trades at 2.1x forward sales, whereas Nvidia trades at 15x forward sales, which is a 600% premium relative to how Intel is valued.

There are good arguments for Nvidia to trade at a premium versus Intel, such as its stronger position in the fast-growing data center market, where Nvidia saw its revenue rise by 60% in Q2, while Intel’s data center dropped. But whether it makes sense for Nvidia to trade at a 600% premium on a sales basis, relative to Intel, while both are seeing their revenues drop, is highly questionable, I believe.

What’s the explanation for the hefty revenue decline that Nvidia forecasts for the current quarter? It’s not the overall semiconductor market, that’s pretty clear, as the World Semiconductor Trade Statistics, or WSTS, has just announced that overall semiconductor revenues would climb 14% in 2022. When Nvidia’s revenues are falling by double-digits, while the broad semiconductor industry is growing by double-digits, then there must be other factors at work. In Nvidia’s case, that’s the current crypto winter. While Nvidia’s chips were useless for Bitcoin mining, they were excellent for Ethereum mining due to the algorithm Ethereum uses, which is very GPU-friendly. With crypto prices plunging in 2022, Nvidia is feeling pressure due to two reasons.

First, the company can sell fewer chips to crypto miners, as Ethereum mining has become less profitable, which is why demand dropped. At the same time, less demand by crypto miners results in a looser supply-demand picture, which leads to price declines for GPUs. This is further accelerated by the fact that some crypto miners are selling the GPUs they own on secondary markets, which further pressures pricing for new GPUs.

Due to the current crypto winter, Nvidia is thus feeling a double hit from lower sales volumes and lower average margins. That’s luckily partially made up by the strong performance in other areas, such as data centers. But as the weak guidance for the current quarter shows, Nvidia is not able to fully offset the headwinds from the weak crypto environment. It thus looks like investors have to come to terms with the fact that Nvidia’s strong underlying performance was at least partially driven by crypto enthusiasm. Now that crypto has been in a downtrend for some time, that former tailwind is turning into a headwind.

What’s The Outlook?

In the very long term, Nvidia will still be a solid growth company, I believe. Data center demand will continue to grow. Autonomous driving is a long-term megatrend that will lead to rising demand for Nvidia’s Hyperion platform and similar products. But in the near term, the outlook is far from great.

Since Nvidia is trading at a pretty high valuation of 46x forward earnings, even before those earnings estimates have declined due to the weaker-than-expected Q3 guidance, I do not believe that Nvidia is a great investment at current prices. There are other semiconductor companies with way better near-term growth outlooks that trade at less than half Nvidia’s earnings multiple, such as AMD (AMD), Broadcom (AVGO), Qualcomm (QCOM), and so on. With those picks being available today, I do not see a great reason to buy Nvidia right now. The long-term outlook is positive, but the near-term issues and too-high valuation make me stay away for now.

Be the first to comment