Portra

LivaNova PLC (NASDAQ:LIVN) operates in the market of neuromodulation devices, which is expected to grow at a CAGR of close to 9.5%. Besides, management continues to make efforts to launch new products like Essenz Perfusion System, and appears to have agreements with insurance companies all over the world. In my view, conservative sales growth estimates lead to stock valuations that are significantly higher than what the market shows these days. My DCF model indicated a valuation of $68 per share.

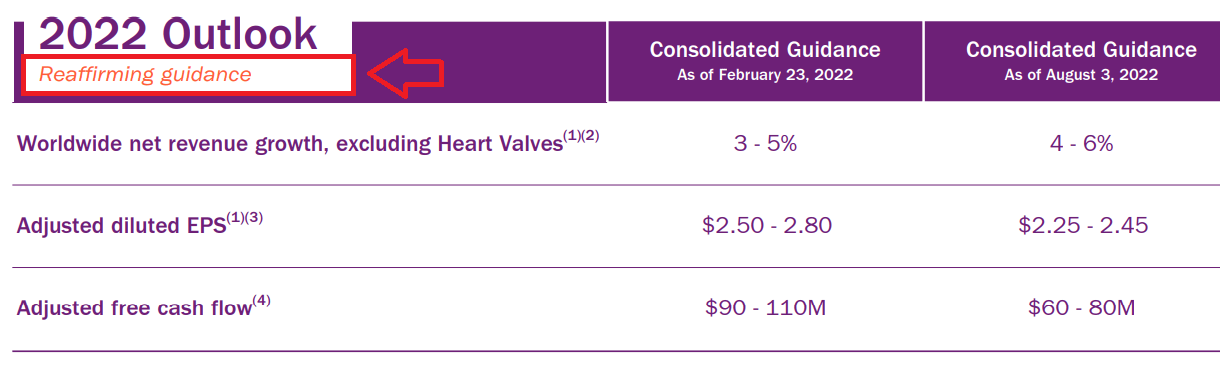

LivaNova Reaffirmed Its Guidance With $60-$80 Million FCF

Based in London and with active operations internationally, LivaNova provides high-tech medical devices for the benefit of healthcare professionals, patients, and healthcare systems around the world.

The main markets in which LivaNova has managed to position its products are the United States, Europe, and Japan, however the company does not rule out taking advantage of emerging markets in the future. Considering the geographic diversification of the business model, LivaNova’s revenue model appears to be more solid than that of competitors that operate only in one market.

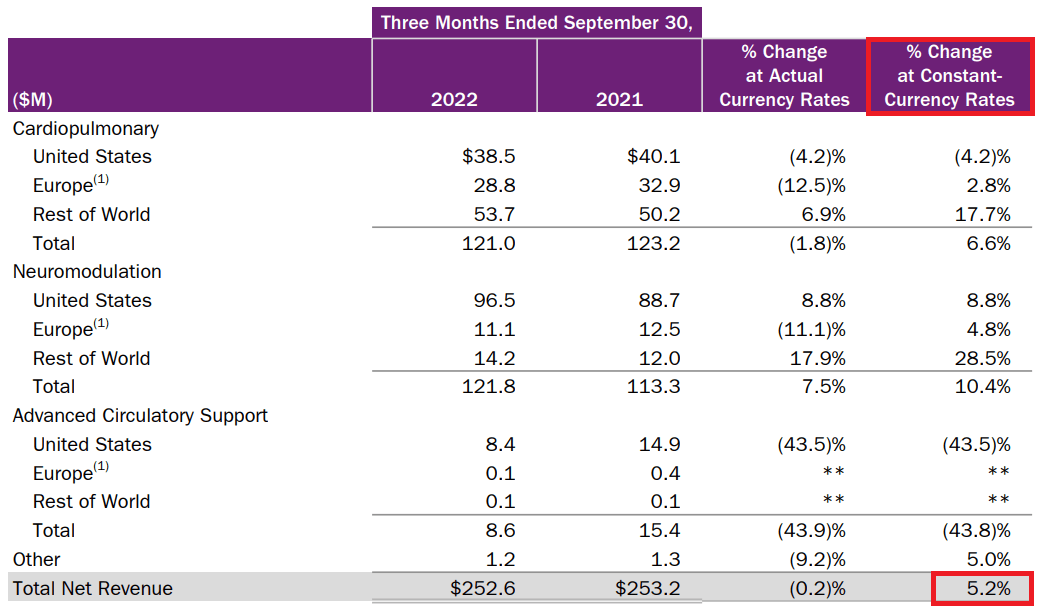

The recent quarterly revenue performance is also worth noting. The fact that the dollar became more expensive recently leads to negative total net revenue growth in dollars. However, if we use constant currency rates, LivaNova’s revenue actually grows at more than 5% q/q. In my view, only investors studying the company’s documents carefully will notice the quarterly sales growth.

Source: Quarterly Presentation

It is also worth noting that management reaffirmed its guidance and included 4%-6% sales growth with adjusted free cash flow close to $60-$80 million. Considering these figures, I believe that running a DCF valuation model could make sense for the company.

Source: Quarterly Presentation

Finally, I am quite optimistic about the recent commercial efforts to sell the new Essenz Perfusion System in Europe. In my view, if the company is successful, and decides to launch the product in more markets, I would be expecting sales growth in 2023 and 2024. In my view, the following lines from the press release are quite relevant in this regard.

The release has been initiated in select centers throughout Europe, following a successful clinical experience in two major centers, Catharina Hospital in Eindhoven, Netherlands and San Donato Hospital in Milan, Italy.

Consisting of a next-generation heart-lung machine and a transformative patient monitor, Essenz puts data at the forefront to deliver a patient-tailored approach that supports data-driven decisions during life-saving cardiopulmonary bypass procedures. Source: LivaNova Initiates Limited Commercial Release in Europe of the Essenz Perfusion System for Cardiopulmonary Bypass Procedures

Business Segments: The Neuromodulation Segment Expects To Enjoy Market Growth Of Close to 9.5%

LivaNova’s business model is divided into three segments, the cardiopulmonary segment, the neuromodulation segment, and the advanced support segment for air circulation. Both the cardiopulmonary and the advanced support segments are usually affected by the winter season, when the greatest number of cases are recorded. The neuromodulation segment, on the other hand, is maintained at the same rate throughout the year.

The cardiopulmonary segment designs and distributes different devices, including oxygen machines, lungs and heart machines, blood transfusion systems, and accessories such as perforating tubes. The neuromodulation segment is mainly aimed at the development and operation of Vagus Nerve Stimulation Therapy, which is a form of therapy through which stimulation of the hypoglossal nerve is used for the treatment of depression and chronic epilepsy. Lastly, the advanced support segment is dedicated to the development and sale of long-lasting products to strengthen the functioning of the lungs and the heart.

The company operates in markets that are expected to grow at a CAGR of close to 6.9% and 9.5% in the near future. I believe that assuming sales growth close to these figures makes sense.

The cardiovascular devices market is estimated to be valued at US$59.57 billion in 2022 and is projected to grow at a CAGR of 6.92% during the forecast period 2023-2033. Source: Cardiovascular Devices Market Rise at 6.9% CAGR [2021-2028]

The global neuromodulation devices market size stood at USD 4.51 billion in 2018 and is projected to reach USD 9.34 billion by 2026, exhibiting a CAGR of 9.5% during the forecast period. Source: Global Neuromodulation Devices Market Growth, Trends | Report, 2026

Balance Sheet

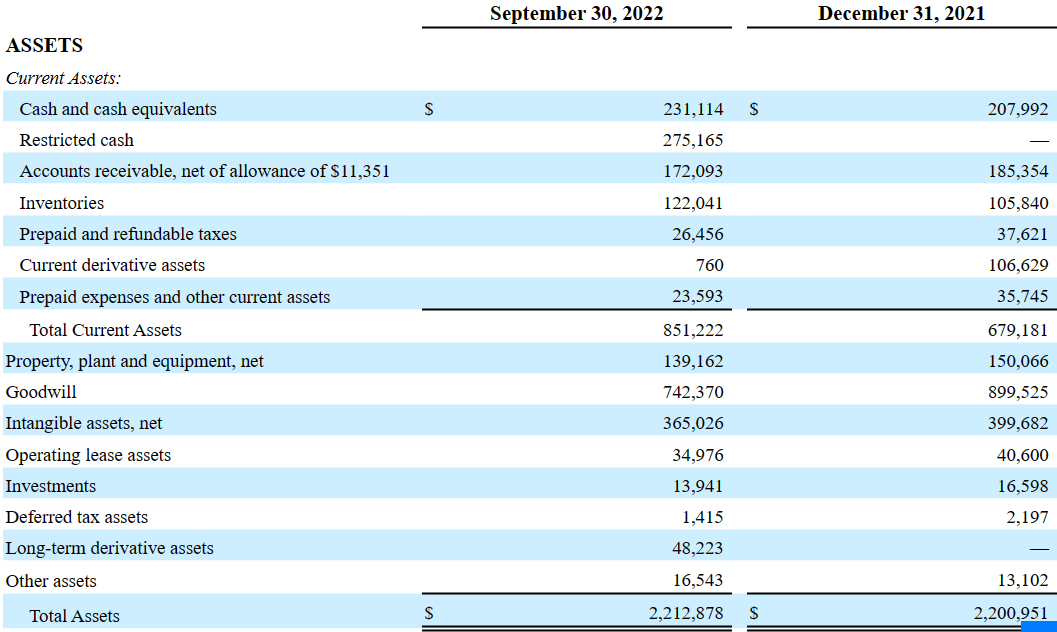

As of September 30, 2022, LivaNova reported cash worth $231.114 million accompanied by restricted cash of $275.165 million. Additionally, accounts receivable stood at $172.093 million with inventories of around $122.041 million, prepaid and refundable taxes worth around $26.456 million, and prepaid expenses of $23.593 million. The total amount of current assets of $851.222 million is significantly higher than the total amount of current liabilities.

With property, plant and equipment worth $139.162 million, goodwill of $742.370 million, and intangible assets of $365.026 million, LivaNova also reported operating lease assets of $34,976 million. Long term derivative assets were equal to $48.223 million with other assets of $16.543 million and total assets of $2.212 billion.

Source: 10-Q

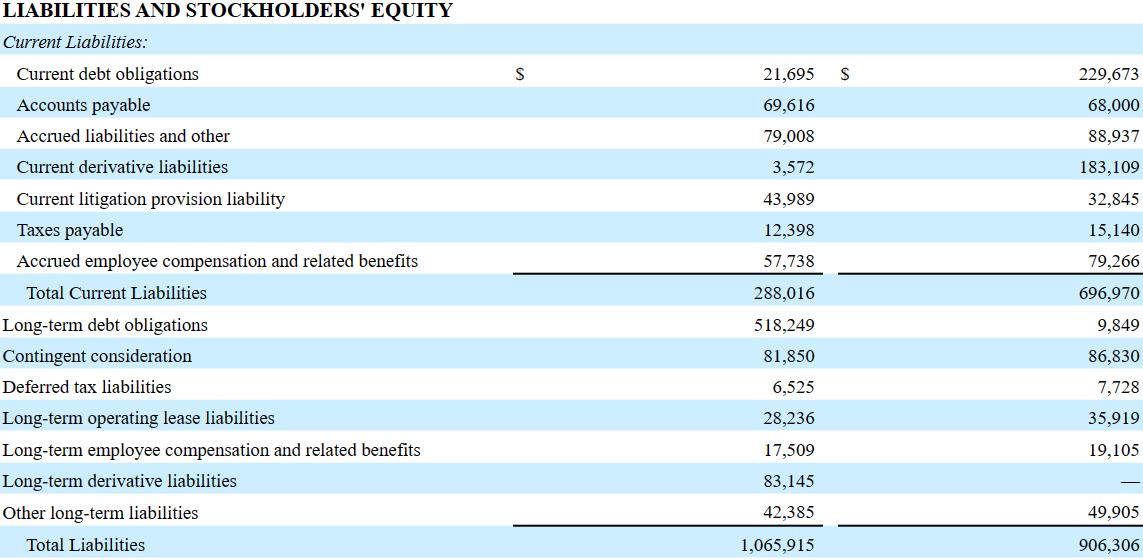

The company also reported current debt obligations of $21.695 million, accounts payable worth $69.61 million, and accrued liabilities of close to $79.008 million. Besides, current litigation provision liability stood at $43.989 million, with taxes payable of $12.398 million and total current liabilities of $288.016 million.

Long term debt obligations were equal to $518 million together with a contingent consideration of $81.850 million and long term operating lease liabilities of $28.236 million. Long term employee compensation was equal to $17.509 million with long term derivative liabilities of $83.145 million. Finally, total liabilities stood at $1.065 billion.

Source: 10-Q

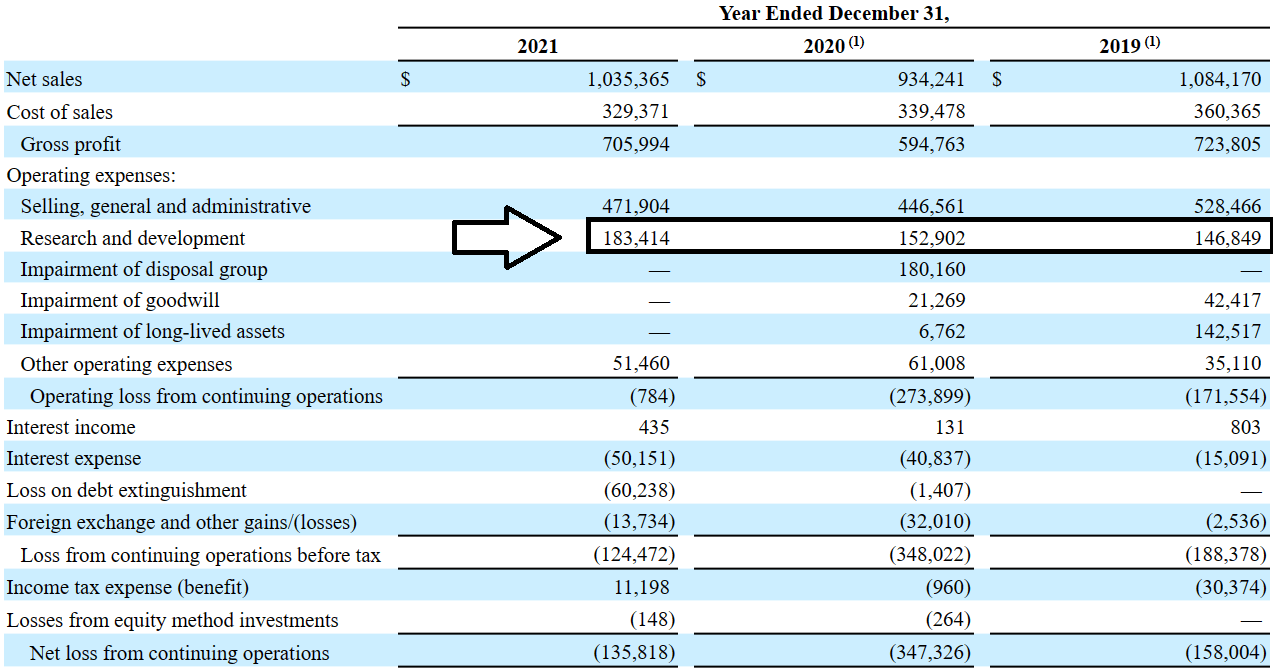

Income Statement Analysis And Expectations From Other Analysts

I carefully studied the company’s income statement to run my financial model. I believe that investors may want to do the same.

In 2021, the company reported net sales of $1.035 billion with cost of sales of $329.371 million and a gross profit of $705.994 million. It is also worth noting that the research and development was equal to $183.414 million, which was significantly higher than what the company reported in 2019. In my view, further investments in R&D will likely lead to new medical devices and may enhance revenue generation.

With operating expenses of $51.460 million, interest expenses of $50.151 million, and loss on debt extinguishment of $60.238 million, operating loss from continuing operations before tax stood at -$124.472 million.

Source: 10-k

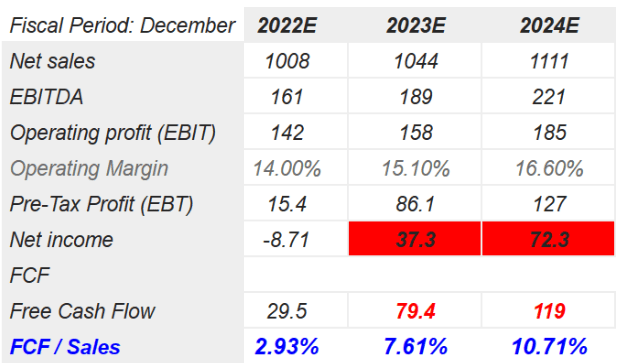

In my view, market expectations are quite beneficial. 2024 net sales are expected to be close to $1.1 billion with 2024 EBITDA of $221 million, an EBIT of $185 million, and operating margin of 16.60%.

Pretax profit would stand at $127 million accompanied by a net income of $72.3 million, 2024 free cash flow of $119 million, and 2024 FCF/sales of 10.71%. Considering that LivaNova is expected to deliver negative net income in 2022, in my view, future forecasts appear quite beneficial.

Source: S&P

I Assumed That The Company’s Strategy Will Work In New Markets And Existing Markets

In my view, LivaNova offers a consistent business model with a large number of possible alliances with public health systems and medical coverage insurance players. Considering that LivaNova is already present in a number of countries, I would expect that other insurance companies or health systems in other countries will likely sign agreements with management. In sum, operating in more markets will likely bring revenue generation.

Taking into account the recognition of LivaNova in the medical industry, I also assumed that LivaNova will successfully expand its relationships with new clients in the existing market. More agreements with neurologists, psychiatrists, medical specialists, and hospitals will likely lead to FCF generation.

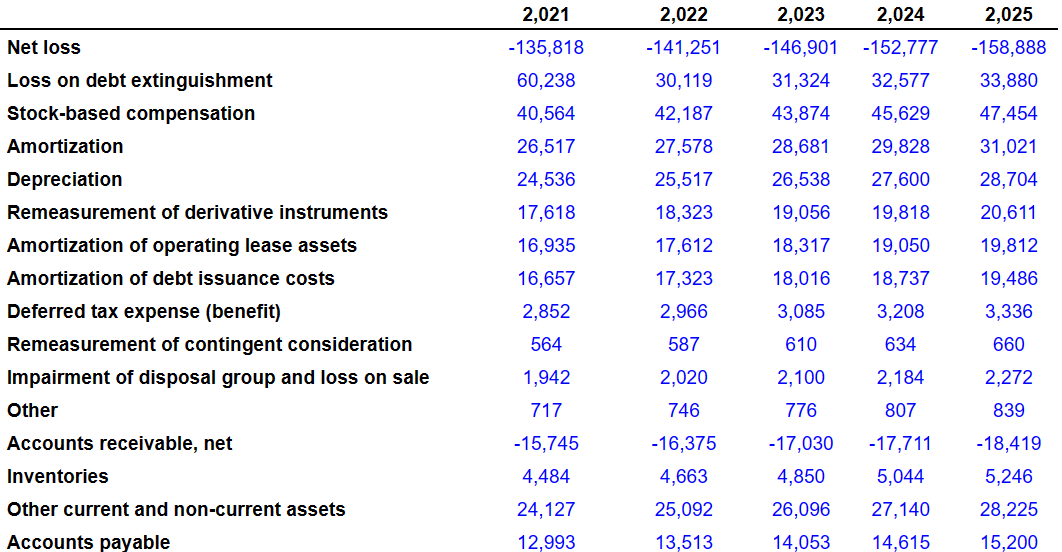

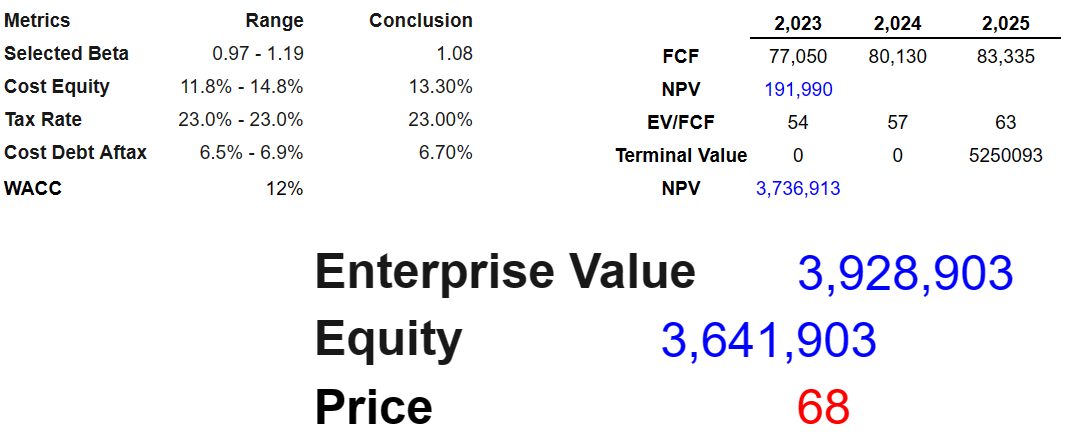

My Cash Flow Model Implied A Valuation Of $68 Per Share

Under very conservative assumptions, I assumed 2025 net loss of -$158 million along with a loss on debt extinguishment of $33.88 million, 2025 stock based compensation of $47.454 million, amortization of $31.021 million, and depreciation of $28.704 million

I also assumed 2025 amortization of operating lease assets of $19.812 million with amortization of debt issuance cost of $19.486 million. 2025 deferred tax expenses would be $3.336 million with impairment of disposals around $2.272 million.

If we also include changes in accounts receivable of -$18.419 million, changes in inventories of $5.246 million, changes in current and noncurrent assets of $28.225 million, and changes in accounts payable of $15.200 million, the CFO would be $83.372 million. Finally, with capex close to $37 million, the free cash flow would stand at $83.335 million.

Source: Internal Estimates

Source: Internal Estimates

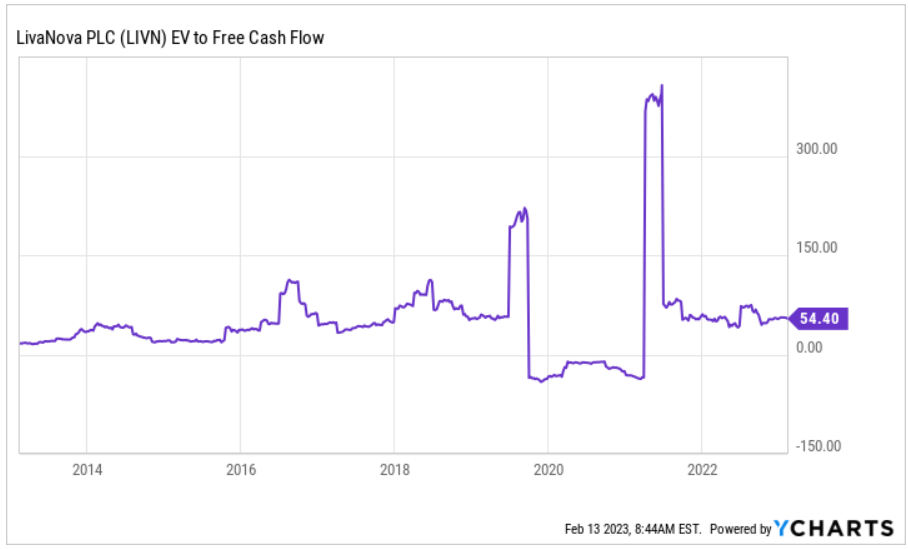

The following graph shows the EV/free cash flow multiple, which currently stands at close to 54.40x. In the past, LivaNova traded at more than 300x FCF, so I believe that assuming an EV/FCF of 63x for the year 2025 would make sense.

Source: YCharts

With a CAPM model that includes a beta around 0.97, cost equity of 13.30%, and cost of debt of 6.7%, the WACC would stand at 12%. With 2025 FCF of $83 million, $80 million in 2024, and $77 million in 2023, the NPV would stand at $191.990 million.

With an EV/FCF multiple of 63x, the terminal value would stand at $5.2 billion, and the net present value would stand at $3.73 billion. Besides, with an enterprise value of $3.92 billion, I obtained an equity valuation of $3.64 billion and a fair price of $68 per share.

Source: Internal Estimates

The company currently trades at a valuation that is significantly smaller than $68 per share. Hence, I believe that there is significant upside potential in the stock price.

Source: SA

Competitors, Risks Related To Changes In Export And Import Regulations, Or Supply Chain Crisis Could Lower LivaNova’s Fair Price

Although LivaNova currently sells its products in more than 100 countries and 5,000 hospitals distributed throughout them, the company operates in a changing market environment. In my view, the level of innovation in technology is high, and can permanently alter the course of the needs of patients. LivaNova’s competitors include both large companies with development resources and small businesses with specialized products. The largest companies under consideration are Terumo Medical Corporation, Maquet Medical Systems, Medtronic plc (MDT), Haemonetics Corporation (HAE), NeuroPace (NPCE) and Abbott Laboratories (ABT).

In my view, any sudden change in the regulatory environment in the United States, Europe, or other parts of the world could affect the normal operation of the company. Besides, LivaNova depends on a large number of external factors, such as supply chain and distribution networks, which are beyond its operating conditions and production centers. Any trouble while trying to send medical devices or increase in the transportation costs could lower the company’s FCF/Sales. As a result, I believe that LivaNova’s total market valuation could diminish.

Takeaway

LivaNova operates in growing markets like that of neuromodulation devices. The company is also launching new products like the new Essenz Perfusion System in Europe. In my view, further investments in research and development and successful commercial efforts in new regions all over the world will likely enhance sales growth. I really don’t believe that market participants did take a look at the recent guidance and the expectations of the investment community. If FCF trends higher as expected, I believe that the fair valuation could stand at around $68 per share.

Be the first to comment