simonkr

Product and Market Overview

Livent Corporation (NYSE:LTHM) is a manufacturer of lithium chemicals used in batteries, agrochemicals, and aerospace alloys. The company operates production sites in the United States, England, India, China, and Argentina. Livent was spun off from FMC’s agricultural research enterprise to focus on lithium. The company is expanding its production capacity and is positioned as a preferred partner for leading automotive and battery manufacturers. The company supplies lithium hydroxide to Tesla, a partnership that will be expanded as early as this year. Rystad Energy data indicate that global lithium production capacity will not be sufficient to meet growing demand until 2030. A supply of 8,800 GWh of lithium batteries will be required (demand in 2021 was about 580 GWh) at 100% capacity, which is unlikely. Consequently, prices have risen to unprecedented levels as demand forecasts continue to rise, leaving automakers struggling to secure future deliveries.

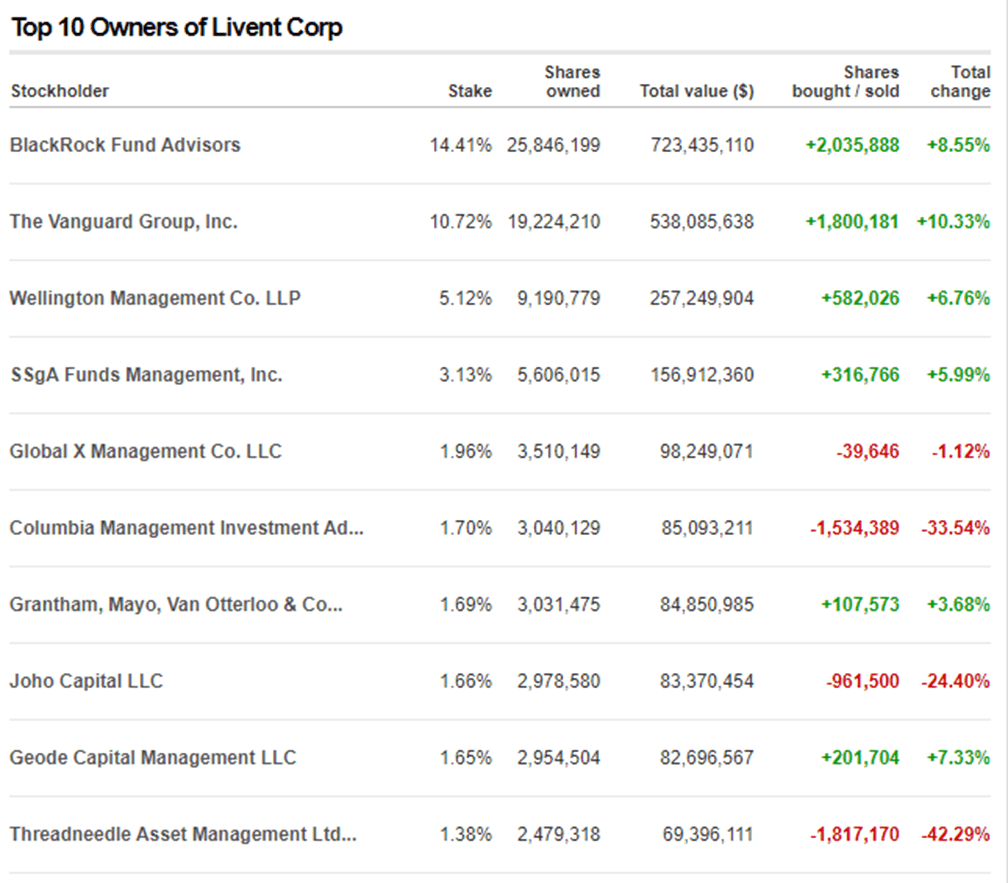

Also, interesting to note that BlackRock and Vanguard also account for 27% of the stock, and they also increased their shares last quarter. About 96% is held by institutional, 1% by management and only 3% by individuals. Most likely, such popularity among funds is due to the ESG trend.

Top 10 owners (CNN)

Recent quarterly results

Overall, Livent had good financial results in the third quarter as the business continues to improve performance in order to reach record levels of profitability. If we look at the numbers, for example, net profit grew by 1170% YoY. EBITDA +17% Q/Q, and more than six times higher than the previous year. The operating margin reached a solid 44%. Of course, high prices for all products and the company’s ability to take advantage of favourable market conditions contributed to all this.

In terms of the balance sheet, Net Debt is 48.6 million. Also, during the third quarter, Livent announced a five-year extension of its revolving line of credit through 2027, increasing it by $100 mn. This brings the total capacity of the line of credit to $500m and remains unused at the end of the quarter.

Interestingly, 70% of the current volume is at fixed prices, which are apparently well below market prices, and this situation will continue in 2023. The CEO has announced that they will no longer enter into long-term contracts without the possibility of price changes. Also, management noted that current lithium prices in China are exceptionally high, but even if they are seriously reduced by half will be able to get more from the sales price.

Q3 financial result (company results)

Forecasts

The market for lithium is tight, as evidenced by dwindling inventories throughout the supply chain and consistently high prices. Even at this high price level, lithium makes up a relatively small percentage of the total cost of an electric vehicle. Despite some short-term supply chain disruptions, especially in China, due to power outages and COVID-zero policies, demand for lithium remains incredibly high. As planned, the 5,000 metric ton lithium hydroxide expansion at Bessemer City was completed in the third quarter and is in the early stages of production and product qualification for customers. Livent is also on track to add the next 10,000 metric tons of lithium carbonate capacity in Argentina by the end of 2023. Nemaska, a project in which Livent has a 50 per cent stake, is also expected to have 34,000 metric tons of battery-grade lithium hydroxide capacity and more than 30 years of mine life.

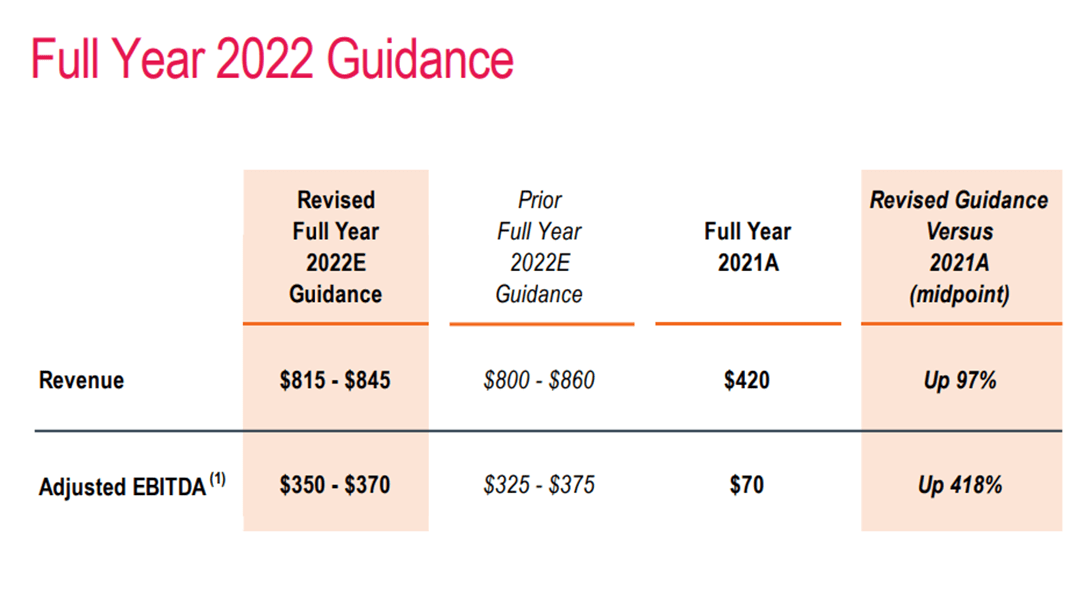

Looking at the numbers provided by management, revenue will be $815m to $845m which is in line with the consensus forecast ,adjusted EBITDA of $350m to $370m compared to the previous forecast of $325m-375m, CapEx of $320m (+142% y/y).

FY 2022 result (investor presentation)

Source: Investors presentation

Valuation

As for the forward multiples, it is about the industry average level, although two quarters ago it was three times more expensive. At the same time, the market has put an increase in production into the valuation. In general, we think that the popularity of lithium will grow and the world-famous major oil traders Trafigura Group and Glencore Plc (OTCPK:GLCNF) are already actively entering the lithium market. Livent can be compared to companies such as Albemarle (ALB) Lithium Americas (LAC) and Piedmont Lithium (PLL). If you look at the multiples, in comparison with these companies and the sector as a whole, Livent looks more expensive. But at the same time, the growth rate is noticeably stronger than that of the competitors. At historical near lows, FWD P/E of 14 and EV/EBITDA of 9, 3-year revenue CAGR of 18%.

Valuation multiples (Seeking alpha)

Summary

The company still looks promising, given the real possibility of becoming the largest lithium producer in the U.S. in the next few years. In terms of costs, no significant increase in prices for raw materials and other production costs is forecast. The customer base is also in place. Management said the immediate goal is to add, one, maybe two more major customers, but first it needs to expand supply. Given that the market now does not reflect a full increase in production capacity, for example, definitely does not take profit from Nemaska. Continued investment in expansion and new mines will also contribute to the company’s growth. Despite long-term contracts, the risks still include dependence on lithium prices. Thus, taking into account all the facts described above, we believe that prices below 20$ are a buying opportunity.

Be the first to comment