samxmeg

Thesis

The Morgan Stanley China A Share Fund (NYSE:CAF) is a closed end fund focused on Chinese equities. As per its literature:

The Fund’s investment objective is to seek capital growth by investing, under normal circumstances, at least 80% of its assets in A-shares of Chinese companies listed on the Shanghai and Shenzhen Stock Exchanges

Source: Semi-Annual Report

What differentiates this fund from other Chinese equities CEFs and ETFs is the investment strategy, namely holding only A-shares:

China A-shares are the stock shares of mainland China-based companies that trade on the two Chinese stock exchanges, the Shanghai Stock Exchange and the Shenzhen Stock Exchange. Historically, China A-shares were only available for purchase by mainland citizens due to China’s restrictions on foreign investment.

Source: Investopedia

An investor can access Chinese equities risk either through U.S. listed ADRs such as the very famous tech behemoth (BABA), or through locally listed equities. Historically it has been much tougher to access the local market for foreigners, due to regulations:

The prices of A-shares are quoted in Renminbi (“RMB”), and only Chinese domestic investors and certain Qualified Foreign Institutional Investors (“QFII”) are allowed to trade A-shares outside of the Stock Connect programs. The Fund’s adviser, Morgan Stanley Investment Management Inc. (the “Adviser”), had obtained a QFII license pursuant to which it was authorized to invest in China A-shares and other permitted China securities on behalf of the Fund up to its specified investment quota of $200,000,000, as updated, modified or renewed from time to time (the “A-share Quota”). The Adviser had received an increase of $250,000,000 to its A-share Quota, of which approximately $138,000,000 was utilized through a rights offering in August 2010. On May 7, 2020, the People’s Bank of China and the State Administration of Foreign Exchange jointly issued the Regulations on Funds of Securities and Futures Investment by Foreign Institutional Investors (PBOC & SAFE Announcement [2020] No. 2), which came into effect on June 6, 2020. The new regulations unify and supersede the rules applicable to QFII and RQFII regimes. One of the key changes of the new regulations is the removal of quota restrictions on investment by QFII and RQFII. There is no guarantee that the new regulations will not be modified in the future.

Source: Semi-Annual Report

While it would seem that the market is much more democratic these days in terms of accessing onshore currencies, change can always happen unexpectedly in China, so buyers beware. However, we think the latest China / USA regulatory actions that finally saw the access of U.S. regulators to ADR’s data points to a more constructive future. China A-shares cannot be ‘de-listed’ because they are already trading on local exchanges only. The only item that comes to mind for A-shares is capital controls and ability to extract capital out of the jurisdiction. The CEF invests in RMB denominated securities, and the liquidation of such names and repatriation of capital involves foreign exchange controls, if ever instituted.

Ultimately CAF gives an investor a unique opportunity to take Chinese equities risk via locally listed shares, thus removing any ‘de-listing’ fears commonly associated with NYSE listed names.

The fund is particular through its composition as well, which is overweight Banks and Household Durables companies, versus technology companies. The likes of The China Fund (CHN) or Templeton Dragon Fund (TDF), which are CEFs investing in Chinese ADRs, are heavily invested in large multi-national Chinese tech firms. Not in CAF. From that angle the fund can also provide a diversification tool in terms of industry exposure.

Analytics

AUM: $0.32 bil

Discount to NAV: -16%

Z-Stat: -0.75

Yield: 0%

St Dev (5Y): 19

Sharpe Ratio (5Y): -0.23

Performance

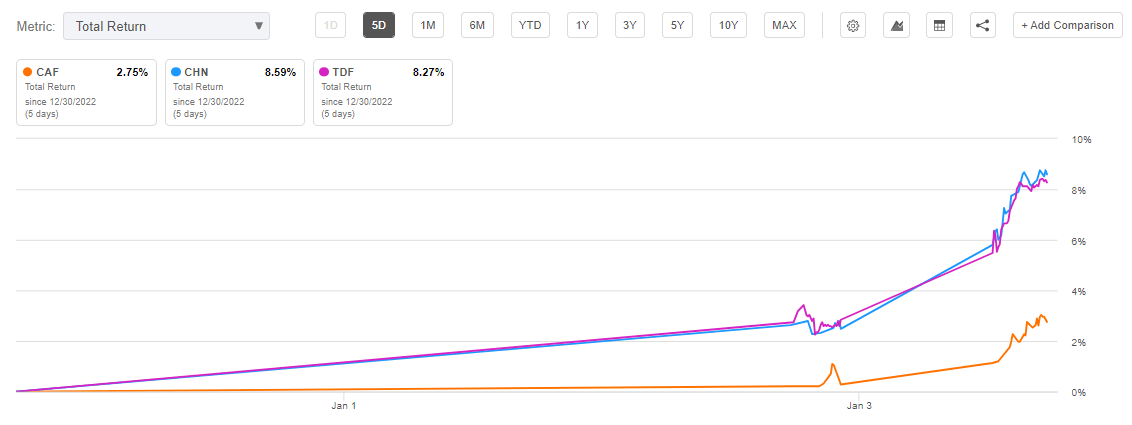

Chinese equities have been on-fire in the past week, on the back of re-opening moves:

Return (Seeking Alpha)

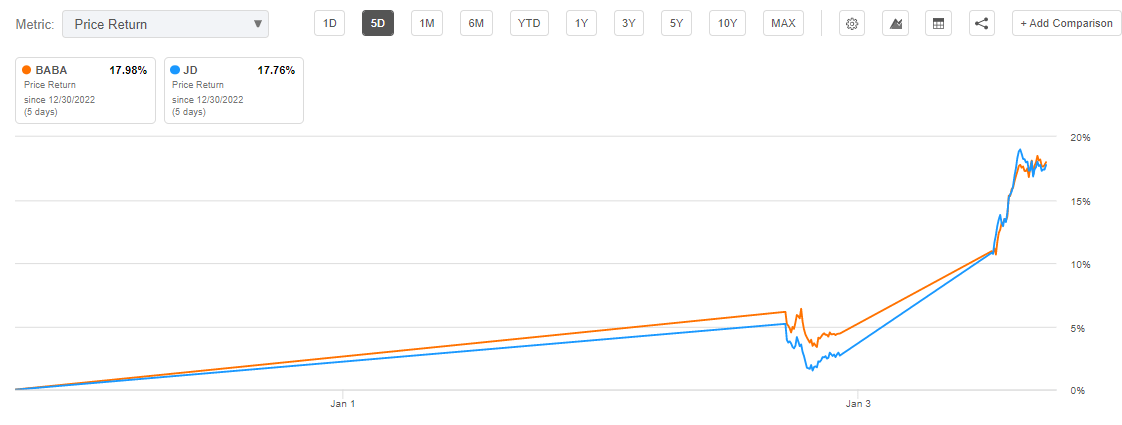

Tech has been the main beneficiary, with the likes of BABA and JD up more than 17%:

5-Day Return (Seeking Alpha)

We believe that as the re-opening progresses throughout the year all sectors will get a positive boost, with all the China funds set for more gains.

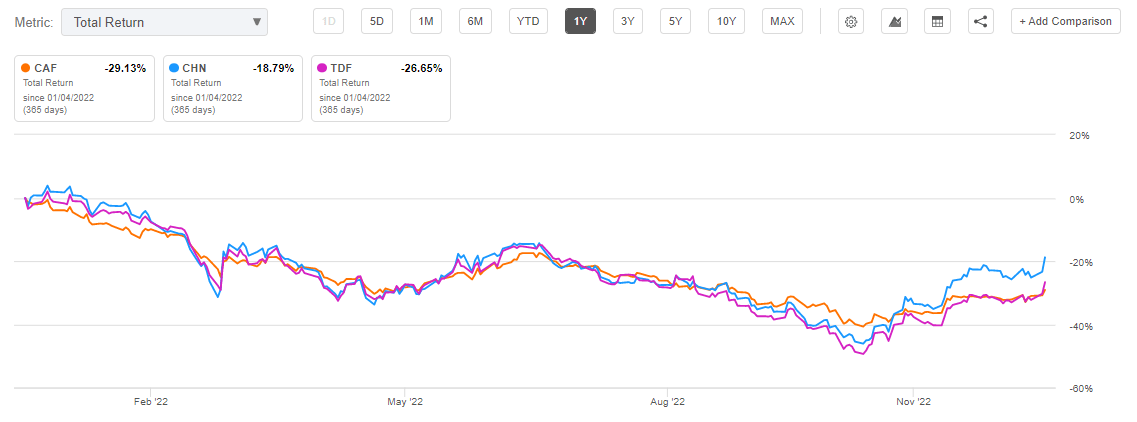

The past year has been tough for all funds involved in the space:

Total Return (Seeking Alpha)

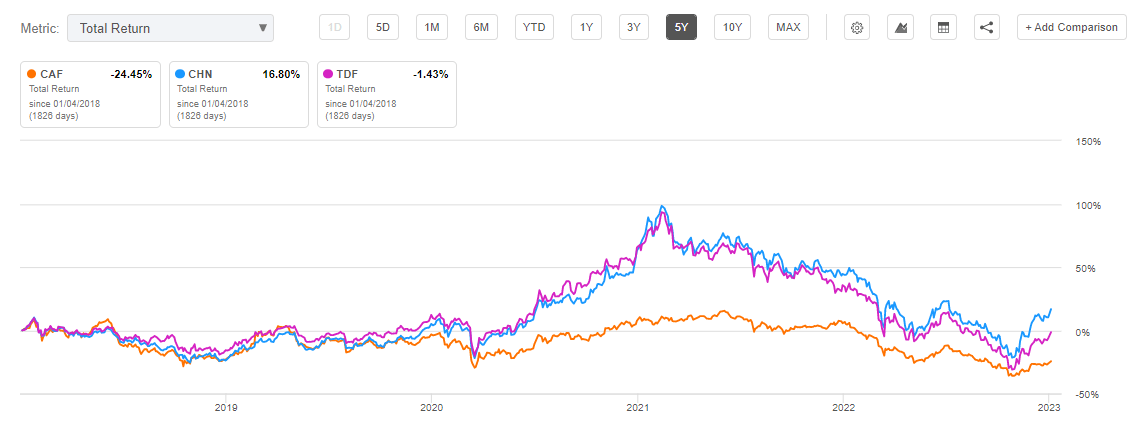

Long term though, CAF underperforms the ADR funds:

Total Return (Seeking Alpha)

Holdings

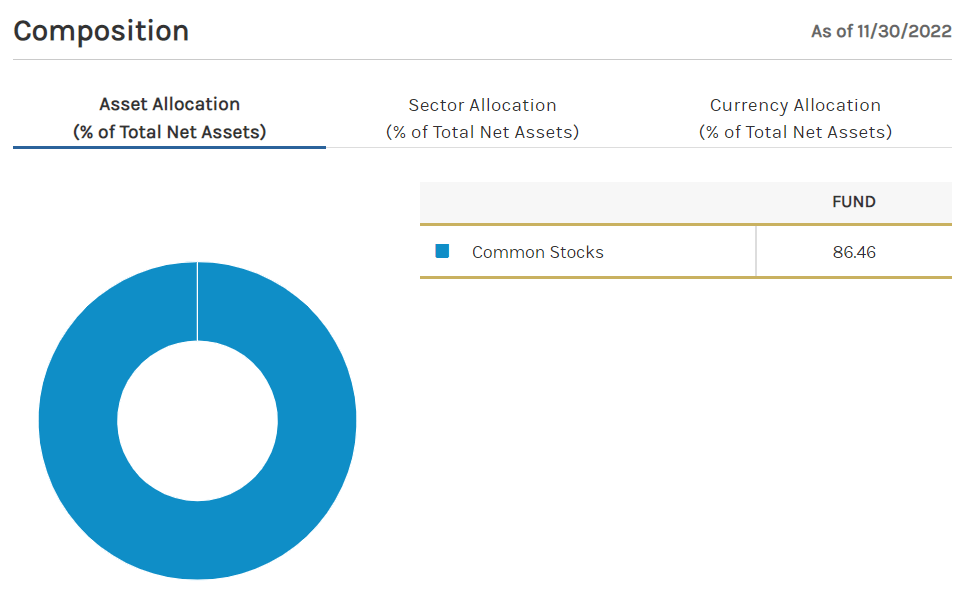

The fund is entirely composed of Chinese equities:

Composition (Fund Fact Sheet)

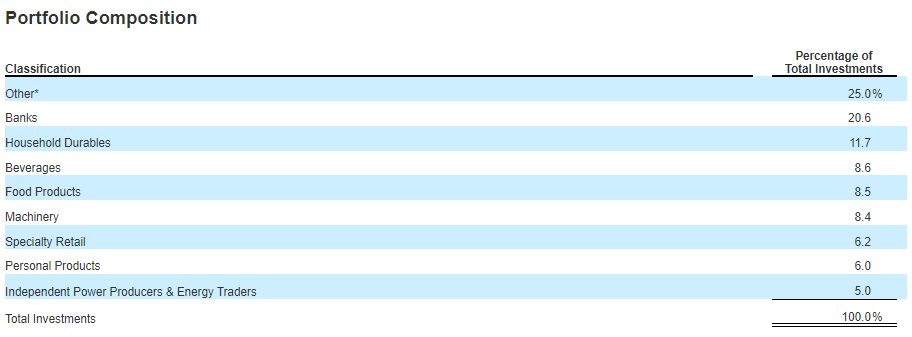

From a sectoral standpoint the CEF is overweight Banks and Household Durables:

Sectors (Semi-Annual Report)

Unlike the ADR funds, this one does not have a significant allocation to technology companies.

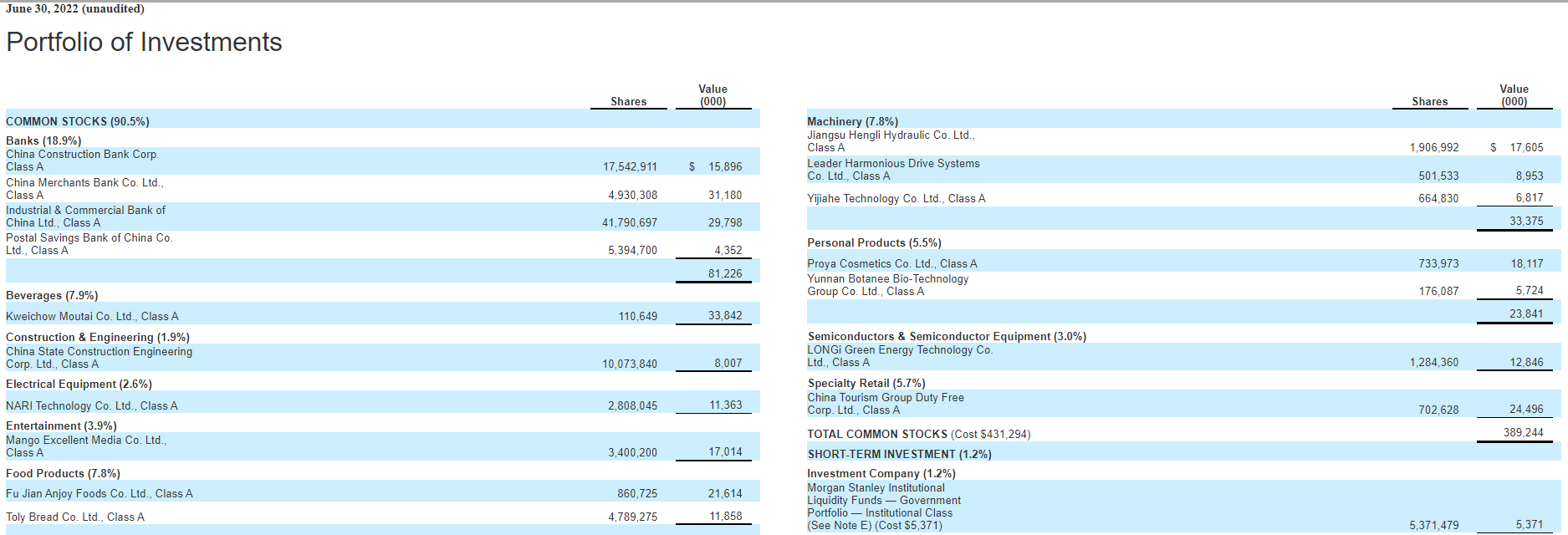

Some of the names in the portfolio are:

Names (Semi-Annual Report)

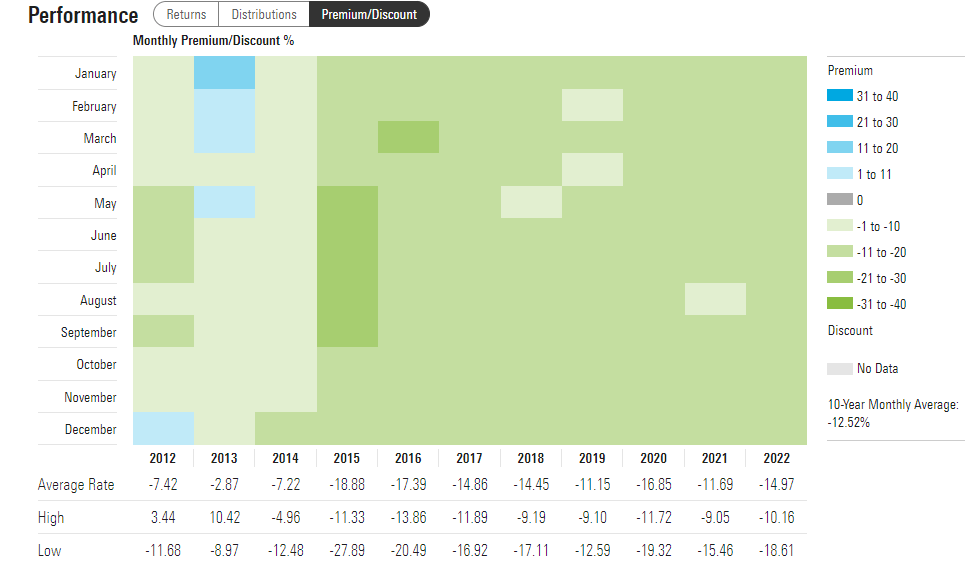

Premium / Discount to NAV

The fund has usually traded at a discount to net asset value:

Premium/Discount to NAV (Morningstar)

The fund has spent most of the last decade at a -14% discount to net asset value. We can observe that outside some distinct instances this range has been fairly tight as well.

Conclusion

CAF is a closed end fund focused on Chinese equities. The fund has capital growth as its objective and does not have a set dividend. In a year without any capital gains, nothing is disbursed to shareholders. From this angle it is more akin to an ETF. The vehicle provides investors with access to onshore Chinese equities, namely China A-shares. A-shares are equities that trade onshore on the Shanghai and Shenzhen Stock Exchanges. These securities do not have any delisting issues associated with them. On the flip side an investor here takes Usd/Rmb foreign exchange risk. Chinese equities have been on fire in the past week on the back of China re-opening after a Zero-Covid policy. CAF is not overweight technology stocks like its peers The China Fund or Templeton Dragon Fund. We expect technology to lead the Chinese equities recovery, but consider CAF a nice portfolio diversifier that eliminates any delisting fears that have manifested themselves in the U.S. listed ADRs.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment