Editor’s note: Seeking Alpha is proud to welcome Yani Hellebaut as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

D3signAllTheThings

Investment Thesis

Future cash flows for Livent Corporation (NYSE:LTHM) look attractive because of the company’s ambitious expansion plans. The company recorded solid growth in sales last year, and so analysts see this trend continuing in the coming years. A Western catch-up in lithium production is gaining momentum but potential headwinds are expected in 2023. Continuing interest rate hikes and rising energy prices could still be a challenge. Despite a 35% drop from its all-time high in September 2022, I believe the LTHM stock is worth buying, given fundamentally strong future projections and internal growth forecasts.

Company Overview

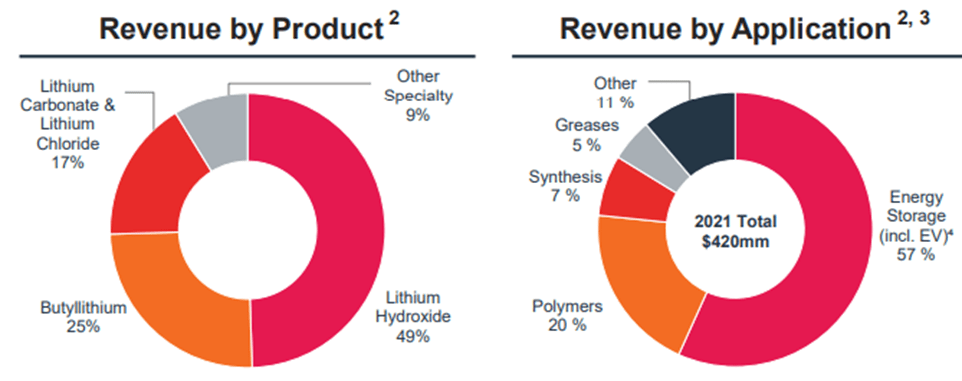

Livent Corporation is a purely lithium-focused company with high expertise in lithium hydroxide and lithium carbonate, which account for more than half of its sales. These two materials are critical in producing electric car batteries and battery storage applications. Consequently, 57% of the company’s sales are in battery storage applications and to the EV industry.

Investors presentation Livent Corp

70% of Livent’s sales come from Asia, which makes sense since China is the third largest lithium producer worldwide. I also have great expectations for their CEO, Paul Graves. Mr. Graves was managing director of investment banking at Goldman Sachs in Hong Kong from 2010 to 2012 and co-head of commodities in China. This experience will be necessary for completing future growth plans. Given Livent’s market value of $4.2 billion, it is still a “relatively” small company in the sector, especially when you look at the more prominent players such as Albemarle Corporation (ALB), Tianqi Lithium (OTCPK:TQLCF), Ganfeng Lithium Group Co., Ltd. (OTCPK:GNENF) and Sociedad Química y Minera de Chile S.A. (SQM). Nevertheless, the company is a unique player that focuses 100% on lithium which gives it a powerful position given the future demand forecast for lithium.

Spectacular revenue growth in 2022

The past year was very bright for Livent as it achieved strong revenue growth primarily due to an exponential rise in lithium prices. Revenue in Q3 of 2022 was $232 million, which is a 124% increase over Q3 of 2021. Capex through Q3 2022 stands at $218 million. So expectations of a $300 million to $340 million CAPEX for 2022 will likely be in that range.

Livent Corp. Form 10-Q (11/03/2022 – 09/30/2022)

Ambitious growth plan

In the coming years, Livent intends to go all out with an expansion plan to put its lithium position even more on the world map. The company’s lithium carbonate and lithium hydroxide projects will undergo a significant expansion. The Nemaska project, of which Livent has 50% ownership in Bécancour Québec, Canada, will require as much as $1 billion in capital to become operational. Production is expected to start in 2025. This is realistic but achievable, with projected sales of $1.62 billion by 2025.

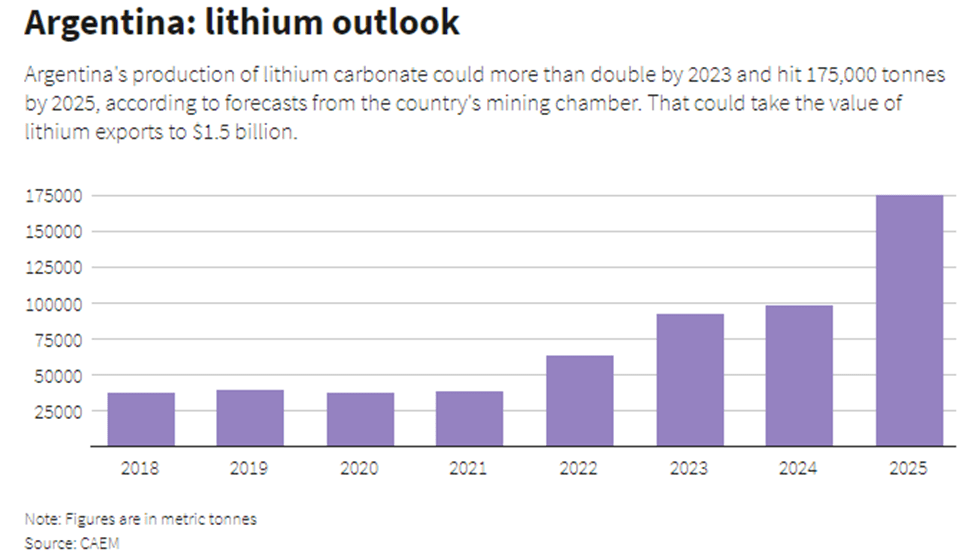

Expansions planned to boost lithium carbonate production primarily relate to the company’s facilities in Argentina. The plan is to bring their lithium hydroxide capacity to 55,000 mt/year by 2025 and lithium carbonate capacity to 100,000 mt/year by 2030. Given the current capacity, which is at 30,000 mt/year for lithium hydroxide and 20,000 mt/year for lithium carbonate, these are very ambitious expansion plans.

The chart below shows Argentina’s projected lithium production outlook over the next three years.

CAEM

Argentina is betting heavily on lithium production. An article in the Economist stated that by 2030, 16% of the global lithium production could come from China. On the other hand, Argentina exports 10% of the world’s lithium today. This figure could well go up sharply. Given the high demand for lithium, Argentina will only promote it from an economic standpoint, as it is a win-win situation for the country. Livent’s first two expansions in the country will involve capital spending of roughly $1 billion. The 2022 revenue was at $830 million. The plan with these expansions is to fund all expenses with the cash flow that will come in simultaneously. Low costs combined with a strong growth plan will put Livent in a much stronger position by 2023, increasing its incoming cash flow. Revenue expectations for 2023 are at $1.13 billion, which will net the large expenses required for expansions.

Livent has signed a partnership with U.S. carmaker General Motors to supply lithium hydroxide starting in 2025 for six years. That automakers will need to be assured of lithium supplies in the future is no longer a surprise. Given the increasingly scarce supply of raw materials in general, lithium will also be in short supply. Automakers who anticipate this and enter into cooperation agreements with lithium producers will be in a very strong position against their competitors. Livent is also strong today because of the GM partnership; I expect the company to get into other partnerships in the coming years.

Future Growth Expectations

If we look at the growth expectations from Seeking Alpha, we can see that Livent stands out. The company is the industry’s pre-eminent performer based on growth expectations. It already saw a significant increase in sales last year, which, combined with rising lithium prices, resulted in a substantial rise in its share price.

SeekingAlpha, growth Grade LTHM

These growths remain as expectations, which, of course, is not a certainty, but the plans in place can confirm the projections. I look forward to the next 1 or 2 years to see if Livent is able to meet its targets. The expansion plans are quite ambitious, but if executed well and under the supervision of strong management, I believe they will provide a lot of future cash flows.

Valuation

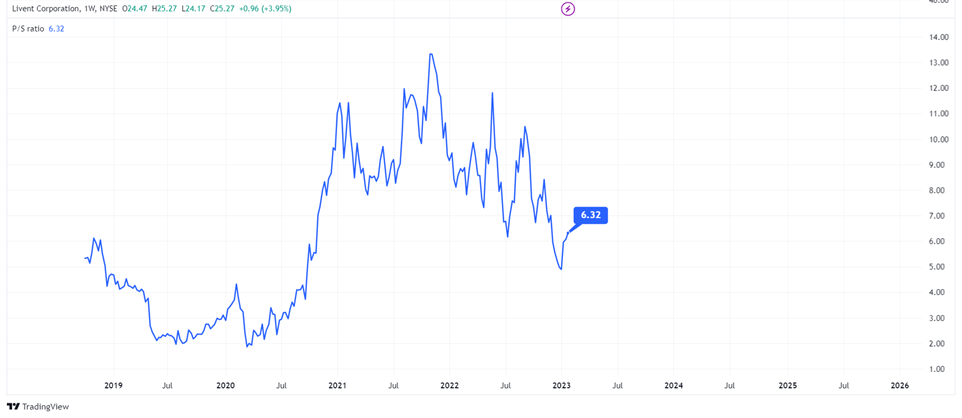

For a company primarily focused on growth, I prefer to use the P/S ratio since it is commonly used with cyclical companies and industries. Livent’s P/S ratio is down more than 50% since November 2021. The P/S ratio is much more useful than the P/E ratio in the case of Livent because profitability is not yet of great importance for a high-growth mining company.

P/S ratio Livent Corporation (Tradingview)

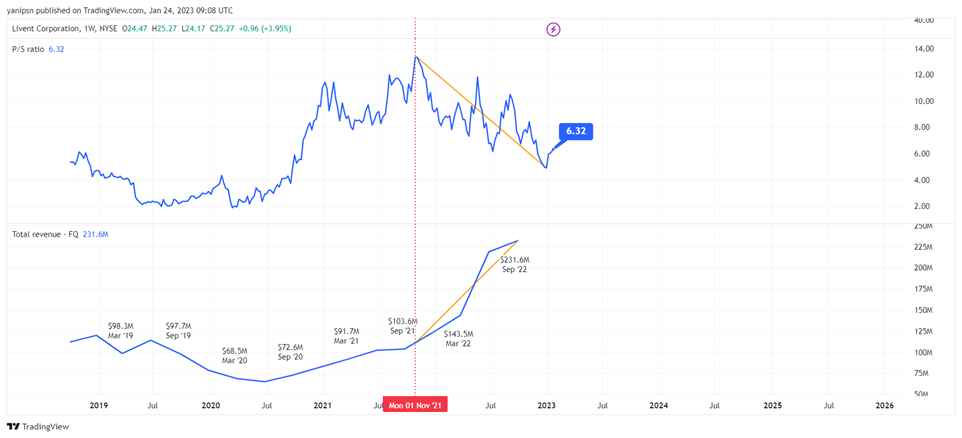

Livent’s P/S ratio stands at 6.32. The lower the P/S ratio, the better. We are just above the five-year average at present, but the ratio has fallen sharply since November 2021. In my opinion, a correct way to value the company will be based on its P/S ratio. Below is the comparison between P/S ratio and the revenue for Livent. Since November 2021, we have seen a strong increase in sales which today’s P/S ratio confirms.

P/S ratio vs. revenue – Livent Corp. (Tradingview)

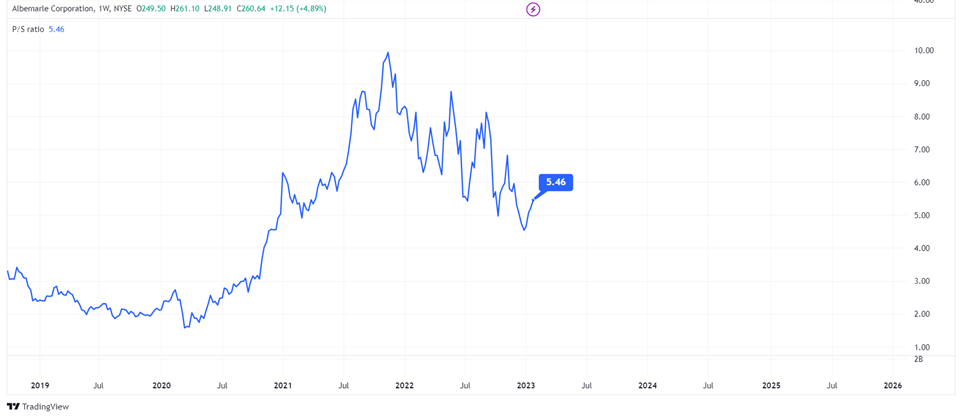

Now, I will compare Livent with Albemarle, which is almost ten times larger vs. the company in terms of market cap.

P/S ratio Albemarle (tradingview)

Albemarle had a very similar situation combined with strong sales growth last year. Despite Livent’s smaller size, the next few years look good because of expected sales growth. Because Livent still has growth up its sleeve, I believe the upside potential is much greater.

Looking at the P/E ratio, which currently stands at 18, Livent does perform slightly worse than the sector. This is because Livent is seen as a strong growth company in the lithium sector, and because of the expected revenue growth, it makes sense that their forward P/E ratio is higher than the sector. Hence, I would not use the P/E ratio for comparison with the sector, and it is best to look at P/S as a useful ratio. Strong growth expectations are still the most important factor with Livent.

China is leading, for now

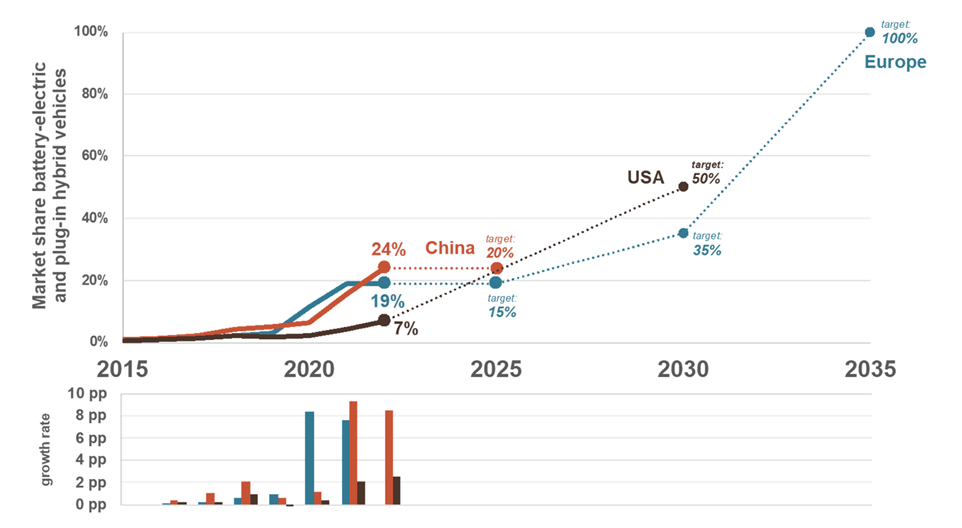

China is strongly ahead of the West in regards to lithium and battery production. Roughly 80% of the global battery production comes from the country. These are strong numbers, giving producers a great competitive edge over their Western counterparts. Also, electric car adoption is already much more advanced in China. 5.67 million EVs were sold in the country by 2022, according to the China Passenger Car Association. That the West needs to catch up is clear – both in lithium and battery production and in the adoption of electric cars. The green deal with climate goals and the Inflation Reduction Act are already good incentives to promote this catch-up, but in the short term, it will still be at a steady pace. The chart below shows the EV market share targets of China, the United States, and Europe.

A 2022 UPDATE ON ELECTRIC CAR SALES: CHINA TAKING THE LEAD, THE U.S. CATCHING UP, AND EUROPE FALLING BEHIND (theicct.org)

This a positive trend Livent can benefit from. China stands strong based on the market share it has today. Assuming that the West catches up, Livent can expect a dominant position in lithium and battery production by 2030. Putting this alongside the goals set by Europe and the US places Livent on the cusp of the electric revolution. For instance, Europe aims to bring carmaker emissions to 0 by 2035, while the United States wants 50% of all cars sold to be electric by 2030.

2023 could be a challenge but this is a long-term play

Livent has many investments re planned that will require a lot of capital. The plan is to be able to pay for these with incoming cash flows. The problem lies with production, which could see headwinds in 2023 due to recession fears and, if the Fed does not scale back on monetary policy, rising interest rates. Although I would consider the latter very unlikely, it is still important to consider because it could slow production and make it more difficult to secure the cash flows needed for expansion. Many analysts agree that a recession will occur in 2023. A December 2022 survey by Bloomberg of economists about the chances of a recession in 2023 resulted in a 70% chance that there will indeed be a recession, which will cause a lower overall demand for lithium. Whether that recession will occur is uncertain, so 2023 remains unpredictable. Livent has built a strong cash flow position through 2022, which will allow the company to get through a difficult year as 2023 could be. Despite these concerns, we should mainly look at the long-term trends in the lithium market. We can generally observe that battery and electric car production are at the cusp of a revolution. Even if we were to see a downturn in the economy this year, the long-term forecast in the lithium sector is still in favor of Livent Corp.

Key Takeaways

Livent has a strong growth forecast due to its ambitious expansion plans. A strong increase in future cash flows is expected but this is not yet an absolute certainty. The company already has a strong position as a lithium producer, and the partnership with General Motors is a confirmation of that leading position. Livent still has a lot of growth potential and will focus strongly on that growth in the coming years. In my opinion, it remains to be seen whether these expansions can be realized in 2023 if the recession and possible further interest rate hikes can throw a spanner in the works, which if they occur will have a negative effect on the share price in the short term. In the long term however, I believe Livent remains an interesting lithium stock with a lot of upside potential in the coming years.

Be the first to comment