Editor’s note: Seeking Alpha is proud to welcome Harvy James Espellarga as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Sundry Photography

Investment Thesis

MKS Instruments (NASDAQ:MKSI) is cheap and undervalued because the company: 1) continued to increase its revenue despite macro headwinds, 2) continues to make smaller, denser, and cheaper semiconductors and PCBs, and 3) can improve the company’s revenue mix with the Atotech acquisition through improving the Advanced Electronics market.

Business Overview

MKSI sells computing solutions. They provide solutions that can measure, monitor, analyze, and control processes to optimize process performance and productivity for its customers.

Their Three Main Markets

MKSI operates in three different markets, with the Semiconductor leading in revenue and demand.

Semiconductor: They produce silicon wafer chips that customers can use for lithography, metrology, packaging, and inspection. They help build electronic circuits because of their conductivity.

Advanced: Advanced electronics manufacturing includes flexible and rigid printed circuit boards (“PCBs”).

PCBs are essential for connecting different parts, letting them communicate with each other, and protecting these components from damage and interference.

Specialty Industry: Products for industrial, life, and health sciences, research, and defense use are sold on this market.

Three Reasons Why MKSI Is Undervalued

First, macro headwinds and supply constraints didn’t disrupt MKSI’s revenue in the semiconductor market because of management’s ability to manage costs and improve factory efficiency.

Second is their pursuit of miniaturization, or making Semiconductors and Printed Circuit Boards PCBs, smaller and denser. A smaller semiconductor has lower latencies and shorter signal paths which means better efficiency.

Third, the Atotech acquisition just got approved. Atotech can improve MKSI’s Advanced Electronics market by creating better PCBs and laser-based processing.

Revenue Growth Despite Macro Headwinds and Supply Constraints

Strong demands in the Semiconductor market are the main factor that increased MKSI’s revenue growth in the second quarter. Because of solid demands, the Semiconductor market counterbalanced the revenue decline in the Advanced Electronics market.

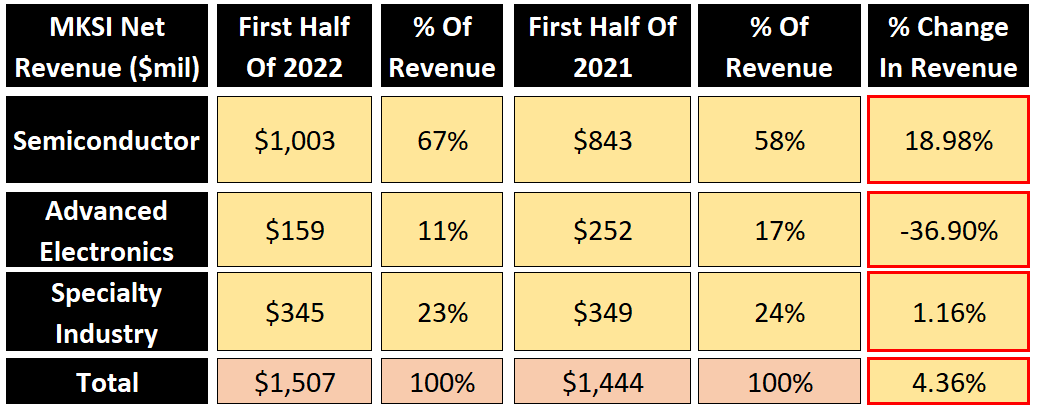

Image Created by Harvy James Espellarga with data from MKSI H1’22 & H1’21 Results

For the first half of 2022, MKSI’s Semiconductor market gained over 19% in revenue due to solid demands, a 1.2% revenue increase in the Specialty Industry driven by a steady demand across Industrial, Life and Health Sciences, and Research and Defense applications, and a 37% decline in Advanced Electronics because their customers have temporarily slowed capacity expansions due in part to softness in smartphone demand.

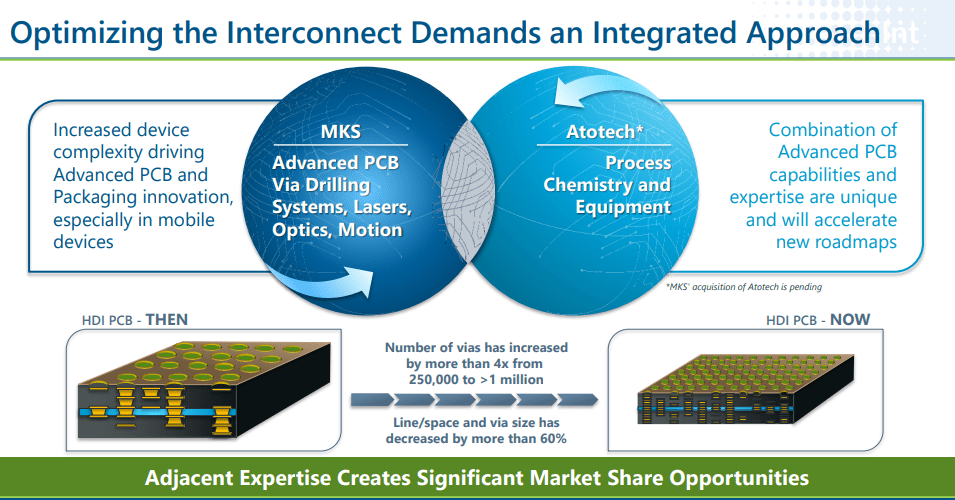

Making Semiconductors and PCBs Smaller & Cheaper

MKS Instruments Investor Presentation

A smaller and denser High-Density Interconnector Printed Circuit Board, or an HDI PCB, performs better because it has shorter signal paths, which means less latency and better performance. Earlier versions of PCBs, have many lines/spaces, making them inefficient and costly. Atotech’s technology will make MKSI’s PCB efficient and will increase the revenue mix of the Advanced Electronics market.

The same trends that drive our semiconductor business, miniaturization and complexity are key drivers for advanced electronics, as customers demand more processing power, more features and new form factors for their devices.

It’s excellent that MKSI’s CEO, John Lee, confirms that the company is putting its focus on improving its Semiconductor and Advanced Electronics performance.

John Lee has this to say regarding PCB demand for the Advanced Electronics Market:

Industry demand for flexible PCB via drilling has continued to soften, as customers have temporarily slowed capacity expansions due in part to softness in smartphone demand.

– MKS Instruments Q2’22 Earnings Call

Management thinks that the Advanced Electronics market will be similar to the second quarter’s performance because customers have temporarily slowed capacity expansions due in part to softness in smartphone demand.

Making semiconductors smaller can reduce the cost of producing semiconductors and PCBs while improving the product’s overall performance because of shorter signal paths, which means lower latency and better efficiency.

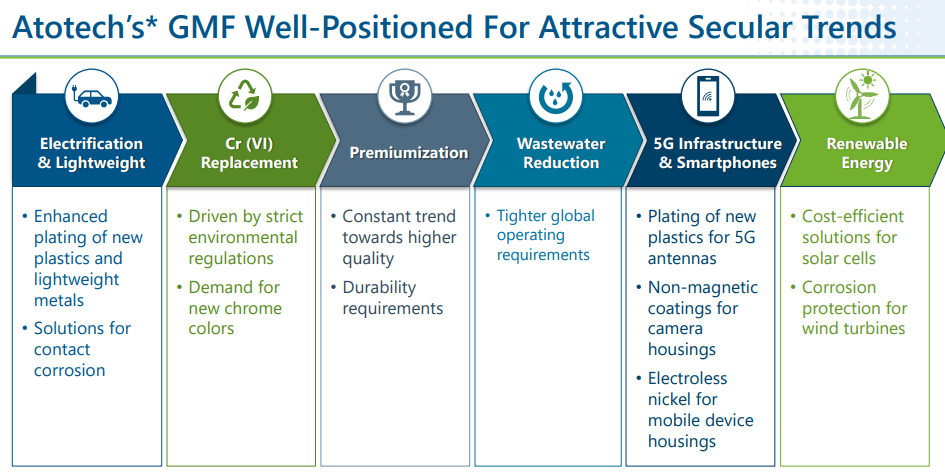

Improving Revenue Mix Through Atotech Acquisition

MKS Instruments Investor Presentation

With Atotech, the company can improve overall quality, cost-efficient solutions, durability, and plastics for new 5G antennas. Atotech has a lot to offer for MKSI’s current operations, mainly in:

Enhanced Plating & Solutions For Contact Corrosion: Enhanced plating of new plastics and lightweight metals can reduce the cost of production and corrosion in semiconductors.

Premiumization: They can improve their products’ quality by enhancing the durability of their semiconductors and PCBs.

5G Infrastructure & Smartphones: Atotech offers a better 5G Infrastructure and better smartphone PCBs. 5G will be prevalent in the future, and having Atotech make 5G capable devices semiconductors can help expand the business.

Renewable Energy: Atotech can create cost-efficient solutions for solar cells and corrosion protection for wind turbines. Atotech can bring revenue diversity to MKSI because they can get more opportunities for the Advanced Electronics market since they can help improve the advanced capabilities of their PCB products, giving MKSI more revenue and profitability with its 48% gross margin.

Financial Analysis

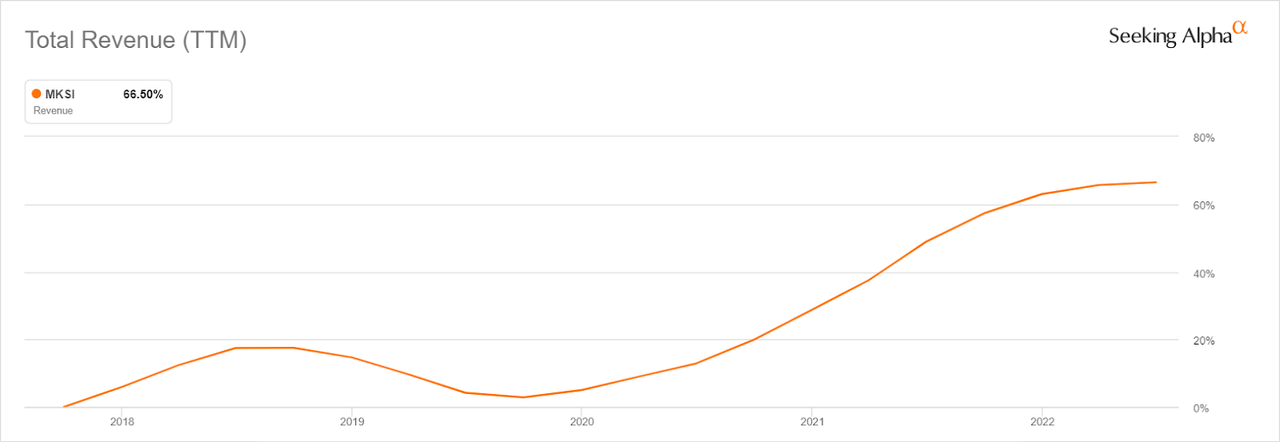

Seeking Alpha – MKSI Total Revenue (TTM)

MKSI’s revenue is steadily growing. Although revenue dropped in 2019 by 8% compared to the previous year, it came back in 2020 and 2021, featuring a 23% and 27% growth, respectively.

MKSI also has a trailing twelve-month $1.1 billion in cash & cash equivalents and steady cash growth. Their balance sheet looks attractive, and for a company with a market cap of $6.7 billion, management can invest this money in growth opportunities.

Image Created by Harvy James Espellarga with data from MKSI Q2’22 Results

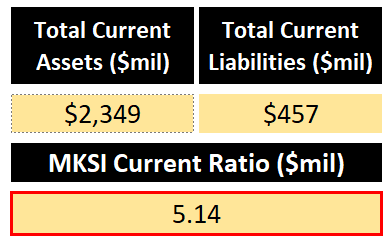

Everything looks attractive on the short-term side of things in MKSI’s balance sheet. The company has a trailing twelve-month total current assets of $2.3 billion and total current liabilities of $457 million. I divided MKSI’s total current assets by their total current liabilities, this gives us a 5.14 current ratio, no foreseeable liquidity problems here.

Image Created by Harvy James Espellarga with data from MKSI Q2’22 Results

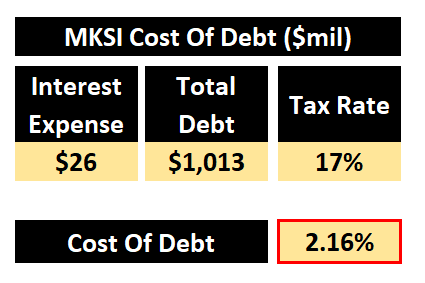

To determine a company’s debt cost, we divide the interest expense by the company’s total debt. In MKSI’s case, they have a $25 million trailing twelve-month interest expense of $26.4 million and total debt of $1.1 billion.

I use this to determine if the company pays a lot of its revenue in debt. In MKSI’s case, they have a low single-digit 2.2% cost of debt. I like MKSI because their company has a relatively low cost of debt. Low debt levels are always good for the company because instead of paying more debt, the money can be used to reinvest in the company.

I think MKSI’s balance sheet is strong, proven by a current ratio of 5 and a relatively low cost of debt of 2.2%. Not only do they have a strong balance sheet, but with the current macro headwinds, I think the company’s doing great, and this is why I rate it as a Buy:

Valuation

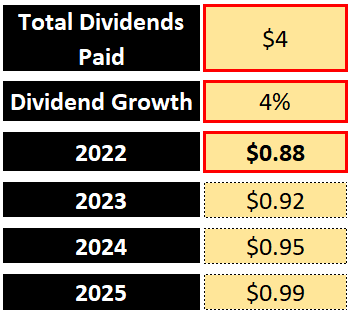

Image Created by Harvy James Espellarga with data from MKSI Dividend History

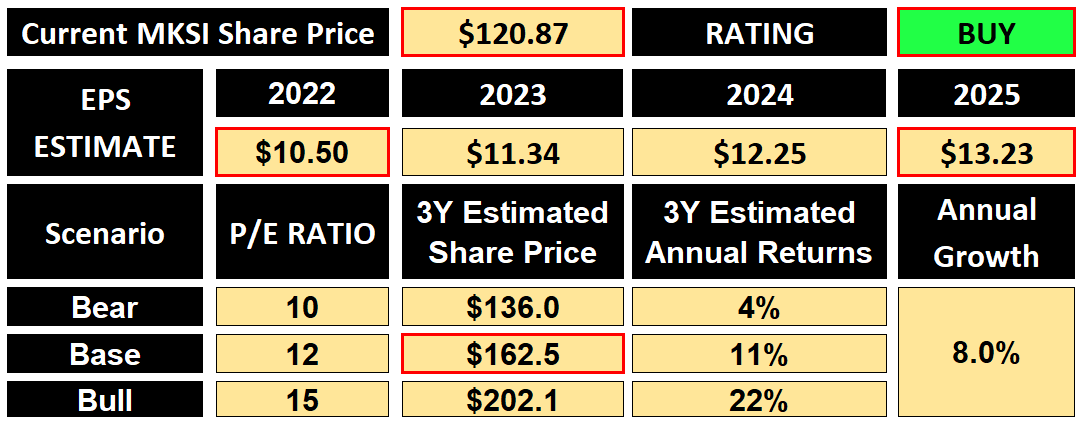

To have a better EPS estimate, I decided to factor in the estimated dividends that MKSI pays out in the future. That way, we have a better view of the price range for our three-year estimated share price.

In line with the current dividend valuation, I estimated the company’s 4% three-year dividend growth forecasting MKSI to pay out $4 in dividends from 2022 to 2025. The company consistently pays out dividends, but dividend increase depends on management.

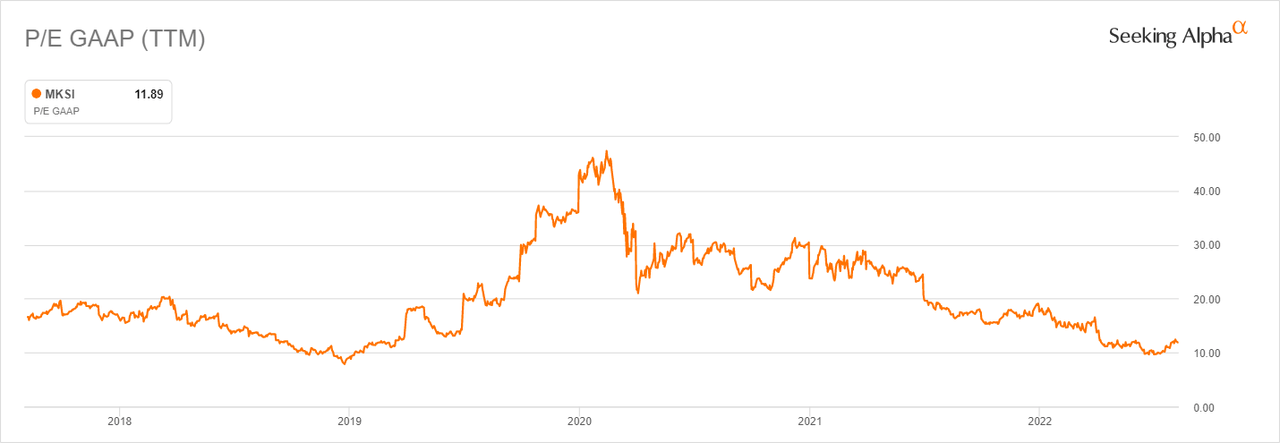

Seeking Alpha – MKSI P/E GAAP (TTM)

MKSI also has a P/E ratio average of 22 ratio in the company’s past performance. However, we can’t base the company’s future growth solely on past performance. Since the company’s currently trading at a 12 P/E ratio, I used it as a base case for the valuation, 10 for the bear case, and 15 for the bull case.

Image Created by Harvy James Espellarga with data from MKSI Q2’22 Results

I am predicting the estimated share price by calculating the company’s EPS, multiplying it by a growth rate %, then multiplying the EPS by an estimated P/E ratio, and adding the total dividends paid in a three-year forecast.

Going forward with the valuation side of things, I estimated $10.50 on MSKI’s 2022 EPS estimate, a little bit conservative to the consensus EPS estimate of $10.66.

With a $13 EPS in 2025 multiplied by an annual 8% growth calculated through past performance, I’d assume if the company continues to have strong demands, they’d still have an 8% annual growth, then multiplying the $13 EPS to a 12 Base P/E ratio; we get a $158 share price. I added $4 from the total dividends MKSI paid to get a three-year Base estimated share price of $163.

Risks

Supplier Power

There are higher demands for semiconductors and lesser supply, which causes supply chain issues. The primary bottleneck of supply is wafer production capacity. Taiwan and China are the ones capable of producing a high number of these chips and semiconductors.

In 2021 alone, Taiwan’s semiconductor output value reached $146 billion, representing a 27% year-over-year increase. With increasing demands and fewer supplies, MKSI is at risk of a chip shortage.

Buyer Power

Since MKSI has three markets, Semiconductor, Advanced Electronics, and Specialty Industrial, the buyer power in these markets vary. Any weakness in buying power amongst the three markets will result in revenue losses.

In MKSI’s H1’22 results, Advanced Electronics suffered a decline in demand in the flexible PCB market, which means that they also had a decrease in revenue.

Taiwan and China’s Situation

Amongst all the risks, I think that Taiwan and China’s situation can be the most damaging for MKSI’s markets. The business mainly gets its revenue from the Semiconductor market, which accounts for about 60% of its revenue.

Why do I find this issue devastating for MKSI? Taiwan accounts for most of the semiconductors in the world, and the tension can potentially affect the Atotech acquisition, depending on how grave the situation is.

Investor Takeaway

Atotech’s acquisition will improve the performance of MKSI’s product line, specifically in the Advanced Electronics market. The merger has been approved, and once the deal closes, this may be a bullish catalyst for MKSI.

MKSI has performed well in its second-quarter results, setting a record by gaining $765 million in revenue. Even though two out of three markets declined in revenue for the first half of the year compared to 2021’s results, the strength in the Semiconductor market offset that decline.

I believe that if the company constantly increases its revenue growth, makes semiconductors and PCBs smaller, cheaper, and much more compact, and closes the Atotech acquisition, it will have better results in the foreseeable future.

I rate MKSI as a Buy because right now, it is cheap, and I believe the business has excellent potential. With a forecasted EPS of $13 by 2025, estimated annual growth of 8%, and a three-year 11% annual return estimate, I estimate the base share price to be $163.

It might be experiencing headwinds now, but the company is set for long-term performance. Almost everything in this world has a semiconductor. That’s why semiconductor demands will constantly increase. Atotech’s acquisition can hopefully improve the company’s Advanced Electronics. I hope to see more of the business in the intermediate future.

Thank you for reading. I appreciate your time.

Be the first to comment