Zolak

Modiv Inc. (MDV) is an internally managed net lease real estate investment trust (“REIT”) that just became publicly traded about a year ago from the time of this writing. On two occasions, I’ve written about MDV as an interesting microcap newcomer to the net lease REIT space, but also that the REIT has a big disadvantage in terms of its high cost of capital.

See:

- Modiv: An Intriguing, High-Yielding, Small Cap Net Lease REIT With A Disadvantage

- Modiv: Executing Well But Hampered By 3 Problems

In both articles, I explained why I am avoiding MDV’s common stock but simultaneously find its Series A Cumulative Preferred Stock (NYSE:MDV.PA) very attractive.

I purchased more shares of MDV.PA on Friday, January 13th for $20.66 apiece, a price that renders a dividend yield of 8.9% and upside to par of 21%. What’s more, the redemption date for these prefs isn’t until September 2026, leaving over 3.5 years before management can even consider redeeming them at the $25 par value.

In what follows, we’ll look at a brief overview of MDV followed by a discussion of the preferred dividend coverage.

Overview of Modiv

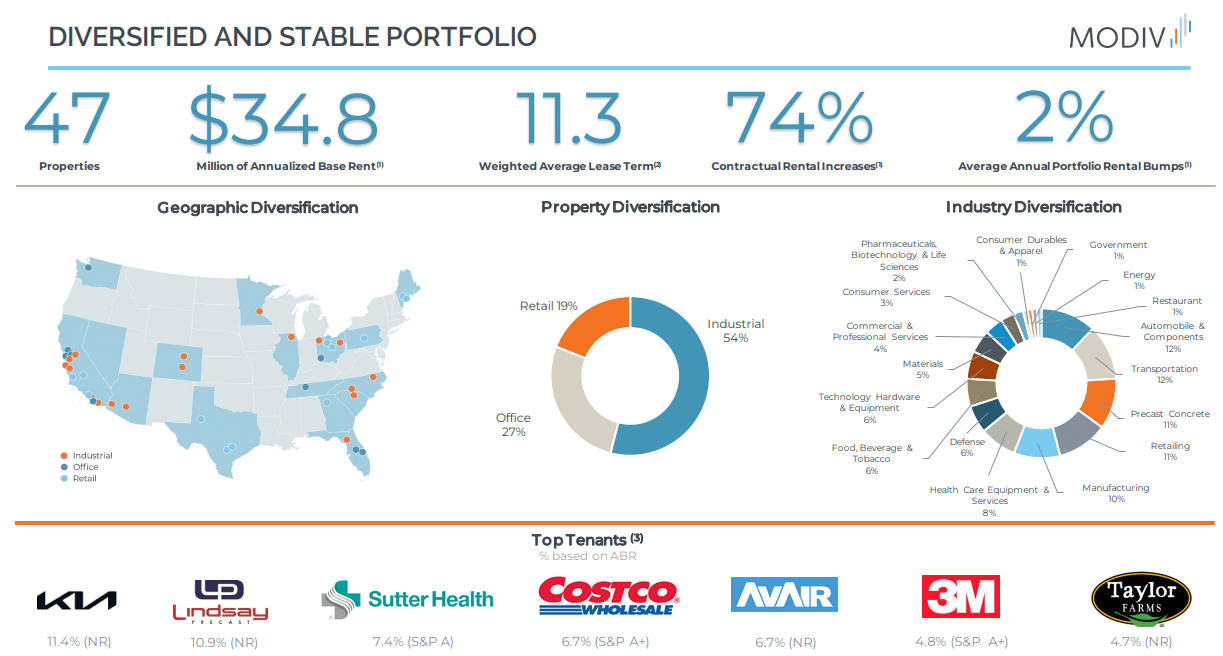

MDV is a net lease REIT primarily focused on industrial manufacturing properties but also has about 20% of its portfolio in retail properties (up from 9% at the end of 2021) and another ~25% in legacy office properties (down from 50% at the end of 2021) that are slowly being sold off.

MDV Q3 2022 Presentation

The downside of focusing so heavily on manufacturing properties is that they are big and chunky and typically located outside of population centers.

MDV Q3 2022 Presentation

Moreover, these properties are typically designed to suit the particular tenant-user’s needs. If a tenant vacated or went bankrupt, it would be extremely difficult to find a replacement tenant – at least not at anywhere near the rent rate being paid by the original tenant.

On the plus side, MDV asserts that they make sure each of their acquisitions are mission-critical properties for their tenant-users and that the likelihood of the tenant relocating elsewhere is low. These properties are usually acquired through sale-leasebacks directly with the tenant, which means MDV can insist on certain lease terms such as long durations and relatively high annual rent bumps.

Notice above that MDV’s portfolio has a weighted average remaining lease term over 11 years and average annual rent escalations of 2%. Those are both slightly higher than the average for net lease REITs.

Rather than being forced to issue high-cost equity and debt for future acquisitions, MDV can still use its ~25% of office properties as a source of capital for recycling into its preferred sector of industrial. In Q3 2022, MDV was able to sell office properties for a cap rate of 7.4% while reinvesting that into industrial assets at an initial cap rate of 7.6%.

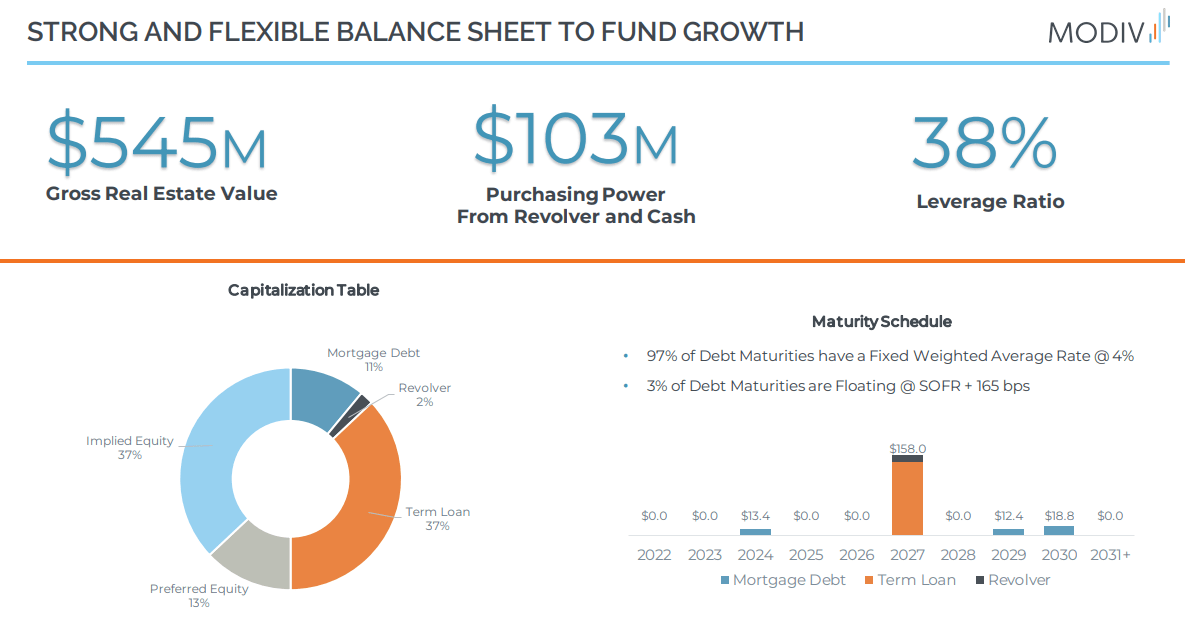

As for the balance sheet, it isn’t the strongest in REITdom nor among the subsector of net lease REITs, but it doesn’t portend any imminent doom either.

For one thing, note that MDV has no debt maturing in 2023 and only $13.4 million (6.7% of total debt) maturing in 2024. Thereafter, there are no maturities until 2027.

MDV Q3 2022 Presentation

Also, the leverage ratio of 38% certainly strikes me as conservative.

But, given the small portfolio size and the fact that general & administrative expenses (somewhat akin to the “management fee”) accounts for 18% of revenue, MDV’s net debt to EBITDA is rather high at 7.6x. For net lease REITs, I prefer to see this metric below 6x.

Actually, in Q3 2021, MDV’s net debt to EBITDA ratio was under 6x (5.6x to be exact), but the addition of a ~$149 million credit facility term loan for the purpose of acquisitions and refinancing pushed the net leverage ratio up.

Another thing I like to see about the balance sheet is that in spite of MDV’s small size and the fact that preferred stock is one of its few sources of capital, preferred equity makes up only 13% of total capitalization.

That’s a nice segue into a discussion of the preferred stock dividend.

Modiv’s Well-Covered Preferred Dividend

Let’s take a look at some numbers directly from MDV’s Q3 earnings report:

| Adj. EBITDA | Interest Expense | Pref. Stock Dividends | |

| Q3 2022 | $6.73 million | $2.51 million | $0.92 million |

| Q1-Q3 2022 | $19.80 million | $5.28 million | $2.77 million |

| Q1-Q3 2022 Annualized | $26.40 million | $7.04 million | $3.67 million |

In Q3, MDV.PA’s “preferred dividend payout ratio” equaled 21.8%, or a coverage ratio of 4.6x.

In the first nine months of 2022, the preferred payout ratio was 19.5%, or a coverage ratio of 5.1x.

In Q3 2022, adjusted EBITDA increased 10.8% YoY, but unfortunately, interest expense increased by 37.3%. As such, the preferred payout ratio rose a bit.

As of October 31st, 2022, MDV’s total debt load stood at $201.4 million and had a weighted average interest rate of 4.08%. At the end of Q3, though, most of that debt was in the form of borrowings on the company’s credit facility – $156.8 million was drawn on the $400 million revolver.

Back in October, though, MDV purchased a five-year swap agreement that fixed its interest rate on the credit facility, resulting in 97% of total debt becoming effectively fixed.

However, the interest rate on the credit facility will still vary depending on the leverage ratio. Namely, if the leverage ratio rises above 40%, the rate will reset higher. Currently, MDV’s leverage ratio sits at 38%. As such, if the company takes on virtually any more debt, its interest expenses could rise.

Management is well aware of this, though, and I see no reason why they would intentionally increase debt above the 40% threshold, unless they wanted to acquire a property at an accretive spread above MDV’s cost of capital inclusive of the additional interest costs.

Bottom Line

The primary risk with MDV as well as MDV.PA is the REIT’s small size. Failure of any single investment could spell disaster because each one accounts for a sizable portion of revenue and cash flow.

That said, I do believe MDV’s tenant base to be fairly strong and moderately recession-resistant. Industrial tenants won’t want to give up their build-to-suit manufacturing facilities because of a temporary downturn in the economy.

As such, I believe MDV.PA’s nearly 9% yield to be safe. And the upside to par of over 20% is attractive as well. If MDV.PA was redeemed on its September 2026 redemption date, buying today would result in annual total returns of 15%.

Be the first to comment