kali9/E+ via Getty Images

Investment Thesis

Nucor (NYSE:NUE) is a well-positioned steel manufacturing company, with solid near-term prospects.

Since my last bullish analysis of Nucor, so much has happened. Here I’m obviously discussing Nucor’s preannounced its Q2 2022 results where Nucor asserts that investors will see record earnings for the quarter.

Also, the preannounced results gave investors visibility into its capital allocation strategy. In this analysis I discuss what investors should think about.

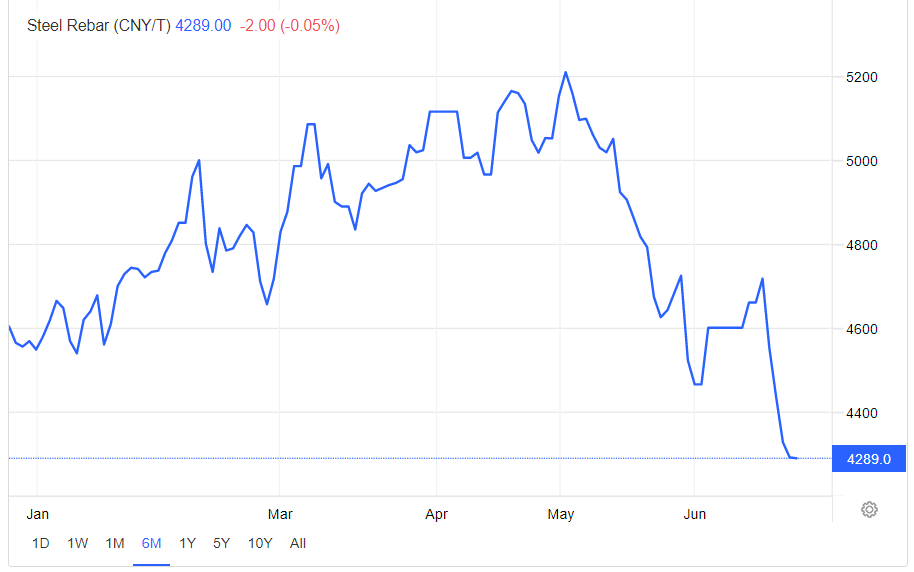

But going beyond that, there’s a lot to think about. Least of all, that steel prices have fallen by circa 5% in the past week.

The reason for steel prices falling have obviously coincided with increasingly pervasive fears that the US is about to enter a recession.

Nevertheless, while acknowledging that there are countless headwinds at play and that this investment is far from a home run, I still argue that there’s a lot to be excited about this investment.

Here’s why I rate this stock a buy.

Nucor Preannounced Q2 Results

As mentioned in the introduction, Nucor preannounced its Q2 2022 results, noting that it expects its EPS to come in at the mid-point of $8.80. This is an increase of 14.7% from $7.67 reported in Q1 2022.

This record EPS number comes on the back of the previous record result in the previous quarter.

Put another way, even though the share price is down since the end of Q1 by approximately 18%, the EPS number is up nearly 15% sequentially.

Now, let’s understand why the share price is down.

Bearish Considerations to Consider

There’s the expectation that a slowing economy will lead to a rapid build-up in steel products. This is a substantial risk that has many investors on hedge. What’s more, recent comments from the Fed, particularly when it comes to potentially hiking interest rates soon again have led many to believe that a recession is now imminent.

However, I would push back that there are different levels of recessions. Some are deeper than others.

Indeed, there’s a possibility that steel demand may not be significantly dampened, particularly once President Biden’s $1.2 trillion infrastructure bill gets rolled out.

Trading Economics

Nevertheless, steel prices do appear to be moving lower, particularly since the Fed’s meeting last Tuesday where interest rates were hiked by 75 basis points.

Those are the bearish considerations. Next, let’s discuss the bullish arguments.

Capital Allocation Strategy, Estimated at 13.1%

Recall that Nucor’s balance sheet at the end of Q1 had approximately $2.4 billion of net debt.

Given that Nucor made approximately $2 billion of free cash flow during Q1, I suspect that Nucor’s free cash flow in Q2, which was a record quarter after all, should at least come close to $2 billion of free cash flow again.

Hence, I estimate that Nucor’s balance sheet will end Q2 with approximately $1 billion of net debt, after returning capital to shareholders.

Indeed, we know that Nucor repurchased approximately $900 million worth of stock in Q1. We also know that Nucor repurchased $803 million worth of stock in Q2 (5.1 million shares * $157.37 per share).

Accordingly, including its dividend allocation, during H1, Nucor’s capital return program returned $1.9 billion to shareholders.

This implies that if annualized this total return, we are looking at somewhere near 13.1% total return.

Needless to say that this is an estimate since we don’t know what steel prices are going to be for the remainder of 2022. If steel prices continue moving lower, this capital return program could also diminish.

NUE Stock Valuation – Priced 4x EPS

For H1 2022, Nucor’s EPS reached $16.77. If we use analysts’ consensus estimates for H2 2022 of $11.55, that means that Nucor is expected to reach $28.32 in 2022.

That puts the stock priced at 4x its 2022 EPS.

Obviously, the main risk here is that typically you don’t want to buy steel companies or commodity companies in general when the multiple is low, because that often means that it’s the end of earnings cycle.

Indeed, analysts continue to expect that once we get towards the end of 2022 and into 2023, that Nucor’s strong earnings could revert lower.

The Bottom Line

There are a lot of moving parts when it comes to Nucor. On the one hand, investors are fearful that in an economic recession demand for steel would be reduced.

Along these lines, there’s the expectation that earnings have now reached a peak and as we move forward from Q2, Nucor’s earnings will start to revert lower.

On the other hand, the business is clearly making a lot of free cash flow and I estimate it’s priced around 4x free cash flow, or even slightly lower.

On the other hand, Nucor recognizes these headwinds and is returning meaningful capital to shareholders via dividends and buybacks. In fact, I estimate that Nucor will return 13.1% capital to shareholders in 2022.

In essence, the business is clearly generating a lot of free cash flow and is cheaply priced. Hence, I’m rating this stock a buy.

Be the first to comment