Anne Czichos/iStock Editorial via Getty Images

Dear readers/followers,

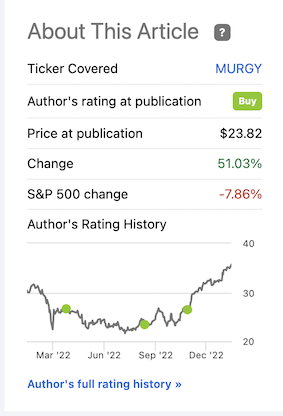

One of my best investments for all of 2022 and going into 2023 has been the company Munich Re (OTCPK:MURGY), the largest reinsurance business on earth. I say this because if we look at the RoR since my August article back in 2022, the RoR has been close to 60% compared to the market, annualizing into the triple digits.

Munich RE Article (Seeking Alpha)

Many people asked me when I posted the fact that I outperformed the broader market by over 40% last year, how such a feat was possible – going over 5% in the green during a double-digit dip year. The answer is simple – through investments exactly like this one.

This is the approach I try to take.

- I find the undervalued, underappreciated and higher-yielding/fundamentally safe companies out there, wherever they may be at the time.

- I buy them.

- I hold them until my target, and either hold them for longer or start trimming and repeating investments into companies that fulfill step #1.

MURGY has been a perfect example of this strategy working very well in the short term. Now it’s time to reap the rewards.

Let’s recap MURGY and look at the 2023 thesis.

Munich Re – I Hope you bought

So, the reason I loaded up on a full MURGY position of 5% in my portfolio when the company was cheap was easy. It’s all about company performance, fundamentals, safety, lack of negatives/risks, and a very storied tradition of outperforming and anti-risk approaches.

The company’s operations as we move into 2023 come in the form of Life, Non-Life, and Reinsurance operations, with the third obviously being the largest at still over 70% of overall sales. Munich Re has made a history of performing well when competitors have been down or posted losses, thanks to really superb underwriting standards and safeties. On a high level, Munich Re is perhaps the most conservative, traditionally German-led reinsurance business on the entire planet – and this is why, and what I wanted to invest in.

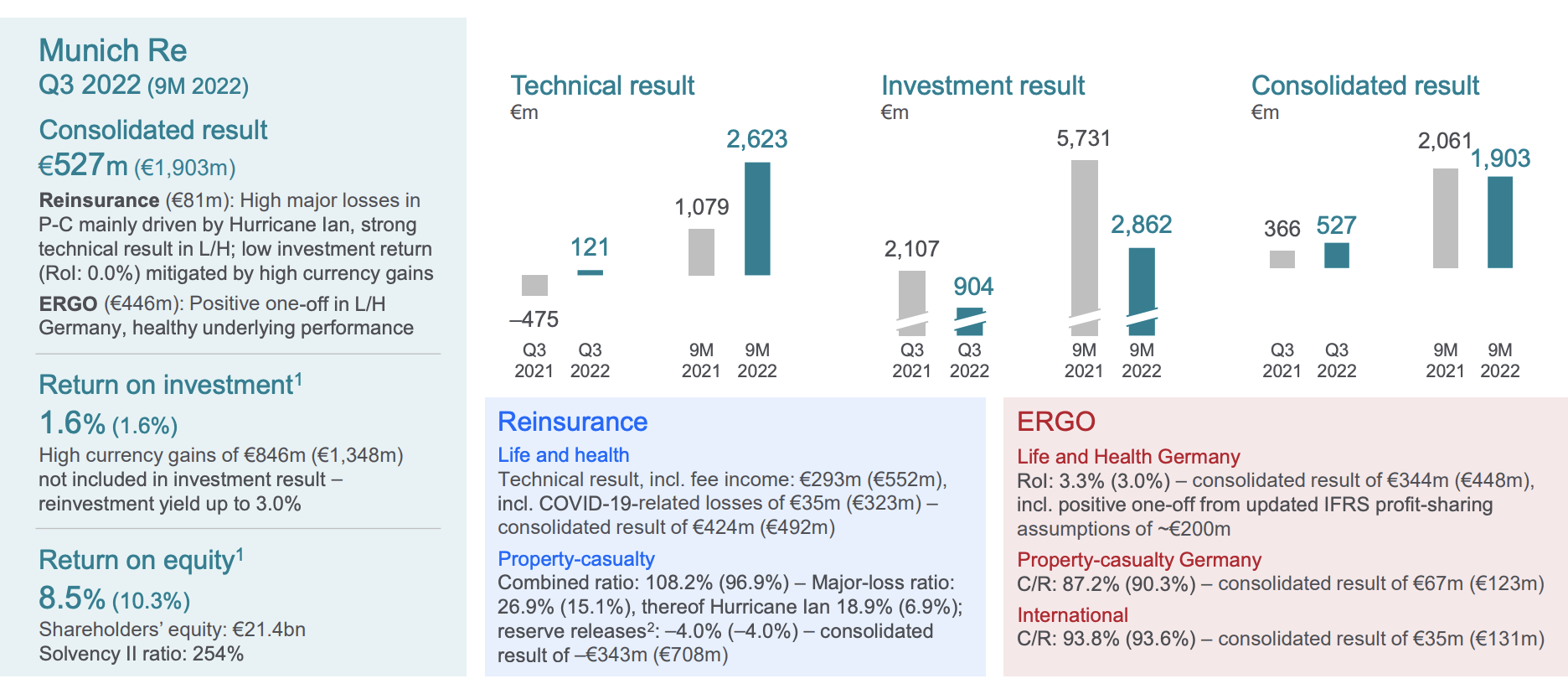

3Q22 results confirm why this was a good idea to invest, aside from the overall obvious returns that we’re seeing here. Despite overall losses, with investment results, consolidated results, and technical results down for the year, the company’s operations were resilient.

Munich Re IR (Munich Re IR)

The company, being a reinsurer, suffered from Hurricane Ian, but was weighed up by strong results in L/H, but then further pressured by negative market returns. RoI came in low, and RoE was down as well. ERGO provided the sort of cushion that the company has been looking for to offset its more volatile segment, but it didn’t manage to offset every piece of volatility here – there was simply too much of it. Unlike AXA (OTCQX:AXAHY), which managed to offset its Hurricane losses quite impressively, Munich Re remains somewhat overexposed due to its reinsurance lines, and I don’t see that changing in the near-term future.

However, this is the life of reinsurance companies.

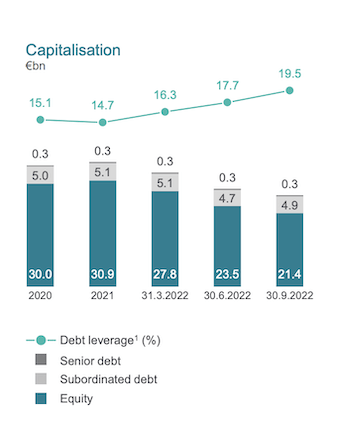

During times of trouble, the company’s dynamics come into play – so we need to look not at the negative/lower results, but at how the company’s capital position has played out. The dividend payout, unrealized gains and losses, and share buybacks led to lower equity, which in turn affected debt leverage. The company’s leverage has gone from 15.1% to nearly 20% at this time, though the company’s capitalization is still solid.

Munich Re IR (Munich Re IR)

Munich Re is a very dollar-heavy business, so USD FX will continue to have an impact here, regardless of how things go. The company’s investment portfolio is far from as large as Allianz, but still comprises total investments of €228B as of 3Q22. This is comprised mostly of fixed-interest and loans, though it’s less safe than some investment portfolios I’ve seen. The company has seen an increase in the reinvestment yield due to interest rate increases and credit spreads – and this is expected to continue going forward as well.

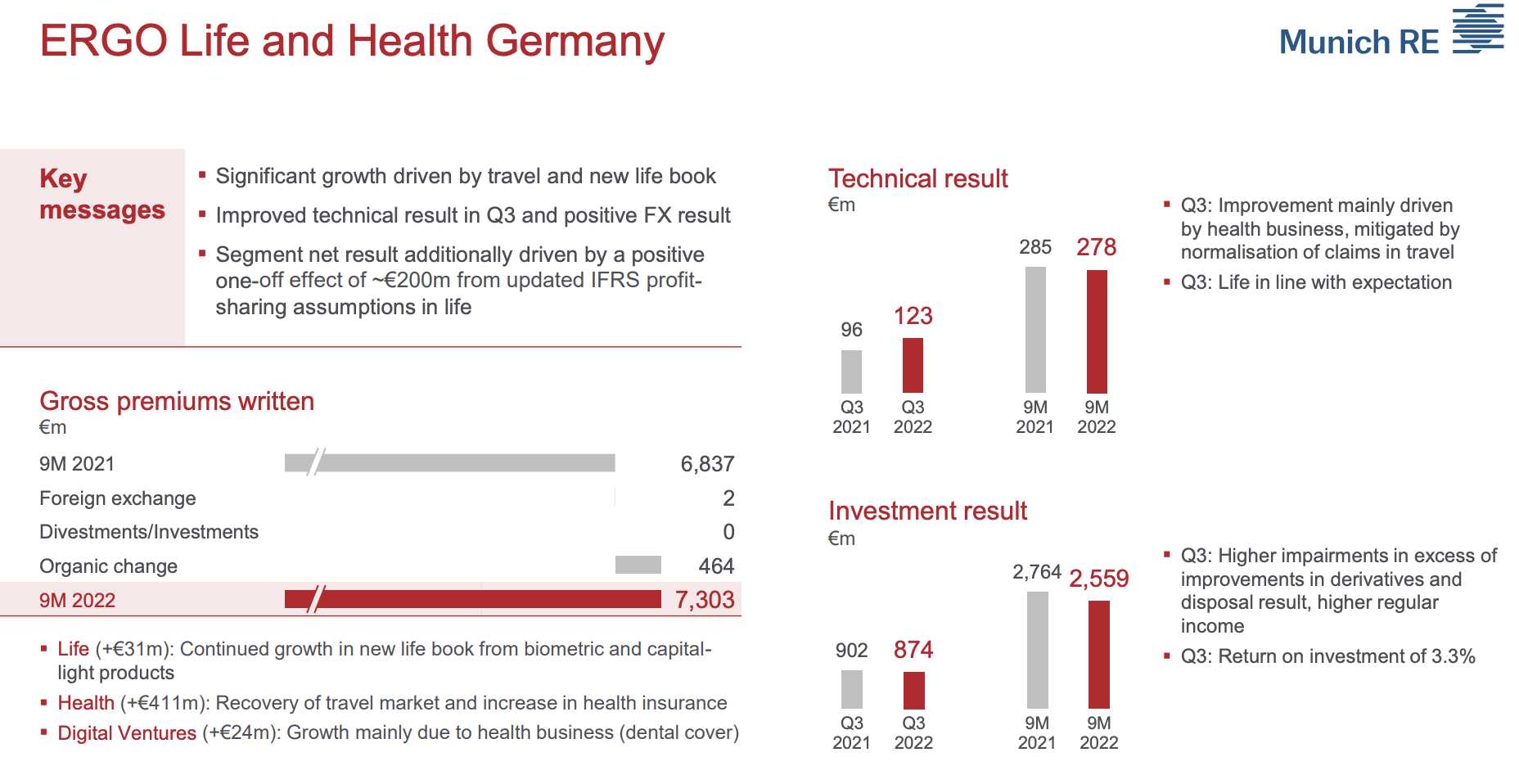

The positive we can look at here, that’s a straight plus for the quarter, is Ergo.

Munich Re IR (Munich Re IR)

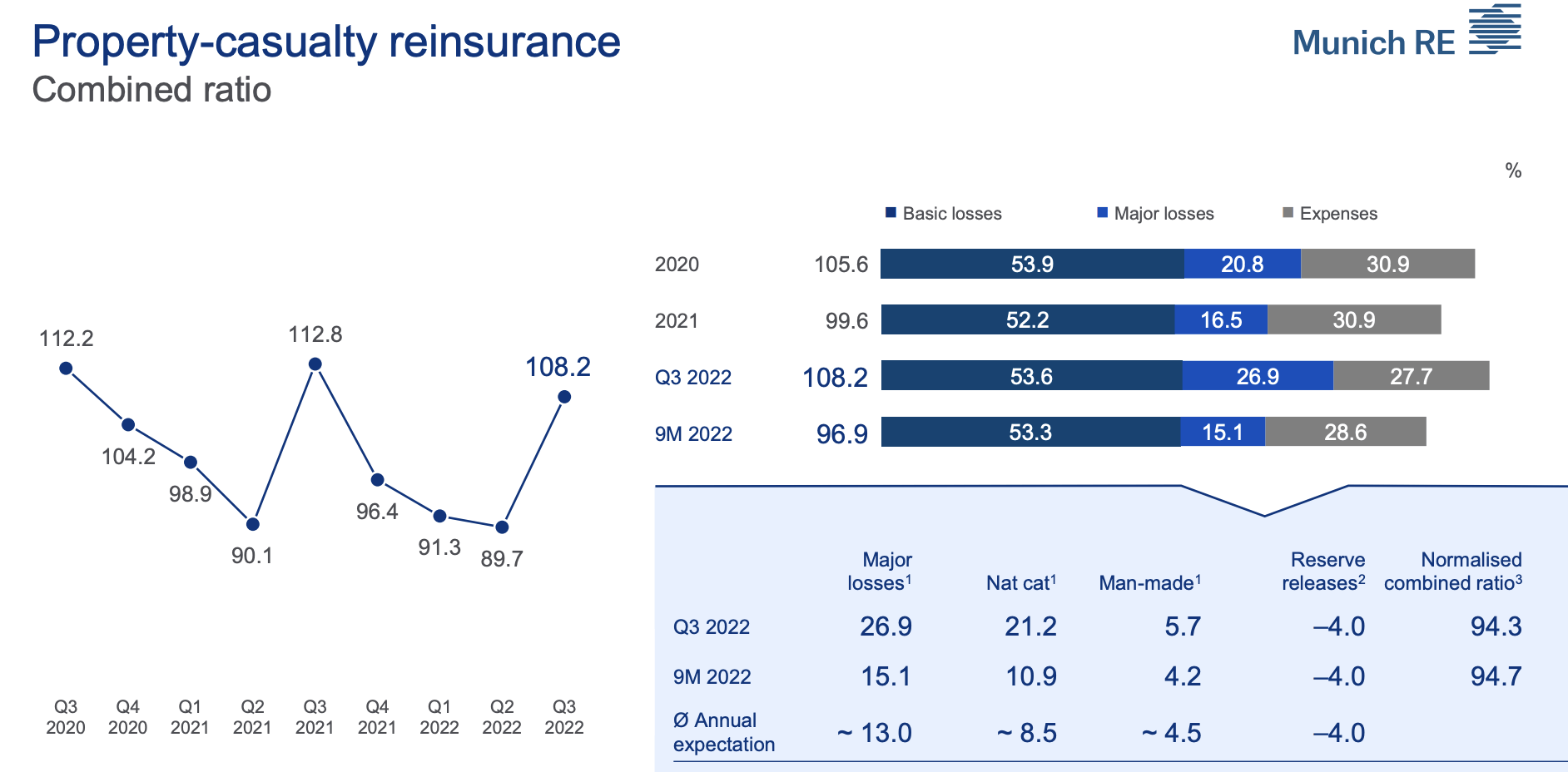

ERGO also had solid results in P&C and in the international segment, showcasing combined ratios of below 94%. It’s not as good as some Scandinavian insurance companies, which routinely work below 88%, but it’s still good enough. Gross premiums are up, and while Ergo can’t measure to the company’s core reinsurance operations, it’s still an impressive set of results.

Despite the company’s suffering from hurricanes and other impacts, strong technical results and premium growth were recorded in the reinsurance P&C and L/H segments – though due to these ups and downs, combined was up over 105%. However, as you can see in the company’s QoQ, this is a relatively normal sort of thing with this company, at times going below 90%, and sometimes below 110%.

Munich Re IR (Munich Re IR)

More importantly, the normalized combined ratio here was solid, and the company has given us 2022E, with a 2025E as well. The company’s ambitions for 2025E are being met, and 2022E is mostly on track. The company now expects €3B more in gross premiums, with the same result at around €3.3B net, with an RoI of somewhat above 2%. They are not record results, but they still present a more appealing, diversified mix than it was some years ago, thanks to Ergo. The company’s insurance arm is really becoming a force to be reckoned with, writing almost €20B worth of premiums at a result of €0.8B, which is frankly a better result than the lower RoI-reinsurance number.

Risks to Munich Re here? Relatively few, all things considered.

I’m looking at how P&C renewals might become depressed in the near term, I expect seasonality out of some of these results even if guessing the quarterly flows from here on out is just that – bit much; guesswork here. The company is in a growth stage due to Ergo, and due to that, we can expect some volatility going forward. The company did provide a bit of an idea, an income target for 2023. The company also seems to be planning to sell at a loss some of its bonds, in order to be able to reinvest at some of the higher yields available on the fixed income market today – not a huge loss, as things are being forecasted, but still one to be considered as it will lead to higher loss realizations, which the company is already facing.

All in all, Munich Re is performing very well, as the share price reflects. But the share price also reflects a growing, perhaps overconfidence in the company which might turn out to be a step taken too far.

Let’s move into valuation and see where we have things here.

Munich Re’s valuation – is a bit tricky at this point.

The reason I say MURGY’s valuation is growing a bit tricky here is that when I bought the company, it was essentially quite undervalued. I invested at P/Es of below 9x. At a 4-year TSR of almost 71.6%, the company drives sector-leading profitability and growth, and its outlook for 2022 includes over €60B of gross premiums and a net result of €3.3B.

None of these recent results influence that positive outlook, but the pricing for this company has now reached nearly a fair-value sort of level.

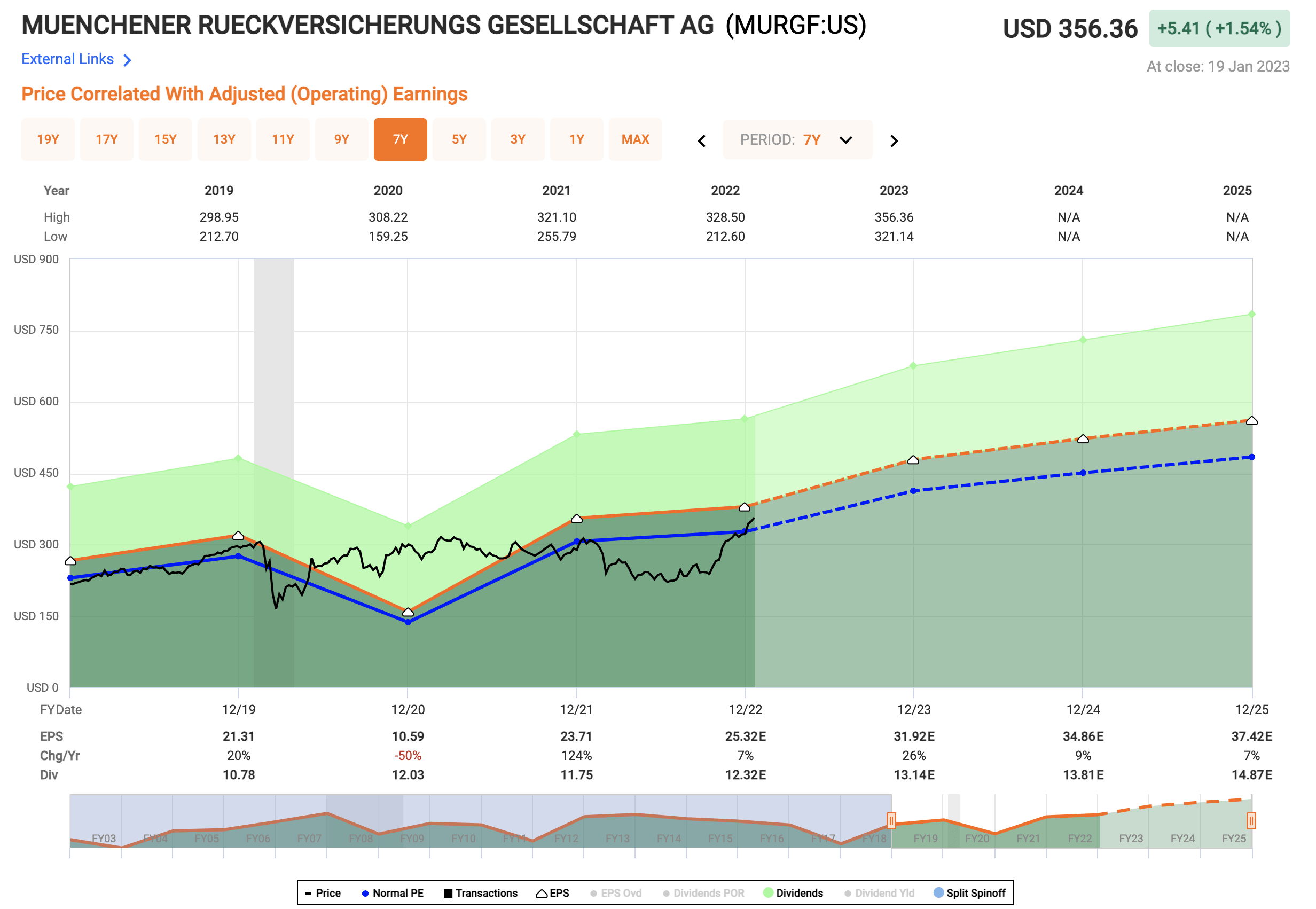

Since my last article, we’re now also firmly above the company’s 7-10-year P/E average, which comes to about 13x for the ADR, and where the company now trades closer to 14x.

Munich Re valuation (FAST Graphs)

Yes, the company is AA-rated, and yes, the company may still have far ways to go in terms of valuation. The fact that it’s set to grow earnings at double digits going forward should be enough to see the company climb further, but don’t forget that this company typically doesn’t go for a premium, but for a discount.

Looking at the native share price trends further illuminates this. MURGY’s 10-year average lies somewhere close to 10.64x NTM P/E – the current multiple is closer to 10.9x. Anywhere you look, you find implications that the company has reached the top of the range of where it usually trades. Even S&P Global analysts and their target have sort of reached an end, with the average coming to €327 from 18 analysts, with 7 of these analysts at a “BUY” – but only 7. The upside is becoming more and more difficult to see, and there’s no more than a 1% upside from the current share price of €326/share.

Assuming the company does realize its growth and goes for its 12-13x P/E, that’s still potentially a double-digit 2025E upside. At the same time, the company’s share price history shows the potential for volatile downturns in earnings, which could have driven share prices lower. MURGY has been a flat investment, underperforming the market with a sub-5% RoR for almost 8-9 years at times.

Whenever a company moves like a rocket in one direction without seeming cause – and I don’t see anything new at this point for MURGY, there’s the very real possibility of a normalization that could happen just as quickly.

MURGY is a non-trivial position for me. I invested almost 4.5% of my net worth in the company a year ago. Because of this, I’ve started slowly carving away at my position to realize profits and reinvest them at better-valued investments with upsides that go higher. Not because MURGY is bad, but because I see better upsides elsewhere.

Back in April, I ended at a conservatively-adjusted PT of €280. If I didn’t shift this PT at this point, MURGY would be overvalued to the degree where rotation or trimming would become, according to my model, a necessity, not an option. I do see improved trends, but not enough to raise my PT to €330. The cyclicality for these companies is still very much in play. While the company will deliver slightly more business, it’s also weighed down by the fact that returns will be slightly lower. Hurricane Ian is a very good example of this, and this volatility and potential for losses on a quarterly basis is the main reason why I’m not bumping my share price target higher than €295 – I simply feel that at the valuation multiple, despite Munich Re’s fundamentals, there are more solid alternatives out there that will give you better potentials for outperformance. In order to go over €300/share in my target, I would want to see confirmed, positive renewals out of the business, which we’ll see in early 2023, while negatives decline.

I am conservative here, but I’m slightly bumping my PT – but the first number is not a “3”. For that reason, I’m also needing to shift my stance here.

My current stance for the company is a “HOLD”, and I give MURGY a long-term target of €295/share for the native.

Thesis

My thesis for Munich Re is as follows:

- Munich Re is the largest reinsurance company in the world, and also one of the most conservative in existence. It has a double-A credit rating, a high, 4.5%+ yield, and a set of fundamentals and titanium-clad underwriting processes that make the company a no-nonsense leader in the business.

- The recent set of results confirms the long-term upside for me, and I see no reasons why this company should be valued as it currently is – even though I am happy that it is.

- I would give the company a PT of €295/share here. That makes the company overvalued, and I would give the company a “HOLD” here. I have started trimming, and I don’t believe it is a bad idea to do the same.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.’

Here are my criteria and how the company fulfills them (bolded).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Munich Re is no longer cheap, or has a sort of realistic upside based on a price or margin of safety that I would look for. Because of that, it’s a “HOLD”.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment