da-kuk

Last April Fool’s day, I sold F5 (NASDAQ:FFIV) for a 25% gain, and since then, the shares have dropped about 30% against a loss of 11.5% for the S&P 500. A more secure man than me would not linger on that performance, but that’s not me, I’m afraid. Keeping that performance firmly in mind, I want to review the investment again. After all, a stock trading at $145 is, by definition, a much less risky investment than the same one when it was trading at $210. Since the company just reported earnings, I’ll review those, and I’ll compare them to the valuation of the stock. Previously, I did well selling put options, and I want to see if it’s possible to make some decent risk adjusted returns with those also.

I know you’re a busy group of people, dear readers. For that reason, I want to save as much of your time as possible. This is one of the many ways that I try to make your reading experience as enjoyable as possible. I think F5 has just had a moderately good financial year, in spite of an alarming uptick in expenses over the past few years. Additionally, the capital structure remains very solid for this consistently profitable firm. Finally, the valuation is much more attractive than it was when I sold my shares, so I’ll be nibbling today. I’m not going to take a full position, but will buy 100 shares to start, and I hope to buy another 200 opportunistically over the next few months. Finally, while I normally like selling deep out of the money put options on companies like this, I think it makes much more sense to simply buy the shares at the moment.

Financial Snapshot

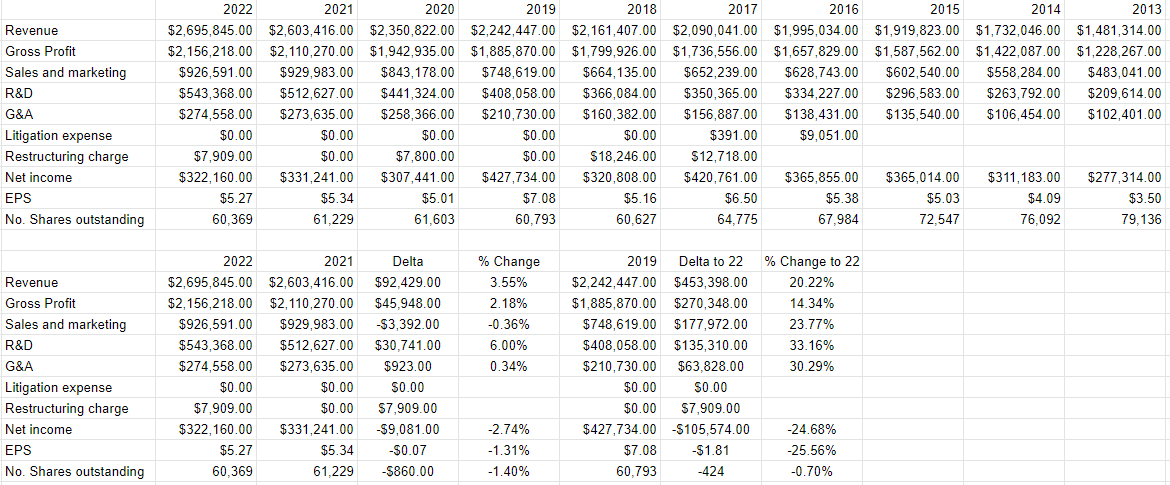

As I mentioned way back at the start of this article, the company has just released annual results, and I don’t think they’re too bad, actually. Revenue grew at a very moderate 3.6%, while net income fell by about 2.75%, mostly driven by a $30.7 million uptick in R&D expenses. So, the company remains consistently profitable at least. Additionally, sales are up about 20% relative to the pre-pandemic era, which is not something I can write about every company I’ve reviewed recently. Net income is down dramatically from then, though. This is because ongoing expenses like R&D, G&A, and sales and marketing are up even more than revenue. In 2022, the company spent about $177 million more on sales and marketing expenses, $135 million more on R&D expenses, and $63 million more on the ambiguously named “G&A” expense than they did in 2019. I’m not sure why these expenses rose by between 23 and 30% in two years, but it’s concerning.

On the plus side, the capital structure remains fairly strong here. Specifically, cash and short-term investments represent about 31% of total liabilities at the moment, which is a positive development. For that reason, I don’t see much credit or insolvency risk here.

All that written, the company remains profitable enough, and the balance sheet is quite strong. Given that, I’d be willing to buy back in at the right price.

F5 Financials (F5 investor relations)

The Stock

My regulars know that I’ve talked myself out of some profitable trades with the words “at the right price.” So, if you’re heading to the comments section to write about how my fastidiousness in this regard is self-harming, save yourself the effort because I’m way ahead of you. In response to this criticism, I’d point out that I’m of the view that it’s better to miss out on some gains than lose capital. My regulars also know that I consider the “business” and the “stock” to be quite different things. Every business buys a number of inputs and turns them into a final product or service. The stock, on the other hand, is an ownership stake in the business that gets traded around in a market that aggregates the crowd’s rapidly changing views about the future health of the business, future demand for cloud security services, future margins, and so on. The stock also moves around because it gets taken along for the ride when the crowd changes its views about “the market” in general. A reasonable sounding, if counterfactual, argument can be made to suggest that shares of F5 have dropped since last April in large measure because the S&P 500 itself is down since then. In other words, some portion of F5’s 30% loss could reasonably be attributed to the 11.5% drop in the overall market since. Of course, it’s impossible to prove this point definitively, but it’s worth considering. In any case, the stock is affected by a host of variables that may be only peripherally related to the health of the business, and that can be frustrating.

This stock price volatility driven by all these factors is troublesome, but it’s a potential source of profit because these price movements have the potential to create a disconnect between market expectations and subsequent reality. In my experience, this is the only way to generate profits trading stocks: By determining the crowd’s expectations about a given company’s performance, spotting discrepancies between those assumptions and stock price, and placing a trade accordingly. I really hate to remind you of my performance here, because I’d hate to come off as a braggart, but this is the approach I took when I bought the shares at a cheap price, and when I then sold them at an expensive price. The expectations went from “too dour” to “too optimistic.” I’ve also found it’s the case that investors do better/less badly when they buy shares that are relatively cheap, because cheap shares correlate with low expectations. Cheap shares are insulated from the buffeting that more expensive shares are hit by.

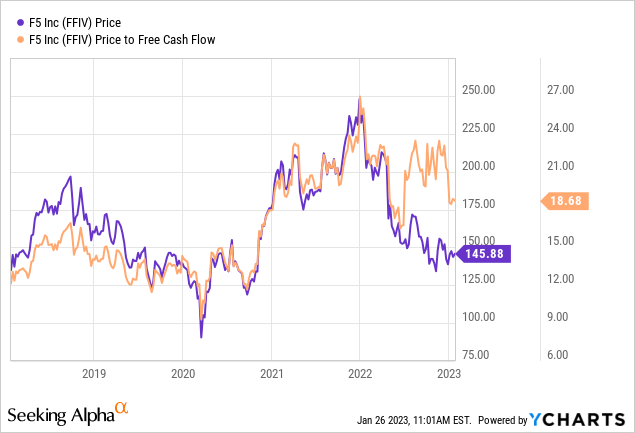

As my regulars know, I measure the relative cheapness of a stock in a few ways, ranging from the simple to the more complex. For example, I like to look at the ratio of price to some measure of economic value, like earnings, sales, free cash, and the like. I like to see a company trading at a discount to both the overall market, and to its own history. I sold F5 back in April when the shares were trading at a price to free cash flow of 22.8. Fast forward to the present, and the shares are about 18% cheaper per the following:

Source: YCharts

Although they’re “cheaper,” they’re not “cheap,” especially when compared to their own history, which makes me a bit nervous.

My regulars know that I think ratios can be instructive, but I also want to try to work out what the market is “thinking” about a given investment. If you read my stuff regularly, you know that the way I do this is by turning to the work of Professor Stephen Penman and his book “Accounting for Value” for this. In this book, Penman walks investors through how they can apply some pretty basic math to a standard finance formula in order to work out what the market is “thinking” about a given company’s future growth. This involves isolating the “g” (growth) variable in this formula. In case you find Penman’s writing a bit opaque, you might want to try “Expectations Investing” by Mauboussin and Rappaport. These two also have introduced the idea of using the stock price itself as a source of information, and we can infer what the market is currently “expecting” about the future. Applying this approach to F5 at the moment suggests the market is assuming that this company will grow earnings at a rate of ~2.5% in perpetuity. I consider that to be a pretty reasonable forecast, actually. Given the above, I’m willing to nibble on the shares at current prices.

Finally, while I like deep out of the money put options, I think the shares make more sense at current prices. For instance, the July F5 put with a strike of $120 is currently only bid at $2.80. Given that this yield is fairly paltry, and given that I think the valuation is reasonable, I think stock ownership makes more sense in this instance.

Be the first to comment