At the beginning of September, we wrote here about an impeding tender offer in the Tortoise Midstream Energy Fund, Inc (NYSE:NTG). Specifically, the Tortoise Midstream Energy Fund management team was trying to address the persistent discount to NAV by targeting share retirements via tender offers:

OVERLAND PARK, KS / ACCESSWIRE / August 10, 2022 / Tortoise and the Board of its closed-end funds previously announced its approval of conditional tender offers as part of the discount management program. A Fund would conduct a tender for 5% of the Fund’s outstanding shares of common stock at a price equal to 98% of net asset value if its shares trade at an average discount to NAV of more than 10% during either of the designated measurement periods. The first measurement period for 2022 ended on July 31, 2022 and it has been determined that a tender offer will be executed in each fund. The tender offers are expected to commence on or around October 3, 2022. The Funds will issue a press release announcing the tender offers on the day the tenders commence. The Funds’ portfolio managers, officers and Board of Directors will not tender their shares. The second conditional tender offer measurement period is from August 1, 2022 through July 31, 2023.

In our article, we discussed the opportunity for investors to take advantage of the corporate action and the expectation for the premium to NAV to narrow. The results are now in for the tender offer, and we are going to have a closer look at the fund’s performance and specifically the performance of the discount to NAV.

Tender Offer Results

Tortoise just announced the results of their tender offer:

OVERLAND PARK, KS / ACCESSWIRE / November 2, 2022 /

Tortoise announced today the preliminary results of cash tender offers for each of the following Funds that expired at 5:00 P.M., Eastern Time on November 1, 2022.The table below shows the preliminary results for each Fund. Shares Properly Purchase Price of Fund Tender Offer Amount Tendered Properly Tendered Shares*

Grid (Tortoise)

* Equal to 98% of the relevant Fund’s net asset value per share as of the close of regular trading on the New York Stock Exchange (NYSE) on November 1, 2022 (the date the Tender Offer expired).

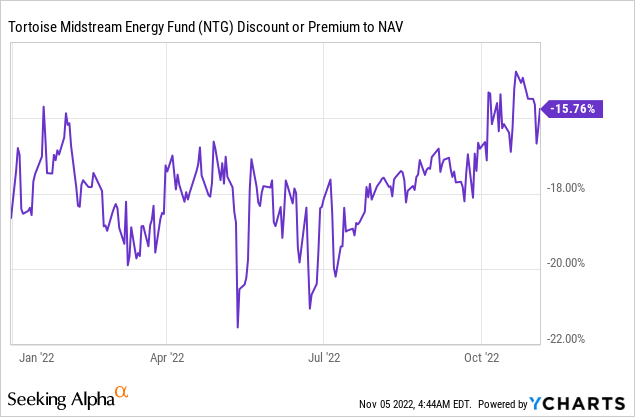

The tender offer represented a medium for the fund management to try to tighten the persistent discount to net asset value. If we have a look at the discount to NAV performance since the announcement, we can see the corporate action succeeded:

Despite the massive risk-off environment witnessed in September, the fund’s discount to NAV continued to tighten, after the June lows. We can see a change in the fund’s beta to the overall market. While during the June market sell-off the fund displayed a widening discount, during the September rout the fund posted a tightening discount. The corporate action worked.

Performance

Since our article outlining the NTG corporate action play, the fund has rallied:

Performance (Seeking Alpha)

The main drivers for the fund rally since the corporate action announcement have been:

positive performance in the MLP asset class

tightening of the discount to NAV for the fund

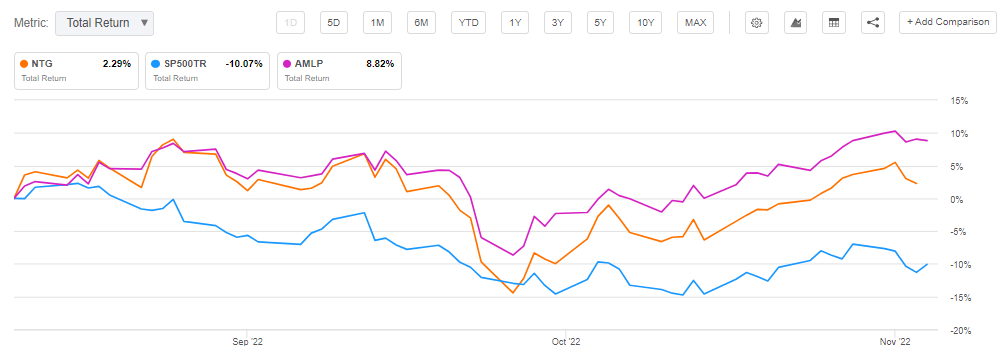

Let us have a look at the total return graph for NTG and the unleveraged MLP ETF AMLP:

Performance since August 10 (Seeking Alpha)

We can see that since the corporate action announcement, the market is up for MLPs, while the overall S&P 500 index is down. NTG lags the overall MLP market performance, but has seen its discount to NAV tighten.

We would like to see more corporate actions like this one for NTG. Recurring tender offers would put a floor, in our view, under the discount to NAV for NTG and provide for a tighter range for the fund’s discount to NAV.

Conclusion

Tortoise Midstream Energy Fund, Inc (NTG) is a closed end fund focused on midstream energy entities. The CEF has traded at very substantial discounts to net asset value after the Covid crisis, discounts which have averaged almost -20%. The reasons behind this trading pattern are the shunning of the MLP asset class by investors and the leverage in the NTG CEF structure, which magnified the down move during Covid. The fund’s management has resorted to tender offers at 98% of NAV in order to tighten the persistent discount to NAV. The most recent offer which just concluded was successful, and the corporate event has resulted in the fund’s discount to NAV to narrow, even during a significant risk-off market event as the one we saw in September. We would like to see more tenders, and we feel playing NTG tender offers for further narrowing of the discount to NAV is a robust strategy. We believe we are in the middle of an energy super-cycle, and the MLP asset class will slowly grind up as companies emerge with stronger balance sheets. We expect NTG’s discount to NAV to further tighten in 2023 and any new tender offer announcements would represent good entry points to trade the corporate action.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment