Robert Way

MUFG logo (MUFG)

Investment thesis

In our previous article on Mitsubishi UFJ Financial Group (NYSE:MUFG), we shared our lackluster interest in the bank as its ROE is lower than other financial institutions we compared it to.

With Japan’s largest bank’s recent announcement of their financial results for the 9 months up to 31st December 2022, it is an excellent time to check how the bank is doing.

Latest 9 Months’ Financial Results

Let us start where we left off in our last article. The issue we had was MUFG’s rather low ROE.

That has actually gotten even worse than before. It has gone from 9.9% at the end of December 2021 to just 2.9% at the end of December 2022.

In its defense, one reason given by MUFG was the impact of differences between Japanese GAAP and U.S. GAAP and the effect of transfers across entities with different consolidation periods.

This amounted to about ¥20 billion, or $152 million.

We doubt that such a small amount can be given as an excuse for such a large deterioration.

When we look at their profit and loss, we do see that gross profits and especially net interest income were up considerably, in line with what other banks are reporting these days.

MUFG – 9 months P&L up to 31 Dec 2022 (MUFG Financial Results up to 31 Dec 2022)

We need to consider the reversal of the MUB transfer which comes as an extraordinary gain once the transfer is completed.

As such the net profit to owners of the company was up just 7% from ¥1,070 billion to ¥1,145 billion.

Their expenses as a ratio to revenue are quite high when we have compared it with other large banks in the past, and it is now even higher at 68.3%.

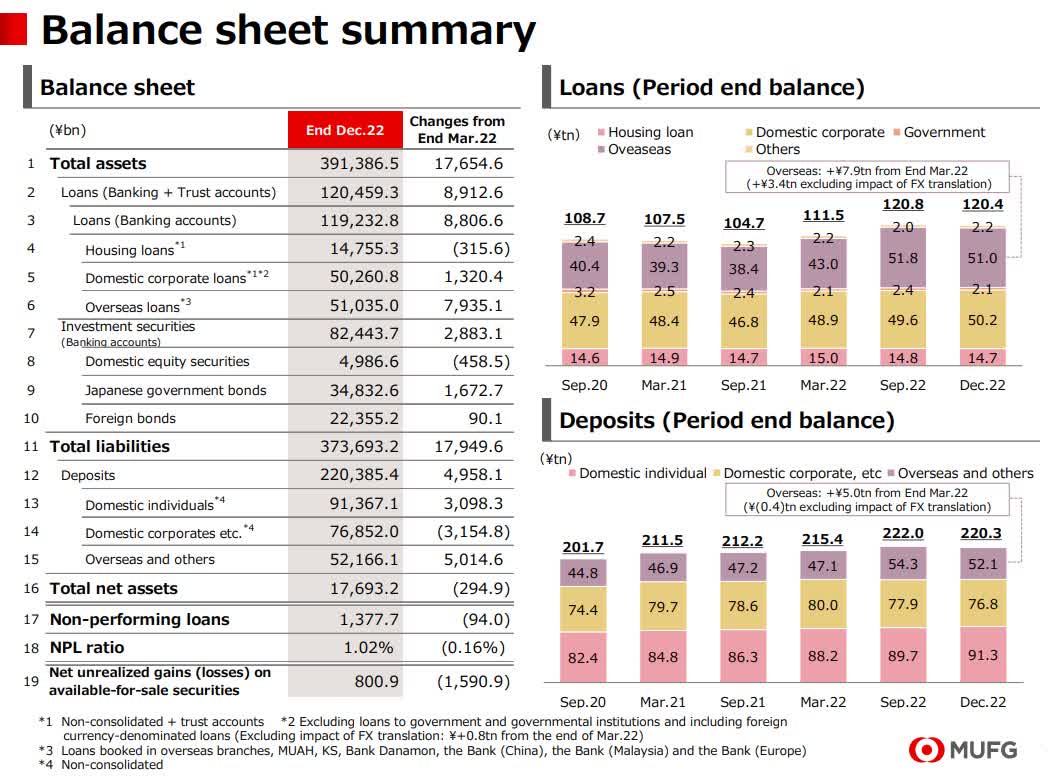

We then look at their balance sheet.

MUFG – Balance sheet 31 Dec. 2022 (MUFG – financial results 31st Dec. 2022)

Their loans to deposit ratio are 0.55.

Fitch rating agency recently affirmed MUFG’s rating as “A-“ with a stable outlook. In terms of the bank’s CET-1 ratio, it believes it will remain in the 9.5-10% range. Any capital above this range will likely prompt the bank to consider new investments and/or additional dividends and share buybacks.

MUFG CET-1 ratio is still much lower than banks like HSBC (HSBC) with 13.6% and Citigroup (C) with 13%.

Returning capital to shareholders and final thoughts

MUFG is estimating that its dividend for FY ending 31st of March 2023 will be ¥16 per share. This brings their total for the year to ¥32 per share which is ¥4 more than the year before.

That is a dividend growth of 14%.

The yield works out to 3.4% which coincidentally is very similar to that of HSBC and Citigroup.

They have also done some share buybacks over the last 9 months. The number of shares outstanding was reduced by 958 million shares. Treasure shares increased by 87 million shares.

MUFG has communicated that its target for profit for this FY ending 31st of March 2023 will come in at around ¥ 1 trillion.

We missed the recent jump in share price in our previous call, as it has gone up 32% in such a short time.

MUFG share price up 32%, SA

This does not change our view, as for us to get interested we would like to see fundamentals improve – and not just the share price.

As such, it is still a Hold stance from us.

Be the first to comment