peterschreiber.media

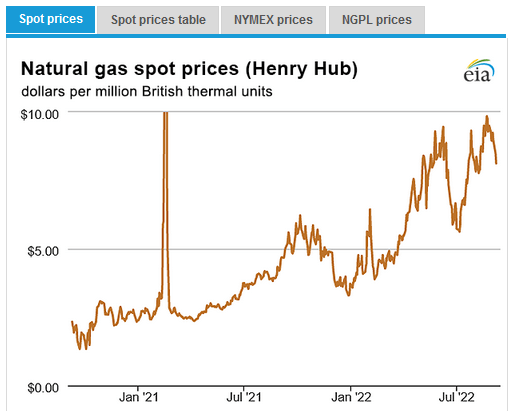

In my opinion, the depth of the 2020 bear-market and current high inflation rates seen across the globe are in direct relation to the high-price of oil and natural gas. The price of oil began rising in late 2021 but was turbo-charged by Putin’s war-of-choice on Ukraine and the resulting sanctions place on Russia by the U.S. and its Democratic and NATO allies. The combination broke the global energy supply chain. While many want to blame the current high-price of electricity in the EU and the U.S. on clean-energy policies, the majority of the price increase has to do with the reduction of natural gas flow to the EU from Russia, and the resulting rise in the price of natural gas in the EU – which has reflected back into rising natural gas prices in the U.S. as well (see Henry Hub price graphic below). Many believe the solution to these problems is the increased use of nuclear power. That being the case, today I will take a close look at the thematic VanEck Uranium+Nuclear ETF (NYSEARCA:NLR) to see if it can help re-energize your portfolio.

EIA

Source: EIA Natural Gas Weekly

Investment Thesis

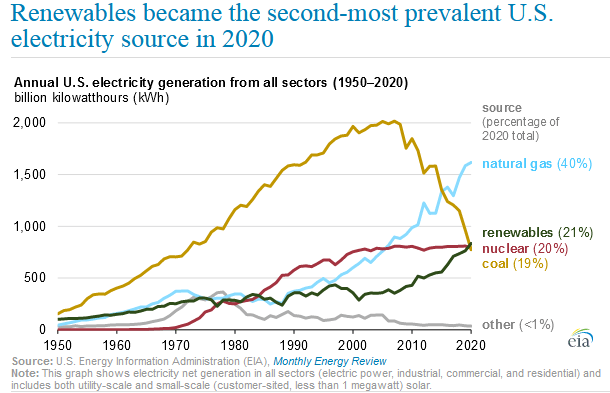

As you know, the electrical power generation profile in the U.S. has changed dramatically over the past twenty years:

EIA

Source: EIA

Clearly, natural gas has taken over from coal, which is a dying industry. This was due to two primary reasons:

- Nat-gas emits 50% less CO2 than does coal; 100% less particulate emissions; and does not result in leaving millions of tons of toxic heavy-metal fly-ash leftovers after burning it, that needs to be stored, as does coal. These toxic fly-ash storage sites are an environmental nightmare.

- Nat-gas power generation plants are much cheaper to build and operate. No train-track terminals to deliver coal by rail, many fewer workers to operate, and none of the big on-going maintenance and fly-ash storage costs that coal has.

This is why I presented the nat-gas price chart above, as it is now the primary input cost for much of America’s power generation.

The next important observation is that nuclear energy’s share of the U.S. power-gen market has remained flat at about 20% over the last twenty years while renewable power has increased dramatically and now -at 21% – is slightly ahead of nuclear.

One reason natural gas took over so much of U.S. generating power capacity was due to the shale revolution, which brought abundant U.S. gas reserves to market and lowered the price. However, with Russia shutting down nat-gas supplies to the EU, there is much more global demand for LNG, much of it coming from America. That has caused a significant increase in the domestic natural gas price as shown in the first graphic.

That being the case, many energy policymakers and pundits are pushing nuclear power as the solution to the high-cost of energy inflation. So, let’s take a closer look at the VanEck Uranium+Nuclear ETF to see if it has positioned investors for success going forward.

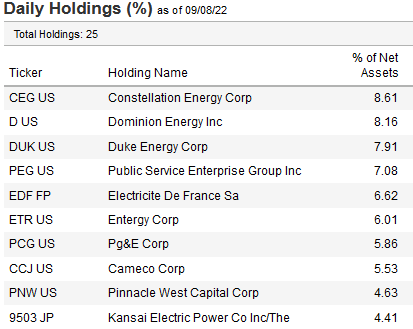

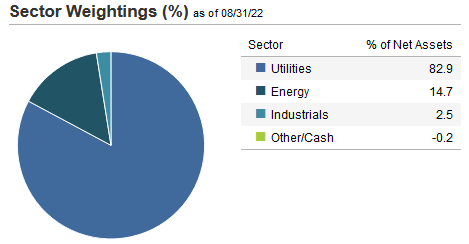

Top-10 Holdings

The top-10 holdings in the NLR ETF are shown below and equate to what I consider to be a very concentrated 65% of the entire 25 company portfolio:

VanEck

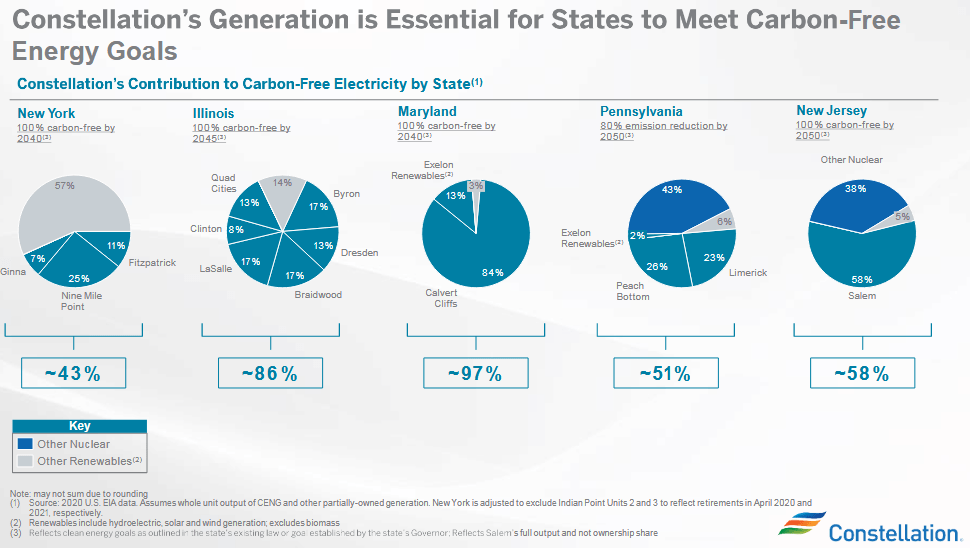

The #1 holding with an 8.6% weight is Constellation Energy (CEG). Constellation Energy is one of the largest nuclear energy providers in the U.S. and operates 6 nuclear plants:

Constellation Energy

These nuclear plants provide the majority of carbon-free power across five states:

Constellation Energy

Source: August 2022 Presentation

CEG’s stock yields 0.49% and trades with a current forward P/E of 28.8x.

Dominion Energy (D) has a 8.2% allocation in the NLR ETF and is the #2 holding. Dominion owns and operates four nuclear power plants. The stock is up 6.7% over the past year, yields 3.23%, and trades with a forward P/E of 20x.

Duke Energy (DUK) is the #3 holding with an 8.2% weight. Duke owns and operates two of the nation’s top-10 largest nuclear energy plants: the Oconee Nuclear Station (three PWR units, with a combined capacity of ~2.62 GW) and the McGuire nuclear power plant (two PWR units with a combined capacity of 2.38 GW). Duke Energy stock is up 5.1% over the past year and yields 3.68%.

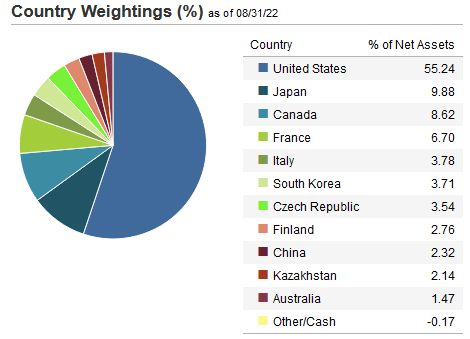

The #5 and #10 holdings are foreign nuclear operators in France and Japan. It is notable that Japan has shifted policy and is expected to restart 19 of 33 nuclear power plants that were shut-down after the Fukushima disaster. The NLR ETF has 9.9% of the portfolio to Japan-based companies and has only 55.2% of the total portfolio invested in U.S. based companies:

VanEck

Source: VanEck NLR ETF Webpage

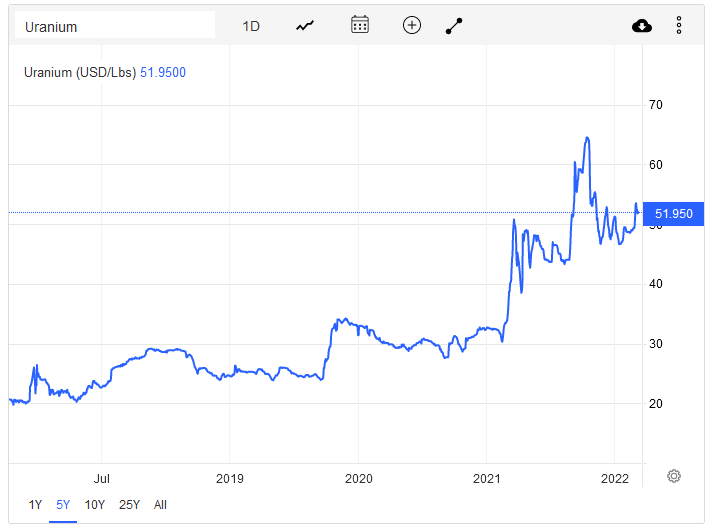

Canadian company Cameco (CCJ) is the only pure-play exposure to uranium production in the top-10 holdings. The price of uranium has been on a bullish run that started well before Putin’s invasion of Ukraine:

tradingeconomics.com

However, much of that price appears to already be built into Cameco’s stock price: it’s up 33% over the past year and currently trades with a forward P/E=120x. Meantime, the NLR portfolio hasn’t really cashed in on the big move in uranium because it is primarily exposed to utility companies, not the precious metal:

VanEck

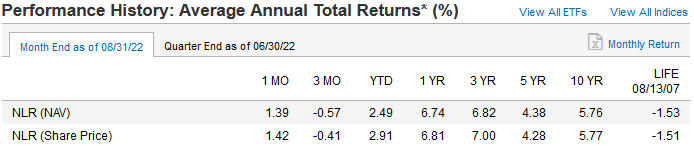

Performance

The long-term performance track-record of the NLR ETF is shown below:

VanEck

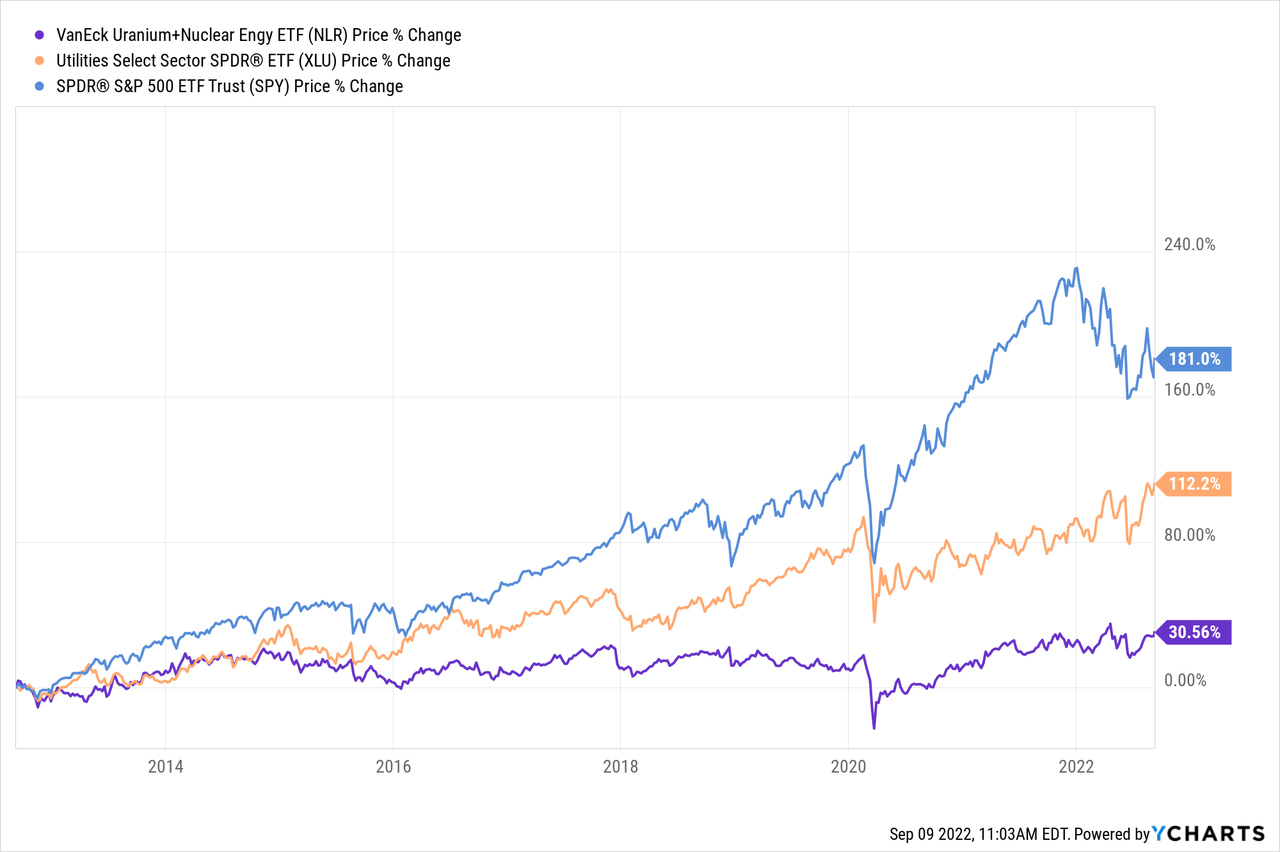

As can be seen by the graphic, this fund has been a significantly under-performing asset. To illustrate that fact further, the chart below compares the price returns of the NLR ETF with that of the Utility SPDR ETF (XLU) and the broad market average as represented by the S&P500 ETF (SPY) over the past 10-years:

Clearly the NLR ETF has been a good way to not only to significantly lag the returns of the broad market as represented by the S&P500, but even the Utility Sector is up more than 3.5x that of the NLR over the past decade.

Risks

Going forward, the risks appear to be considerable, starting with the fact that NLR has a rather exorbitant expense fee of 0.89%, which is a whopping 40% of its 2.2% yield.

Meantime, the foreign currency exposure as a result of the strong U.S. dollar is likely to be a significant headwind for some time to come considering that the NLR ETF’s has significant exposure to foreign companies.

But the biggest risks is that nuclear energy simply doesn’t take off as expected. The two most recent nuclear projects in the U.S., Watt’s Bar in Tennessee (which is in operation) and Vogtle in Georgia, were both dogged by massive cost-overruns and schedule delays. That is the primary reason utility company CEO’s in the U.S. are building out solar, wind, natural gas, and battery backup capacity as opposed to nuclear power.

Meantime, as I pointed out in my recent Seeking Alpha article on NuScale (SMR), which is not even in the NLR ETF’s portfolio, small modular nuclear reactors (“SMRs”) have been discussed and worked on for decades (at least since I was in engineering school back in the 1970’s) but have yet to come to fruition. NuScale’s SMR project (yet to be built …) is another example of a nuclear project that has had cost and schedule concerns, causing several of the original partners to drop out of the project.

Meantime, there is still no U.S. federal plan to store radioactive wastes because no state wants it in their backyard. As a result, radioactive waste from nuclear power plants continues to be stored on-site and are, what some environmentalist consider, environmentally ticking time-bombs.

Summary & Conclusion

The VanEck Uranium+Nuclear fund is a very expensive fund with a dreadful long-term performance track record. Meantime, utility company CEO’s continue to build out solar, wind, nat-gas, and battery backup capacity instead of nuclear because they know these projects can be completed on-time and on-budget. And, they won’t have the problem of storing and/or otherwise dealing with leftover radioactive waste.

Investors would be well advised to sell the NLR ETF and simply move the proceeds into the XLU Utility ETF – if they are after income (2.63%) – or into the S&P500 if they are after total returns. NLR is a SELL.

Be the first to comment