sdominick/E+ via Getty Images

Speculation is an effort, probably unsuccessful, to turn a little money into a lot. Investment is an effort, which should be successful, to prevent a lot of money from becoming a little.”― Fred Schwed Jr.

Today, we take a look at an intriguing small cap developmental name. The stock has seen a nice rally after a large sell-off and also seen some insider buying lately. An analysis follows below.

Seeking Alpha

Company Overview:

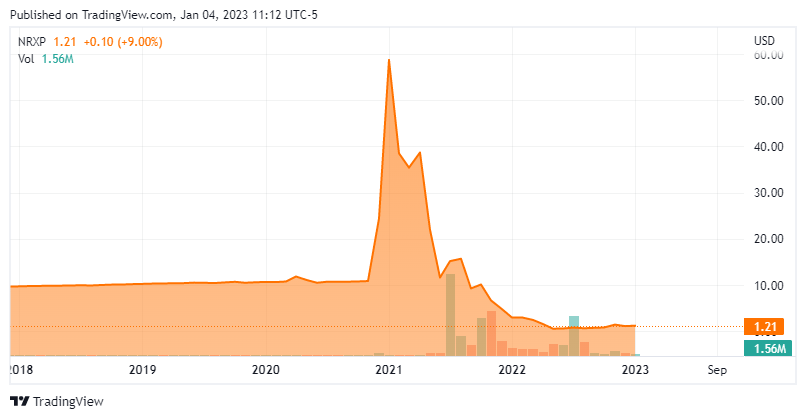

NRx Pharmaceuticals, Inc. (NASDAQ:NRXP) is a Wilmington, Delaware based clinical-stage drug concern focused on the development of therapies for the treatment of psychiatric conditions. It has one primary clinical asset, NRX-101, which is being evaluated as a monotherapy and in combination with ketamine (NRX-100) for the treatment of two bipolar depression indications and post-traumatic stress disorder (PTSD). NRx was founded in 2015 and went public when it reverse-merged into special purpose acquisition company (SPAC) Big Rock Partners Acquisition Corp. in May 2021. The SPAC went public in 2017 with an implied value to its common shares of $9.60. When the merger was first announced in December 2020, Big Rock’s stock skyrocketed to $76.99 a share (intraday), proving the market is sometimes comprised of very irrational participants. Shares of NRXP have revalued to $1.20 a share, translating to a market cap of approximately $80 million.

NRX-101

The company’s raison d’etre is NRX-101, an oral combination of N-methyl D-aspartate (NMDA) antagonist (and broad spectrum antibiotic) D-cycloserine [DCS] and lurasidone, which is a 5-HT2a atypical antipsychotic and antidepressant typically prescribed for bipolar disorder. The NMDA receptor is known to regulate the speed of the thought process: a pace too fast can cause mania; too slow can actuate depression and suicidality. NMDA antagonists have demonstrated antidepressant outcomes but at the expense of addiction, hallucinations, and neurotoxicity. However, NRx believes concurrent blockade of NMDA (preventing psychosis) and 5-HT2a (preventing akathisia (agitation)) can provide relief from depression and suicidality without adverse side effects.

NRX-101’s lead indication is severe bipolar depression in patients with acute suicidal ideation and behavior (ASIB) after initial stabilization with ketamine (NRX-101). It is also being evaluated as a monotherapy in the treatment of bipolar depression in patients with sub-acute suicidal ideation and behavior (SSIB), as well as PTSD. The major difference between ASIB and SSIB is that the former requires hospitalization while the latter does not.

ASIB. NRx initiated a Phase 2b/3 trial for patients with bipolar depression and ASIB in 2017. In the Phase 2 portion of the study (STABIL-B), patients received either NRX-101 or lurasidone after an IV infusion of NRX-100. In the Phase 2 portion, NRX-101 achieved a mean 7.7 point benefit versus lurasidone on the Montgomery-Asberg Depression Rating Scale (MADRS) (p=0.03), a 1.5 point improvement on the Columbia Suicide Severity Rating Scale (C-SSRS) (p=0.002), and a 2.9 improvement on the Clinical Global Impression Suicidality Scale (CGISS) (p=0.002). Perhaps most impressive – albeit not statistically significant – was the lack of relapse in the NRX-101 population (n=10) versus a 40% relapse rate in the control group (2 of 5). Furthermore, hospital stays for patients on NRX-101 were significantly shorter than for those on lurasidone.

Based on the results of this study, NRX-101 received Breakthrough Therapy Designation with a Special Protocol Agreement, which means if NRx can achieve similar results in its 72-patient Phase 3 portion – mimicking the Phase 2 part of STABIL-B, which assessed only 15 patients – it would pave the way for approval. This trial is just initiated and the company is scheduled to have a Type B meeting with the FDA in later this month to align the registrational plans for NRX-101 to target adults with SBP-ASIB.

If approved for ASIB, NRX-101 would be the only approved medicinal therapy for suicidal bipolar depression – the only approved treatment is electroshock therapy. That said, there are over 100 drugs green-lighted for major depressive disorder and treatment resistant depression, as well as five therapies approved for bipolar depression – all of which excluded suicidality patients in their clinical trials. The company puts the domestic market opportunity for NRX-101 in ASIB at ~$600 million.

SSIB. However, ASIB is not the entire story with NRX-101. The SSIB indication actually encompasses more patients than ASIB (500,000 versus 180,000 in a total domestic bipolar market of ~7 million). NRx has entered its lead asset into a Phase 2 study assessing it – taken twice daily – against lurasidone in patients with severe depression (defined as MADRS > 30) and subacute suicidality (C-SSRS of 3 or 4) who have not been previously stabilized on ketamine. Endpoints include depression and suicidality at six weeks. Results from this trial are expected in 1Q23. If eventually approved for SSIB, the domestic market opportunity for NRX-101 would expand by an additional ~$1.6 billion.

PTSD. In addition to suicidal bipolar depression, NRx is pursuing the PTSD indication through NRX-101. After one of its components [DCS] demonstrated the ability to extinguish recurring images of traumatic events (a.k.a. fear memory) in preclinical murine models, the company elected to enter NRX-101 into a Phase 2 trial, which should initiate in 4Q22. There is clearly an unmet need as more than four times as many servicemen and women have succumbed to suicide than died in combat since 9/11. There are no approved therapies specifically designed to treat PTSD symptoms, only selective serotonin reuptake inhibitors for depression, which have black boxed warnings for suicidal tendencies and do not address fear memory. With ~10% of the nine million PTSD sufferers in the U.S. presenting suicidality, an FDA approval could significantly raise the market opportunity for NRX-101 – by as much as $5 billion.

Share Price Performance

With encouraging results for its lead asset to date and two important data readouts coming over the next ten months totaling a blockbuster market opportunity, the question becomes, “why is NRx’s market cap sub-$100 million?” Part of the answer lies in the company (and investors) getting sidetracked by the ‘easy money’ in Covid-19. The company inked an agreement with Swiss concern Relief Therapeutics (OTCQB:RLFTF) to commercialize a reformulated (sterile liquid) version of ZYESAMI (aviptadil acetate) for the treatment of patients with critical Covid-19 and respiratory failure in October 2020. When the company went public, it did so on the back of the NYESAMI narrative, essentially forsaking NRX-101. To make a long story short, Relief and NRx became entangled in lawsuits against each other, which proved inconsequential when NYESAMI was found to be ineffective in May 2022 with the FDA formally rejecting it for emergency use authorization in early July 2022. These developments cratered shares of NRXP to $0.50. The company has recently reached an agreement/settlement with Relief, essentially exiting the Covid-19 business. (It also briefly flirted with a SARS-COV-2 vaccine.)

Balance Sheet & Analyst Commentary:

These developments compelled NRx to refocus on NRX-101 in March 2022, but the market didn’t seem to care, viewing it as a failed Covid-19 concern. As such, with its balance sheet reflecting cash of only $18.5 million (as of September 30, 2022) and an equity raise promising to be highly dilutive, NRx was able to secure a high-interest (9%) $10 million loan, providing it a cash runway to YE23.

The company enjoys a small yet bullish two-analyst following from the Street. It is comprised of HC Wainwright, who initiated coverage in June 2022 with a buy rating and a $2 price objective and Ascendiant Capital Markets, who initiated coverage with a buy rating and a $4 price target on November 9, 2022.

With the exception of co-founder and beneficial owner Daniel Javitt, who has sold ~215,000 shares of NRXP during November 2022 – his total position is still north of 9.6 million shares – two board members and the CFO are bullish on NRx’s outlook, having collectively acquired over 528,000 shares in the back half of November, all around $1 a share.

Verdict:

The company’s detour into Covid-19 was a mistake, but it is likely the reason that it is currently publicly traded. NRx is essentially a binary play with the Phase 3 readout in 3Q23 setting the stage for a melt up or a meltdown. Even with the stock more than doubling off its mid-2022 lows, the risk-reward is still very asymmetrical with multi-bagger potential, and it could trade higher into its first data readout this quarter.

As such, a very small/speculative holding seems merited for aggressive investors. That said, with the clinical patient population treated by NRX-101 for bipolar depression with ASIB (to date) extremely small (n=15), there is significant risk of failure. And if the news is positive, there will almost certainly be a significant (albeit less dilutive) capital raise, unless an overseas commercial partner can be cultivated. If the stock trades up meaningfully in front of either data readout, take some profits in front of the news.

The basic speculative impulse, which is to believe whatever best serves the good fortune you are experiencing.”― John Kenneth Galbraith

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment