photoman/E+ via Getty Images

Meta Platforms (NASDAQ:META) is having one of those years, and it could get worse. First, during Q1, the company sustained the largest ever single-day loss of value by a public company. Since then, shares essentially languished before continuing their decline. This further weakness has taken Meta back to valuations last seen during the 2020 lows.

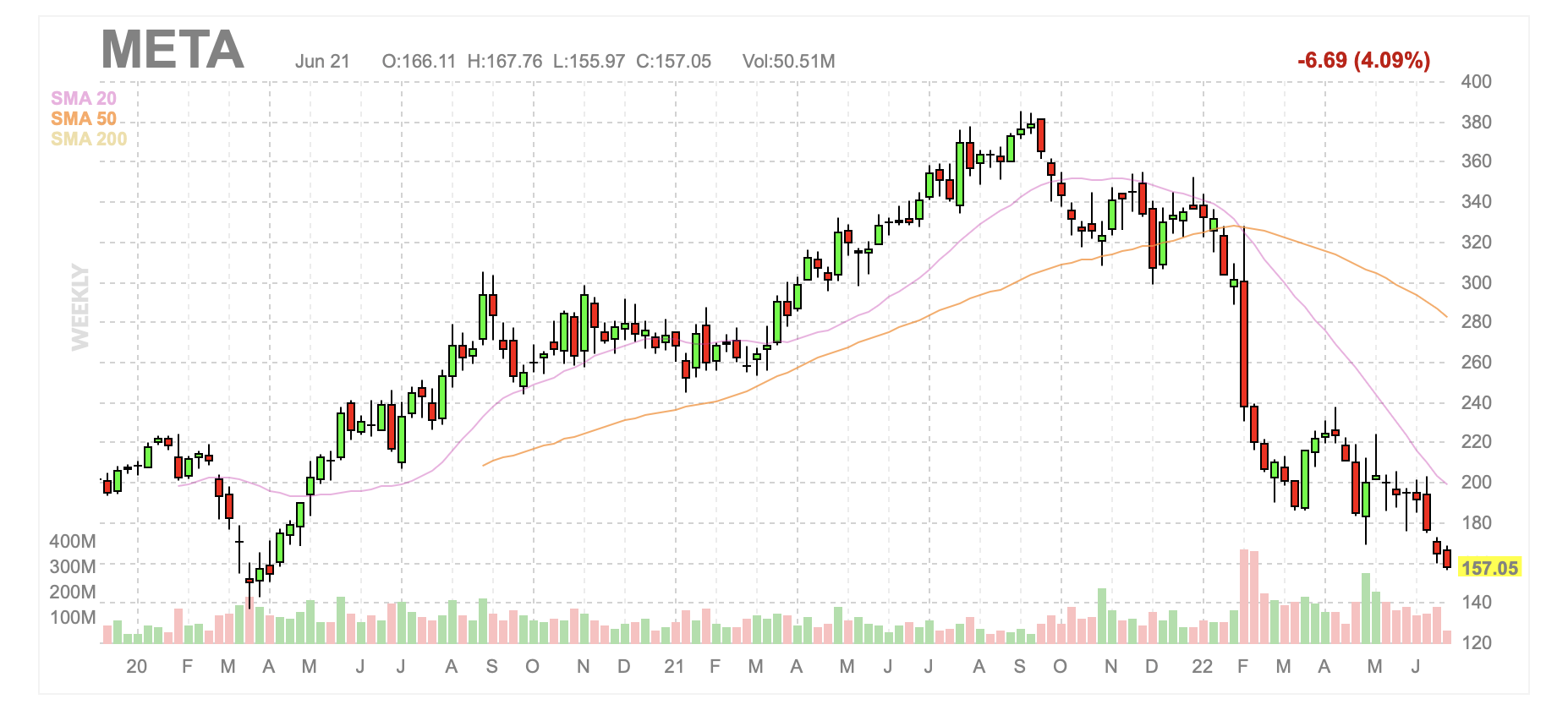

Meta weekly candlestick chart (Finviz)

The chart indicates there were quite a few buyers who acquired shares in 2020 and 2021 at prices well above $250, or even $300. A fair amount of those shareholders would probably love an opportunity to sell at their original cost.

This will be incredible resistance as Meta mounts any comeback. Many are probably wishing they sold for a loss between $200 and $220 earlier this year. Others bought in at those levels, and that is resistance now too. I suspect it is unlikely for Meta to return to the high $200s any time soon, and that a capitulatory decline below $150 is reasonably probable in the near term.

One of the more pressing issues facing Meta appears to be the significant level of uncertainty regarding its capacity to overcome Apple’s (AAPL) more recent privacy initiatives. The loss of that personal data affects the value of ads to iPhone users who restrict access to their data, turning high-margin targeted ads to iPhone users into lower-margin ones.

Simultaneously, there is a reasonably high probability that individuals are likely to cut costs in the coming months. Inflation has been unusually high, and many are suffering from it. It is likely that many have plans they will not cancel or otherwise substantially alter this summer, but spending patterns could change shortly thereafter.

At the same time Meta’s business worsened due to Apple’s privacy control features, Meta used a large portion of its substantial cash horde to repurchase shares. In doing so, Meta effectively took the profit it made throughout the Covid-19 lockdowns and halved its value.

Meta repurchased around $44.8 billion worth of stock in 2021, with about $33 billion of that occurring in the second half of the year, when the company’s shares were priced at over $300 per share. Meta spent $19.2 billion on buybacks in Q4 of 2021 alone. At the end of 2021, Meta held about $48 billion, so last year Meta basically spent half its money on its own shares, and at a time when they were twice as expensive as they currently are.

Meta has also earmarked where a significant portion of that remaining cash will end up. The company is spending to build its metaverse. The costs associated with simultaneously developing their metaverse while also adjusting to deal with enhanced data protection will end up being substantial, and this makes it more difficult for Meta to continue to repurchase shares at the same rate.

Due to rising interest rates, 2022 is not looking like the best of times to be proposing concepts that may be profitable in the future. Rather, the market currently desires returnable cash flow. Meta has the flow, but the company already indicated they will reinvest it.

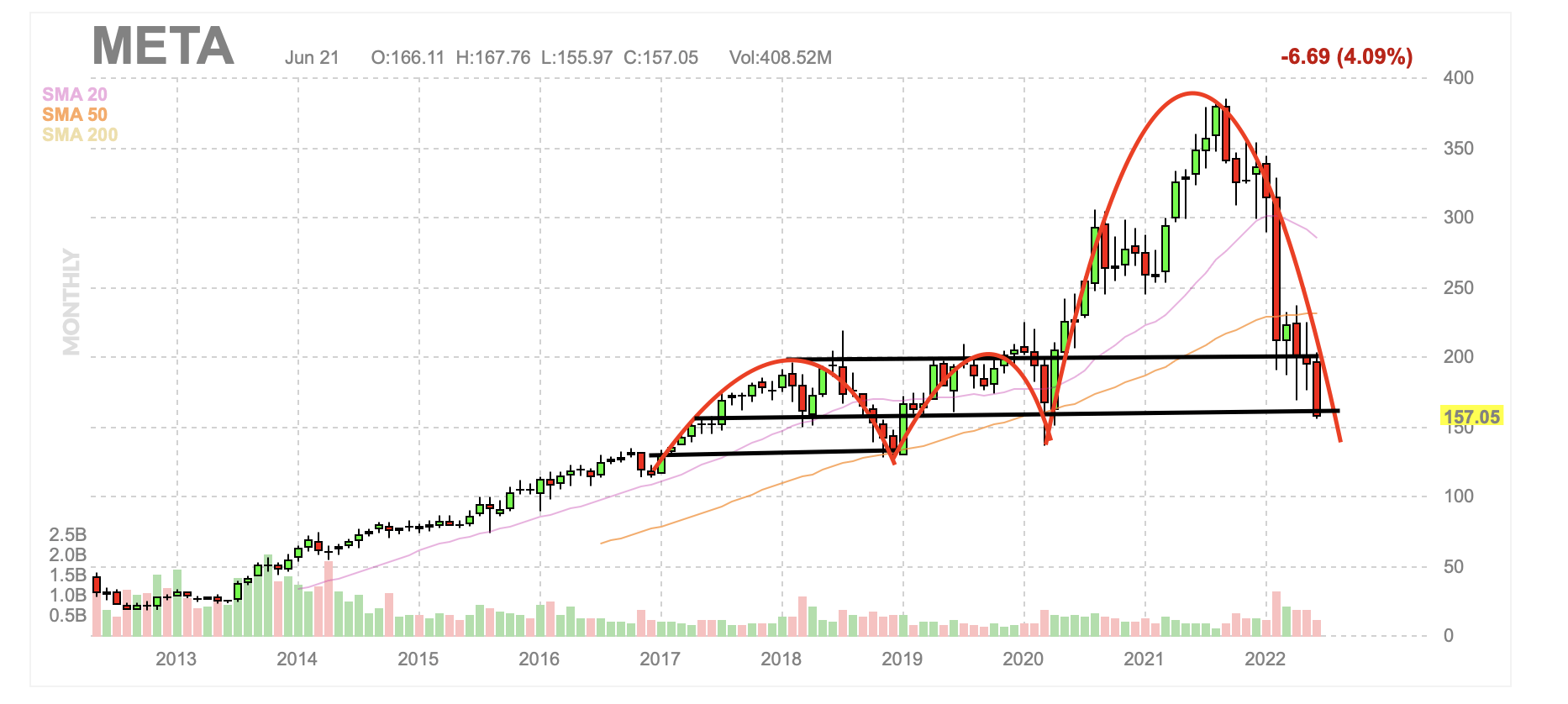

At the same time, it appears Meta shares face strong resistance at around $180, $200 and $250 per share. It appears unlikely that shares should substantially appreciate above these levels without a meaningful improvement to their business.

Meta monthly candlestick chart with red and black markings by Zvi Bar (Finviz)

As a result, Meta shares do not appear to offer a strong value at risk here, despite the significant and continuing selloff. Instead, the prudent move appears to be waiting for a capitulatory bottom. This could easily occur within the next quarter, as political risk heats up on account of the United States’ mid-term elections, as well as the possible further weakening of the economy.

Be the first to comment