style-photography

Shares of Lumen (NYSE:LUMN) fell 21% after the telecom submitted its earnings sheet for the fourth quarter. Lumen beat topline and bottom line estimates for the quarter, but the guidance for FY 2023 is nothing short of a disaster. Because I bought Lumen’s shares chiefly because of the company’s strong free cash flow and growing broadband business, I am down-grading my rating for the telecom from strong buy to hold!

Strong broadband performance, but guidance for FY 2022 is a huge disappointment

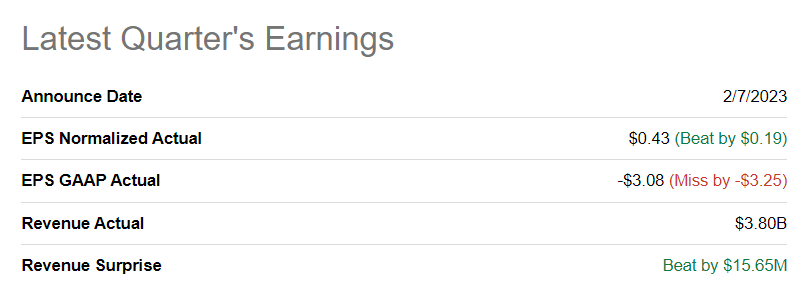

Lumen beat predictions for the top and bottom line for its fourth quarter on Tuesday. The telecom reported Q4’22 revenues of $3.80B, beating the consensus estimate by $16M. Lumen also reported better-than-expected adjusted earnings per share of $0.43 which beat the consensus estimate by $0.19.

Seeking Alpha

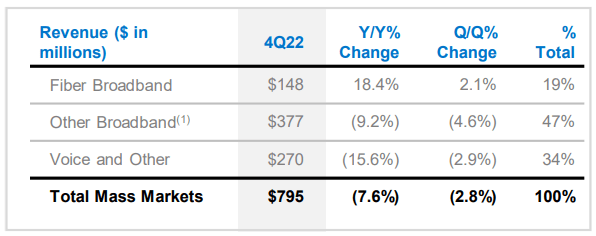

Although Lumen’s topline growth remains challenged in a saturated market, the company’s fiber business performed well and Lumen continued to make progress regarding the addition of new enabled locations. In Lumen’s continuing fiber business – the portion of the business that hasn’t been sold to Apollo in FY 2022 – the company added 19 thousand new broadband subscribers in the fourth quarter, bringing the year-end total to 832 thousand. Fiber-enabled locations grew 95 thousand quarter over quarter to 3.1M. Lumen has said that it sees an opportunity to triple its enable locations footprint in the longer term. Fiber broadband continued to be the fastest-growing segment for Lumen in Q4’22 as revenues increased 18.4% year over year to $148M.

Lumen

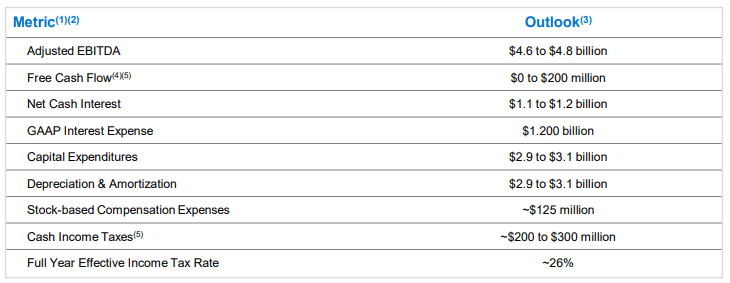

While Lumen’s broadband subscriber growth is solid, the most disappointing part of Lumen’s earnings release was the forecast for FY 2023. This year’s guidance implies $2.9B to $3.1B in CapEx – which is at about the same level as in the previous two years – and free cash flow of $0-200M, which is way below what I thought Lumen could achieve on a disposition-adjusted basis. Lumen sold assets worth about $10.2B in FY 2022 and I estimated that the sale-adjusted baseline free cash flow of Lumen was around $1.0B. Lumen expects organic declines, asset sales, inflation, and growth investments to weigh on its free cash flow in FY 2023. Last year, Lumen generated free cash flow in the amount of $2.26B.

Lumen

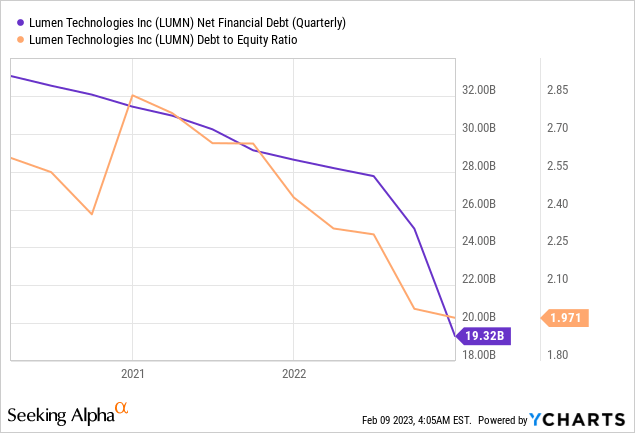

Lumen needs to accelerate debt repayments

Lumen operates with a heavily leveraged balance sheet that has been a key motivation for the company to sell non-core assets and to suspend its dividend in the fourth quarter. At the end of the December quarter, Lumen had net financial debt of $19.3B, which is a lot considering that the telecom’s total equity is just about $10B. Lumen, therefore, is carrying twice as much debt as equity on its balance sheet and the telecom needs to accelerate its debt repayments if management wants to get shareholders back into the stock in the future.

Lumen generated $10.2B in gross proceeds from asset sales in FY 2022 as the company sold its ILEC assets in 20 states as well as its business in Latin America. Of those proceeds, Lumen used $9.9B to reduce its net debt. Although Lumen has already had success in bringing down the total level of debt from more than $28.0B a year ago, Lumen’s attractiveness as an investment is likely going to be judged chiefly by how much management can reduce the telecom’s indebtedness over the next year or so.

Lumen also said in its earnings release that Colt Technology Services exercised its option to acquire Lumen’s EMEA business, which the telecom put up for sale for a price of $1.8B. The transaction could close at the end of the year, and Lumen is likely going to apply the proceeds to lower its net financial debt as well.

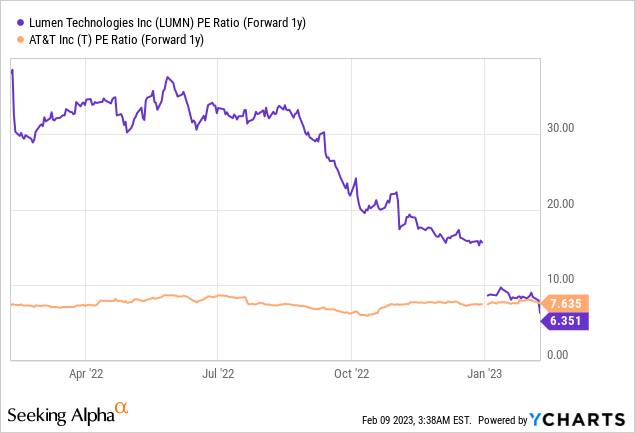

Lumen’s valuation

Lumen is currently valued at a price-to-earnings ratio of 6.4 X which seems low, but with free cash flow disappearing, investors have other, better choices to invest in telecoms. Specifically, AT&T (T) has a similar valuation based on earnings – a P-E ratio of 7.6 X – and AT&T is projected to generate $16B in free cash flow in FY 2023. This free cash flow implies a forward dividend payout ratio of approximately 50%, so I believe AT&T is pretty safe going forward. Considering that Lumen and AT&T are trading at a similar valuation level, AT&T would obviously be the better choice for investors that seek out an investment in the telecom space… and they get broadband exposure with AT&T as well.

Risks with Lumen

Lumen’s dividend is gone, and now investors have to make their peace with a breakeven (or very low) free cash flow projection for FY 2023. Going forward, I can imagine that investors will focus more on the company’s high leverage, which presents a risk in itself. Lumen expects to pay $1.1B to $1.2B in net cash interest in FY 2023, so if Lumen’s growth investments in areas like fiber broadband don’t pay off and free cash flow doesn’t rebound, the telecom could run into trouble meeting its debt obligations.

Final thoughts

Although Lumen submitted an earnings sheet for Q4’22 that was better than expected, the guidance for FY 2023 is a deal-breaker because it seriously limits Lumen’s revaluation potential. The guidance was the second blow the telecom has dealt shareholders in a matter of just a few months, the dividend suspension in Q4’22 being the first major blow that pushed shares of Lumen into a new down-leg. Now that investors may see only free cash flow breakeven in FY 2023, I believe the stock has a rather unattractive risk profile!

Be the first to comment