dzika_mrowka/iStock via Getty Images

Nordstrom (NYSE:JWN) is a higher end department store type retailer that we have liked and traded in the past, but it has been a horrible market and a horrible time for many retail stocks. Department store stocks have been an absolutely wild ride. They ebb and flow big time. They suffered so badly in 2020 in the pandemic. Those that found a strong online strategy did well to recover, and Nordstrom did pretty well in this regard. The stock rebounded sharply in late 2020 and into 2021. Then it moved mostly sideways, only to start collapsing in 2022 with both a weak market and devastating inflation.

Now the retailer is not only facing inflation, it is also seeing the consumer tighten up, as evidenced by horrific December consumer sales dropping 1.1%. Between these types of retailers, there is stiff competition. Those retailers who are best managing their inventory, using tactical promotion, and watching costs that are doing well in this environment. Inflation has been a retail killer. Rising input costs have too. Retailers are taking it on the chin from many fronts. Nordstrom stock has come down to levels that trigger our value screens at our service, so we took a look.

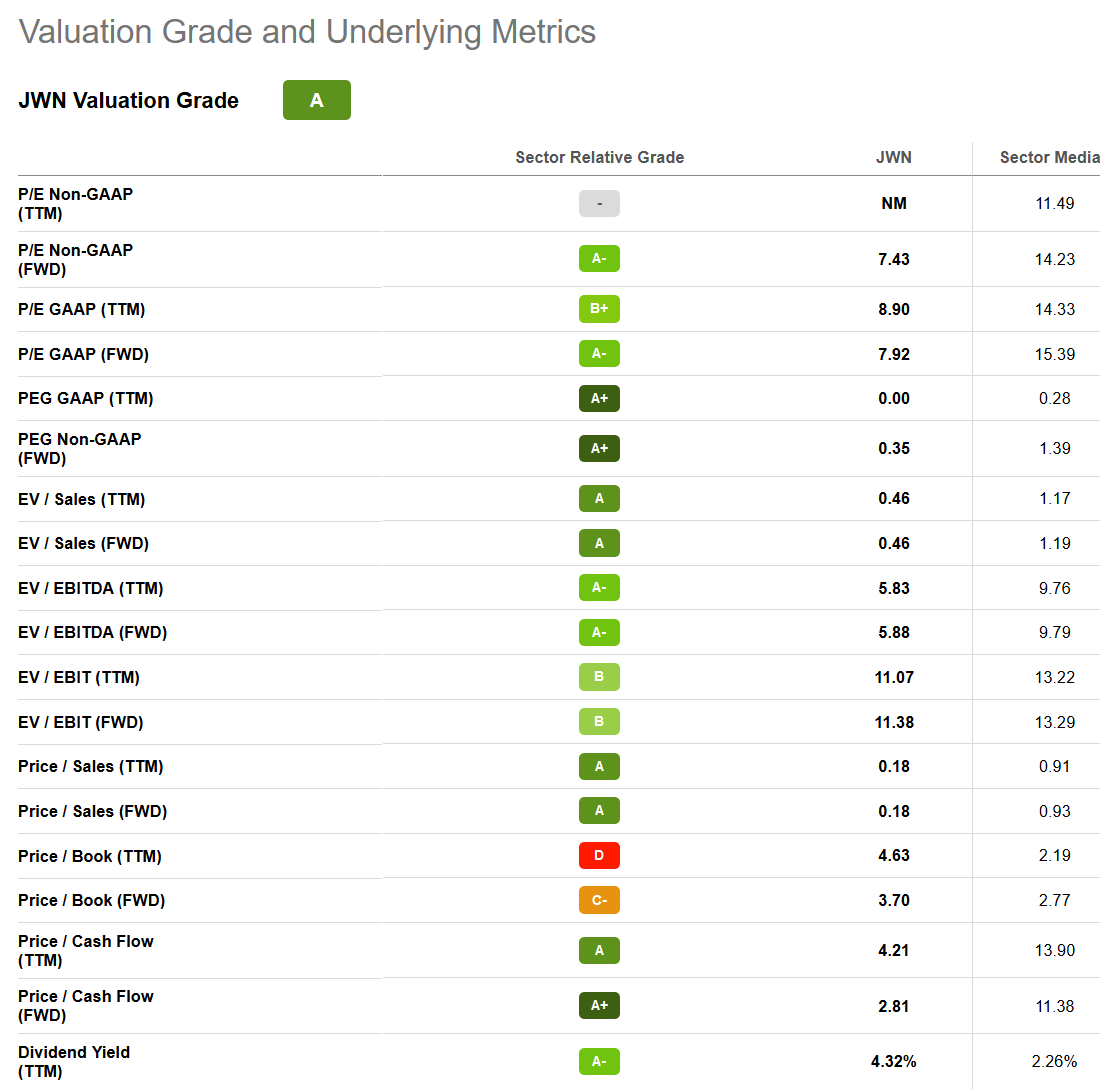

When you take a look at the valuation metrics, things look pretty attractive, but the low multiples continue to be a warning sign in our opinion, rather than a deep value situation. If the company was not saddled with debt, this could be a great entry point, especially if the future looked promising.

Seeking Alpha

The stock has slowly declined to 7X earnings and is offering a 4.4% yield. We would love to think that the stock is setting up for a trade, but do not see a real bottom in sight for the stock and company until it can stop relying so much on promotion which is crushing margins, and EPS. The dividend was gone for a while and only recently made a return. The company has put out some very moderate growth that we do not think is set to weaken further and although the value metrics are attractive at first glance there is a big $2.86 billion in debt as well as $8.8 billion in liabilities. When you factor in that we are in a much higher rate environment now, refinancing the debt is going to be expensive. That is a headwind, on top of all of the issues on the macro scene being faced.

It is not exactly a very tough macro environment, but there are a lot of macro pressures that continue to combine to weigh on performance. The company will report full earnings in march for the entire year 2022, but the company came out and preannounced that it was going to have a pretty bad quarter, and year, relative to prior expectations.

Just how bad is it? Well sales are going to be at the lower end of guidance, but margins are getting demolished. The management team currently sees revenue growth for the full-year 2022 now coming in toward the bottom of the 5% to 7% range that it had previously issued. Why? Well remember the consumer sales number we mentioned above? Nordstrom was part of that malaise of the consumer. The company is blaming “slower than anticipated holiday sales”.

CEO Erik Nordstrom said:

The holiday season was highly promotional, and sales were softer than pre-pandemic levels. While we continue to see greater resilience in our higher income cohorts, it is clear that consumers are being more selective with their spending.

So there you have it, sales will be down. But wait, there’s more! On top of sales coming in at the lower end of expectations, the entire year’s 2022 EPS is going to come in far lower than expected too. So the valuation numbers above, at least on the near term FWD basis, are no longer valid. At $17.50, the true 2022 EPS multiple is around 10-12X. This is due to being ‘promotional’ which means there were significant markdowns offered which crushed margins and is now going to result in $1.50 to $1.70. This is a huge reduction compared with the prior outlook of $2.30 to $2.60 in EPS. This is essentially a preannounced result for Q4 and obviously for the year.

The one key metric that we focus on with retailers is comparable sales. Comparable store net sales will likely take a beating too now that sales figures were guided lower. We love to look for strong and growing comps. We do believe we will see positive news regarding online sales.

We will closely be watching for the exact gross margin and gross profit. Why? Despite management telling us earnings will be drastically less than expected, we want to see the precise impact of the promotions relative to other expenses. We are very hopeful that operating margin will not take a massive hit. If we see rising expenses despite low growth sales and busted gross margin, that will be problematic going forward. The company needs to push cost savings plans.

Is it all bad? Well this news is pretty terrible for a company that has struggled to really come back on strong since the pandemic. While positives like the dividend coming back and store traffic returning have pumped life into the company, the inventory issue led to this. The company simply over ordered in our opinion when supply chains were a mess. Then there were was simply too much ‘stuff’ on hand. With consumers weakening more than expected in a key holiday month, the heavy promotion is not a surprise. However, the company should come out of this with much better inventory levels. The company will have a much leaner line of product which should mean having a “healthier” line to “quickly adapt to changing consumer demand.”

What to do?

There are a ton of macro pressures. While the stock has come down significantly, there is likely more downside ahead, especially if promotion is spilling into Q1, which we cannot see any other option. Had the company cleaned out inventory to levels they really wanted, they likely would have stated that. What was stated was inventory is “healthier” implying there is more work to do. But folks, we are very likely coming into a recession. It may be mild, it may be moderate, but recession is more likely than not in our opinion. On this news, we are sellers. Shares are still off a bottom, which we think will be retested.

Be the first to comment