kenneth-cheung

Since our latest publication, we are back to comment on Michelin (OTCPK:MGDDF). Last time, we were looking for an “upside between 20% and 25% from current levels, of which is a cash payout at a 2.3% dividend yield“. After almost two years, we can clearly say that we got it right.

Mare Evidence Lab’s previous publication

Why are we looking back to Michelin?

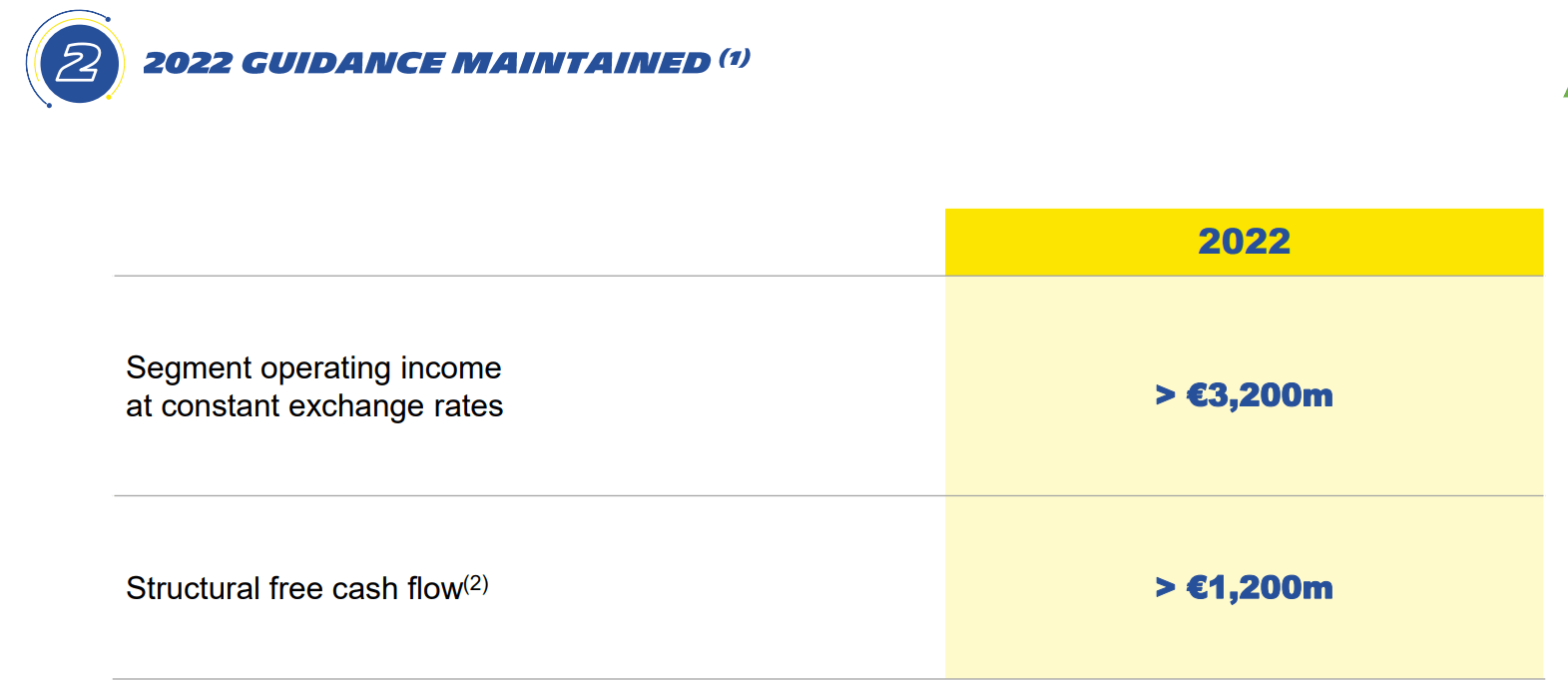

- Michelin’s 2022 guidance remains unchanged;

- We appreciate the fact that the company is able to increase prices over costs;

- Russian exit strategy and further implications.

Starting with the latest point, we can say that the number of multinational corporations that in protest against the war in Ukraine decided to leave Russia is continuously increasing. On June 28, Michelin and Nokian, active in the production of tires, both announced their exit from Russia. Our internal team believes that the two companies face two very different futures.

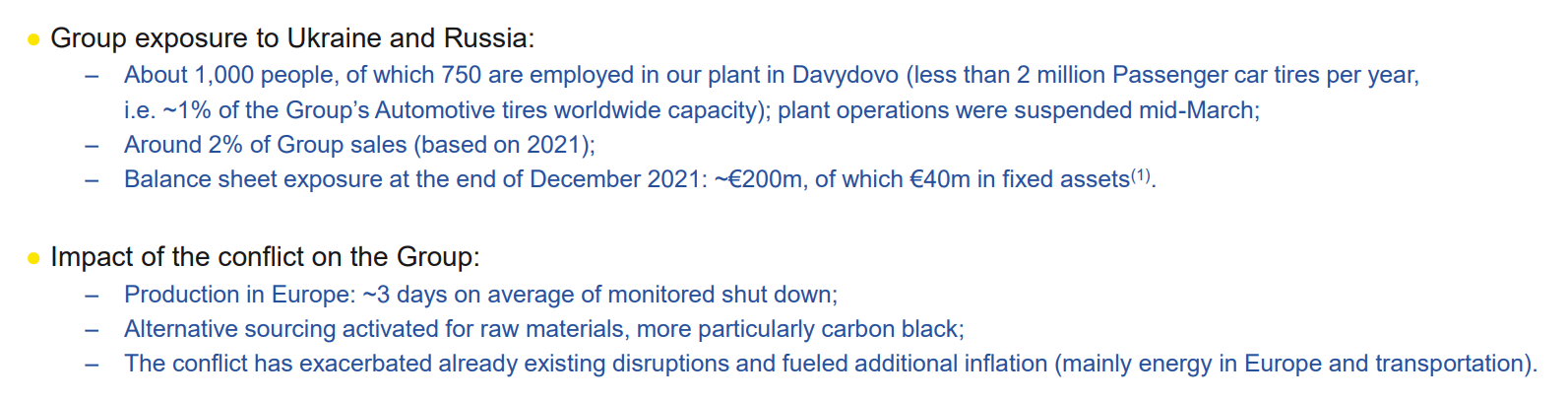

According to the French company, the complex geopolitical situation combined with the blockages of supply chains makes it impossible to resume production. In the country, Michelin has about a thousand employees, less than 1% of the total, an annual capacity of 1.5-2 million wheels mainly for cars, and it was currently generating 2% of the group’s sales. We have estimated that the exposure at the asset level is around €250 million and that this figure could correspond to the value of the provisions if the company terminates its business in Russia.

Michelin Russian’s exposure

Source: CEO Conference Exane BNP Paribas

Different is the case of Nokian which has a third of its employees and 80% of the annual capacity in the country. Shortly after the outbreak of the conflict, the Finnish company said it wanted to “keep the tire manufacturing plant in Russia active to make sure it remains operational and under the control of Nokian Tires into the future,” adding that it would seek to increase the production capacity of plants in Finland and the United States and to create additional capacity elsewhere. But as hostilities continue, management seems to want to focus on other markets. According to Mare Evidence Lab, Finland’s upcoming entry into NATO may also have played an important role.

Whatever the causes, Nokian risks write-downs of around €300 million in the second quarter of this year alone. By abandoning the country where it generates 20% of turnover, the company is preparing for a major downsizing, with a drop in production capacity from 23 to only 6 million; of which 5 million is in Finland and 1 million is in the United States now that it is in the ramp-up phase.

Aside from the Russian consideration, the company seems to have sufficient pricing power to mitigate the ongoing inflationary pressure. Over the first half of the year, tire demand has remained robust and Michelin has managed to increase prices to offset higher raw material costs.

Michelin Price MIX

Source: Michelin Q1 Results

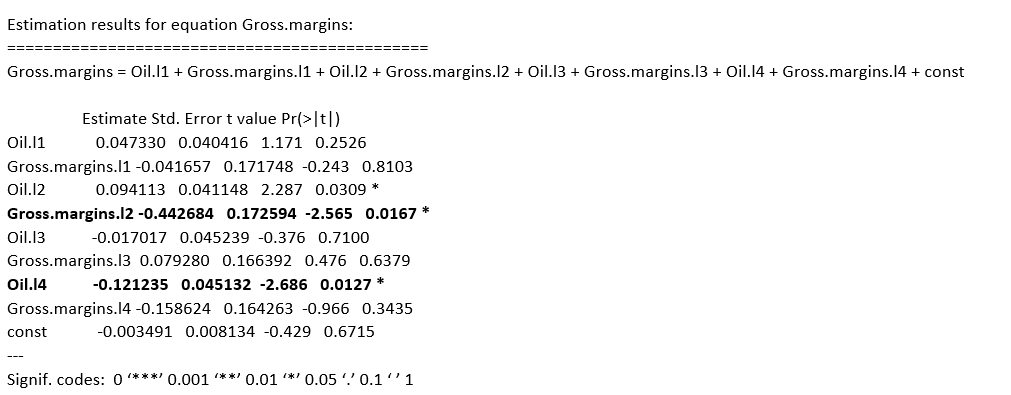

Thanks to our stats team and looking at the cost side, only gross margins exhibit the highest effect on the raw material price increase. As expected, it gets quickly diluted going down to the EBITDA line. Only in serious cases of the oil shock, does our statistical analysis shows a big impact on margins.

Mare Evidence Lab analysis

Source: Mare Evidence Lab analysis

Conclusion and Valuation

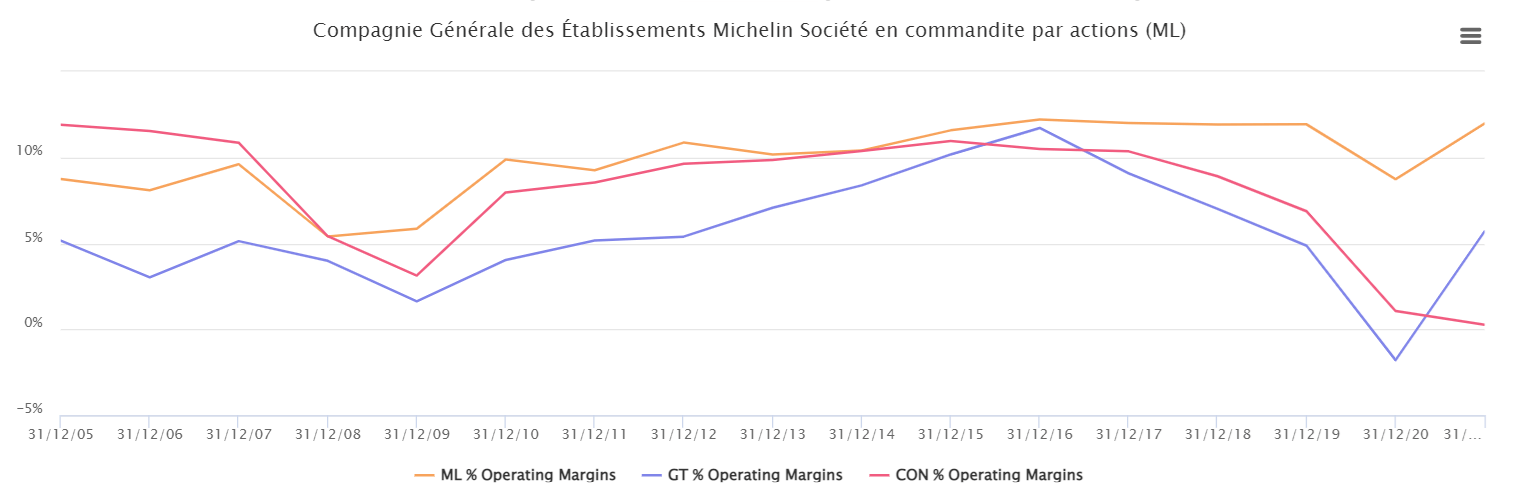

Despite the semiconductor shortage and lower volume of car production, Michelin has reaffirmed its 2022 guidance, maintaining its EBIT at €3.2 billion and FCF at €1.2 billion. Furthermore, the European Union has announced further sanctions against Putin’s country, which currently include a restriction on tire imports to EU countries from Russia. So, Michelin can take advantage of the fact that Nokian won’t export anymore. This could translate into a new slice of the European tire market and would make Nokian a potential future M&A target. Michelin’s growth is average compared to its peers, however, marginality is what makes the company superior to both competitors.

Operating margin compared to peers

Source: Mare Evidence Lab analysis

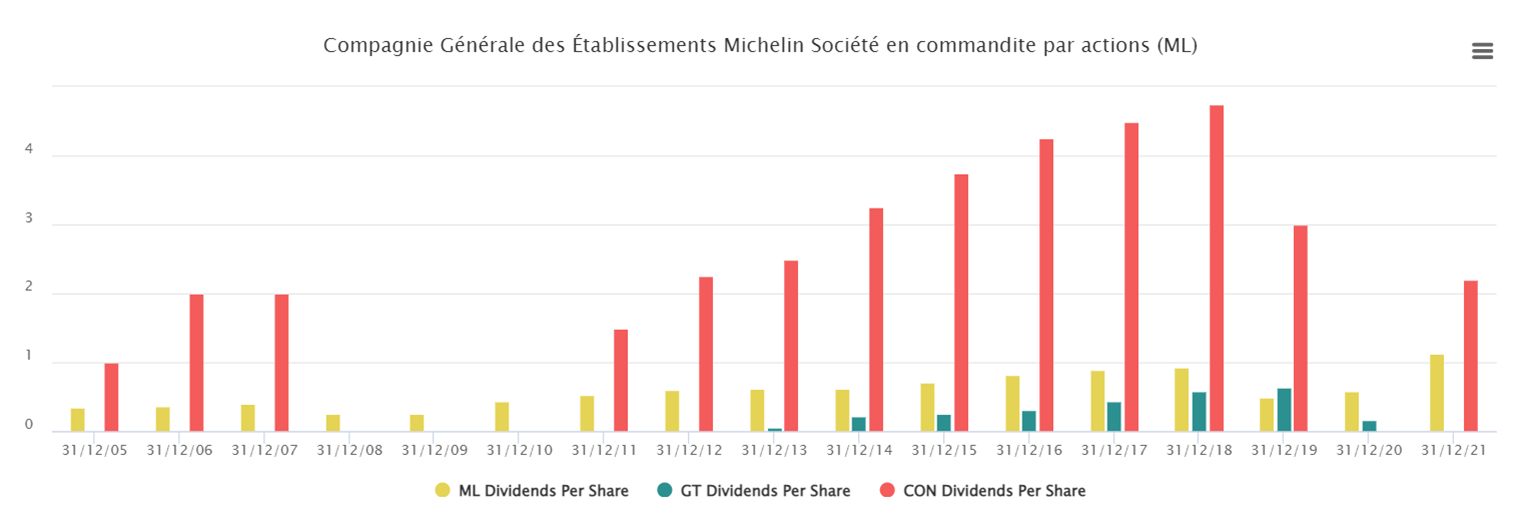

Finally, given the limited Michelin exposure of the group in Russia, we do not believe that the group de-consolidation could affect the 2022 guidance, and based on a 5.5x EV/EBITDA we confirm our target price at €34 per share. Based on a historical basis, we should also note that the company is currently trading at a higher discount on EV/EBITDA of 4.5x. versus the past five years at 5.5x. This discount is not justified compared to its peers namely Pirelli and Continental. As a margin of safety, investors might enjoy a pretty high dividend yield compared to the Michelin historical average. The company is currently yielding almost 4%.

Michelin Guidance

Source: Michelin Q1 Results

Michelin DPS compared to peers

Source: Mare Evidence Lab analysis

Be the first to comment