Lemon_tm

The Liberty All-Star Growth Fund (NYSE:ASG) takes a fund-of-funds approach to growth investing. ALPS Advisors, the fund advisor, evaluates and selects three ‘all-star’ fund managers to manage the ASG portfolio. Historical returns for the ASG fund has been strong, although increases in interest rates have hit growth stocks hard, leading to poor YTD performance.

Looking ahead, there are signs that we may have seen a peak in growth investing, particularly as interest rates normalize to long-term averages. However, for those inclined to chase growth, ASG may be a good way to gain exposure while enjoying a high distribution yield.

Fund Overview

The Liberty All-Star Growth Fund is a closed-end fund (“CEF”) that takes a fund-of-funds approach to growth investing by allocating the funds’ portfolio to several independent asset managers that are curated by ALPS Advisors. ASG has over $300 million in assets.

Strategy

The ASG fund aims to help investors sort through the thousands of investment funds available in the marketplace and invest with the ‘all-stars’. ALPS Advisors, ASG’s fund advisor, research and evaluate a broad universe of investment funds on behalf of investors to select funds that not only meet ALPS’ selection criteria, but also complement each other in a portfolio setting.

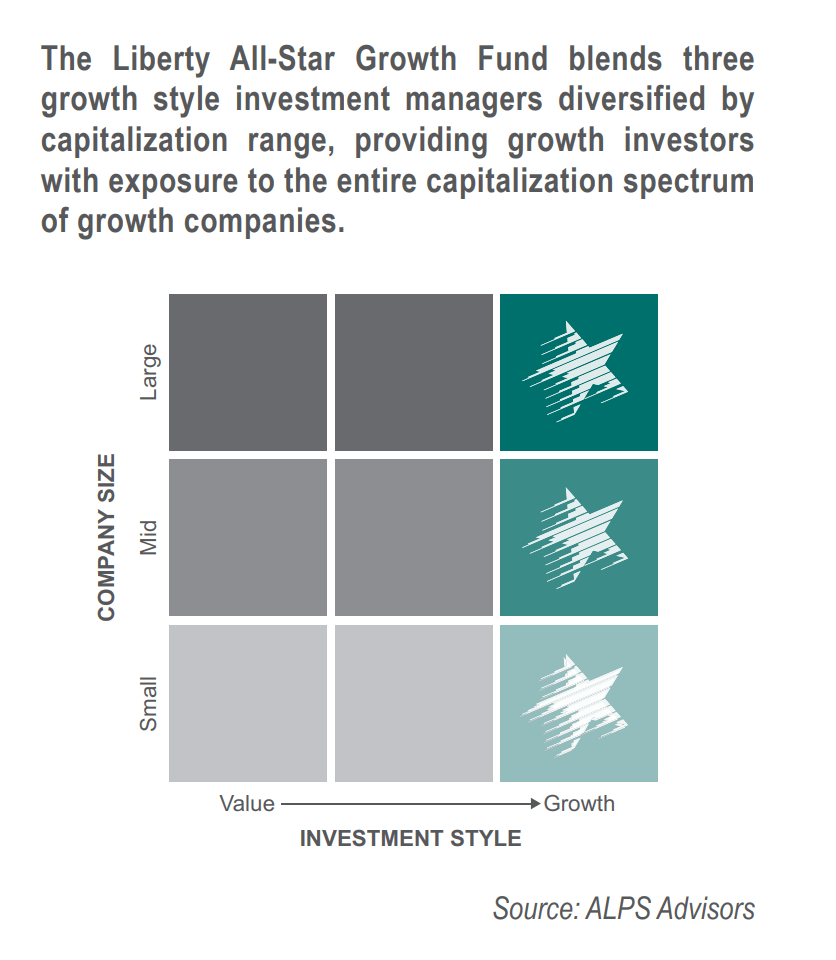

The ASG fund blends together 3 different investment managers, each specializing in a particular market cap range, within the Growth Investment Style (Figure 1).

Figure 1 – ASG growth style / market cap matrix (ASG fund marketing brochure)

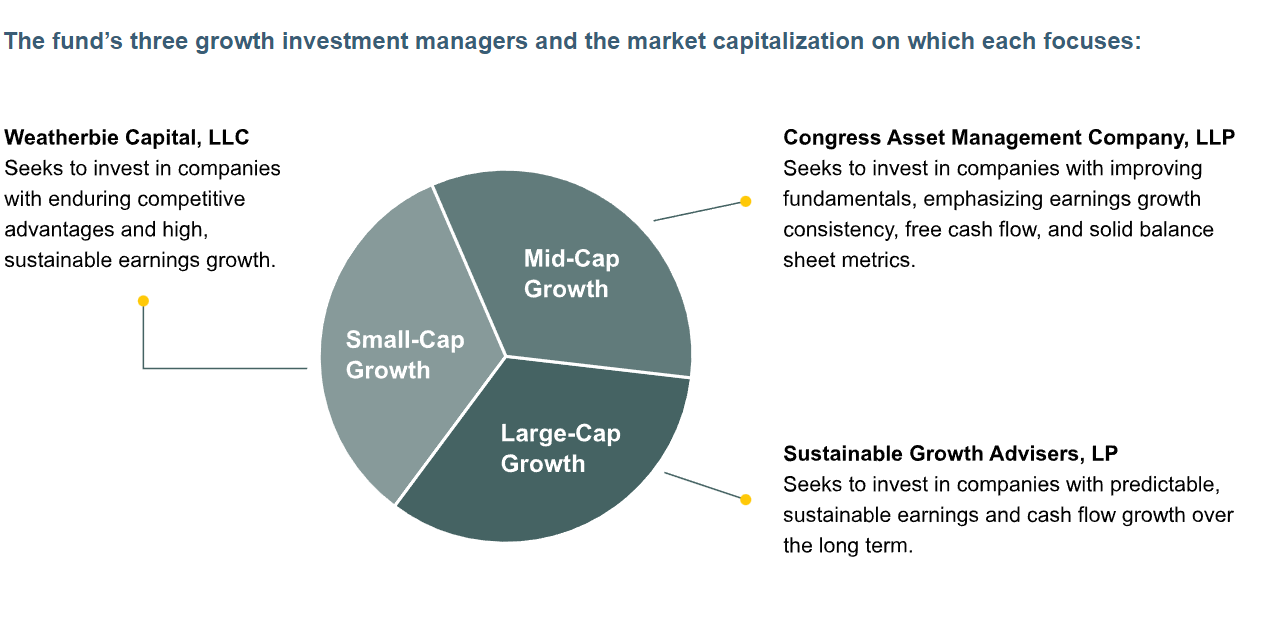

For small-cap growth, ASG has chosen Weatherbie Capital, LLC; for mid-cap growth, the fund invests with Congress Asset Management Company, LLP; and for large-cap growth, ASG has chosen Sustainable Growth Advisers, LP (Figure 2). Each manager is given a third of the portfolio to manage and their allocations are rebalanced periodically.

Figure 2 – ASG’s selected fund managers (all-starfunds.com)

Portfolio Holdings

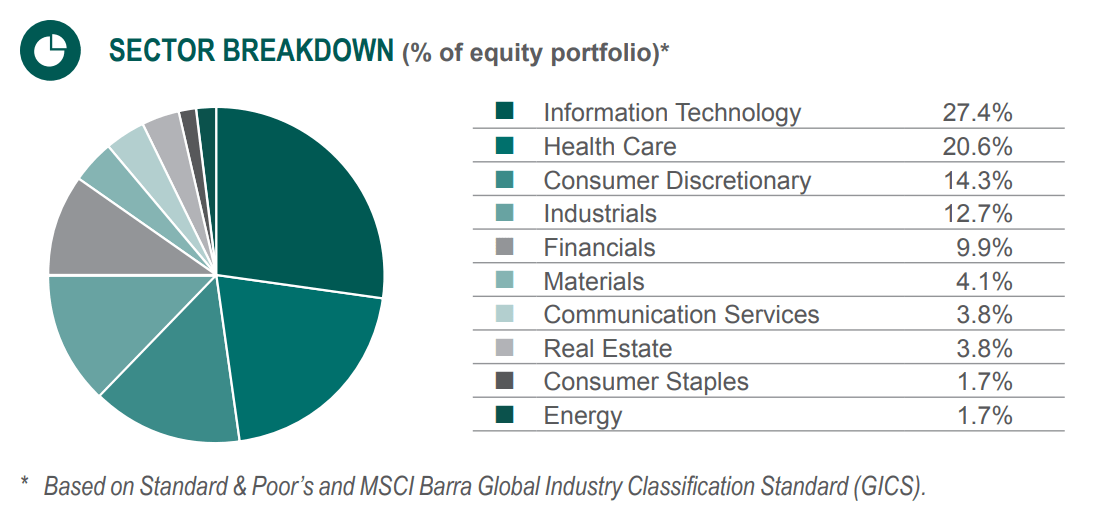

The ASG fund’s sector allocation as of November 30, 2022 is shown in Figure 3. As a growth-focused fund, it has low weightings to defensive sectors such as staples (2%) and real estate (4%).

Figure 3 – ASG sector allocation (all-starfunds.com)

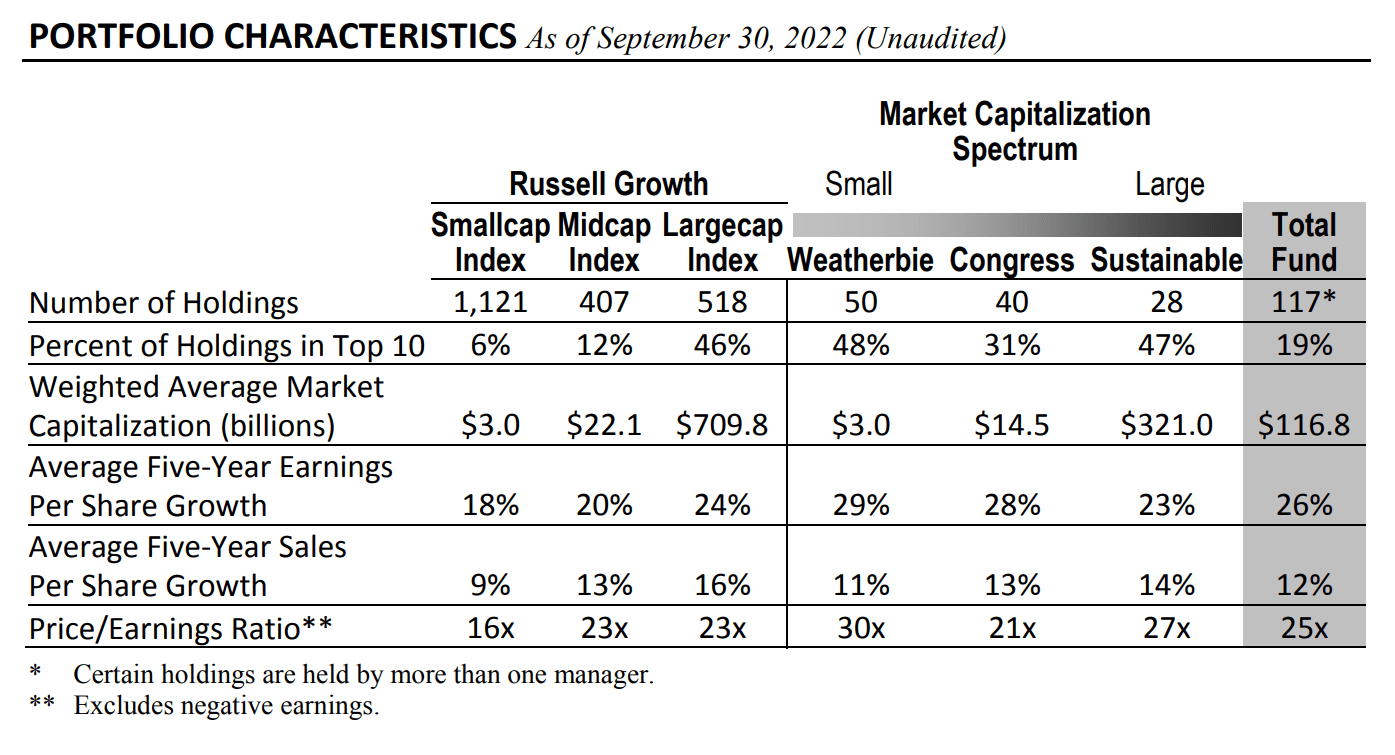

A more detailed analysis of the ASG fund’s portfolio is available in the quarterly reports. As of September 30, 2022, the ASG fund had 117 holdings across the three managers (it appears there is 1 overlapping security). Compared to their respective indices, the managers run much more concentrated portfolios of stocks that have higher earnings growth than the indices (Figure 4). Notably, the smallcap portfolio have stocks that trade at almost twice the valuation of the index (30x P/E vs. 16x).

Figure 4 – ASG portfolio characteristics (ASG Q3/2022 report)

Returns

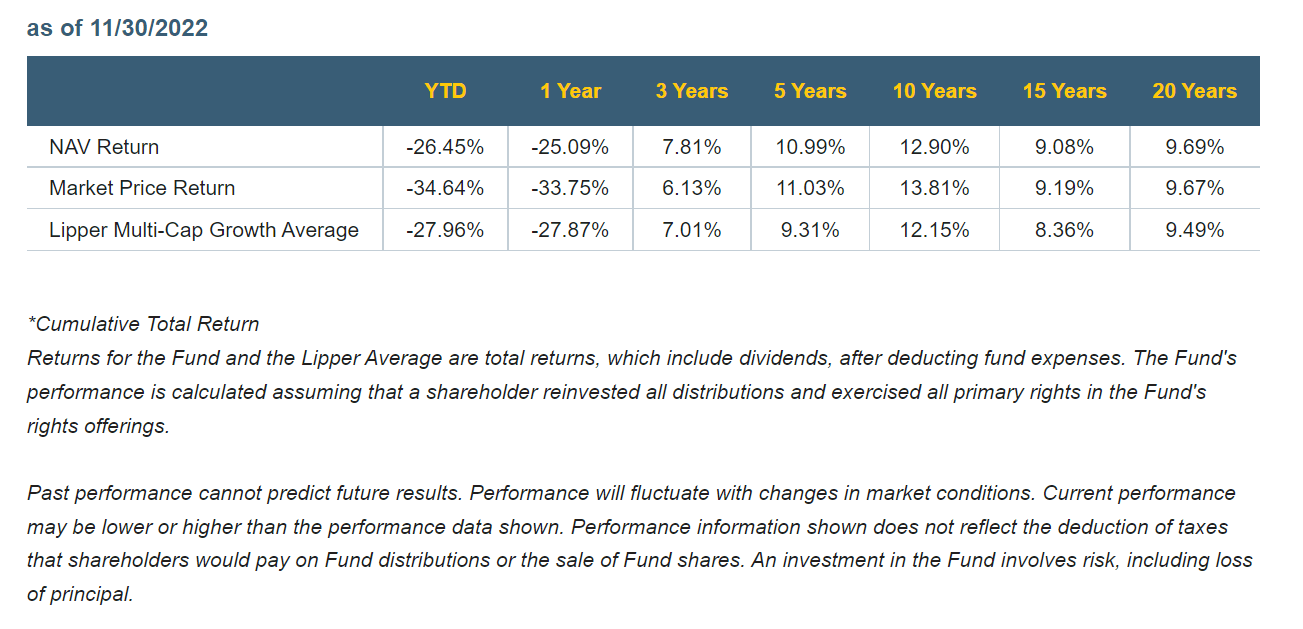

The ASG fund has delivered fairly robust long-term average annual returns, with 3/5/10 Yr average annual returns of 7.8%/11.0%/12.9% respectively to November 30, 2022 (Figure 5). 2022 has been a bad year with YTD returns of -26.5%, as many high flying growth stocks were hard hit by a rise in interest rates. Growth stocks are considered long duration assets as the companies typically have the majority of their cash flows and value far in the future. When interest rates rise, these long-dated cash flows are discounted at higher discount rates, which dramatically reduce their present value.

Figure 5 – ASG returns (all-starfunds.com)

The ASG fund has outperformed its benchmark, the Lipper Multi-Cap Growth Average, in the timeframes highlighted.

Distributions & Yield

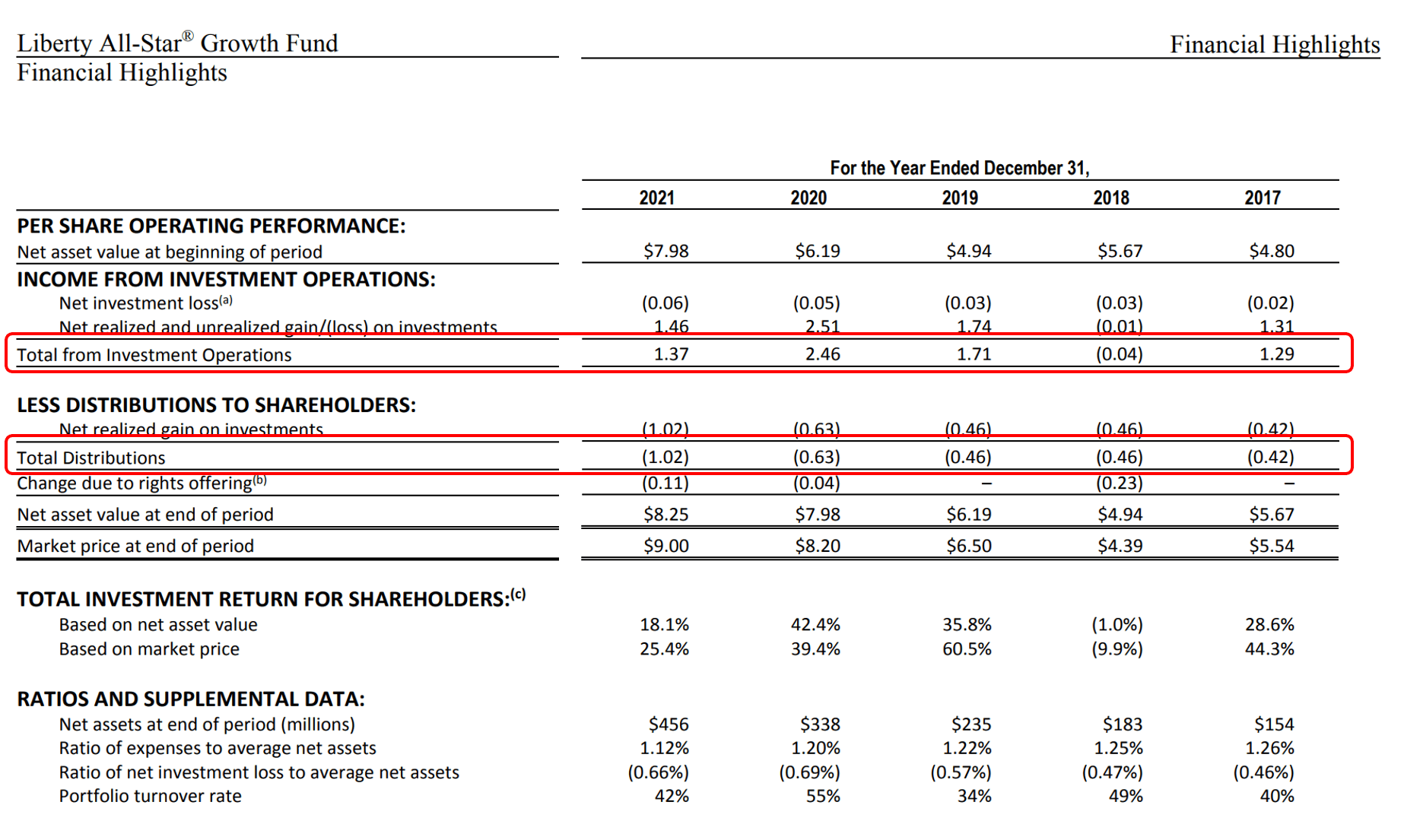

One of the main attractions of the ASG fund is its distribution yield. The ASG has paid a trailing 12 month distribution of $0.50 / share, or 10.0% yield. Investors should note that ASG’s distribution is primarily funded through realized gains (as growth stocks tend not to pay high dividend yields). This is quite different from other CEF’s that fund their distributions from net investment income (Figure 6).

Figure 6 – ASG financial summary (ASG 2021 annual report)

In my opinion, as long as the fund earns a sufficient level of returns, either through investment income or capital gains, it should not matter to investors how their distributions are funded (aside from tax considerations). Historically, ASG’s distribution appears well supported, as investment income (income plus realized and unrealized gains) totalled $6.79 / share vs. distributions of $2.99 / share from 2017 to 2021.

However, poor investment performance YTD plus $0.50 / share in distributions have taken a toll on the NAV, with the latest November NAV at $5.58, essentially at the same level as at the end of 2017. This may impede future distributions, as the fund may run out of capital gains to harvest.

In fact, the quarterly distribution has declined from $0.15 / share in Q1 to $0.10 / share in Q4 this year. If investment returns continue to be poor, investors should be prepared for further cuts in the distribution.

Fees

The ASG fund charged a 1.12% net expense ratio in 2021.

Have We Seen A Peak In Growth Investing?

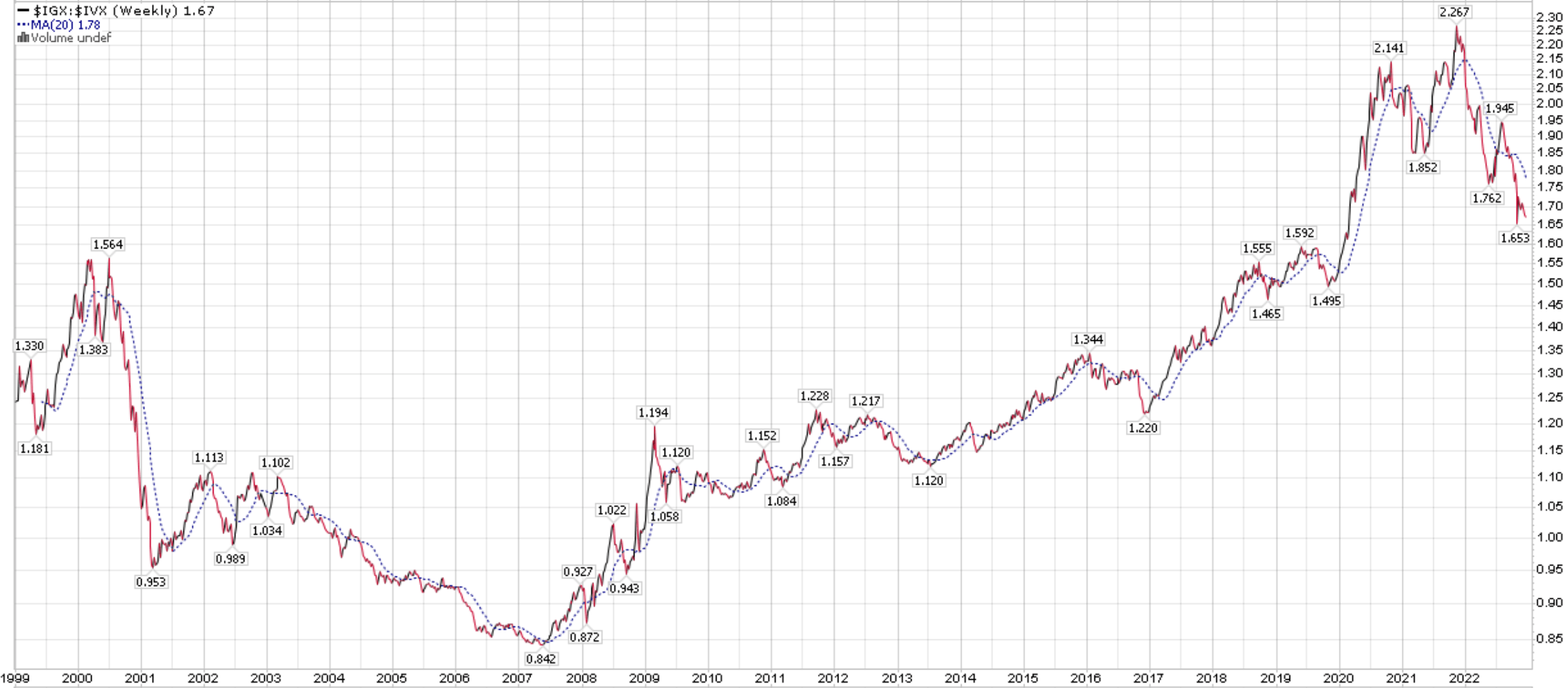

With respect to ASG, the main worry for me is whether we have seen a secular peak in growth investing, similar to the 2000 dot com bubble. If we look at the ratio between the S&P Growth Index and the S&P Value Index, we can see that after the dot com bubble, growth underperformed value for nearly a decade (Figure 7).

Figure 7 – S&P Growth vs. Value ratio (Author created with price chart from stockcharts.com)

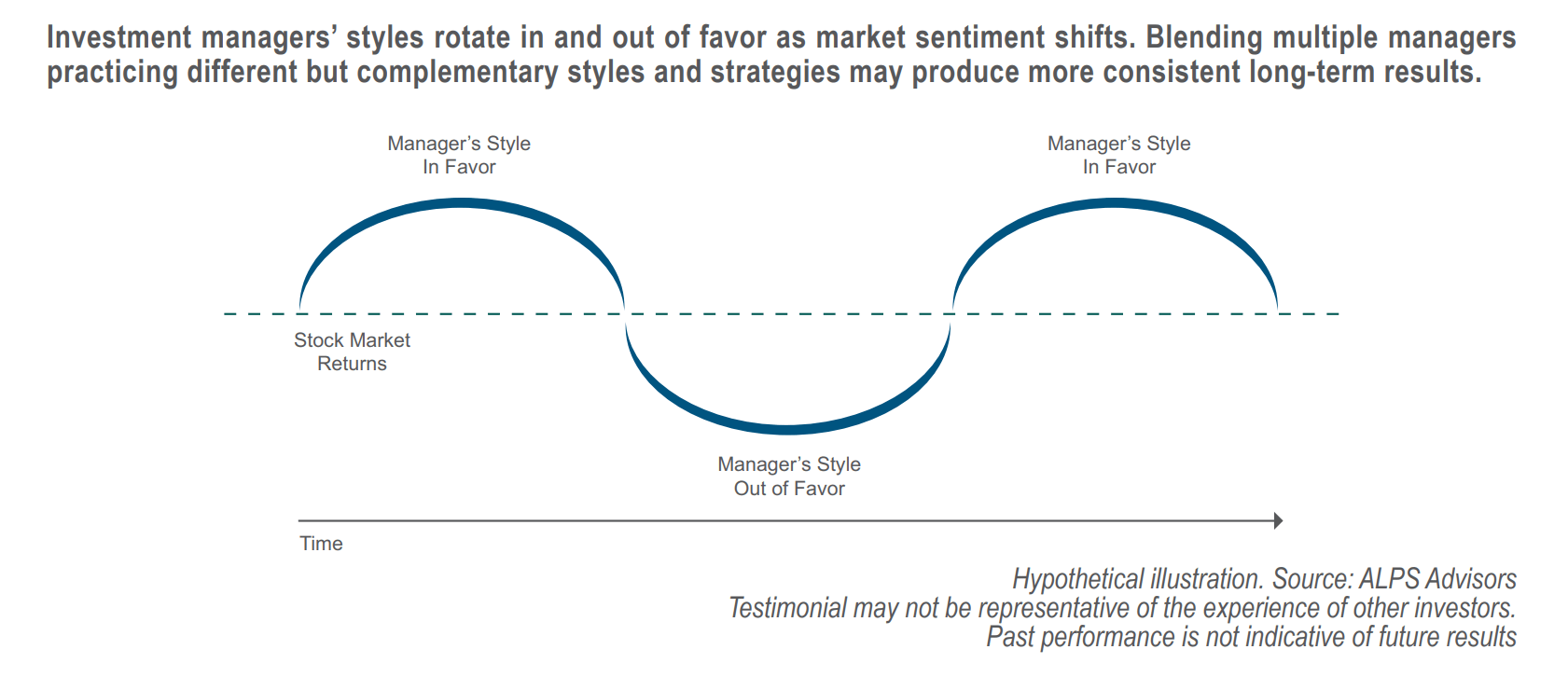

As ALPS Advisors like to say in their marketing materials for the ASG fund, investment styles come and go in favour. After a nearly 15 year period of outperformance by growth over value from 2007 to 2021, perhaps we will see a multi-year period of underperformance of growth stocks (Figure 8).

Figure 8 – investment styles go in and out of favour (ASG fund marketing brochure)

Conclusion

The ASG fund gives investors curated access to three ‘all-star’ growth managers, as selected by ALPS Advisors. Each manager focuses on a separate market-cap category: small, mid, and large-cap. Historical returns for the ASG fund have been strong, although increases in interest rates have hit growth stocks hard, leading to poor YTD performance.

Looking ahead, there are signs that we may have seen a peak in growth investing, particularly as interest rates normalize to long-term averages. For those inclined to chase growth even after a 15 year period of outperformance, ASG may be a good way to gain exposure to growth stocks while enjoying a high distribution yield funded through realized gains.

Be the first to comment