Douglas Sacha/Moment Unreleased via Getty Images

Introduction

In 2020 and 2021, we discussed accelerating economic growth, improving consumer sentiment, and new orders that were so strong that supply chains couldn’t take it anymore. In 2022, we discussed peak economic growth, persistent inflation, and central banks trying to fight inflation without hurting economic growth. 2023 is shaping up to be a worse version of 2023. At least when it comes to economic growth. One of the victims is the Norfolk Southern Corporation (NYSE:NSC), one of my largest industrial holdings. The company just reported disappointing fourth-quarter results. While earnings were slightly below estimates, the company suffered from a steep cost surge. When adding moderating revenue growth, we get an ugly picture with a high operating ratio.

Moreover, the company expects weakness to last, which is understandable given economic developments. It gets worse when adding higher CapEx, which should keep a lid on free cash flow growth for a while.

Yet, despite all of these challenges, I do not regret aggressively adding to NSC in 2022. Not only did I get a good price, I believe that NSC is a tremendous investment during corrections. The company has pricing power, operating fluidity is improving, and the moment economic growth expectations bottom, we can expect long-term outperformance to resume.

Now, let’s dive into the details!

Here’s What Happened In 4Q22

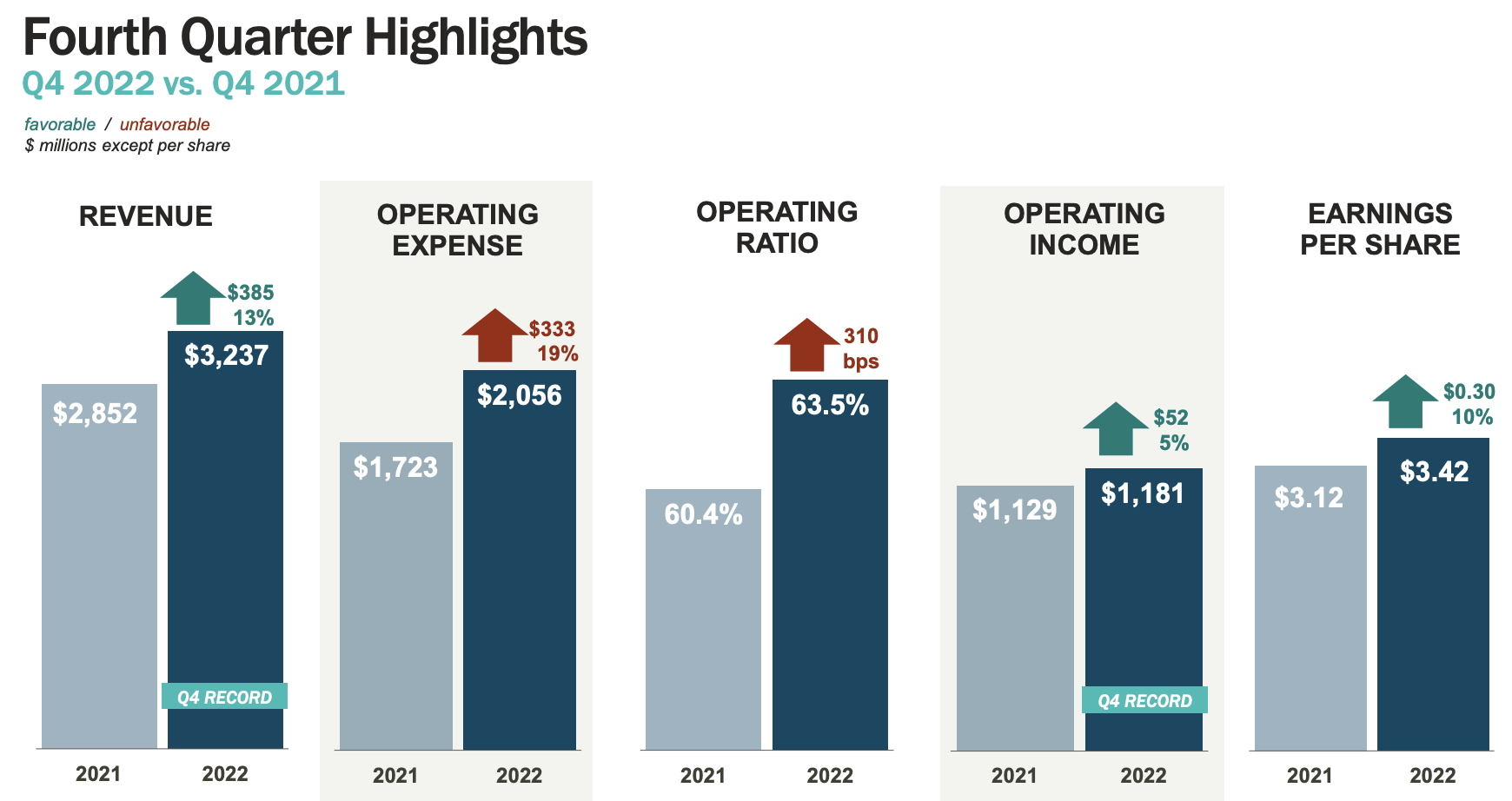

In its fourth quarter, Norfolk Southern reported $3.2 billion in revenue. That is in line with expectations and 12.3% higher compared to the prior-year quarter. GAAP EPS came in at $3.42, which was slightly ($0.05) below consensus estimates.

Norfolk Southern

With that said, these headline numbers are boring, and they don’t give us the details we need. Hence, it’s time to dig deeper.

What To Make Of Shipments & Revenue?

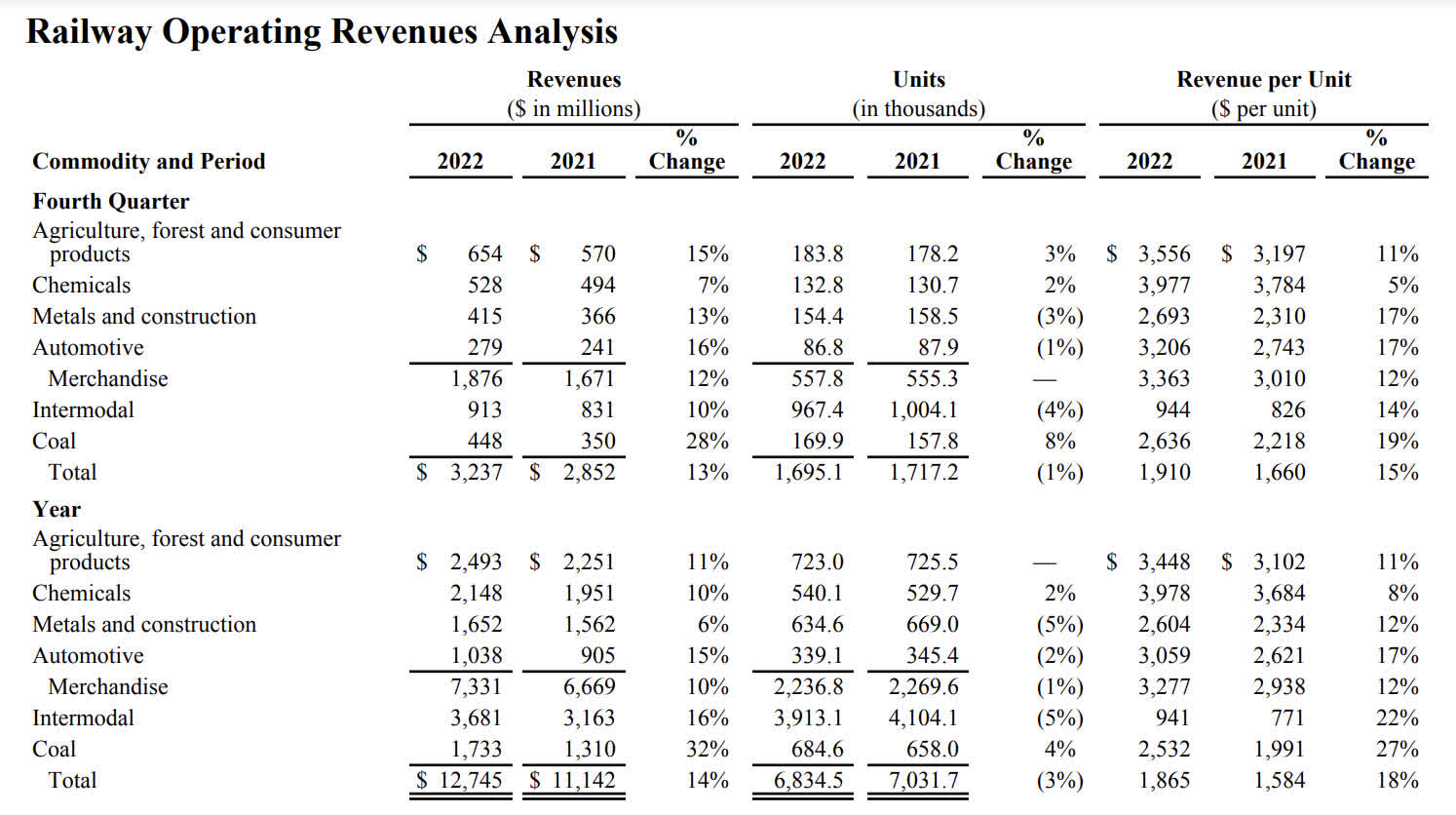

In its fourth quarter, the company reported a 1% decline in total volumes. On a full-year basis, volumes are down 3%. In the company’s merchandise segment, growth came from agriculture and chemical products, which benefited from high demand. Especially in agriculture, I expect strength to last.

Metals and automotive shipments were weak, partially offsetting the aforementioned gains. Intermodal shipments were down 4%, which is now a common sight. Inventory de-stocking and slower consumer demand are hurting. In this case, Norfolk Southern is the nation’s largest stock-listed intermodal railroad. Buffett-owned BNSF ships more intermodal, but that company isn’t publicly traded – at least not independently.

Coal was also strong, thanks to high natural gas prices overseas and a need to refill coal inventories. Norfolk Southern is one of the railroads with excellent connections in that industry and access to major export ports.

Norfolk Southern

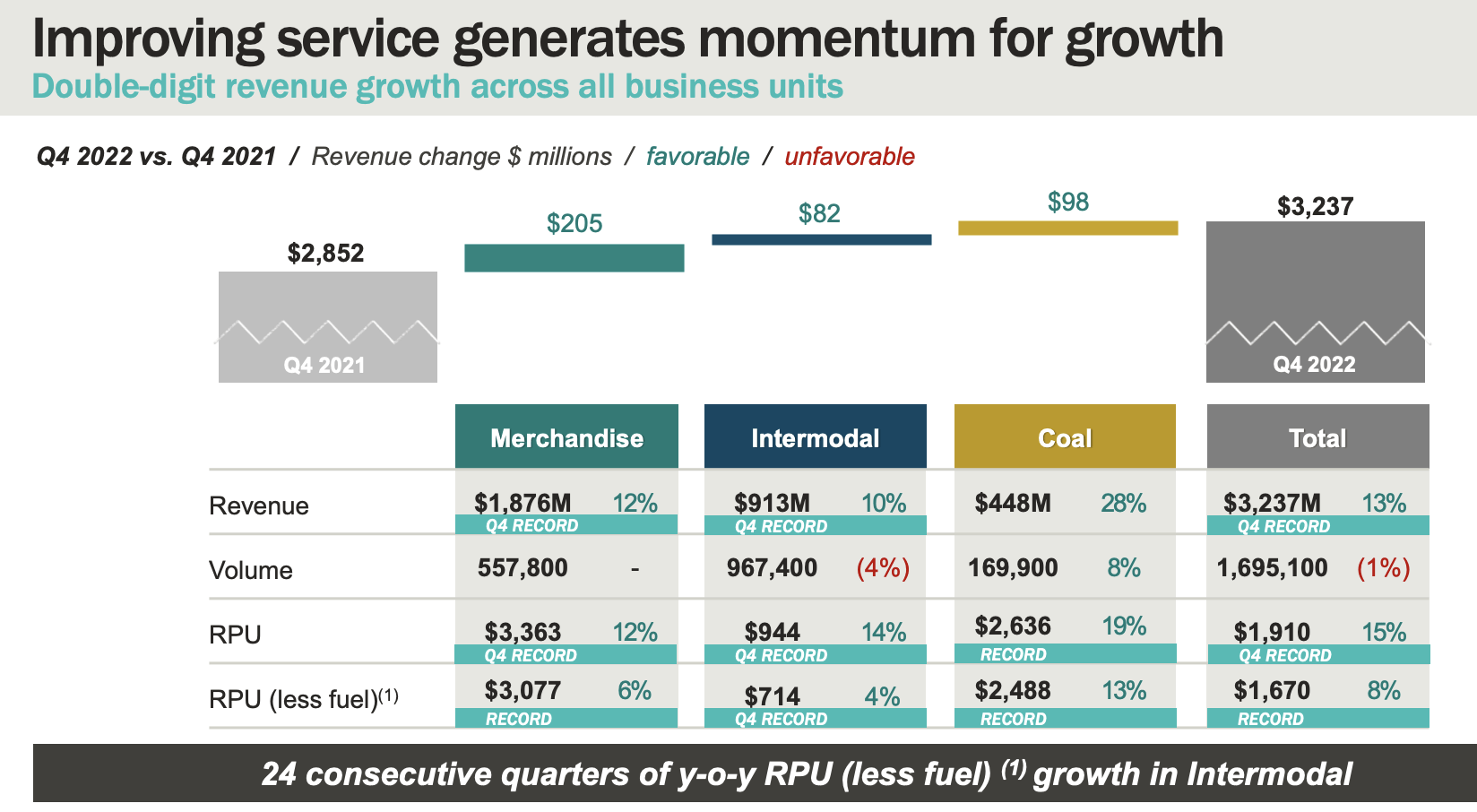

With that said, the overview below is a more fancy version of the table above. I’m using this one as well, as it shows that weak volumes did not keep the company from generating record results.

For example, pricing gains allowed the company to turn 1% lower shipments into 13% higher revenue. $3.2 billion in revenue is a new 4Q record. The same goes for revenue per unit and revenue per unit (less fuel).

Norfolk Southern

The company achieved record 4Q revenue in all segments but coal.

Readers who frequently read my NSC articles will know that the company has used pricing and efficiency improvements to consistently grow its business, even if shipments were slow.

With that said, operating expenses ruined the party.

The Operating Ratio Exploded

Freight revenues were up 13%. So far, so good. Unfortunately, operating expenses were up 19% to $2.1 billion. This lowered margins, meaning the operating ratio rose by 310 basis points to 63.5%. That’s ugly. Last year’s 60.4% OR wasn’t even a good number, to begin with.

Norfolk Southern

To give you an idea, this is what the breakdown of total expense growth looks like:

- Fuel: +62% due to rising diesel prices.

- Materials & other: +60% due to higher claims and higher material costs.

- Wages: +9% as a result of higher wage inflation and higher employment levels.

One of the things pressuring the operating ratio since 2020 is operating inefficiencies. In 2020, lockdowns as a result of the pandemic caused demand to implode. Railroads responded by lowering employee and material levels. After all, they didn’t need a lot of labor and equipment to deal with lower shipments. Also, nobody knew how bad things could get.

Once lockdowns ended, railroads were overwhelmed by accelerating demand. Supply chains were broken, ports were experiencing congestion, and the labor market was extremely tight. It also didn’t help that railroads applied precision railroading, which was based on keeping inventory levels and material spending as low as possible. There was no room for error.

The good news is that Norfolk has made tremendous progress when it comes to operating fluidity. Its services reached the highest fluidity since the start of the pandemic.

- Train speeds improved from 19.1 miles per hour in 3Q22 to 22.2mph in 1Q23 (as of January 20).

- Terminal dwell hours fell from 27.2 hours in 2Q22 to 23.6 hours in 1Q23.

- Locomotive productivity increased by 6% to 202 miles per day.

- Fuel efficiency improved by 1%.

- Workforce productivity declined by 10% as a result of higher employment levels and adjustments to higher volumes.

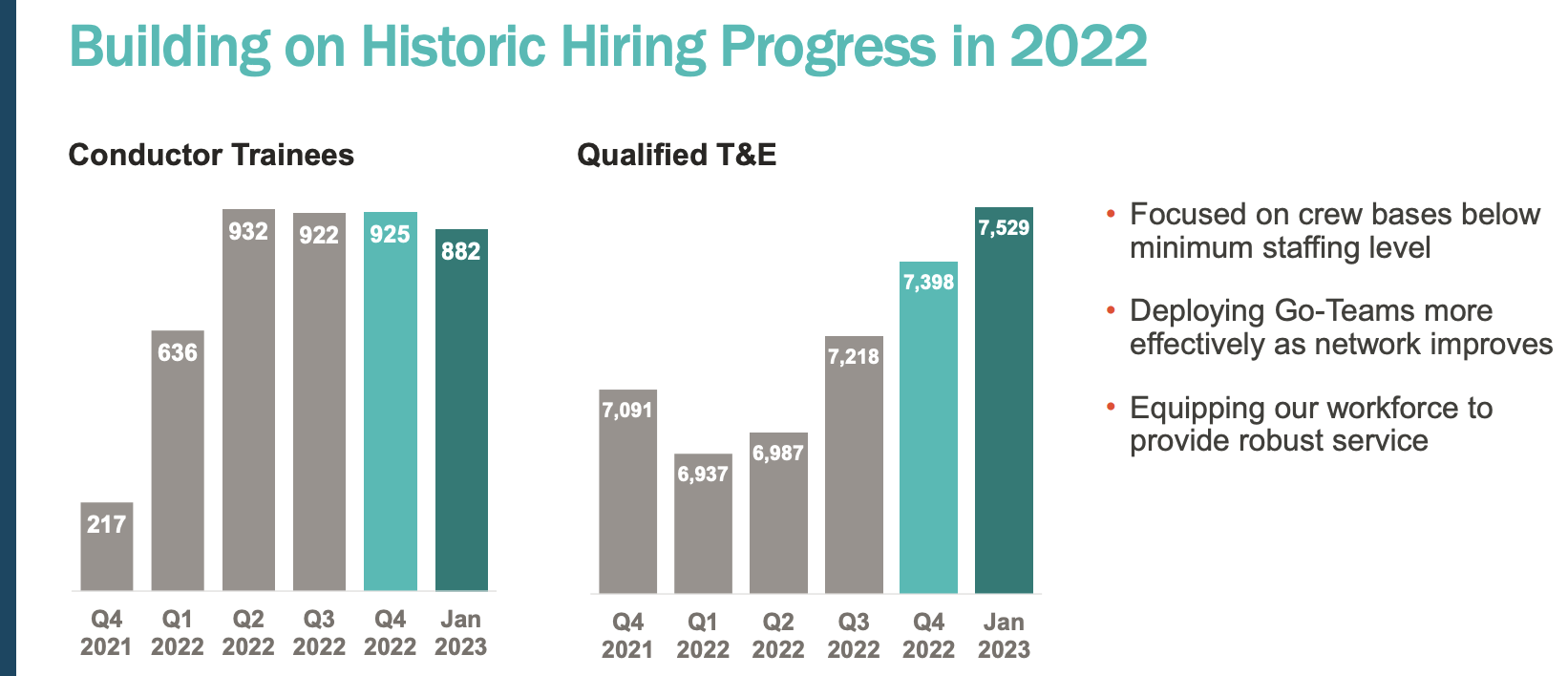

Moreover, the company has more than 7,500 qualified train and engine employees as of January 2023. That is up from 6,900 in 1Q22.

The employee pipeline isn’t bad either, as NSC continues to have close to 900 conductor trainees.

Norfolk Southern

The outlook wasn’t that great.

Expect More Headwinds In 2023

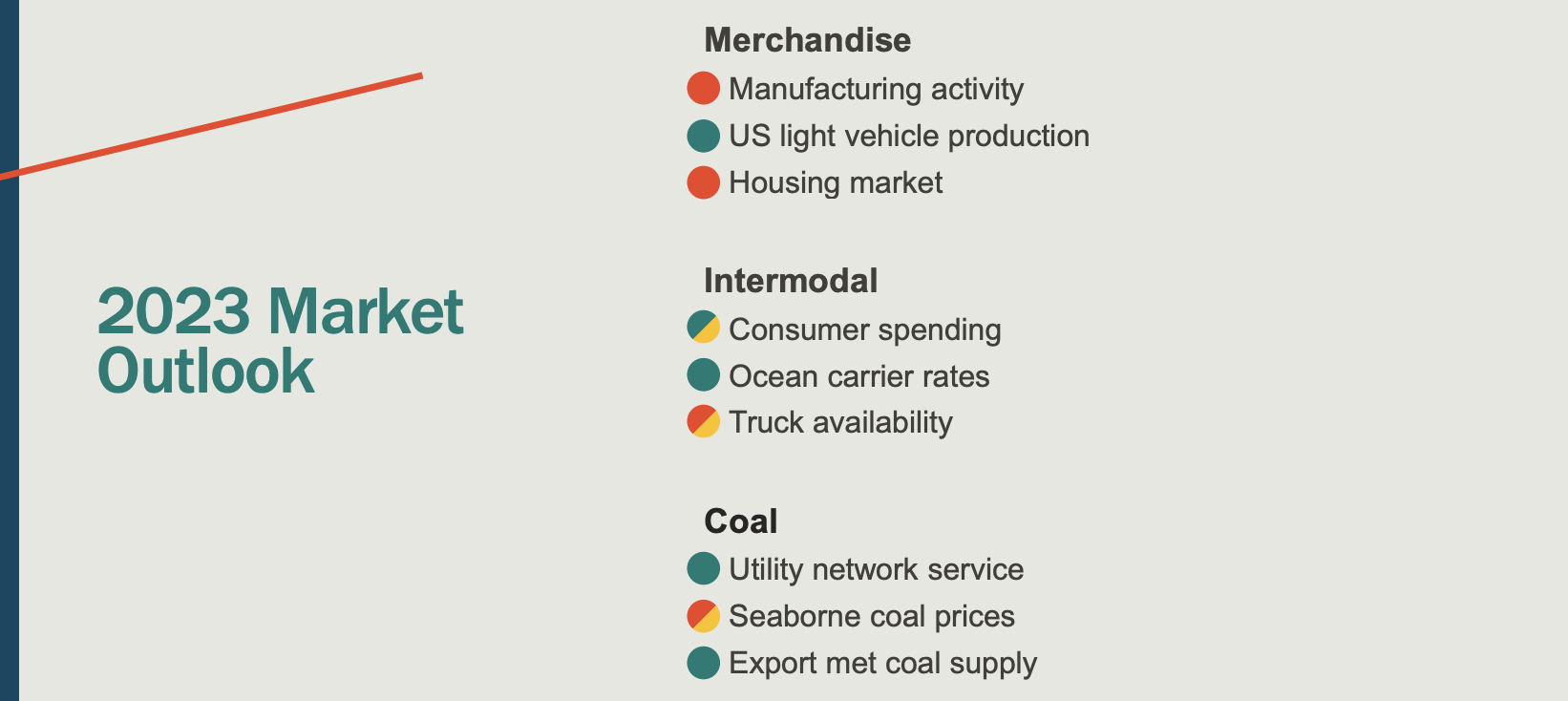

The company’s well-known segment outlook slide is slowly turning from green to red. The company sees headwinds in manufacturing, housing, and challenges related to higher truck availability and pressure on seaborne coal prices.

Norfolk Southern

Especially in this environment, pricing is under pressure. The truck market is not tight anymore, and declining demand is hurting commodity prices in certain areas.

In this case, the outlook is based on a mild recession. That is no surprise, as most companies use estimates from banks and related advisors.

Using Wells Fargo estimates, we’re likely looking at 0.5% growth in 2023, with two negative quarters in the second half of the year.

Wells Fargo

I believe that the consensus outlook is too rosy. I do not believe in an economic soft landing. That is only possible if the Fed accepts that pivoting prematurely will (likely) result in a steep inflation rebound. We would get a 1970s-like scenario.

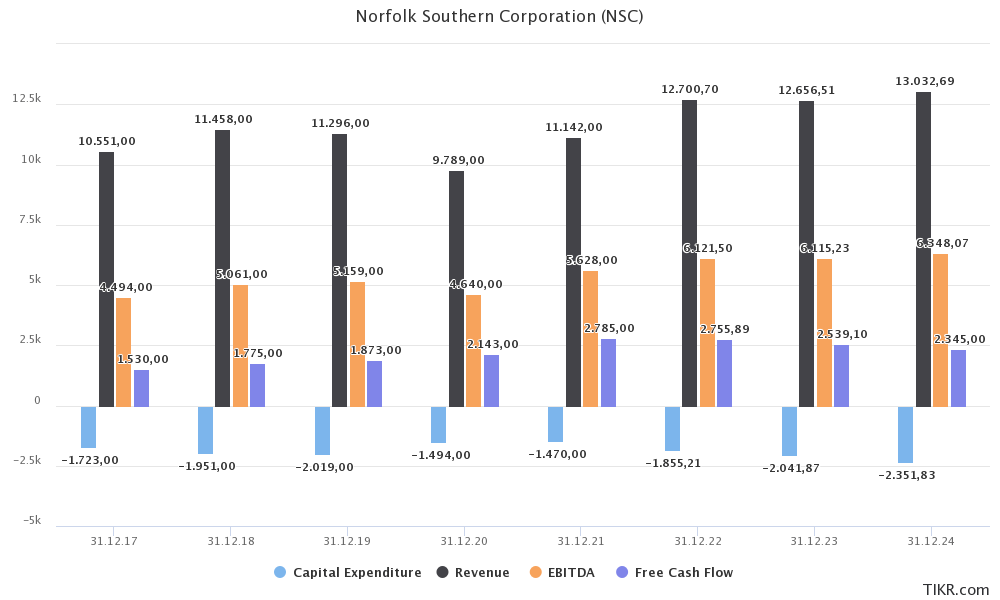

With that said, NSC expects flat revenue growth in 2023 and $2.1 billion in CapEx. The chart below shows what that would look like.

Analysts incorporated flat revenue growth before the earnings release. They also expect CapEx needs to rise well into 2024, causing free cash flow to fall in both 2023 and 2024. That’s not great.

TIKR.com

Using 2023 estimates, the company is currently trading at an implied free cash flow yield of 4.4%. That isn’t bad, as it supports sustained dividend growth. The company also hiked its dividend by 8.9% before releasing its earnings.

On a full-year basis, NSC spent $1.2 billion on dividends. That is up from $1.0 billion in 2021. Buybacks were lowered from $3.4 billion to $3.1 billion as a result of $511 million lower free cash flow.

Valuation

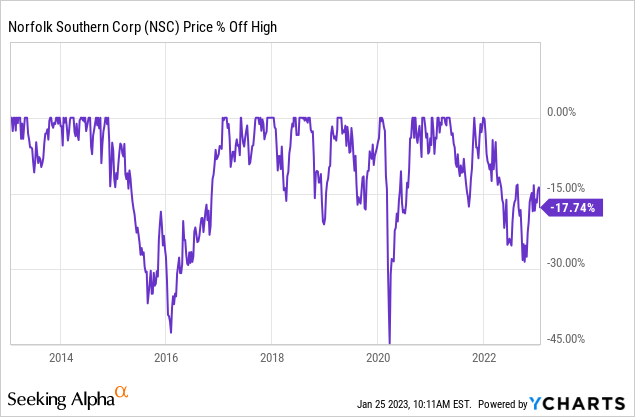

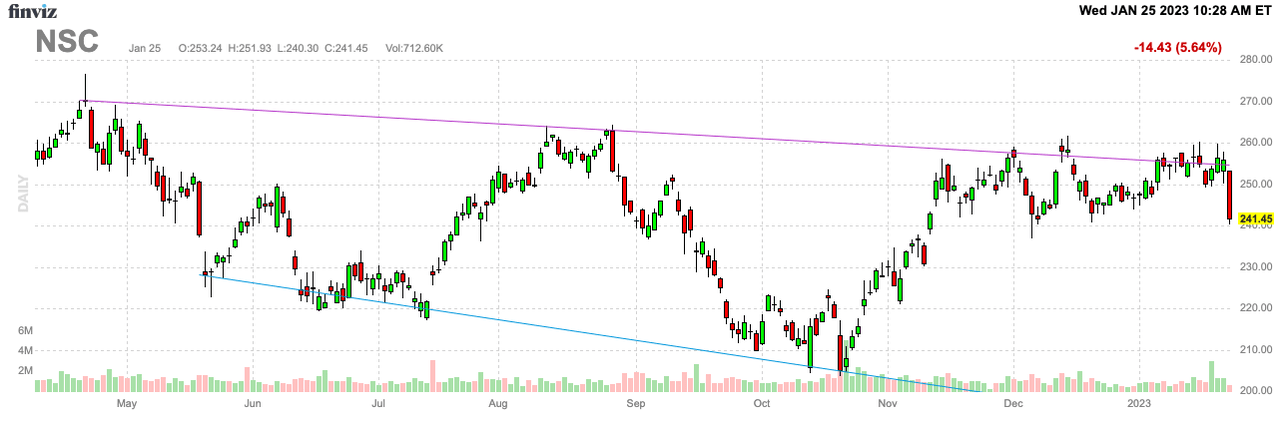

As I already briefly mentioned, it helps that the market has already priced in a lot of weakness. The stock is down 18% from its all-time high. This is up from last year’s lows when NSC was trading almost 30% lower.

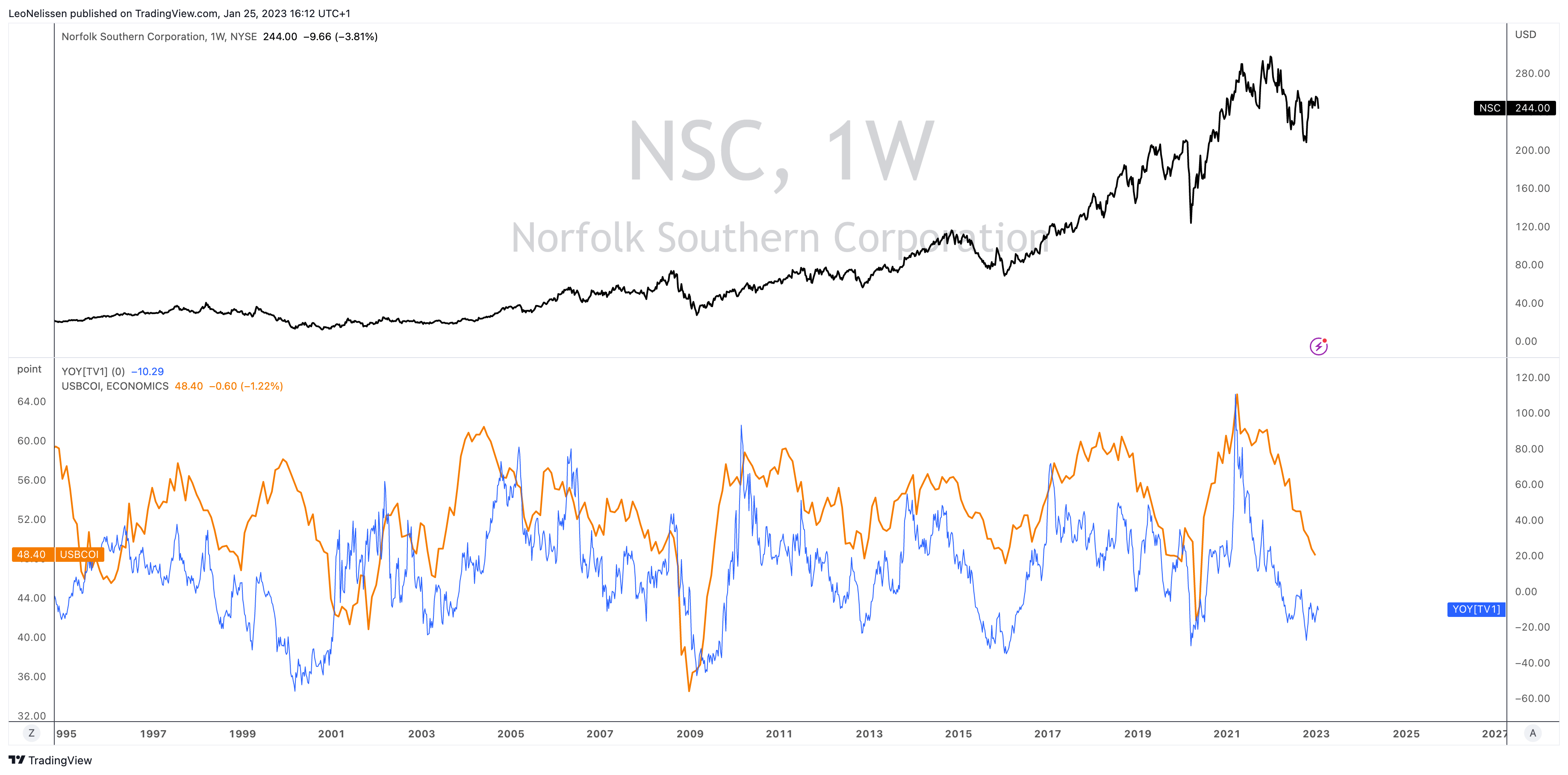

The chart below shows the NSC stock price. It also shows the year-on-year performance of the stock price compared to the ISM manufacturing index. Needless to say, the high correlation makes sense, as NSC is highly tied to economic expectations.

TradingView (NSC, NSC Y/Y vs. ISM Index)

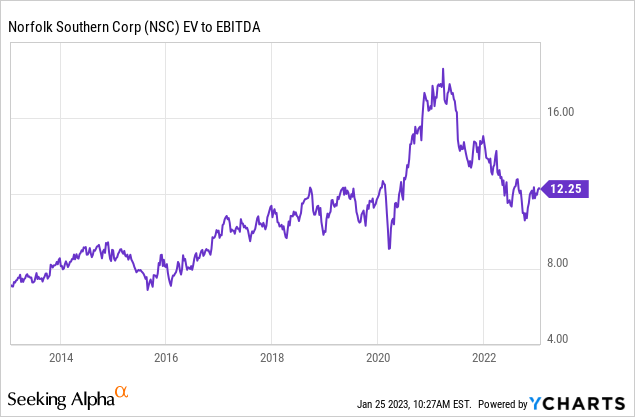

NSC is currently trading at 11.7x 2023E EBITDA based on its $56.3 billion market cap, $14.7 billion in 2023E net debt, and $500 million in pension liabilities. That valuation is fair, yet given the circumstances, I would like to see a bigger discount to incorporate weaker growth.

Last year, I was “lucky” enough to expand my NSC position close to the lows. This year, I hope to do it again. I think we could see a move lower to $210. At that point, I’m a buyer again – regardless of my already high industrial exposure.

FINVIZ

Takeaway

I’m a bit disappointed, yet not surprised, as I’ve incorporated slower-than-expected growth in most of my articles since last year. The economy is weakening, inflation is still an issue, and higher spending is needed to improve network fluidity.

In 4Q22, NSC suffered from a much higher operating ratio, a weakening outlook, and volume headwinds in intermodal. Nonetheless, it used pricing and improved operations to achieve record 4Q revenues.

While I expect NSC to suffer a bit more in 2023 due to my belief that we won’t see a soft landing and ongoing operating/cost headwinds, I’m very upbeat when it comes to using a lower stock price to buy more NSC exposure.

Investors monitoring NSC should look for an entry close to $210. At that point, I think the risk/reward for a long-term investment in NSC is very attractive.

(Dis)agree? Let me know in the comments!

Be the first to comment