Evkaz

Author’s note: This article was released to CEF/ETF Income Laboratory members on September 8th.

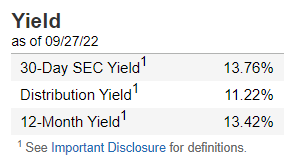

The VanEck Vectors Mortgage REIT Income ETF (NYSEARCA:MORT) is an index ETF investing in mREITs, which focus on leveraged mortgage investments. Leverage boosts income, leading to a strong, fully-covered 13.4 yield%. Leverage boosts risks, volatility, and potential losses during downturns too, and could prove particularly ruinous during a severe downturn centered on the housing market, as during the financial crisis of 2008-2009. In my opinion, MORT’s risks outweigh its benefits. As such, I would not be investing in the fund at the present time.

MORT – Basics

- Investment Manager: VanEck

- Underlying Index: MVIS US Mortgage REITs Index

- Dividend Yield: 13.4%

- Expense Ratio: 0.41%

- Total Returns CAGR 10Y: 3.01%

MORT – Overview and Analysis

Index and Holdings

MORT invests in mREITs, financial institutions which focus on leveraged mortgage investments. It tracks a broad-based mREIT index, with investments in most relevant securities of its kind. mREITs are a bit of a niche, unique asset class, so a closer look at their operations might be warranted. Let’s use Annaly Capital Management (NLY), MORT’s largest holding, as a representative example.

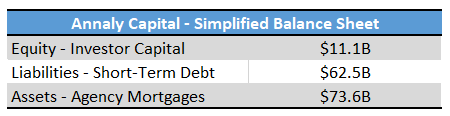

Annaly’s latest balance sheet, simplified, is as follows.

Annaly Quarterly Report

From the above, one can say the following. For every dollar in investor capital (equity), Annaly borrows six dollars (liabilities), for a total of seven dollars in capital. All seven dollars are invested in agency mortgages (assets). Debt is significantly greater than investor capital, and most assets are financed with debt.

Annaly’s balance sheet is typical for its industry, with important implications for the company and its investors. Let’s have a look at these.

Leverage – Risks and Negatives

Liabilities are senior to equity. Annaly must make contractually obligated interest rate and capital payments on its debt before paying investors a single penny in dividends. Annaly has a lot of debt, so these are very large payments, and there are risks and difficulties to these. Two stand out.

First, debt must be repaid, in full, even if asset prices decrease or mortgage payments cease. Shortfalls must be covered by investor capital if there are no other sources of capital available. Annaly has a lot of debt, but very little in equity, so investor capital would be rapidly depleted from even a small drop in asset prices.

As an example, if asset prices were to drop by 10%, Annaly would see capital losses of around $7.4B. As debt must be repaid in full, these losses would entirely accrue to investors, which only have $11.1B in capital. Investors would see most of their capital evaporate from a 10% drop in asset prices. Disastrous losses from only a moderately negative scenario.

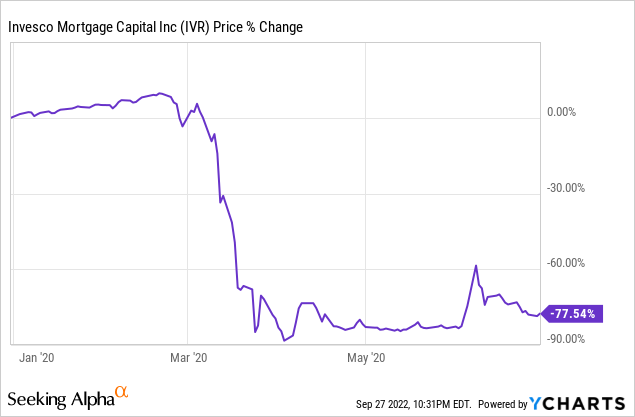

The risks above are lessened by the fact that mortgages are relatively safe securities with low default rates, but not eliminated. mREITs do sometimes see disastrous losses and results, as was the case for The Invesco Mortgage Capital (IVR) during early 2020. The coronavirus pandemic led to declining asset prices and evaporating liquidity across investment markets. IVR was forced to sell its assets at fire-sale prices to pay back its debt, leading to capital losses for investors of 80%, and a dividend cut of 95%. These losses were mostly permanent, so investors have not, and will not, be made whole.

Seeking Alpha

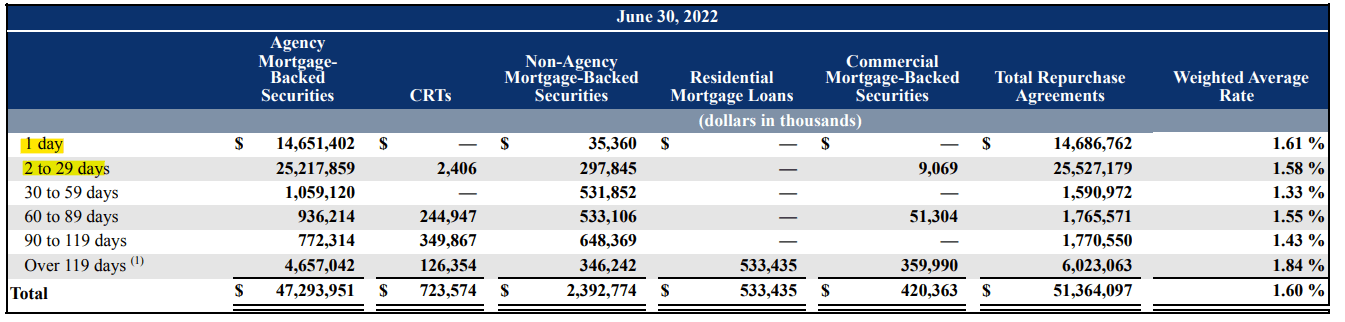

Second debt-related risk is asset-liability mismatch. Annaly and other mREITs have a lot of assets which can be used to cover their liabilities, but the terms and conditions of these are different, so there might be difficulties in doing so. Specifically, most mREITs have long-term maturities but short-term debt. Annaly’s assets, for instance, have an average maturity of between five and ten years.

Annaly Quarterly Report

Annaly’s liabilities, on the other hand, have an average maturity of less than thirty days.

Annaly Quarterly Report

So, Annaly might have to pay back a significant portion of their debt next month, but it will only receive back their mortgage principal next decade. Annaly bridges that massive duration gap by continuously rolling over their debt: every month they ask for another loan, and every month they get it. There is, however, no guarantee that they will receive another loan next month. Liquidity is not guaranteed, and tends to dry up during downturns, recessions, and other periods of worsening economic conditions. IVR, for instance, was hit with margin calls in early 2020, and the company faced severe liquidity and financial constraints at the time. IVR survived, but the company and its peers might have less luck next time.

MORT focuses on mREITs, which tend to be excessively leveraged, risky investments. Leverage does, however, have its benefits. Let’s have a look.

Leverage – Positives and Negatives

Let’s go back to Annaly’s simplified balance sheet.

Annaly Quarterly Report – Chart by Author

As can be seen above, Annaly’s assets are financed mostly with debt, only a small bit with equity.

Investors are entitled to the residual income and cash-flow generated by the company’s assets after paying debt holders. Importantly, Annaly’s investors are entitled to the residual income of the company’s entire, massive asset base even though they only made a relatively small capital investment. Investors made a $11.1B equity investment, but receive the (residual) profits of $73.6B in assets. Potential profits for investors are quite large relative to the size of their investment, a significant benefit for the same. Annaly’s assets are almost entirely income-producing mortgage-backed securities, so these higher potential profits take the form of significantly increased income, with the company yielding a massive 17.1%.

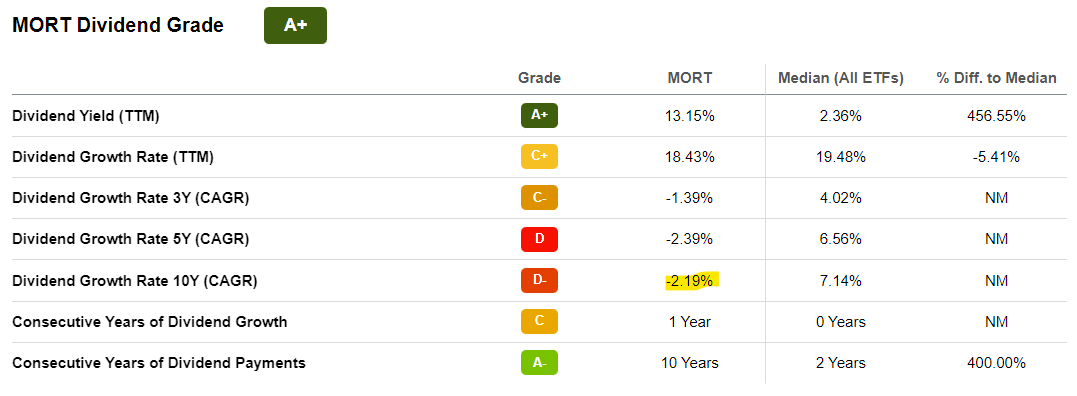

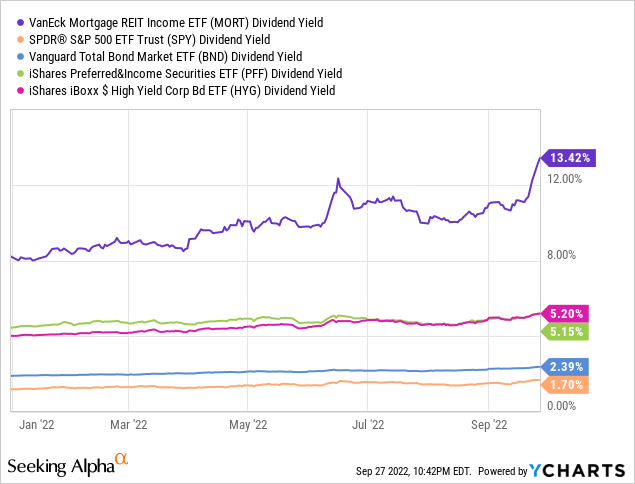

MORT itself yields 13.4%, an incredibly strong yield, and significantly higher than that of most broad-based asset class index funds.

MORT

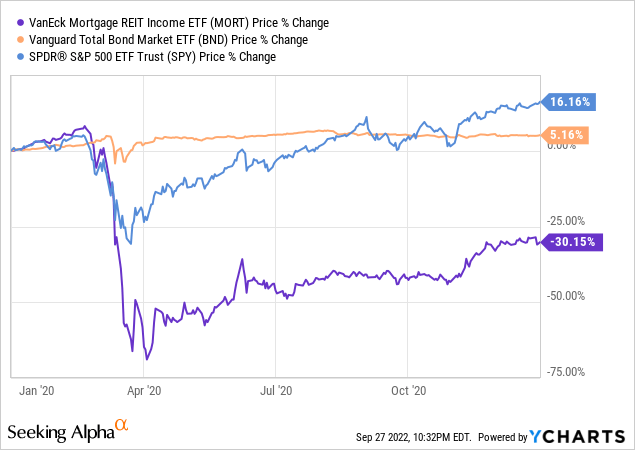

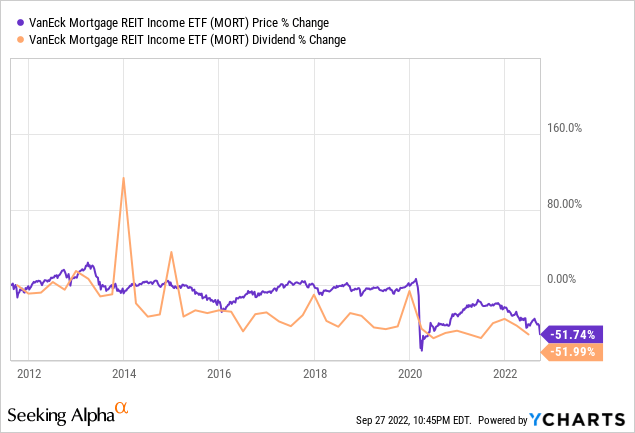

MORT’s strong, fully-covered 13.4% dividend yield is a significant benefit for the fund and its shareholders. Nevertheless, in my opinion, the fund’s strong dividends do not adequately compensate investors for the excessive leverage and risk of the fund’s underlying holdings. mREITs are simply too risky, too prone to capital losses, dividend cuts, and underperformance for the yields to be worth it, enticing as they may be. MORT itself has seen capital losses and dividend cuts of more than 50% since inception, close to a decade ago. Total returns have been positive, but not particularly high. These are broadly negative results, and particularly harmful for long-term investors.

As a final point, although mREITs are generally excessively risky investments, there are many, many exceptions. A carefully curated portfolio of higher-quality mREITs, bought when prices are low, would almost certainly outperform MORT, and would be a much more compelling investment opportunity.

Conclusion

MORT offers investors a strong, fully-covered 13.4% dividend yield. The fund’s underlying holdings are excessively leveraged, leading to significant risk, volatility, and losses during downturns. In my opinion, MORT’s risks outweigh its benefits. As such, I would not be investing in the fund at the present time.

Be the first to comment