Michael Vi

Introduction

My thesis is that NIO (NYSE:NIO) is becoming a substantial force with respect to high-end battery electric vehicles (“BEVs”) in China.

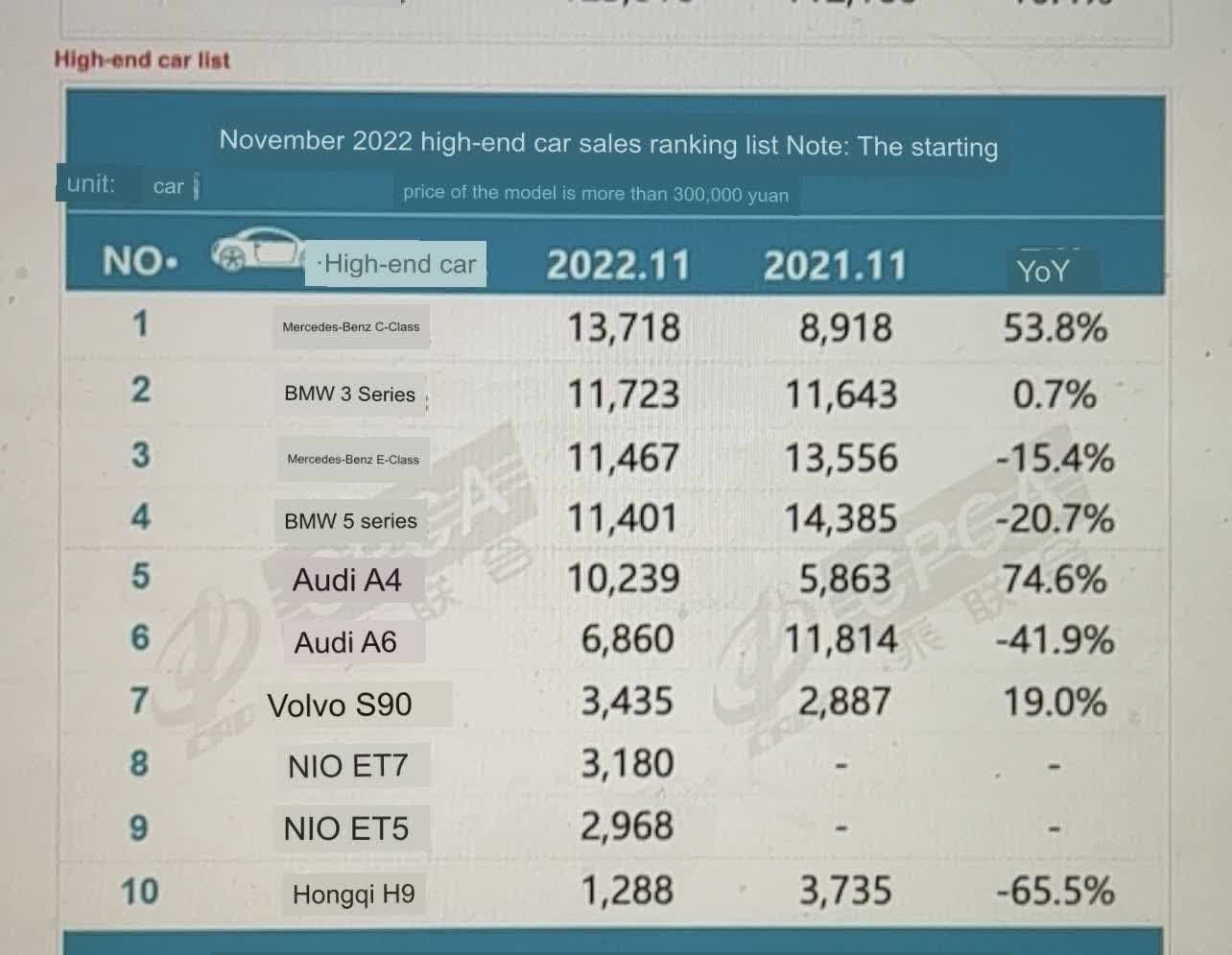

The November 2022 CPCA Monthly Analysis shows the usual German cars like the VW (OTCPK:VWAGY) Audi in the high-end list, but we also see the NIO ET5 and the NIO ET7. The Tesla (TSLA) Model 3 is not in the list because it is priced at a little bit under 300k yuan:

High-end cars in China (The November 2022 CPCA Monthly Analysis through Google Translate)

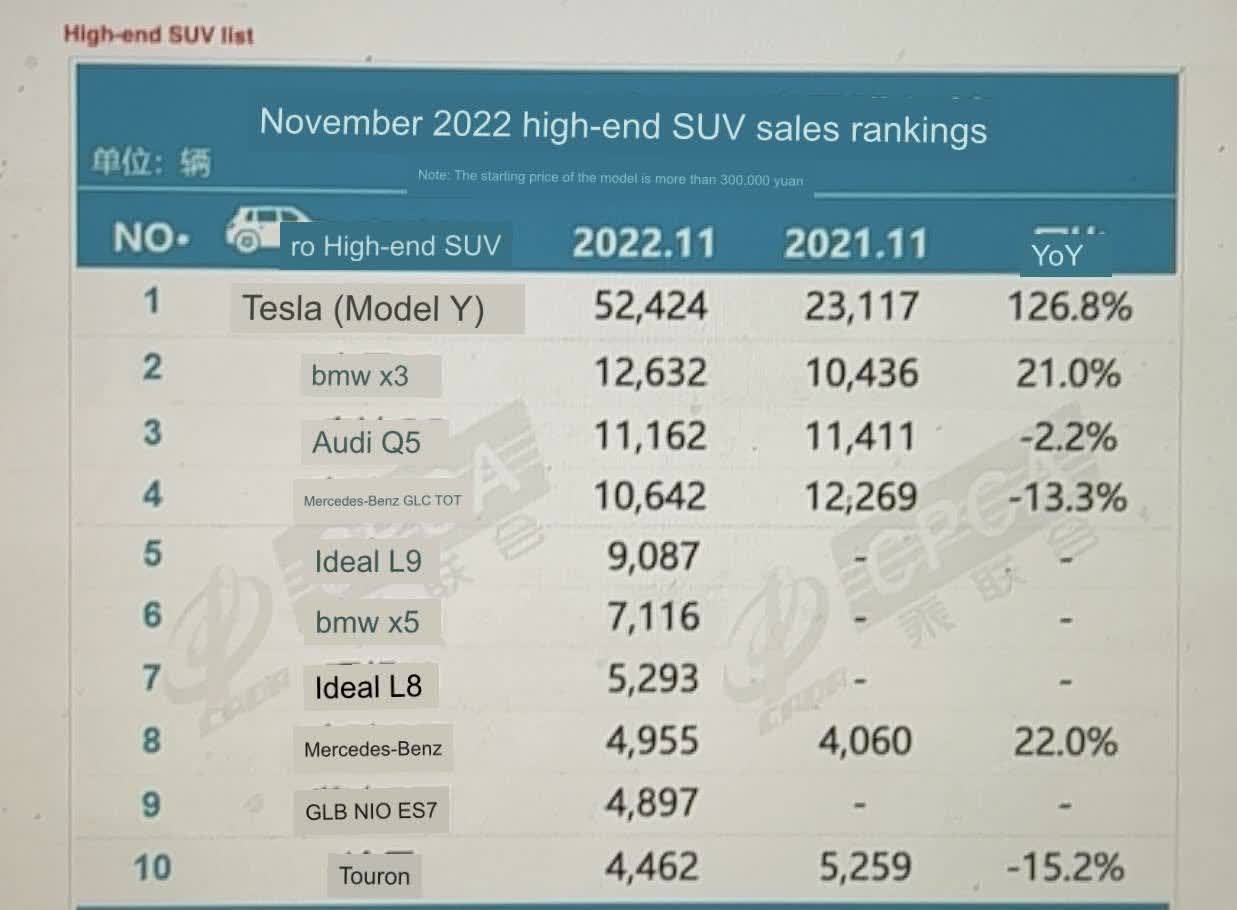

As expected, the November 2022 CPCA Monthly Analysis shows the Tesla Model Y in the high-end SUV list, along with the usual German brands. Less known to folks outside of China are the Li Auto (LI) Ideal L8, the Li Auto Ideal L9 and the NIO ES7:

High-end SUVs in China (The November 2022 CPCA Monthly Analysis through Google Translate)

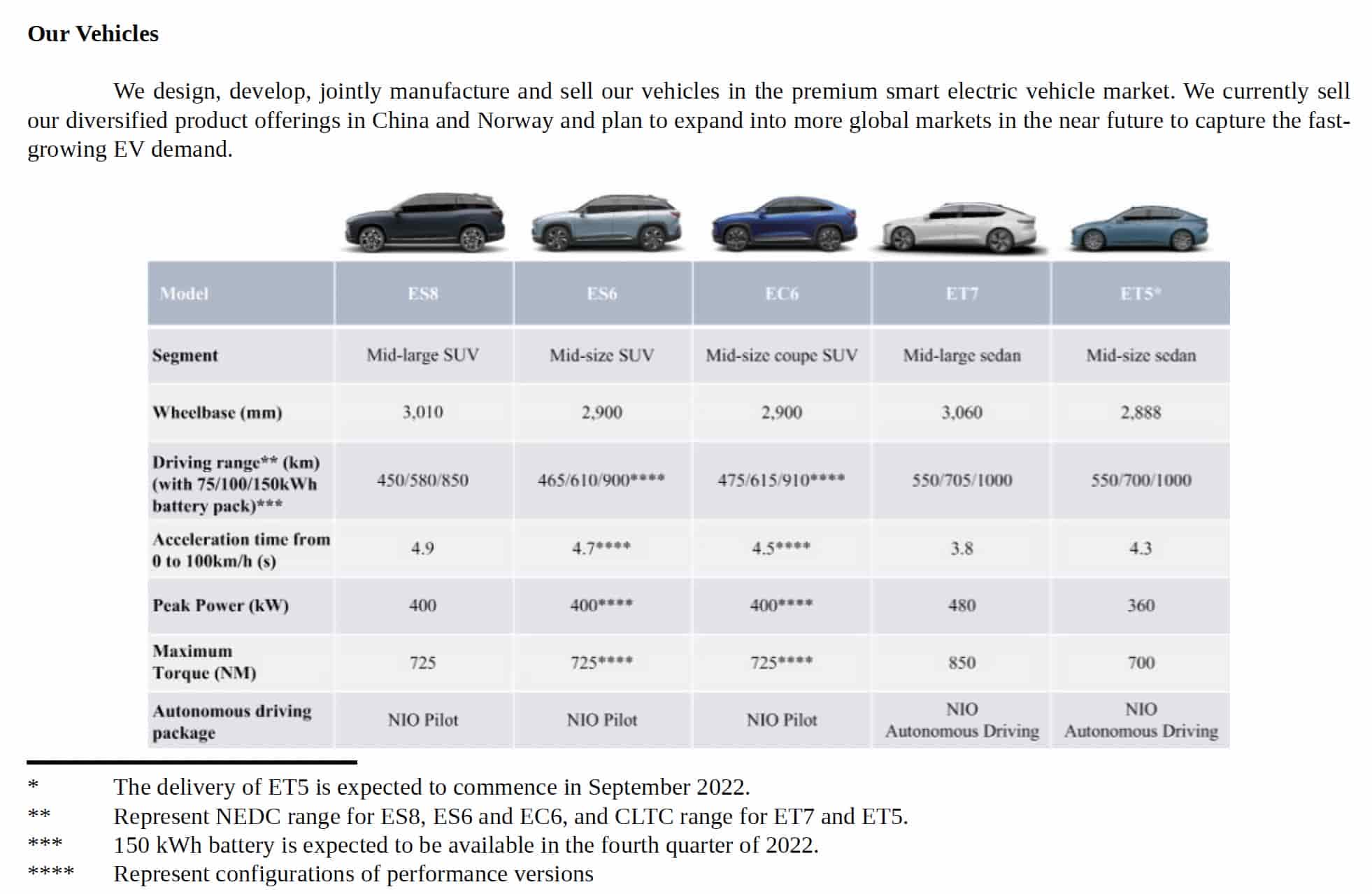

The three NIO models above combined to make up 11,045 units of NIO’s November total of 14,178. The 2021 annual report shows the above ET5 and ET7 models, but they aren’t listed in the final delivery figures for the year, and neither was the ES7 model. The 2021 annual report says for the year, they delivered 91,429 vehicles, including 20,050 ES8s, 41,474 ES6s and 29,905 EC6s:

NIO models (2021 annual report)

At the time of this writing, 100 RMB is equivalent to a little over $14.

The Numbers

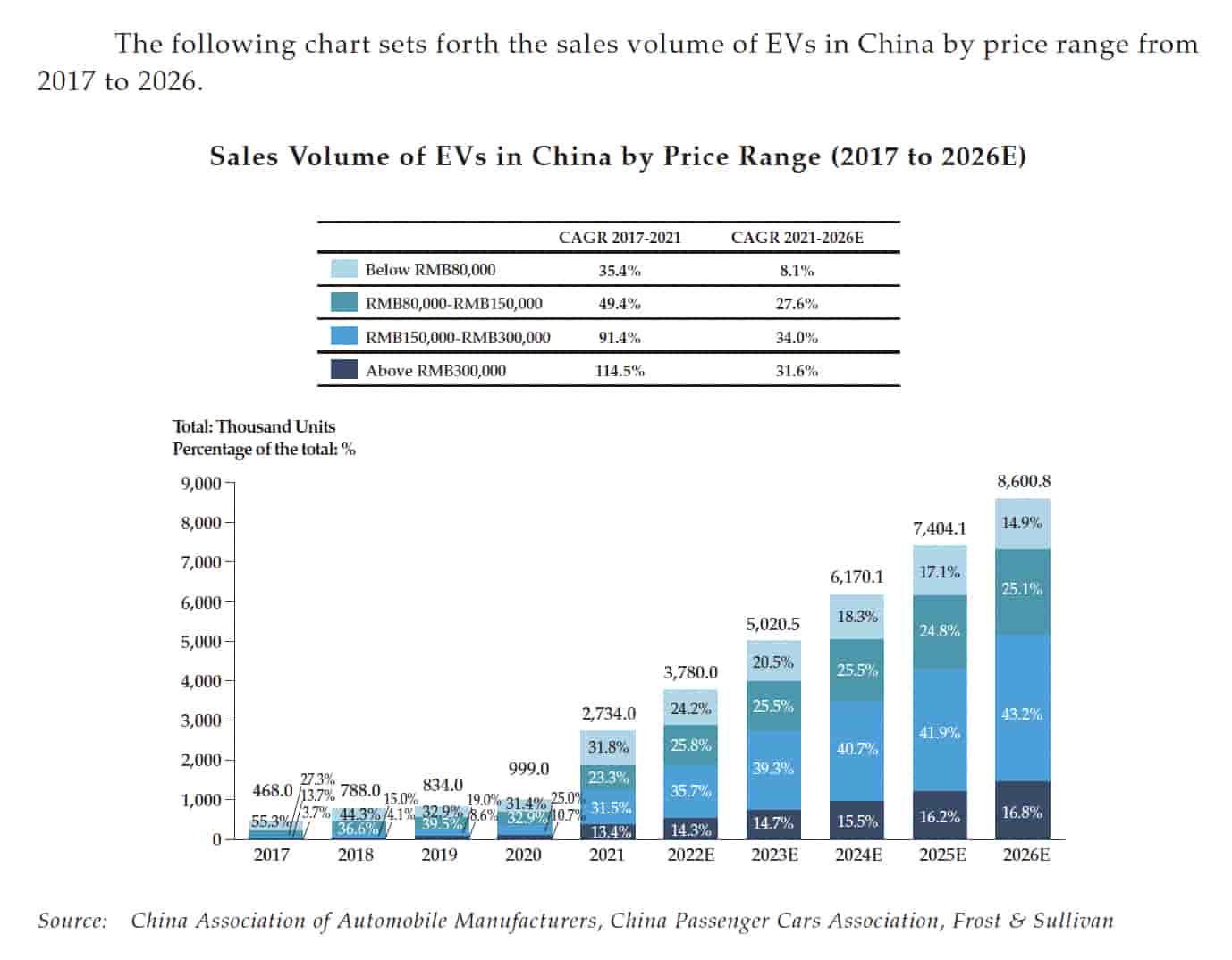

Looking at the Leapmotor global offering from September, we see prodigious growth is expected in China for BEVs selling above 300k RMB. They estimate that in 2026, we’ll see over 1.4 million [8.6 million*16.8%] BEVs sold in China in the high-end price range above 300k RMB:

China EV market (Leapmotor global offering)

It isn’t surprising that NIO is making progress in the high-end CPCA lists above. Citing a Gasgoo article, a December 2021 Seeking Alpha article talked about the face that NIO is out to replace high-end internal combustion engine (“ICE”) vehicles in China:

NIO Co-founder and President Lihong Qin clarified any doubt that investors have over which companies it is going after. The premium legacy OEMs. Affectionately coined “BBA” in China, which stands for “BMW-Benz-Audi,” these automakers are NIO’s most important competitors that it’s attempting to displace as they own the lion share of its target market segment.

We should continue to see companies like NIO and Li Auto in the high-end CPCA lists as the market moves towards electric vehicles and companies like VW and Mercedes struggle. A November Bloomberg article talks about VW’s plans to delay a key electric project due to software issues. It also reveals that Mercedes had to cut prices in China after misjudging the market.

CarNewsChina.com summarized the December 24th NIO Day in English. NIO is a charging leader in China, where their Power Home has been installed for 160,000 users. Their 13,087 public charging units are said to be the most of any company. Over 80% of the power charged is for non-NIO customers. The NIO EC7 SUV coupe was announced and deliveries will start in May:

4,968 mm long, 1974 mm wide, 1714 mm high with wheelbase 2,960mm.

75kWh battery – 488,000 yuan

100 kWh battery – 546,000 yuan

Without battery (BaaS) – 418,000 yuan

Premier edition with 100 kWh battery and Nappa interior, 21″ elegant wheels and NOMI Mate 2.0 and 6 piston brakes in Airglow Orange – 578,000 yuan (BaaS 450,000 yuan)

The NIO ES8 NT2 was the big announcement at NIO Day, and it is scheduled to be delivered starting in June. Being an SUV, it won’t compete directly with the Tesla Cybertruck, but they have similarities. Both have long range batteries and both are built with enormous casting machines such that the number of individual parts is small. Here are some details from CarNewsChina.com:

NIO ES8 comes with 22″ high gloss forged wheels

Sensors are invisibly integrated into the body

Size: 5,099mm length, 1,989mm width, 1,750mm height, and wheelbase 3,070mm

ES8 do 0-100km/h in 4.1 seconds, the drag coefficient is 0,250.

ES8 range is 465 km with 75kWh battery and 605 km with 100 kWh battery. With 150 kWh battery range is 900 km. [Multiplying by .62, the 900km range is about 560 miles]

ES8 has all aluminum body created by the world’s largest 8,800 tons die casting machine. 31 parts were merged into one thanks to the die casting.

NIO released the new ES8 pricing details on their website:

The all-new ES8 is priced at RMB 528,000 with 75kWh battery, RMB 586,000 with 100kWh battery, and RMB 458,000 with BaaS (Battery-as-a-Service). The ES8 Executive Version is priced at RMB 548,000 with 75kWh battery, RMB 606,000 with 100kWh battery, and RMB 478,000 with BaaS (Battery-as-a-Service). The all new ES8 is now available for order on NIO App in China, and the delivery is expected to start on June, 2023 in China.

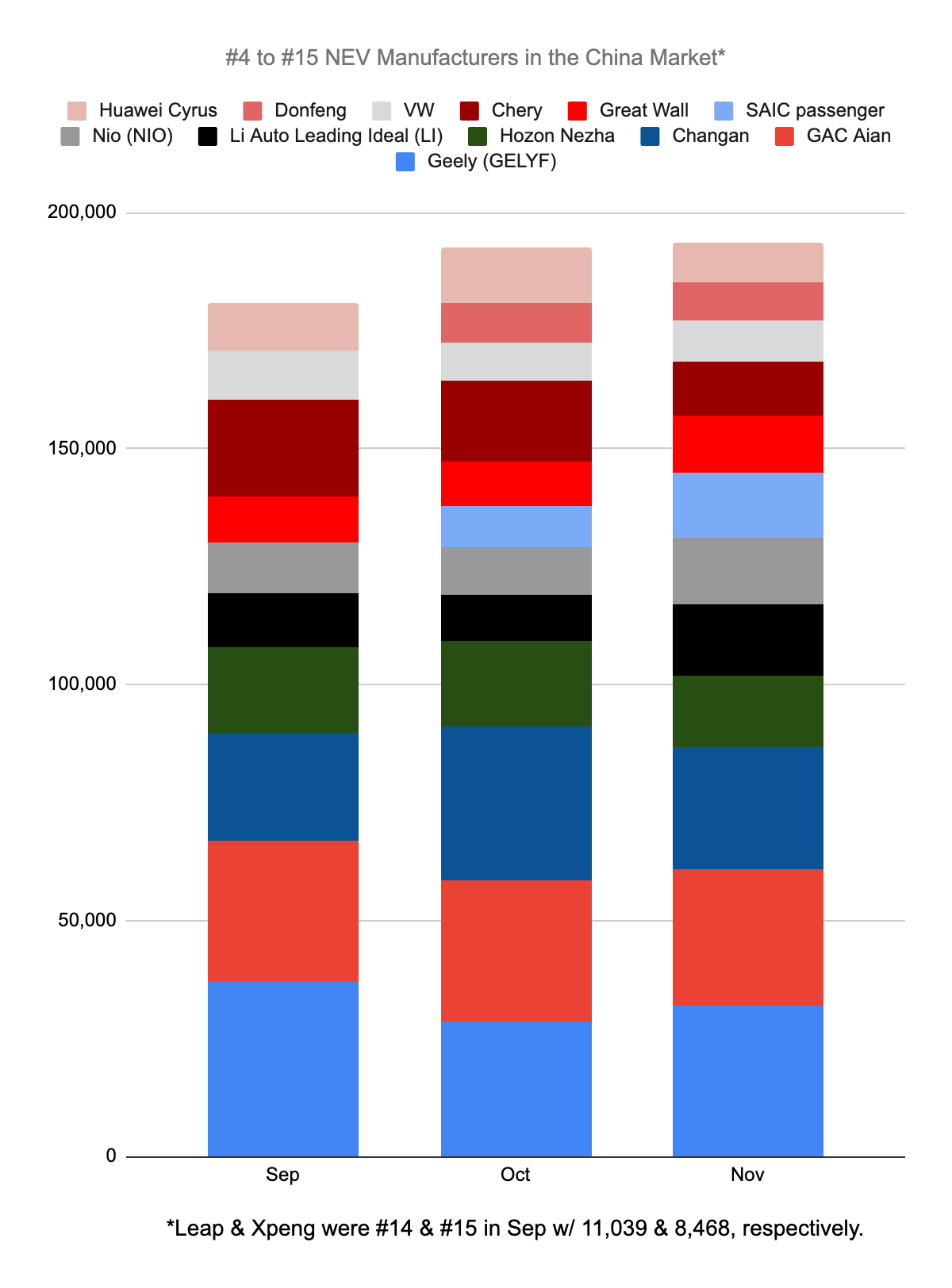

NIO continues to make its presence known in China with respect to new energy vehicles (“NEVs”). The CPCA shows that they went from 10,059 units in October to 14,178 in November:

NEV manufacturers (Author’s spreadsheet)

Looking at the NEV market share in China for November, BYD (OTCPK:BYDDY) was #1 with 36.4%, Tesla came in at #2 with 10.4% and SAIC-GM-Wuling was #3 with 5.8%. The #4 to #15 manufacturers in this graph combined for 29.5% while the remainder combined for 17.9%.

The high-end German brands aren’t the only target for NIO. CNEVPost reports that NIO CEO William Li said NIO should sell more units in China than Lexus in 2023.

Valuation

The 2021 annual report explains that the cost of sales with respect to vehicle sales also includes compensation to JAC for manufacturing. Forward-looking investors should think about how the gross margin would be different if NIO did the manufacturing themselves and how this impacts the valuation. Here is what their annual report says about the manufacturing specifics with JAC:

In March 2021, we entered into definitive agreements with JAC to establish a joint venture for manufacturing management and operations, Jianglai Advanced Manufacturing Technology (Anhui) Co., Ltd., or Jianglai. As of the date of this annual report, we hold 50% equity interest in Jianglai. In May 2021, we entered into renewed manufacturing agreements regarding the joint manufacturing of our vehicles, including ET7 and other future models, and related fee arrangements with JAC and Jianglai. JAC currently manufactures the NIO vehicles in delivery, including the ES8, ES6, EC6 and ET7, in the Hefei JAC-NIO manufacturing plant designed and constructed for NIO vehicles. For the years ended December 31, 2019, 2020 and 2021, all of our vehicles were manufactured in the JAC-NIO manufacturing plant. Pursuant to our original agreements with JAC with respect to the ES8, ES6 and EC6, we paid JAC for each vehicle produced on a per-vehicle basis monthly for the first three years. For the first 36 months after the start of production, which commenced on April 2018, to the extent the Hefei manufacturing plant incurred any operating losses, we would compensate JAC for such operating losses.

Another key consideration impacting valuation is NIO’s Battery as a Service (“BaaS”) business. The 2021 annual report explains that this allows customers to buy EVs without battery packs:

The Battery as a Service (the “BaaS”), allows users to purchase electric vehicles without battery packs and subscribe for the usage of battery packs separately. In PRC [the People’s Republic of China], under the BaaS, the Group sells battery packs to Wuhan Weineng Battery Asset Co., Ltd. (the “Battery Asset Company”), an equity investee of the Company, on a back-to-back basis when the Group sells the vehicle to the BaaS users and the BaaS users subscribe for the usage of the battery packs from the Battery Asset Company by paying a monthly subscription fee to the Battery Asset Company. The promise to transfer the control of the battery packs to the Battery Asset Company is the only performance obligation in the contract with the Battery Asset Company for the sales of battery packs. The Group recognizes revenue from the sales of battery packs to the Battery Asset Company when the vehicles (together with the battery packs) are delivered to the BaaS users which is the point considered then the control of the battery packs is transferred to the Battery Asset Company.

It can be difficult for investors outside China to understand why BaaS is necessary now that NIO has batteries with a range of 1,000 km and an ultra-fast 500-kW charger that will be available in March.. Also, NIO’s BaaS business allows short sellers to make disturbing allegations that bring uncertainty into NIO’s valuation range.

4Q22 delivery estimates were revised downward on December 27th, but December should still be a great month relative to October. Again, NIO is doing a great job increasing the number of high-end BEVs that they sell each year. The CPCA November 2022 retail sales report lists NIO in both the high-end SUV lists [300k yuan or more] and the new energy SUV lists. The ES7 SUV wasn’t available in November 2021, but it had monthly sales of 4,897 units in November 2022. The ES6 SUV had ytd sales of 40,281 units through November, which was an increase of 10.3%. The monthly CPCA new energy manufacturing list shows NIO in the #9 spot for November with 14,178 units, a 30.3% increase over the 10,878 units in November 2021. This is better than NIO’s #12 spot in the ytd list where they have 106,671 units for the first 11 months of 2022 which is up 31.8% from their 80,940 units for the first 11 months of 2021. I think NIO will continue to take share from high-end ICE vehicles, but more competition is coming in the BEV space. A December 8th Pandaily article reported that the logo for BYD’s luxury brand, Yangwang, has been revealed. The price range of these vehicles is expected to be 800,000 yuan to 1.5 million yuan.

The fact that NIO specializes in high-end vehicles is key for the valuation framework. In the 3Q18 call, CFO Louis Hsieh reveals that NIO compares well to premium brands like Mercedes, BMW, Audi and Tesla. He notes that NIO is better than these brands with respect to a more luxurious and spacious interior, a comfortable ride and a customized entertainment system.

Hammering home the importance of high-end vehicles, it is pointed out in the 1Q21 call that a relatively small number of Porsches make up much of the gross profit for the Volkswagen Group. NIO management says Porsche probably contributes 40% of VW’s gross margin, with only about 300,000 units. This shows that market share alone is a shallow way of looking at the business.

In the 3Q21 call, it was revealed that a 25% gross profit margin could be expected with 300k units shipped per year on the NP2.0 platform. This was before battery costs got out of control the next year. In the 3Q22 call, CEO William Li said that battery costs skyrocketed in 2022 which put pressure on gross margins. He said that if battery prices get under control and other things fall into place, then a 25% to 30% gross margin range can be reached.

The 3Q22 results show quarterly revenue of just over 13 billion RMB, which was nearly 33% higher than the 3Q21 figure of 9.8 billion RMB. NIO is worth the amount of cash that can be pulled out of it from now until judgment day, but there are many moving parts during this early time of the company’s history. It’s hard to say what the gross margin will look like over the next 5 to 10 years, let alone the free cash flow (“FCF”).

The 2021 annual report shows 164,249,629 ordinary shares beneficially owned by Tencent entities. Per the 3Q22 results, each ADS represents one ordinary share. There were 1,640,001,909 weighted shares in the 3Q22 period. I think the share count at the end of the quarter was higher than this number, and 18 million shares were issued in November. As such, I think the number of shares outstanding is closer to 1.7 million. Multiplying this by the December 27th ADS price of $10.06 gives us a market cap of about $17 billion. The enterprise value is fairly close to the market cap. At this point in time, I don’t know if the stock is reasonably priced or not. Forward-looking investors should continue to watch NIO’s monthly unit numbers and their gross margins. In time, it will be easier to use these and other numbers to come up with a valuation range. CEO Li said NIO should be able to pass Lexus with respect to unit sales in China for 2023. Obviously, these types of benchmarks will be important from a valuation perspective.

Be the first to comment