jared-m

Immediately after I put out my cautious note on Norfolk Southern Corporation (NYSE:NSC), the shares fell about 15%, which I found gratifying enough. They’ve since rebounded nicely and are now actually up by about 5.4% against a gain of about 1.7% for the S&P 500. The company has since published financial results, so maybe there’s something in the report that put a pep in the step of these shares. I’ll review those financials, and look at the valuation to see if it makes sense to buy back in.

One of the many ways that I’m obsessed with trying to make your lives as comfortable as possible is by saving you time when I can. I’m doing this in this instance by offering you a “thesis statement” that outlines my thinking in one paragraph that is hopefully both “handy” and “dandy.” This allows you to get the gist of my argument without the need to expose yourself to the entire article, with all of my not-so-subtle bragging and tiresome jokes. You’re welcome. I’m of the view that Norfolk Southern remains a poor investment at current prices. The company has grown revenue and profits in spite of the fact that traffic for the first nine months of 2022 was down significantly when compared to the pre-pandemic era. One thing that has gone up is debt. It’s about $1.2 billion higher today than it was this time last year. Further, I think the fact that management spent over $2 billion on buybacks is one reason why share price has held up. In spite of all of this, the shares are trading near multi-year high valuations. I’d remind investors that the last time they hit current valuations, the stock dropped dramatically in price, which suggests limited upside from current levels in my view. I think the combination of slowing traffic and elevated valuations is troublesome, and for that reason, I’m going to remain on the sidelines here. When the inevitable drop in price happens, I’ll certainly reconsider.

Traffic Patterns Offer Context

To put this in context, the following financial results are as of the period ending September 30, 2022. In order to put this in context, I looked at traffic figures for the approximately identical periods in 2018, 2019, 2021, and 2022. We have data for week 35 for the latter two years and data for week 36 for the former two years. So, in order to make comparisons easier, I employed the skills slammed into me by the good sisters at Holy Spirit School many decades ago to work out the average number of carloads per week.

We see from the traffic figures that traffic has been trending down for a few years now.

Comparison of Traffic Data for First Nine Months of 2018, 2019, 2021, 2022 (Norfolk Southern investor relations, AAR, Author calculations)

In case you aren’t the victim of the same kind of education as I received, I’ll walk you through the changes here. Weekly average traffic in 2022 was down by about 12.9% from 2018, down 10.2% from 2019, and down 3.4% from 2021. The trend seems fairly obvious to me, and that’ll form the background for my financial analysis.

Financial Snapshot

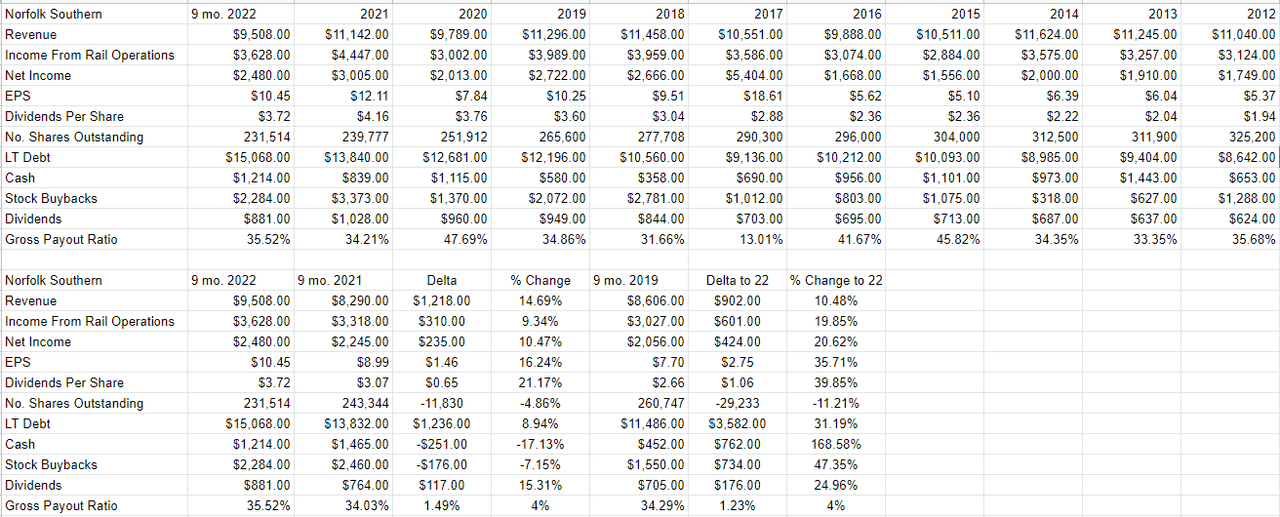

Given what’s happening with traffic, a reasonable person might assume that revenue and profits would have been lower in the first nine months of 2022 when compared to any of the previous few years. While that might be a reasonable assumption to make, it would be wrong. It seems that this company has the capacity to generate higher revenue on lower traffic. Specifically, when compared to the same period in 2021, revenue and net income in 2022 were higher by 14.7% and 10.5% respectively. Management rewarded shareholders with this improvement by increasing the dividend by fully 21%. When we compare the first nine months of 2022 to the pre-pandemic period, similar results emerge. Revenue and net income in 2022 were higher than 2019 by 10.5% and 20.6% respectively. It seems that this company has managed to unlock some kind of secret where they can earn more by doing less.

It’s not all magic rainbows over at Norfolk Southern, though. The capital structure has deteriorated substantially over the past year, with long-term debt up by 8.9%, and cash down by 17% from the year-ago period. Long-term debt is at an all-time high, and if I were a shareholder, I’d like to see the company pay some of this down. In my view, it’s telling that at the same time, the company increased debt by $1.236 billion, they bought back $2.284 billion of stock. I once wrote that railroads are compelling investments because managers are very conservative stewards of capital. What a naive, naive child I was way back in 2019.

Anyway, I think the financial history is reasonably good, though I doubt the company will be able to continue to grow the business on the back of obviously slowing revenue forever. In my view, sooner or later this trend will reverse. Thus, I’d be happy to buy the stock, but it would have to be at a price that compensated me for taking on the risk of eventually slowing business and increasing debt levels.

Norfolk Southern Financials (Norfolk Southern investor relations)

The Stock

If you subject yourself to my stuff on a regular basis, you know that I consider the stock and the business to be distinct from each other. The business makes money by hauling large amounts of bulky freight. The stock, on the other hand, is a speculative instrument that gets buffeted by a host of factors, some of which have nothing to do with the business. For instance, the stock may rise in price because management decides to take $2 billion of shareholder capital to buy the stock because they can think of nothing better to do with it. The performance of another Class 1 railroad may impact this stock. Additionally, stock may be affected by the crowd’s ever-changing views about the desirability of “stocks” as an asset class. There’s no way to prove this definitively, as it’s an obvious counterfactual, but it’s possible to make the case that some portion of Norfolk Southern’s returns since I last wrote about this business are a function of the fact that the overall market was up slightly since.

So, this is why I consider the stock as a thing distinct from the business. The former is often a poor proxy for what’s going on at the company, and I think it’s possible to profitably exploit this disconnect. In my view, the only way to successfully trade stocks is to spot the discrepancies between what the crowd is assuming about a given company and subsequent results. What I want to see in this regard is a stock that the crowd is somewhat pessimistic about that goes on to exceed expectations. When the crowd is pessimistic, the shares are cheap, which is why I try to buy only cheap stocks. Now, I consider this to be a fine investment at the right price, and I want to work out whether we’re near that price or not today.

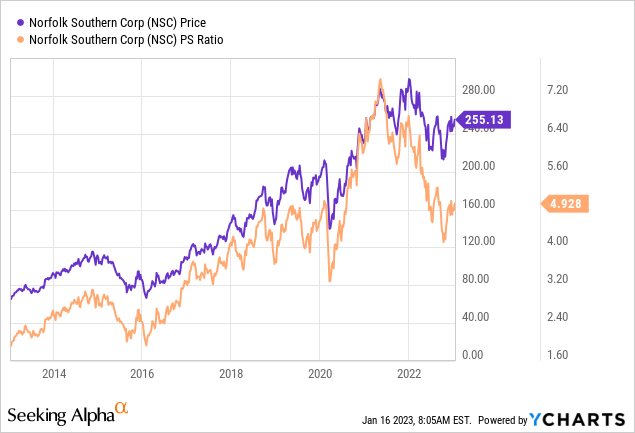

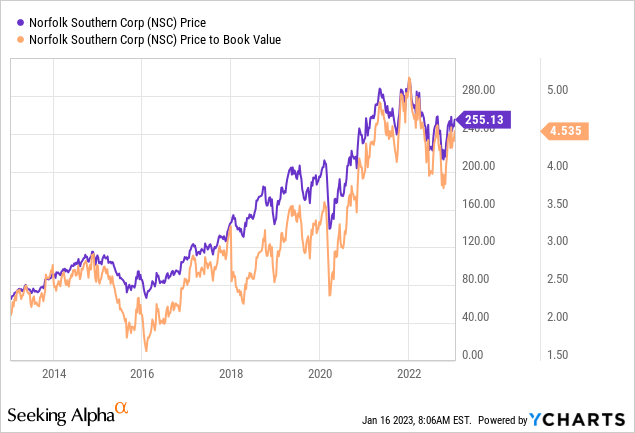

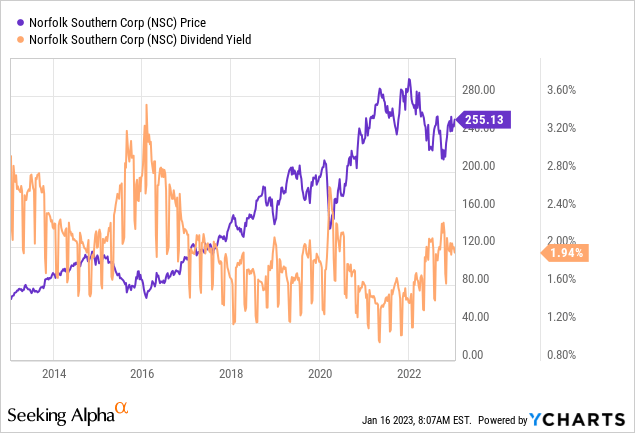

In my previous piece, in case you’ve forgotten, I remained cautious about this stock because the shares were trading near multi-year highs on a price to sales and price to book bases of 5.1 and 4.47 times respectively. Additionally, the dividend yield was on the low side at 1.9%. Fast-forward to the present, and the valuation is approximately equal what it was back in September.

If I were an investor in this stock, I’d be troubled by the fact that traffic is slowing, that the stock dropped significantly when it last reached current valuations, and that the dividend yield is currently about 1.6% less than the risk free rate.

In addition to looking at ratios, I also want to try to understand what the crowd is currently “assuming” about the future of a given company. If the crowd is assuming great things from the company, that’s a sign that the shares are generally expensive. If you read my articles regularly, you know that I rely on the work of Professor Stephen Penman and his book “Accounting for Value” for this. In this book, Penman walks investors through how they can apply the magic of high school algebra to a standard finance formula in order to work out what the market is “thinking” about a given company’s future growth. This involves isolating the “g” (growth) variable in this formula. In case you find Penman’s writing a bit dense, you might want to try “Expectations Investing” by Mauboussin and Rappaport. These two have also introduced the idea of using the stock price itself as a source of information, and then infer what the market is currently “expecting” about the future.

Anyway, applying this approach to Norfolk Southern at the moment suggests the market is assuming that this company will now grow profits at a rate of about 5.8% from here. That is a pretty optimistic forecast in my view. None of the above fills me with a strong urge to buy shares at the moment, so I’ll remain on the sidelines. I may miss some further price gains from here, but one thing I’ve learned after decades of investing is that what the market gives, the market can very quickly take away. I’d rather preserve capital at the moment than take on much risk at the moment.

Be the first to comment