Andrew Linscott/iStock via Getty Images

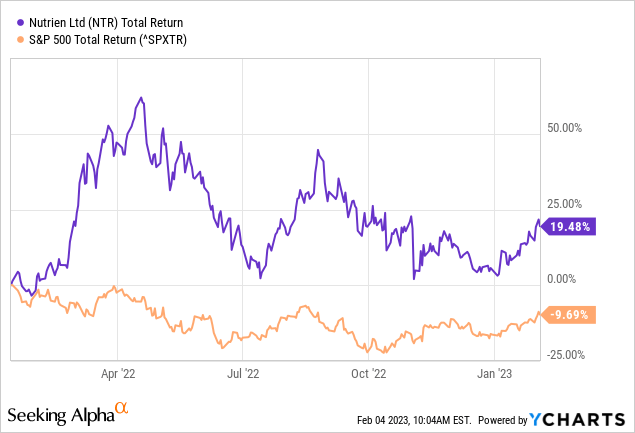

I last mentioned Nutrien (NYSE:NTR) in January 2022 here, as a play on rising grain prices. Then, Russia invaded Ukraine, throwing a monkey-wrench into both the regular supply of grains and fertilizer product, while eventually spiking the cost of natural gas, a key ingredient for nitrogen fertilizer. In summary, prices for farming food inputs spiked and the world’s fertilizer makers saw a sizable upturn in business results. On dramatically higher sales and earnings, Nutrien was able to generate a +19% total return for shareholders since my 2022 article was published vs. a -10% loss equivalent in the S&P 500 index. Share performance has definitely been a success story and one that may be repeated in calendar 2023.

YCharts – Nutrien vs. S&P 500 Total Returns, Since January 2022

The logic for my current optimism is twofold. The first is the valuation story has improved markedly over 13 months. The second is Nutrien’s price changes are less correlated to S&P 500 fluctuations than the typical equity. Plus, the farm economy (including grain and fertilizer prices) marches to a different beat than the regular economic cycle, which is a good thing as we slide into recession.

Strong Valuation Argument

Basically, the late 2022 and early 2023 valuation of underlying business operations for Nutrien is the lowest since the company was formed through the 2018 merger of Agrium Inc. (Agrium) and Potash Corporation of Saskatchewan Inc. (PotashCorp).

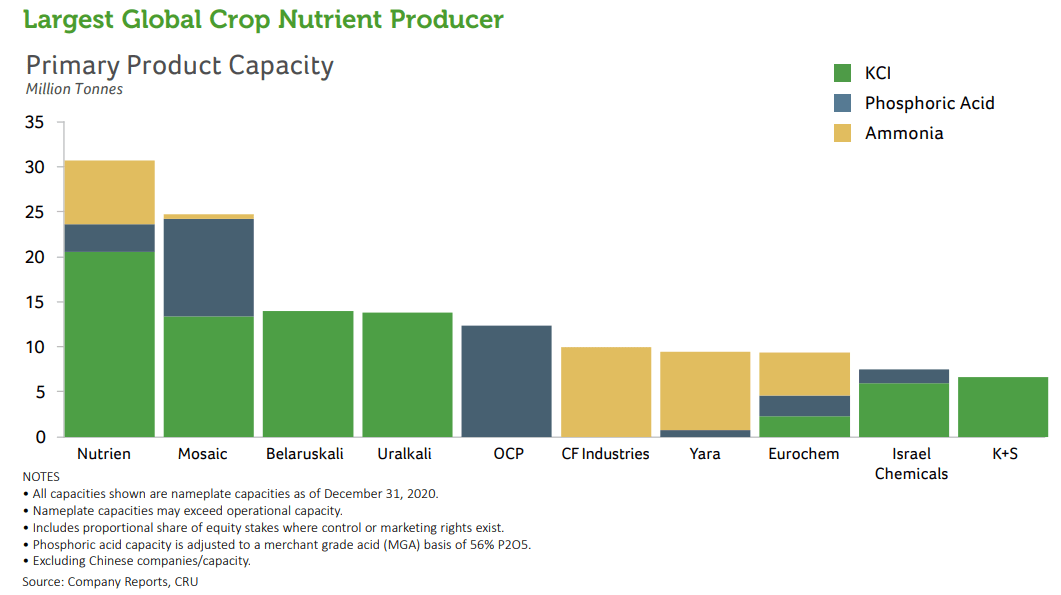

According to the company’s website, Nutrien produced and distributed over 27 million tonnes of potash, nitrogen and phosphate products for agricultural, industrial and feed customers worldwide, selling to 500,000 businesses/individuals. The corporation ranks as one of the biggest fertilizer concerns on the globe. All of its production assets are located in North and South America.

Nutrien 2022 Fact Book – World’s Largest Fertilizer Producers

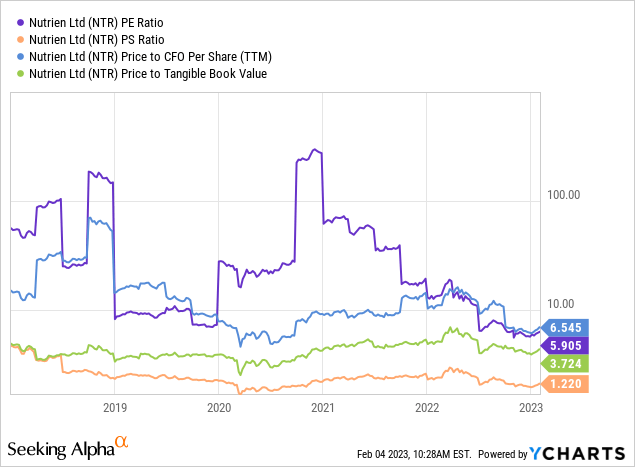

Below is a valuation graph of basic fundamental ratios using price to trailing operating results. You can see that extended fertilizer pricing in 2022 was a boon for the business, yet the stock quote has only risen modestly, compressing multiples.

YCharts – Nutrien, Price to Trailing Fundamentals, Since 2018

On price to trailing earnings, sales, cash flow, and tangible book value in combination, the stock is selling for an approximate 40% discount to its 5-year average since formation. In the end, the share quote appears to be discounting a peak in results last year, with the size of a downturn open to debate. To a degree, this cycle prediction makes sense.

However, fertilizer prices could remain high (or move even higher), if one of a number of circumstances surprises conventional wisdom. (1) The global economy may survive the year without a meaningful recession helping overall food demand, (2) a large weather-related drought in South America, North America, Asia, or Europe hits this year keeping grain prices and farm income near peaks, or (3) Russia’s military conquests disrupt fertilizer supply further.

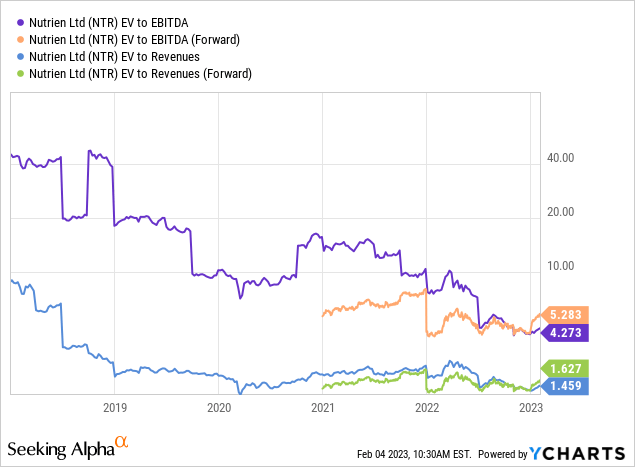

When we include debt and cash holdings, Nutrien appears to have yet stronger long-term worth on enterprise value calculations. If we assume future 2023-24 results beat current estimates, EV to EBITDA (5x) and revenue (1.5x) stats are “cheaper” than a year ago, trading at a level 80% lower than when the company was formed in 2018.

YCharts – Nutrien, EV to EBITDA & Revenues, Since 2018

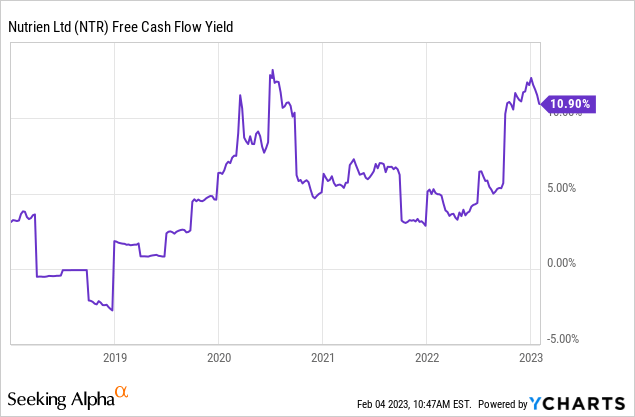

Lastly, free cash flow numbers are usually hard to generate in the capital-intensive mining and manufacturing industries. The excellent management of world-class assets and minimal debts has been a keystone of the Nutrien ownership story, with low-cost production and CapEx spending limited to numbers less than cash flow returns. Below is a graph of the free cash flow yield of 11% on trailing results. The long-term average of 5% since 2018 is actually a superb number, with its decades of resource assets expanding in value with inflation over time.

YCharts – Nutrien, Free Cash Flow Yield, Since 2018

Recession Survivor?

The 40-year record “inversion” spread of the U.S. Treasury yield curve in late 2022 and early 2023 cannot be easily disregarded by Wall Street and main street investors alike. I know the January rally in the equity market has everyone excited the worst of the high inflation environment is behind us. Perhaps this is true. But, if our economic background is replaced by lower corporate profits and rising unemployment throughout the year, your logic for bullish stock market views may be shortsighted.

During prolonged and serious recessions, falling inflation and interest rates are the manifestation of imploding demand forces. Unfortunately, rotten final demand in record-debt situations (the U.S. and world are carrying near record debt to GDP output in early 2023), including dropping income/wages and weakening asset wealth (backward price moves in real estate and stocks) are typically reversed by emergency central bank interventions. Since we are nowhere near a Federal Reserve pivot to easing monetary policy, a whole new round of economic problems will have to develop first.

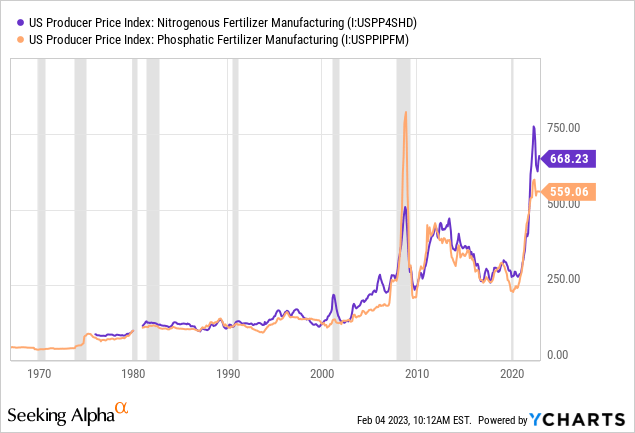

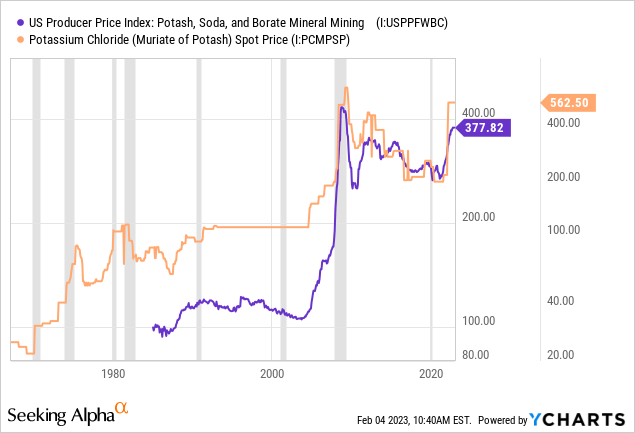

The best news for Nutrien shareholders is fertilizer markets are not always zigzagging in the same direction as the general economy. Below are graphs of fertilizer prices since 1967, measured against recessions, shaded in grey. You will notice recessions do not always lead to lower fertilizer prices. It’s close to a 3-way tie for what will happen, balanced between rising, falling, and flat prices.

YCharts – Nitrogen & Phosphate Price Trends, Since 1967, Recessions in Grey Shading

YCharts – Potash Price Trends, Since 1967, Recessions in Grey Shading

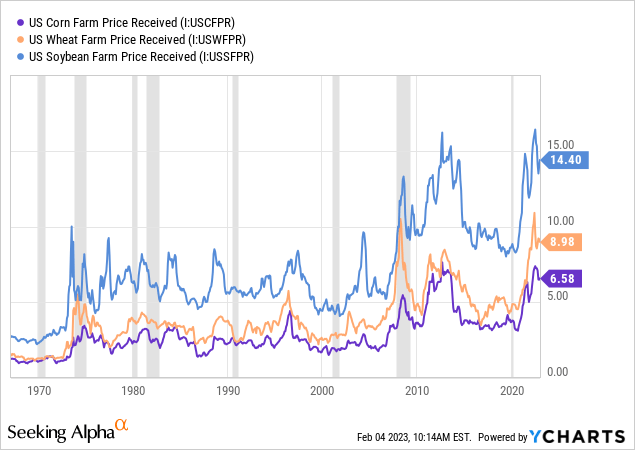

Grain prices for corn, wheat, and soybeans have worked roughly the same for recession reactions. One conclusion you can draw from the charts is price spikes occurring just before a recession (2022 in our case) usually retrace gains during and after the recession, although this did not take place in 1973-74. If we didn’t have to deal with Russian aggression affecting supply, or climate change affecting growing seasons and crop yields, I would be inclined to forecast weaker fertilizer prices in 2023-24.

YCharts – Corn, Wheat, Soybean Prices per Bushel, Since 1967, Recessions in Grey Shading

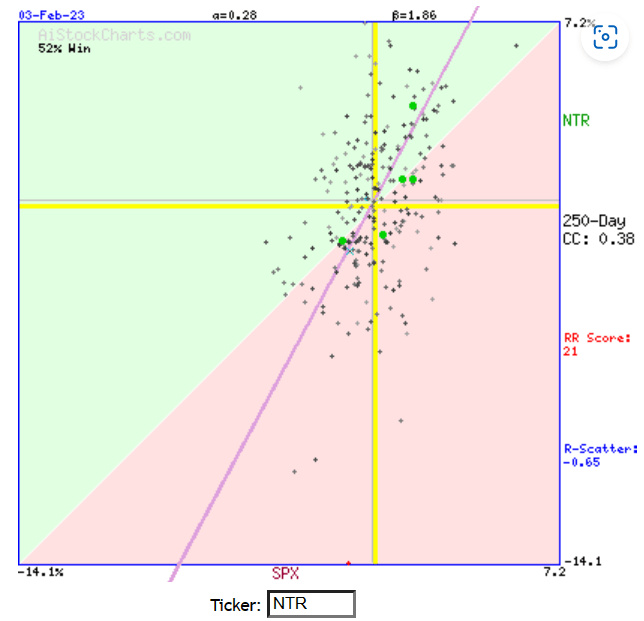

For Nutrien specifically, daily trading over the last year has resulted in little direct correlation to S&P 500 movements, instead tracking fertilizer market changes. According to AiStockCharts, more than 86% of the variation in NTR daily price change was due to factors other than S&P 500 daily changes. Below is a dot plot of the idea over the last 250 trading days, with a correlation coefficient of 0.38 (where 1.0 lines up directly with the S&P 500).

AiStockCharts.com – Nutrien Daily Correlation Chart to S&P 500, 1 Year

Constructive Technical Chart

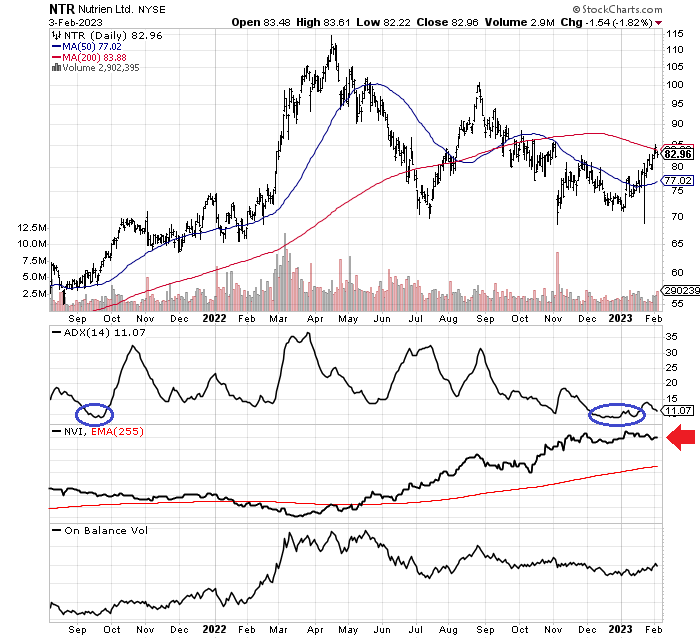

Another piece of the investment puzzle to review is trading patterns in Nutrien shares. Several momentum indicators point to a rosier future. The 14-day Average Directional Index (a measure of daily volatility and price change) has been highlighting a near balance in supply and demand for shares. The last time a score under 10 appeared was at an important price bottom in September 2021. Both instances are highlighted with blue circles on the 18-month chart below.

Another major positive to me is found in 2022’s rising trend for the Negative Volume Index (marked with a red arrow). The pattern is telling us plenty of buying-on-weakness has been taking place. The opposite NVI movement has been part of the heavy selling in Big Tech names. I would rather own a company with steady buying on lower volume days.

My last indicator to review is On Balance Volume. The long-term trend has been quite positive, although changes in December and January do not signal any hurry by investors to sell or buy the stock. My interpretation of the whole technical picture is Nutrien is well established at the current quote, just waiting for the next major move in farm economy/fertilizer pricing.

StockCharts.com – Nutrien, 18 Months of Price & Volume Changes, Author Reference Points

Final Thoughts

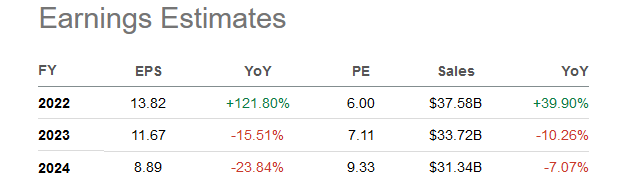

Rumors of a new wave of Russian troops invading eastern Ukraine have been widespread this past week (between 300,000 and 500,000 have amassed near Ukraine’s eastern border according to reports). It is entirely possible, not just an outlier event prediction, new military struggles in Europe could further exaggerate imbalances in fertilizer supplies to that continent while forcing a real shortage situation on the rest of the world. In such a scenario, fertilizer stocks like Nutrien could be substantial gainers in value as investors flock to sharply rising industry profitability, well above 2022’s existing exceptional result. My view is that current analyst estimates for a downturn in fertilizer pricing during 2023-24 may be understating how fertilizer markets will behave in the real world.

Seeking Alpha Table – Nutrien, Analyst Estimates for 2022-24, Made on February 3rd, 2023

So, Nutrien buyers are getting significant upfront value on their investment, noncorrelated future performance to the S&P 500 and normal recession cycles in the economy, plus an upside kicker/hedge if the fertilizer supply chain in the world is disrupted more than last year. What’s not to like?

I am modeling worst-case scenario downside to $65 a share (a new low for the year), if the fertilizer marketplace is able to follow a normalized rebalancing cycle of global supply/demand during an economic recession in the U.S. However, upside targets back to new all-time highs in the $115 to $120 area seem appropriate with all the Russia noise. If the company can earn $14+ for EPS in 2023, today’s $83 price (6x P/E) is way too low.

Using “average” fundamental multiples since 2018 backed by new Russian aggression, I can forecast Nutrien quotes as high as $150 per share. So, my simple risk-reward analysis projects a range of potential outcomes from a total return loss (including its above-average 2.3% in dividends annually) of-20% over the next 12 months to a theoretical gain of +80%. The price and valuation setup is very sound for bulls, in my opinion. It may be sitting in a much stronger position than Wall Street analysts understand. I rate Nutrien a Buy.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Be the first to comment