Sakorn Sukkasemsakorn

Author’s note: This article was released to CEF/ETF Income Laboratory members on December 5th.

I last covered the KraneShares Global Carbon ETF (NYSEARCA:KRBN), a carbon credits ETF, close to one year ago. In that article, I argued that KRBN should see strong, market-beating returns moving forward, as governments confront rising emissions through tightening regulatory standards, which should lead to higher carbon credit prices. Since then, the fund has posted strong, double-digit returns, significantly outperforming relative to most asset classes, including the S&P 500.

KRBN Previous Article

KRBN’s absolute performance was negatively impacted by the Ukraine War, which led to a severe economic contraction in Europe, reducing industrial production, ultimately resulting in lower carbon credit demand and prices. KRBN’s relative performance was still quite good, as most asset classes have suffered significant losses, and as the fund is only moderately impacted by most economic conditions and metrics.

In my opinion, KRBN remains a strong investment opportunity, and one that should post strong capital gains and returns moving forward. As an added bonus, the fund seems to be only moderately correlated to most other asset classes, so investing in the fund should reduce risk and volatility at the portfolio level.

Carbon Credits Overview

KRBN invests in carbon credits, a relatively niche security. Let’s have a quick look at these before tackling the fund itself. Feel free to skip this section if you are knowledgeable about carbon credits, or if you read my previous piece on these.

Carbon credits are a component of cap and trade schemes meant to reduce CO2 emissions.

Cap and trade works by ‘capping’ the amount of greenhouse gasses that can be emitted by an industry, by auctioning or allotting a limited number of carbon credits to market participants. Credits are necessary to engage in activities which emit greenhouse gases, and can be freely traded across companies. Companies with higher emissions than their allotment must either reduce their emissions, or buy credits from companies with comparatively low emissions. Companies are incentivized to reduce their emission levels to profit from selling their carbon credits. As an example, Tesla (TSLA), the largest electric vehicle manufacturer by market-cap, generates a significant fraction (sometimes most) of its profits from selling carbon credits.

Carbon credit prices are dependent on many factors.

Some of these are market-based, including supply and demand, broader economic fundamentals, and consumer demand for high-emission products. These securities are also impacted by government factors, including environmental regulations, carbon taxes and similars, and the broader drive towards reducing emissions. Carbon credits are very different from equities and bonds, so don’t expect them to necessarily perform similarly.

With the above in mind, let’s have a look at KRBN.

KRBN – Holdings Analysis

KRBN is an index ETF investing in carbon credit futures contract. It tracks the IHS Markit’s Global Carbon Index, an index of these same securities.

KRBN does not directly invest in carbon credits, but in carbon credit futures: financial derivatives whose price is linked to the price of carbon credits. These derivatives have their own set of characteristics and issues, which sometimes lead to subpar performance. From what I’ve seen, this has not been the case for KRBN in the past.

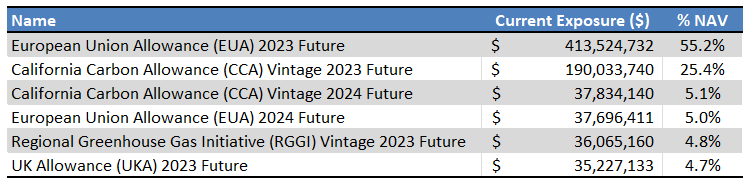

KRBN invests in carbon credit futures from around the world. The fund focuses on EU credits, due to the size of the region’s economy and credit scheme, with sizable allocations to California credits, and smaller allocations to New England and UK credits. As the fund focuses quite heavily on European credits, performance is strongly dependent on the performance of these specific securities, and on the economic conditions in the continent. Allocations are as follows.

KRBN – Chart by Author

As KRBN is a global fund, it should add credits from new cap and trade schemes as these are developed and come into operations. As an example, the fund’s UK holdings are a relatively new addition to the portfolio, as the country’s cap and trade scheme only came into effect in early 2021, once the country exited the EU.

In general terms, KRBN seems to track the global carbon credits market reasonably well, without significant issues or negatives.

KRBN – Performance Analysis

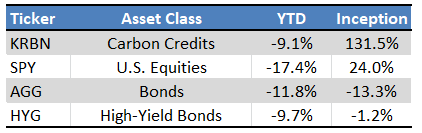

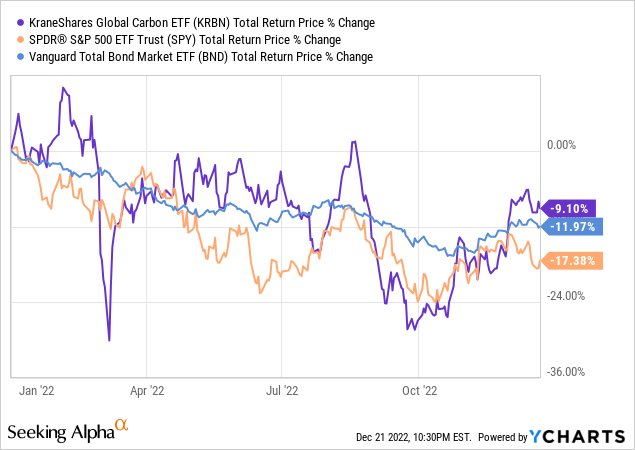

KRBN’s performance track-record is incredibly strong, although somewhat volatile.

The fund has achieved returns of over 40% annualized since inception, a staggering amount, and significantly higher than that of most relevant asset classes, including equities and bonds. Returns were driven by toughening environmental standards, including more aggressive emission limits. California has been particularly aggressive in lowering emission caps, which directly leads to higher carbon credit prices (lower supply means higher prices).

As with most other investments and funds, KRBN has seen moderate losses YTD, almost entirely due to the Ukraine War. Said war led to a spate of sanctions and significantly reduced trade between the EU and Russia, severely constraining energy supplies in the continent, leading to reduced industrial and manufacturing production. As industrial production decreases, demand for carbon credit plummets: no production, no emissions, no need for credits. Credit prices collapsed by almost 40% days after hostilities started, losses settled at around 20% soon afterwards, and have since recovered to around 10%. Very hefty losses, but moderately lower than average.

Seeking Alpha – Chart by Author

Moving forward, I expect KRBN’s performance to remain strong, for two key reasons.

First, is the fact that the European energy crisis is abating, as LNG imports, energy conservation initiatives, and a mild winter have led to full gas stockpiles. Europe has sufficient energy supplies to run their industries at full capacity, which should lead to strong carbon credit demand and prices. Broader economic conditions should improve in the coming months too, as more, sturdier, energy supply routes are established. Just this week Germany completed construction of its first floating LNG terminal, with several more in the way. Industrial and manufacturing production seems set to recover, in my opinion at least.

Second, is the fact that governments and regulatory bodies are toughening environmental standards, and taking decisive action to combat climate change. Importantly, governments are curtailing credit allowances, which straightforwardly increases their price: lower credit supply means higher credit prices.

As an example, the EU plans to reduce carbon credit allowances by 4.5% or more starting from 2024, up from 2.2% currently. Such an aggressive yearly reduction means utilities and other relevant private parties will be hard-pressed to reduce their emissions on time, leading to higher carbon credit demand and prices. The EU expects this, which explains why they will wait until the Ukraine War / energy crisis is abated before reducing their carbon allowances.

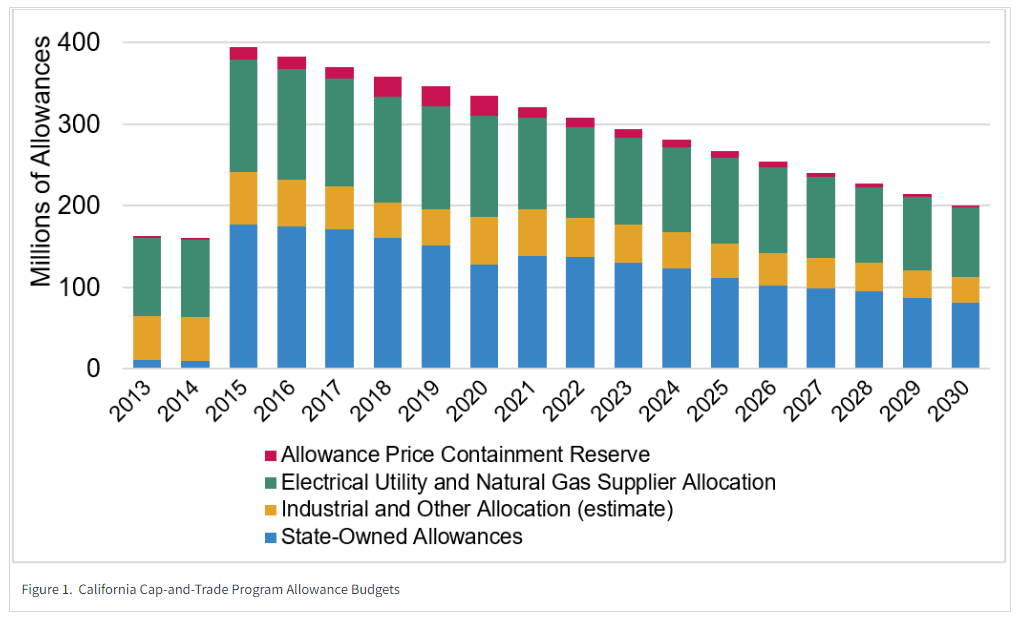

As another example, California carbon credit allowances have declined by 5.0% per year since 2021, up from 3.0% in prior years. Similar situation to the EU, with similar expected results. California is a bit more aggressive than the EU, as the state / country is much more energy self-sufficient.

California State Website

As economic conditions improve, demand for carbon credits should increase. Carbon credit supply, however, will decrease, due to regulatory action. The result should be higher carbon credit prices, resulting in strong returns for KRBN and its shareholders.

KRBN – Risk Analysis

KRBN is a strong fund and investment opportunity, but it is not one without risks. Three stand out.

Market Risk

Carbon credit prices are dependent on market, industry, and economic conditions, so there is heavy risk in these regards. Expect significant losses if economic conditions worsen, especially if the industrial and manufacturing sector is heavily impacted. The Ukraine War is the perfect example of this, with KRBN’s share price declining by almost 40% days after the hostilities started, in late February 2022. KRBN mostly recovered from these days after, but some losses remained.

KRBN focuses on EU carbon credits, and so is particularly exposed to conditions in said region.

Political and Regulatory Risk

Carbon credits are a government creation, and so are significantly exposed to government and regulatory actions. In the past, governments have generally acted in ways that increase carbon credit prices, due to environmental concerns, but this is not always the case, and might cease to be the case moving forward.

As an example, the EU actually took (temporary) steps to increase carbon credit allowances in the wake of the Ukraine War, which served to decrease prices. These were temporary measures, and the long-term trend is towards ever more stringent caps and environmental standards, but governments can always change course, and trends can always reverse. The EU could always decide that energy security takes precedence over environmental concerns, and relax credit caps and other environmental / regulatory standards. I don’t think this is terribly likely, and that is definitely not the path set by current laws and regulations, but it is definitely possible. In a broader sense, investing in a fund whose prospects are tightly linked to regulatory policies is quite risky, and investors need to be aware of these issues.

Technological Risk

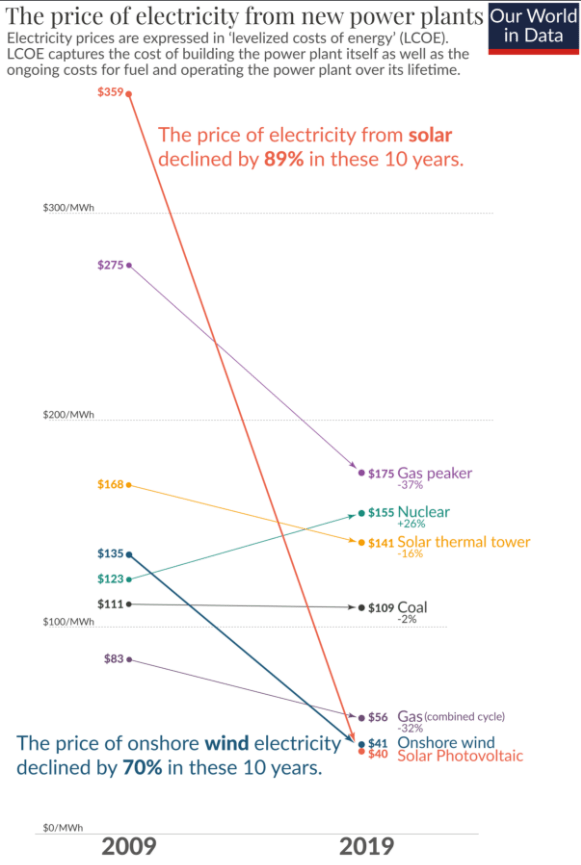

Companies with high emission levels have two choices: buy carbon credits on the market or reduce their emissions. Reducing emission levels is difficult and expensive, but becoming easier and cheaper every year. This is particularly true for solar energy generation, which has decreased in price by almost 90% these past ten years:

Our World In Data

As solar power becomes a cheaper, more competitive energy source, demand for traditional fossil-fuel energy plants decreases, leading to reduced carbon credit demand and prices. If there were to be a technological breakthrough in solar power generation which significantly reduced costs, carbon credit demand could crater, as could prices. More broadly, technological breakthroughs in other areas could, potentially, upend energy markets, significantly reducing carbon credit prices.

Other Considerations

KRBN is a relatively risky fund, but the risks are somewhat different than those of most traditional asset classes.

Equity prices are strongly dependent on corporate earnings and investor sentiment, so there is quite a bit of risk in these regards. Carbon credit prices are not directly dependent on these two factors, but there is an indirect relationship, mediated through economic conditions. A strong economy would lead to higher corporate earnings and higher carbon credit demand / prices, and vice versa.

Bond prices are strongly dependent on interest rates. Carbon credit prices are not directly dependent on these, but there is a (tenuous) indirect relationship, also mediated through economic conditions. Higher interest rates decrease bond prices, and also somewhat worsen economic fundamentals, leading to lower carbon credit demand.

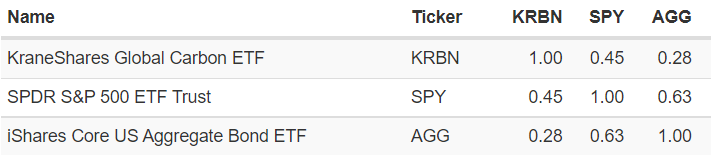

KRBN seems to be only moderately correlated to equities and bonds. Due to this, including KRBN in a portfolio should serve to decrease risk, volatility, and losses during downturns on a portfolio level. This is not because KRBN is a relatively safe fund, but because it would not necessarily go down in price when other funds or asset classes do. In theory at least. In practice, KRBN did perform as expected before the Ukraine War started.

Once hostilities started the fund went crashing down like the rest.

Still, it does seem that KRBN is only moderately correlated to equities and bonds: the Ukraine War was something of a fluke, and performance was very different before this occurred.

The math checks out too, with KRBN’s performance only moderately correlated to that of equities and bonds.

Portfolio Visualizer

Mind you, part of that positive correlation is spurious, product of the Ukraine War.

KRBN is only moderately correlated to other asset classes, so investing in the fund should moderately reduce portfolio risk, volatility, and losses during downturns.

Conclusion

KRBN is a global carbon credits index ETF. KRBN’s strong performance track-record and potential returns make the fund a buy.

Be the first to comment