It’s time to talk about a stock that I haven’t covered as much as I used to. The Milwaukee, Wisconsin, based heavy-duty crane company Manitowoc (NYSE:MTW) is one of the smallest industrial companies on my radar, yet it’s one of the best stocks to use as a trading tool throughout economic cycles. This $350 million market cap company is currently trading 55% below its 52-week high, prices investors haven’t seen since the lows of 2020. The company is now seeing lower new orders on top of ongoing supply chain issues, high inflation, and further deteriorating economic conditions.

However, supply chain issues are easing, and shares have fallen so much that we’re dealing with a favorable valuation. While we aren’t out of the woods yet, I believe it’s time to turn bullish on the company.

Now, let’s dive into the details!

What’s Manitowoc, And Why It’s A Great Trading Tool?

One of the best ways to generate wealth on the stock market is to buy and hold great companies. That’s why I have almost all of my money in long-term dividend stocks.

There are also fantastic companies that I don’t want to hold on a long-term basis. Companies like Manitowoc make for fantastic trading vehicles that traders can use to trade any bullish or bearish thesis they might have.

With a market cap of $350 million, MTW is one of the smallest companies on my radar. Founded in 1902, the company is now a company solely focused on the production of mobile telescopic cranes, tower cranes, boom trucks, and everything related to cranes.

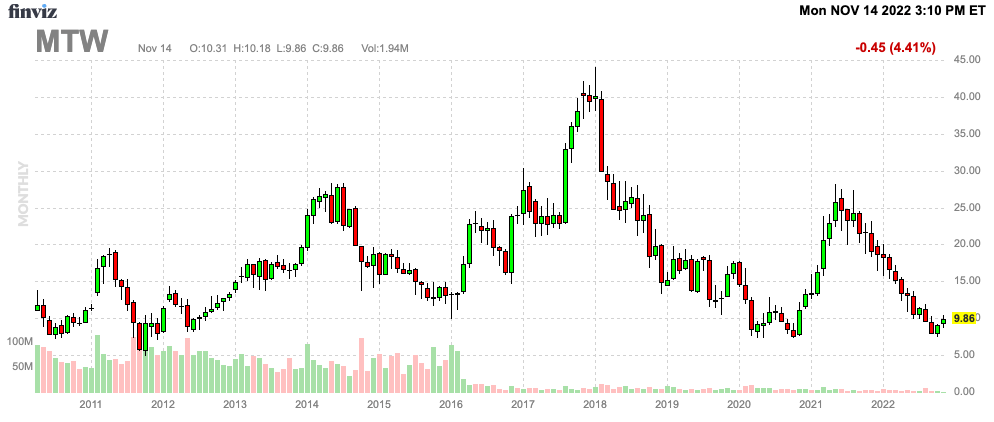

Before 2016, the company also included food service equipment. The volume bars in the graph below perfectly show the moment MTW became a pure-play crane company.

FINVIZ

As the graph above shows, the company has been prone to several steep drawdowns. During the 2014-2016 manufacturing downturn, the stock fell from $29 to (briefly) $10. In 2018, the stock peaked as soon as global growth started to roll over. It resulted in a decline from $45 to less than $10, as it also included the pandemic’s impact on the global economy.

These sell-offs are steep. But that’s OK – as long as investors know what they are dealing with. After all, what matters are the recoveries. MTW is a solid business, as we will discuss in this article, resulting in steep recoveries whenever economic expectations start to rebound.

The tricky part is finding bottoms. Right now, MTW shares are once again trading below $10. That could be a hint.

So, let’s dig a bit deeper.

The Economic Cycle’s Impact On MTW

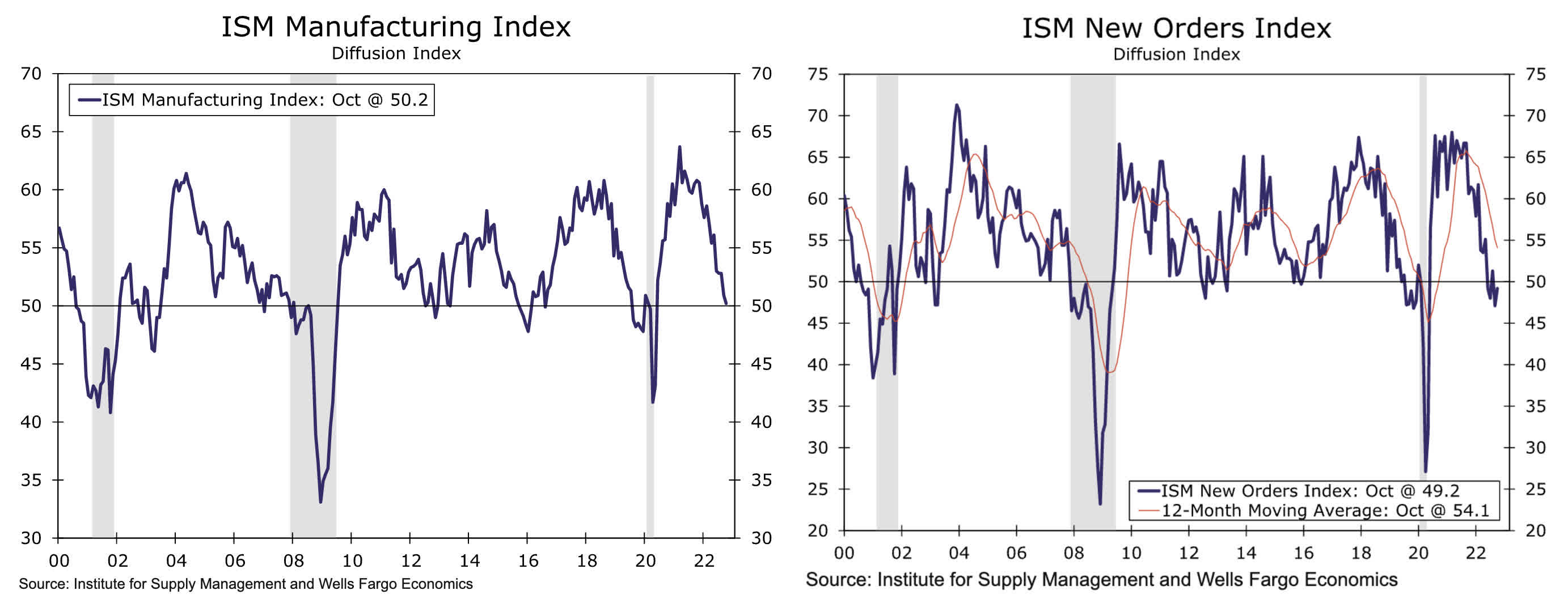

The economic cycle is driving MTW shares. Hence, without looking at any economic data, one may have guessed the state of the economy based on the MTW stock price. As we see below, economic growth has come down considerably. The ISM manufacturing index is flirting with the neutral level at 50, indicating that manufacturing growth has completely faded. The ISM new orders component is already in contraction territory as post-pandemic pent-up demand has completely faded.

Wells Fargo

On November 7, Manitowoc confirmed this economic trend.

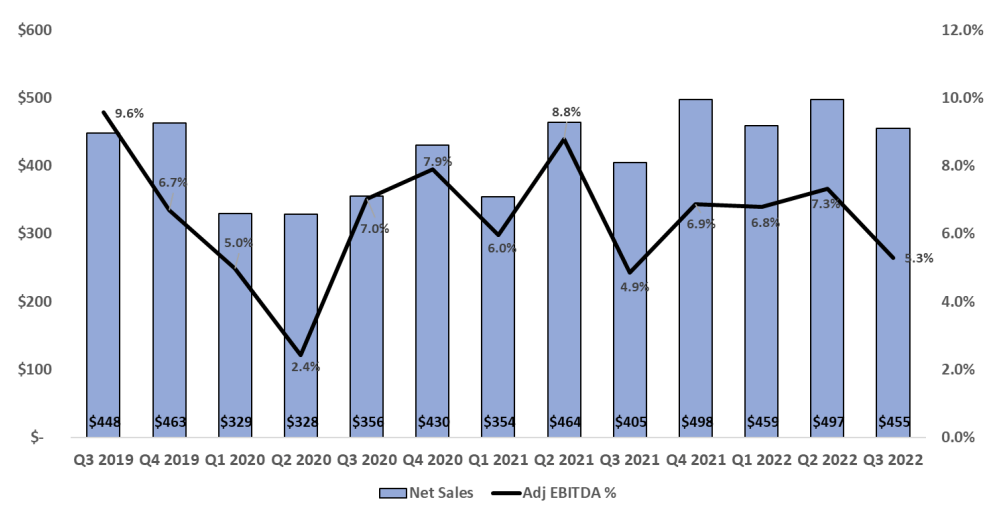

In its third quarter, the company did $455 million in revenue, 12.4% higher compared to the prior-year quarter, yet roughly $40 million less than expected.

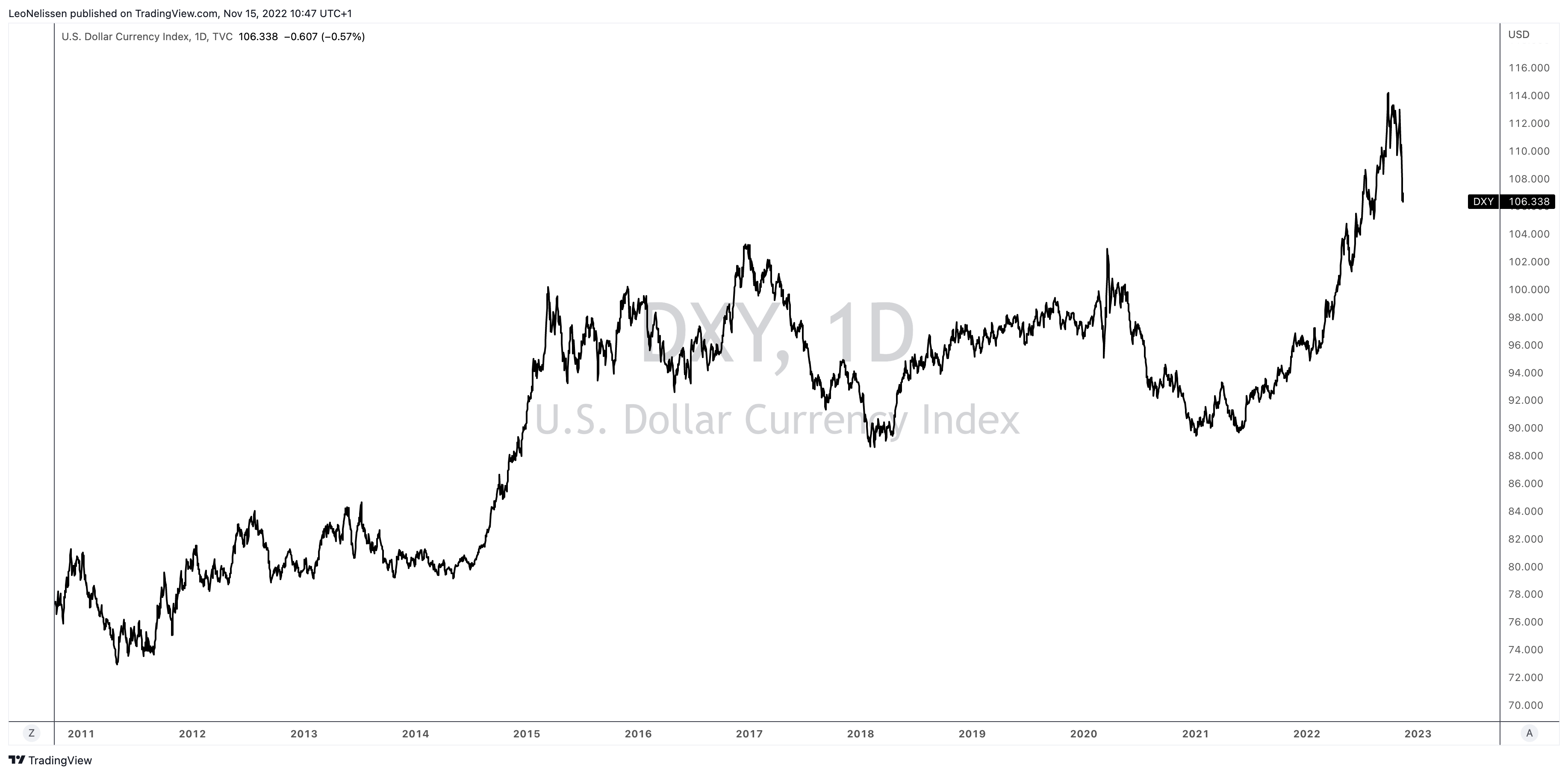

What matters more is the flow of new orders. In 3Q22, new orders totaled $472 million. That’s a decline of 13% compared to 3Q21. $24 million of this $71 million decline was a result of foreign currency translations. Bear in mind that MTW generated just 39% of its revenue in the United States in 2021. This leaves the company prone to currency risks. This is what the dollar index looks like:

The year-over-year decline was driven by lower demand in our EURAF segment, primarily due to softening macroeconomic conditions in the region, as mentioned by Aaron. This was partially offset by higher orders in our Americas segment.

The chart below shows the development of new orders. So far, weaker new orders have not impacted the company’s backlog as much. The company currently has a backlog of $943 million. The elevated level is caused by its inability to produce as much as it would like to, given persistent supply chain problems.

The Manitowoc Company

While I have made the case that I expect supply chain problems to ease in 2023, we continue to see that every single company struggling with heavy equipment is dealing with ongoing problems prohibiting smooth production.

It’s also hurting the company’s margins.

The Manitowoc Company

Moreover, despite the decline in new orders, new orders are still at elevated levels, with monthly new orders being consistent at $150 million per month for the last eight months. That level of consistency is unusual in the volatile crane business – especially in light of macro developments.

The bigger picture is what the company calls a tale of contradictions. According to Manitowoc:

On one hand, high oil prices, significant infrastructure spending, good crane utilization and a large backlog are usually signs of a strong crane cycle. On the other hand, we face an unprecedented supply chain and logistics crisis, the highest inflation in 40 years, an exceptionally strong dollar, rising interest rates and an unpredictable geopolitical situation on the back door of the EU.

It also helps that global crane fleets are aging as Manitowoc commented that every major crane house believes it needs to modernize its fleet.

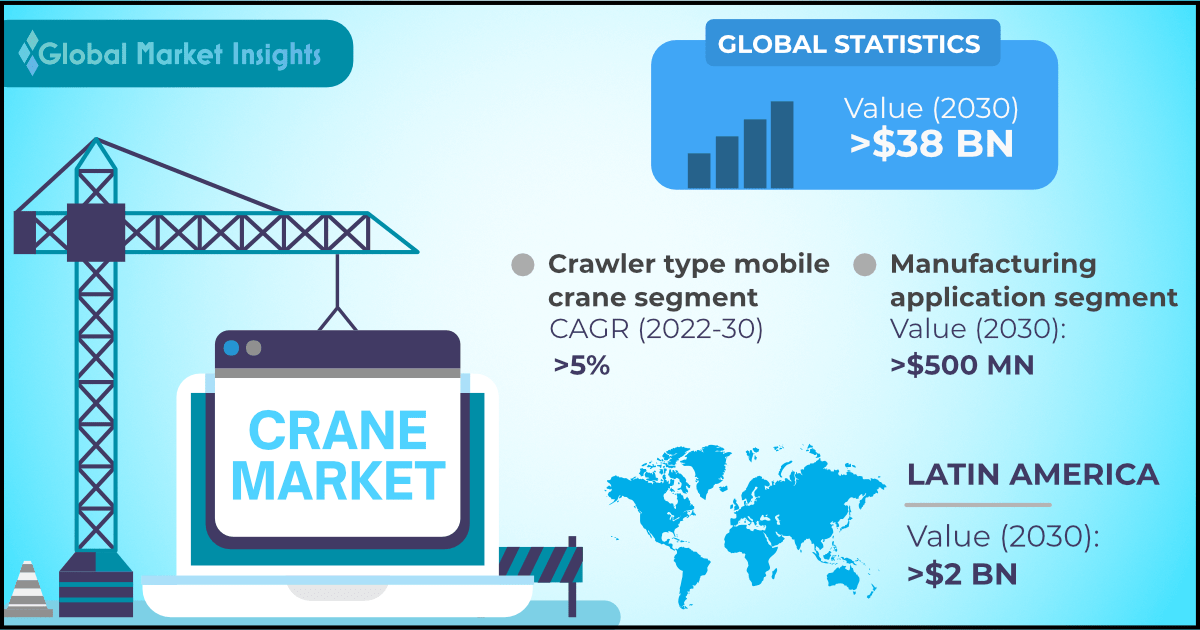

In this case, I believe it’s fair to say that the company is right as independent research confirms high demand. According to Global Market Insights:

The crane market is expected to cross a valuation of USD 38 billion by 2030, according to latest research study by Global Market Insights Inc. Increasing requirement of cranes in urban infrastructure development is anticipated to drive the industry trends. Rising disposable income of the working class, along with technological advancements in cranes, are speculated to increase the demand for cranes.

Global Market Insights

5% annual compounding demand growth would push demand to more than $38 billion in 2030.

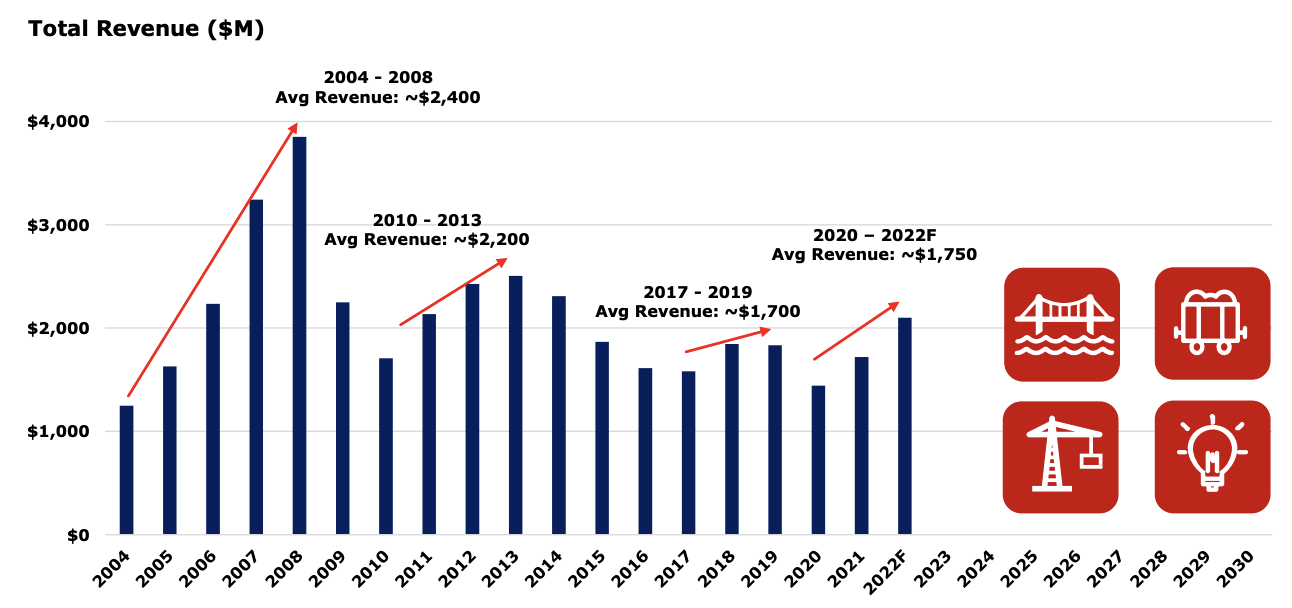

The company is hoping that its market could eventually see a new crane renaissance once macroeconomic conditions start to improve again. I hope they are right as every attempt at a meaningful recovery (since the Great Financial Crisis) ended in weakness before a new high could be reached.

The Manitowoc Company

The icons in the chart above stand for favorable macro tailwinds. This includes infrastructure renewal, electrification, fleet renewal, and strong commodity prices.

Moreover, the company is working on secular improvements that are supposed to stabilize its margins and revenue growth throughout economic cycles.

MTW focuses on non-new machine sales, which includes a stronger focus on parts and services (replacements, aftermarket), rental services with purchase possibilities, and refurbishment of old equipment (Caterpillar (CAT) does this as well).

In the third quarter, non-new machine sales were up 27%, on track to achieve the company’s 2022 targets. So far, this growth rate was mainly caused by acquisitions. Yet, the next few quarters will show improvements as MTW is increasing its field service population and its operating territory for these services.

So, what about the valuation?

Valuation

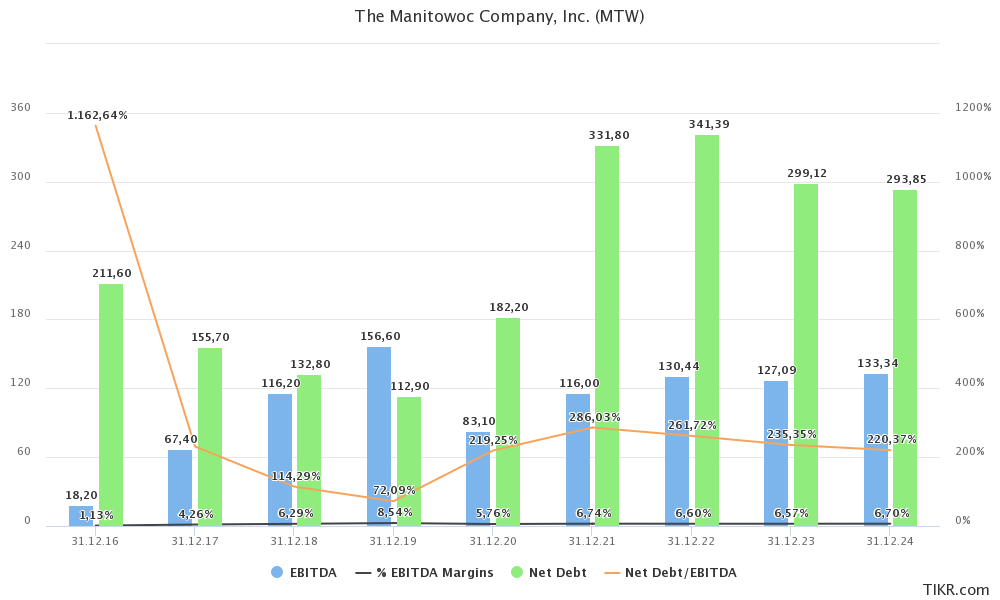

Looking at current expectations, we see that the company is not expected to deal with falling EBITDA – at least not by a lot. If anything, EBITDA is estimated to remain below pre-pandemic levels for a while with EBITDA margins close to 6.6%. Net debt is expected to come down to less than $300 million, providing the company with a favorable leverage ratio of less than 2.4x EBITDA.

TIKR.com

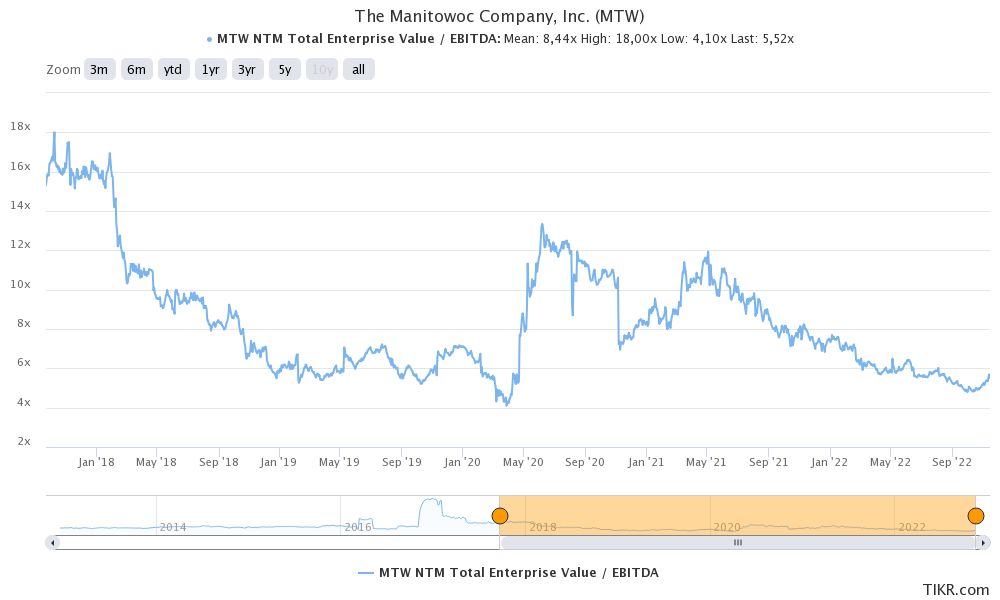

The company is now trading at 5.6x 2023E EBITDA, based on its $350 million market cap, $300 million in 2023E net debt, and $80 million in pension liabilities.

TIKR.com

That is a favorable valuation that could easily pave the way for a 100% to 150% stock price return in the three years ahead.

However, it’s not that easy. Despite its valuation, headwinds are significant. Supply chain issues are not gone yet, interest rates are high, pressuring economic demand, and the Fed continues to be eager to combat inflation, even if it means that more economic weakness is ahead.

Takeaway

In this article, we discussed a fascinating company in the crane business. Manitowoc is one of my favorite trading proxies that is now, once again, trading below $10. In this case, it’s caused by a severe deterioration in economic expectations, ongoing supply chain issues, high inflation, and all the downside that comes with that, like slow new orders growth and lower margins.

However, MTW’s valuation has become favorable. Its backlog is filled and supportive of stable sales growth in the years ahead. Moreover, its market is likely to experience strong demand growth once economic indicators bottom as a result of a much-needed replacement cycle.

It also helps that MTW is adding aftermarket and non-new services and products to its portfolio. This is expected to support margins and fill a niche the company has ignored so far.

The bottom line is that MTW is trading at an attractive risk/reward. However, it’s not a no-brainer. The economy remains in a tricky spot.

So, treat this as a wild card. If you think MTW is right for you, keep your exposure limited. After all, economic risks remain elevated. the stock could easily drop another 10-20% before the Fed is forced to pivot.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment