JamesBrey

Medtronic’s Headwinds Not Over

Medtronic plc (NYSE:MDT) is a leading medical device company that operates in four primary segments. The company has been afflicted by supply chain challenges, healthcare labor demand/supply dynamics, and record inflation rates impacting its profitability margins.

MDT was also lifted to unsustainable pandemic valuation highs, which collapsed after topping in October 2021. The company has also been markedly impacted by forex headwinds, given its ex-US revenue exposure of nearly 50%. As such, the company also reflected an 18-cent impact on its adjusted EPS guidance for FY23 as it reported its FQ2 earnings in November.

Therefore, investors are urged to closely monitor the dollar index (DXY) to assess whether there could be further downside risks to its EPS outlook due to currency headwinds. Moreover, our analysis suggests that the DXY is consolidating as buyers return to support its uptrend bias. Hence, we don’t expect Medtronic’s H2’23 results to be lifted further by DXY tailwinds. As such, it could put further pressure on the company to depend more on its organic growth while still facing challenges from macroeconomic headwinds.

Medtronic highlighted in a recent conference that it’s optimistic about the long-term growth potential of its China business. CFO Karen Parkhill accentuated that it sees the business as a “double-digit grower in the future” despite near-term challenges relating to its value-based procurement (VBP) tenders.

However, Medtronic’s commentary suggests that it had already contemplated the headwinds in its previous guidance, reflecting a 15% to 20% impact. As such, there could be potential tailwinds to its forward estimates moving ahead.

Notwithstanding, the company has yet to receive constructive updates relating to lifting the warning letter by the FDA on its diabetes products. However, it’s still too early for investors to reflect optimism on an FDA inspection for now. Management has also been unable to proffer a timeline relating to the inspection of its facilities.

Still, Medtronic is sanguine over the prospects of the Hugo robot, the company’s robotic-assisted surgery system that could be used for several procedures. Medtronic believes the system could be a critical growth differentiator moving forward, helping to drive the company’s leadership in robotic surgery.

But MDT Has Been Battered

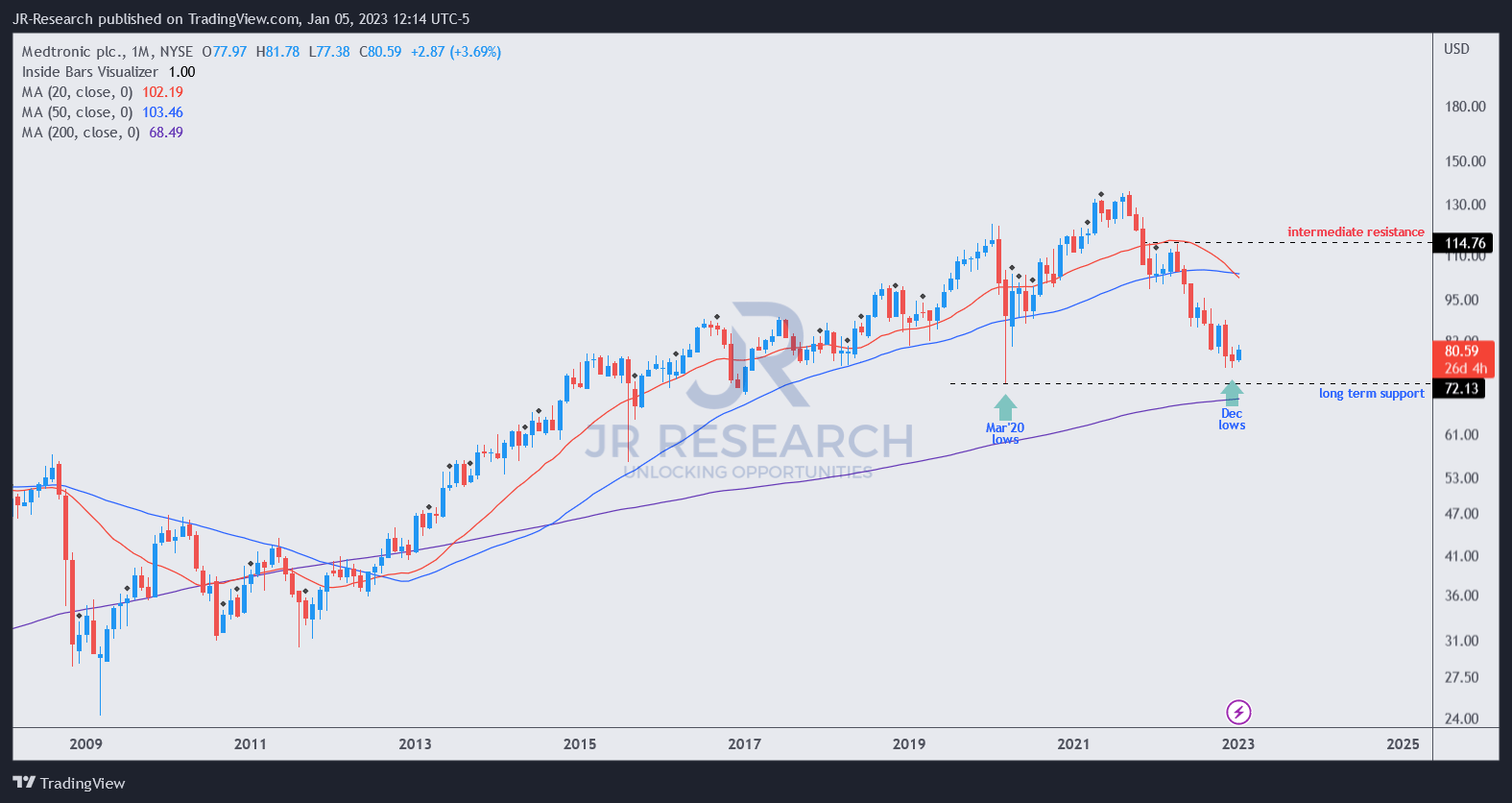

MDT remains 40% below its 2021 highs, even as we gleaned long-term buyers returning in December to stanch further downside.

Therefore, the company needs to execute better in H2FY23, as it telegraphed that it sees less significant supply chain headwinds. According to the New York Fed’s Global Supply Chain Pressure Index, the headwinds have already moderated substantially. Also, inflationary pressure should continue to abate, with the Fed remaining hawkish.

However, it’s also critical for investors to note that Medtronic has proven its profitable business model through the cycles, as it reported an adjusted EBITDA margin of 30% in its most recently reported quarter. Moreover, the consensus estimates suggest that its forward profitability should remain robust, with its FY23 adjusted EBITDA margins projected at 29.7%.

Hence, we believe its solid profitability should help sustain its recent buying sentiments as MDT attempts to recover its long-term uptrend.

Takeaway

MDT price chart (monthly) (TradingView)

MDT has suffered a collapse not seen since 2011, as it fell below its critical 50-month moving average (blue line), potentially losing its long-term bullish bias.

However, we observed that the battering had sent it down close to its COVID lows, improving the reward/risk for buyers at these levels. Moreover, its NTM EBITDA multiple of 13x suggests that MDT’s valuation has normalized. Also, its NTM P/E of 14.8x is well below its 10Y average of 17.5x. It’s also well below its industry peers’ average of 23.8x, according to Refinitiv data.

Hence, we assessed that investors anticipating a bottom to add more exposure should consider the current levels attractive.

Rating: Buy (Reiterated)

Be the first to comment