David Commins/iStock via Getty Images

Millicom (NASDAQ:TIGO) is introducing new products like Tigo money, and investment analysts expect stable free cash flow. If TIGO grows its mobile data services as promised, revenue growth will likely increase. In my view, as soon as TIGO lowers its leverage, and management launches a new buyback program, the stock price may increase. Even considering risks from regulators, my DCF model implied a valuation that is significantly higher than the current price mark.

Millicom And Tigo Money

TIGO offers cable and mobile services in emerging markets. Options include high-speed data, cable TV, direct-to-home satellite TV, and mobile voice among others.

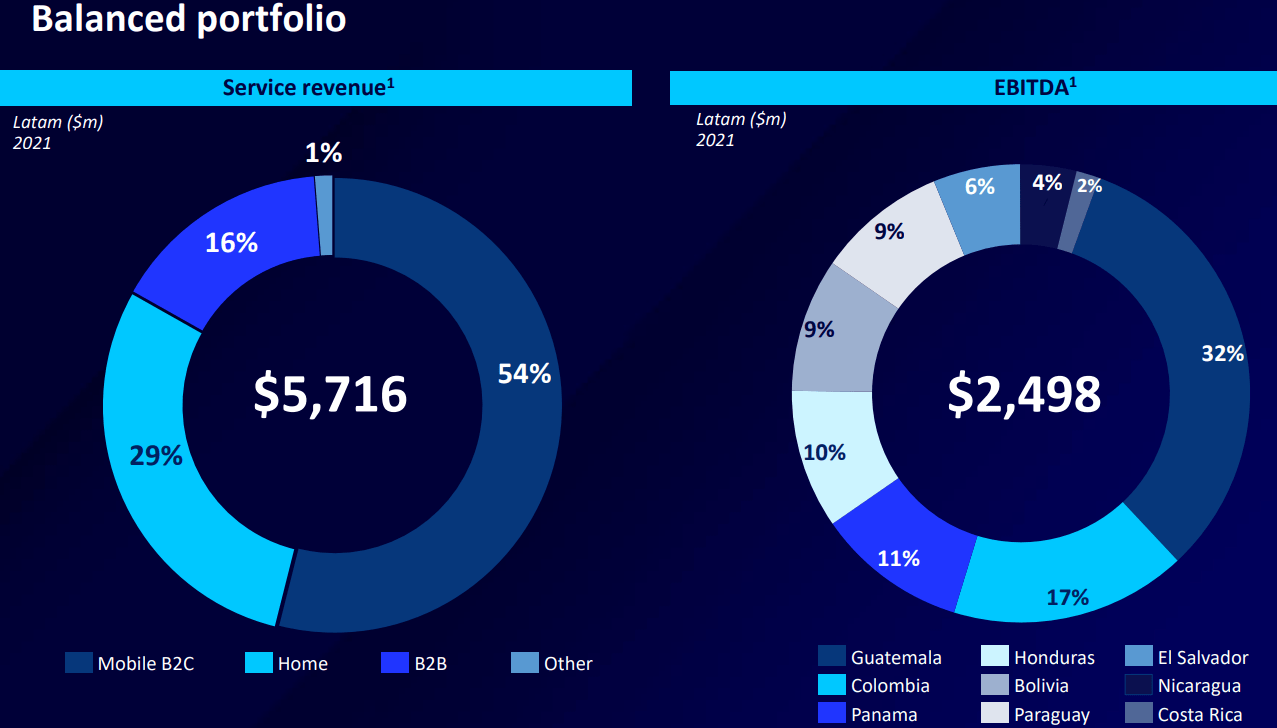

The company’s most relevant revenue comes from mobile services to consumers, however home services and B2B also represent a large part of net sales. In terms of geographic diversification, I believe that investors will like TIGO. The company provides services in many countries in Latin America.

Investor Day

With that about the company’s diversified model, there is one initiative that interested me quite a bit. Tigo Money, which intends to offer merchant platforms, lending platforms, and cards, is reporting 17% more customers. In my view, if Millicom successfully offers these new services to many of its current clients, revenue growth will likely trend higher.

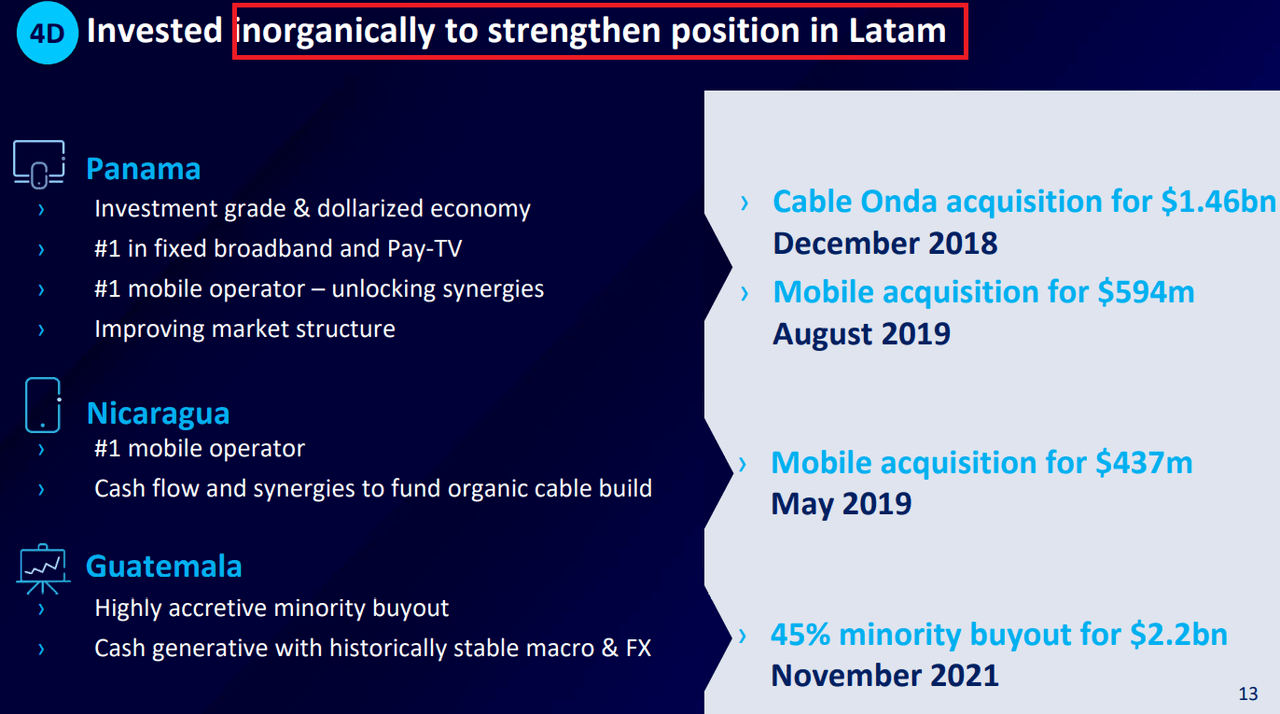

TIGO has proven that it is ready to acquire businesses to enter new markets. It is very beneficial because sales growth could be even larger. I wouldn’t expect many new acquisitions in 2022 because the net debt/EBITDA levels are quite elevated right now. TIGO reported leverage of more than 3x. With that, once the company grows, and leverage decreases, we will likely see more acquisitions.

Investor Day

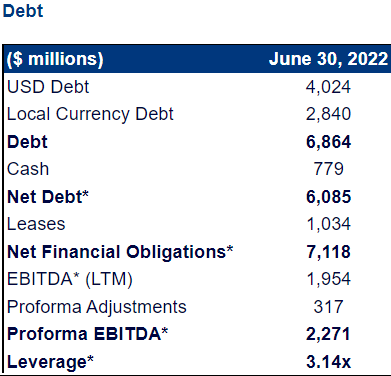

Balance Sheet

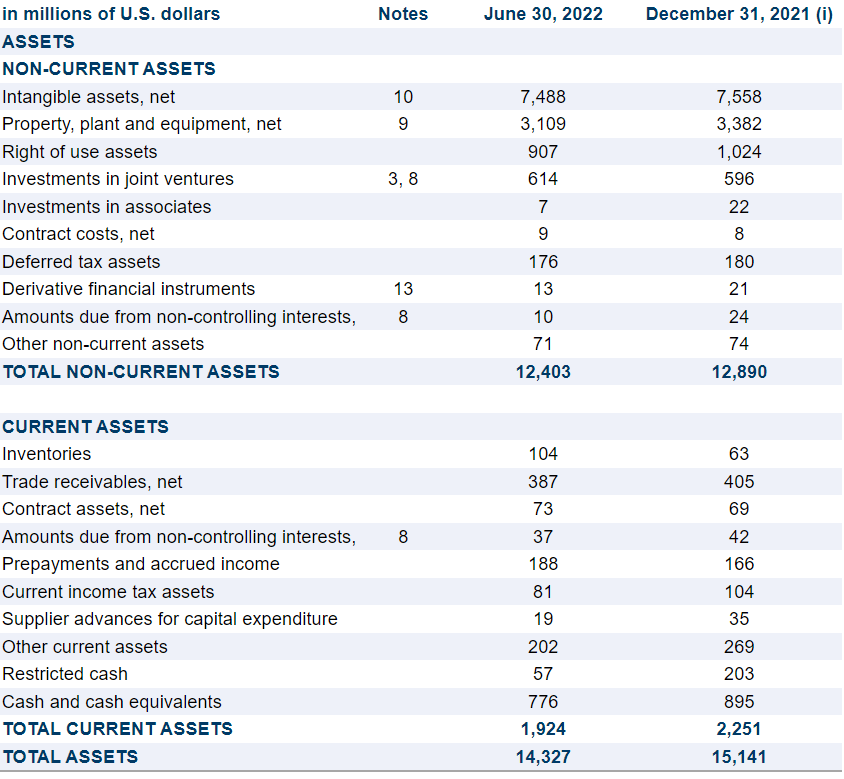

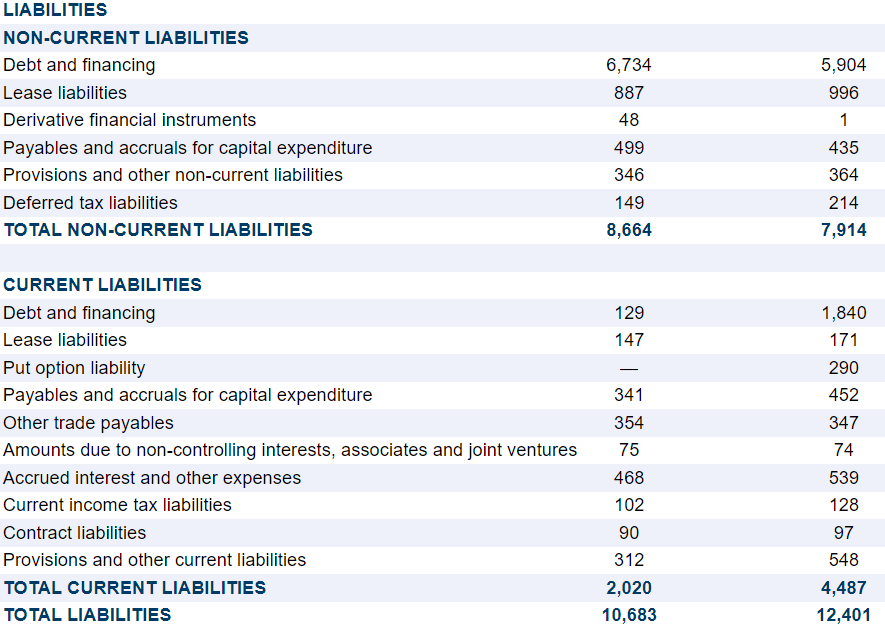

With an asset/liability ratio close to 1x and $776 million in cash, I believe that the company’s financial situation appears quite stable.

10-Q

The total amount of debt does not seem small. As of June 30, 2022, net debt was equal to $6.08 billion. If we assume 2023 EBITDA of $2.3 billion, the net debt/EBITDA stands at close to 2.5x-3.5x. The company promised to lower its leverage over time, so I wouldn’t be worried about the current amount of debt.

10-Q 10-Q

Analysts Expect Sales Growth, And I Obtained A Fair Price Of $41 Per Share

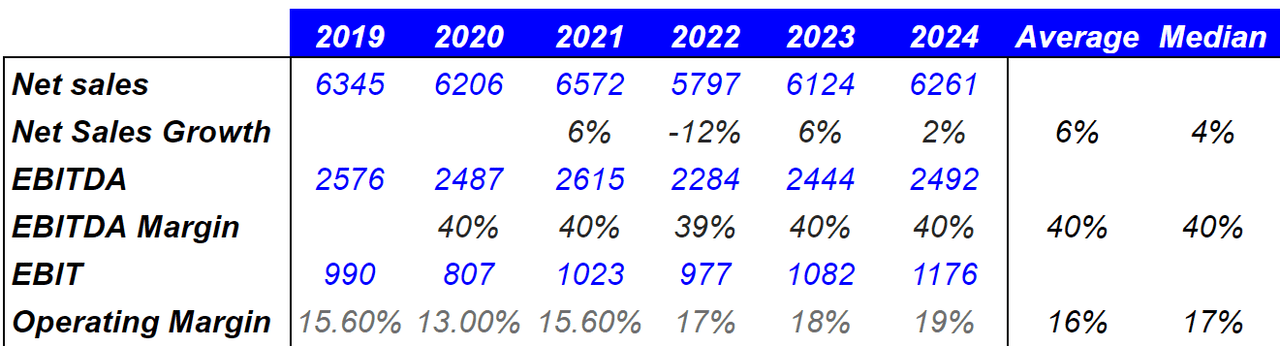

Investment analysts believe that TIGO may report a decline in sales growth of -12% in 2022, a median sales growth close to 4% from 2021 to 2024. Analysts also believe that an EBITDA margin of 40% and operating margin close to 19% could happen in 2024.

Work Of Other Investment Analysts

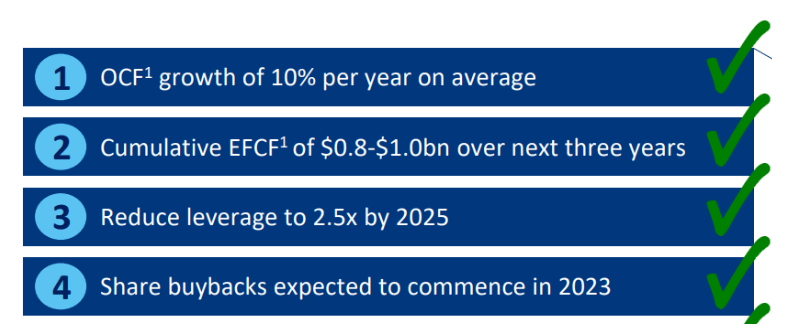

Besides, among the initiatives explained on the investors day, there was a few remarkable pieces of information. First, TIGO expects to collect free cash flow close to $0.8-$1 billion, reduce leverage, and start share buybacks from 2023. With all this in mind, I believe that investors may want to know more about the valuation of TIGO.

Investor Day

With Further Data Networks And More Mobile Data Expansion, I Believe That TIGO Could Sell At $41 Per Share

In my view, if TIGO successfully grows its mobile data services, and clients grow, revenue will likely trend north. Besides, further projects with business clients are likely. These initiatives were depicted in the last annual report:

Our strategic priorities include, among others, expansion of our high-speed data networks (4G, HFC and FTTH), facilitation of growth in our mobile data and cable segments, implementation of technology transformation projects to improve our operating performance and efficiency. Source: 20-F

Besides, the company also intends to separate Tigo Money, which may provide more visibility to this new business segment. If the company can present independent figures of TIGO money from its telecommunications service operations, Millicom may obtain further financing.

The creation of legal entities to separate our Tigo Money and Towers businesses from our telecommunications service operations. Source: 20-F

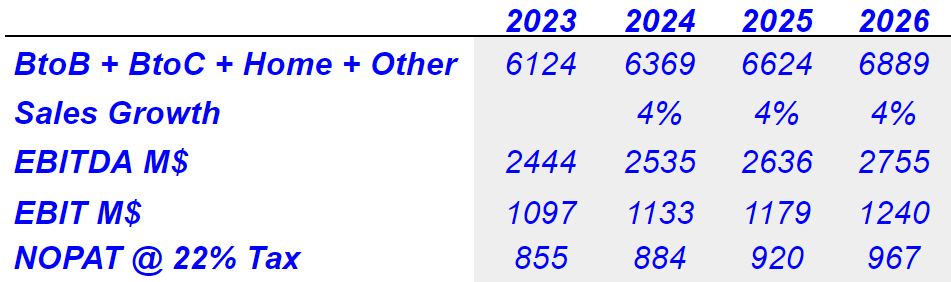

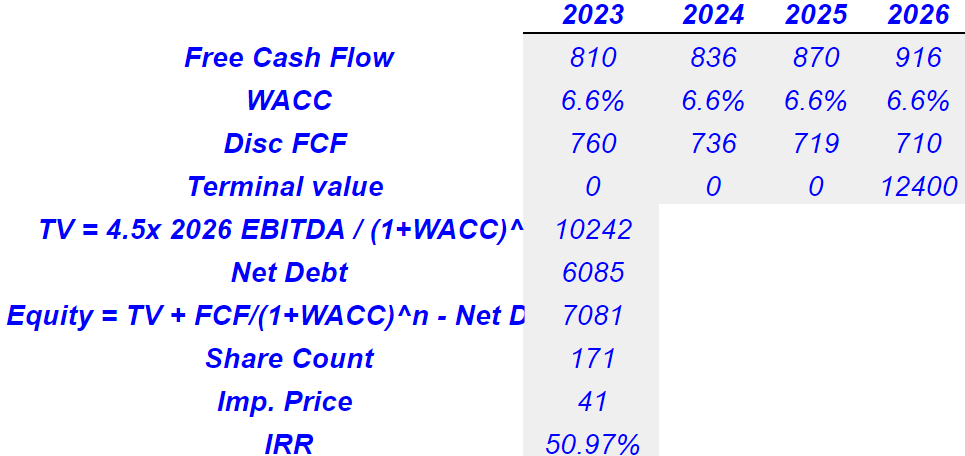

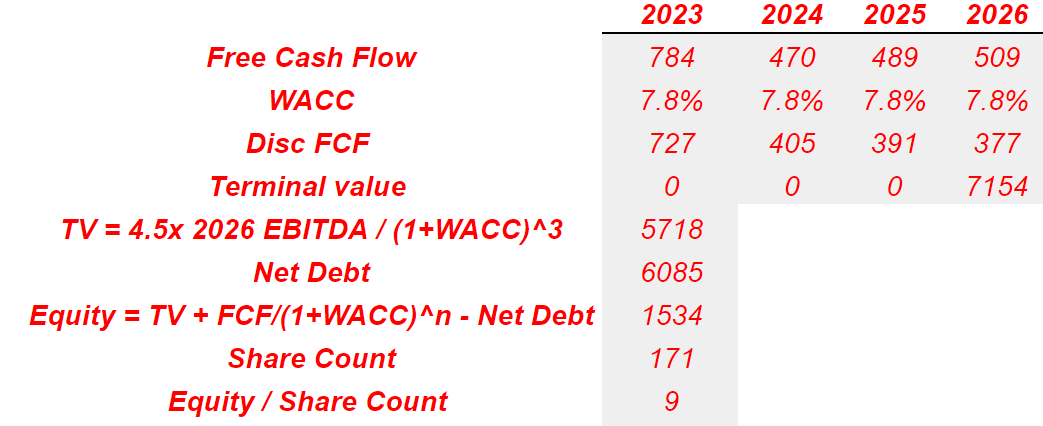

Under my own estimations, with an EBITDA margin of 40%, operating margin of 18%, and effective tax of 22%, I obtained a 2026 NOPAT of $967 million. I believe that my numbers are conservative and realistic.

My DCF Model

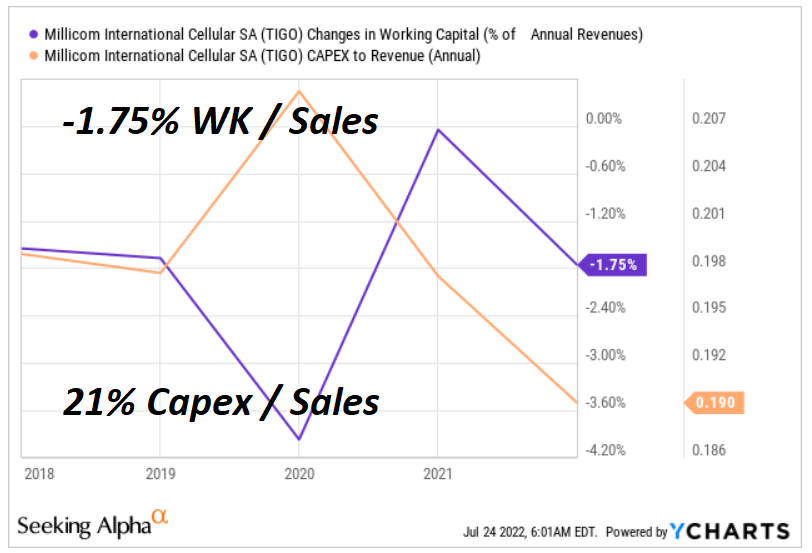

If we also subtract changes in working capital, with a ratio of WK/Sales of -1.75% sales and 21% capex/sales, 2023 FCF would be $810 million.

YCharts

According to Seeking Alpha, the sector is trading at 8x EBITDA. However, TIGO trades at close to 4.51x, so I used an exit multiple closer to 4.5x. With a discount of 6.6% and net debt of $6.08 billion, the implied price would be $41. The internal return appears optimistic at more than 44%.

SA My DCF Model

VoIP Technology, Failed Investments, And Licensing Could Bring The Stock Price Down To $9.5

In the last annual report, TIGO reported that an eventual increase in the demand for Voice over Internet Protocol services could damage TIGO’s financials. If clients decide to use the telephone less, but decide to use the internet more, TIGO would see a decline in its free cash flow. The following lines offer more information about this risk:

Growth in internet connectivity has led to the proliferation of entrants offering Voice over Internet Protocol services and video content services delivered over the internet. Such operators could displace the services we provide by using our customers’ internet access to enable the provision of communication, entertainment and information services directly to our customers. Failure to transform to data-driven products could have a negative impact on our legacy services and impact our results from operations. Source: 20-F

TIGO makes substantial investments in new technologies intending to generate growth in free cash flow. Under this scenario, I assumed that some of the new investments could go wrong, or clients don’t demand the company’s new technologies. As a result, future EBITDA margins are not as large as expected, and some investors may sell some shares.

If we are required to implement new technologies that are unable to generate sufficient returns, our profitability and ability to generate cash flow would be negatively affected, and we may be required to scale back our investments or delay the implementation of new technologies, which may have a negative impact on our growth and ability to attract and retain customers. Source: 20-F

TIGO has to renew some of its licenses from 2022 to 2026. If regulators decide not to sign new contracts with Millicom, I would expect a significant decline in revenue growth and free cash flow. If a sufficient number of equity researchers do note that decline in profitability, the stock price would decline:

Licenses due to expire in the medium-to-near term include our mobile telecommunications licenses in Paraguay (2022 and 2023), Nicaragua (2023) and Colombia (2023). In El Salvador, we have been in the process of renewing certain portions of the 3.5 GHz band with local coverage (not at a national level), which expired in 2018-2020. However, the regulator has shown an interest in reorganizing the band to prepare it for an auction for spectrum with national coverage during the second half of 2022. Other portions of the 3.5 GHz band will expire during 2026 and 2027. Source: 20-F

Let’s also mention that TIGO operates a business model, which is subject to a significant amount of scrutiny by governments. If the company does not comply with laws and regulators, we could expect fines or disputes. New acquisitions could also need the approval of governments in certain jurisdictions:

The licensing, construction, ownership and operation of mobile telephone, broadband and cable TV networks, and the grant, maintenance and renewal of the required licenses or permits, as well as radio frequency allocations and interconnection arrangements, are regulated by national, state, regional or local governmental authorities in the markets in which we operate, which can lead to disputes with government regulators. Source: 20-F

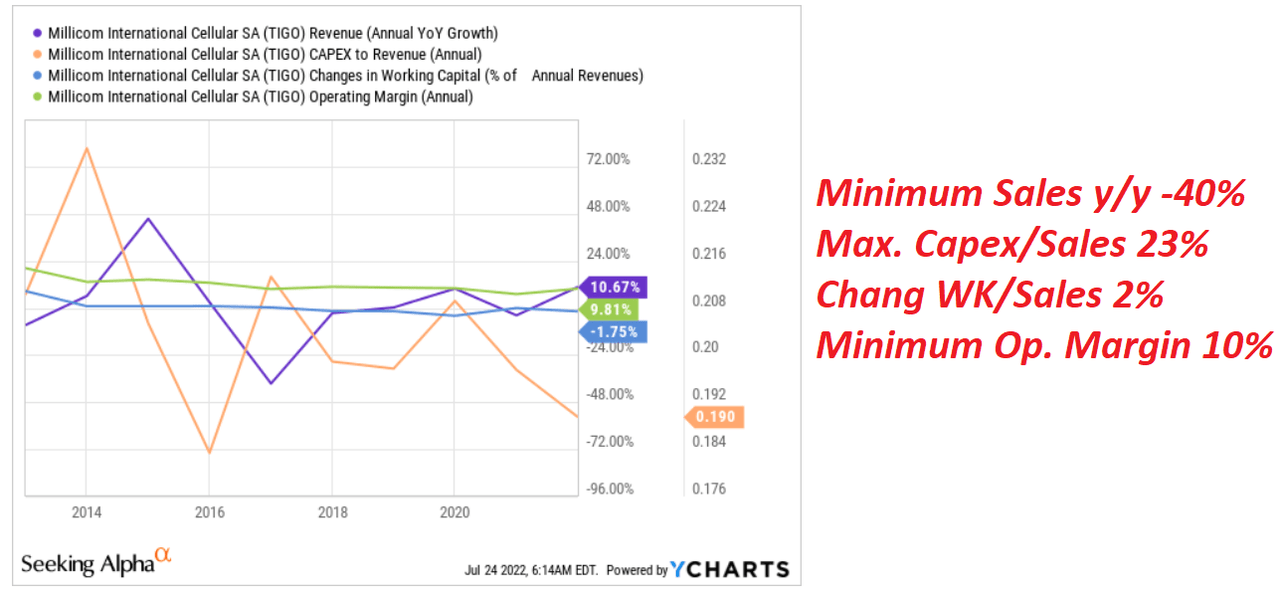

Considering previous figures, I depicted a scenario of large increases in working capital, a decline in sales growth, small operating margin, and a lot of capital expenditures. In the past, I saw sales growth of -40%, maximum capex/sales ratio of 23%, minimum operating margin of 10%, and change in working capital/sales of 2%. I used these figures for my financial model.

YCharts

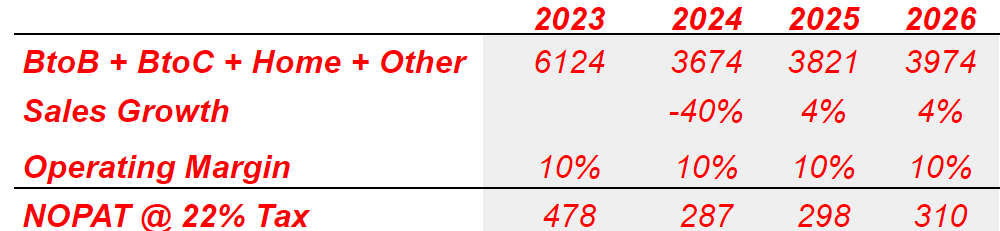

My revenue growth would include 2026 revenue of $3.9 billion, and 2026 non operating profit after tax of $310 million. Sales growth from 2025 to 2026 would stay at 4% y/y, which I believe is quite conservative.

My DCF Model

With declining free cash flow, an exit EV/EBITDA of 4.5x, and a share count of 171 million, the implied price would stay close to $9.5. Note that I am assuming a net debt of $6.08 billion, which was given by management in a recent presentation.

My DCF Model

Takeaway

TIGO reports a geographically diversified business model, and management is introducing products like Tigo Money. Both investment analysts and the company expect revenue growth and decent profitability margins. Considering that TIGO may announce a buyback program in 2023, and leverage may also go down, in my view, the stock price is too small. Under a simplistic DCF model, with conservative sales growth, the fair price could stand at close to $41 per share. It is significantly more than the current stock price.

Be the first to comment