oversnap/E+ via Getty Images

Thesis

While I usually avoid bringing up politics when evaluating potential investment targets, when it comes to regulatory issues the subject sometimes can’t be avoided. Just over a month ago the Federal Energy Regulatory Commission (“FERC”) implemented stringent new environmental rules that applied to both pending and future midstream projects. These rules would have hamstrung many ongoing industry projects including several of Kinder Morgan’s (NYSE:KMI) which are currently awaiting FERC approval such as the Evangeline Pass pipeline expansion and construction of compressor stations in Pennsylvania, New Jersey, Louisiana, and Mississippi. That’s not to mention numerous other potential future plans. The company was vocal in its opposition to the rule changes.

But last Thursday the rules were repealed just as suddenly as they had appeared, and FERC now says it will delay their implementation until FERC has gathered comments and studied the issue further. The sudden change is due to divergent and competing interests between the Administration’s domestic environmental goals and its foreign policy initiatives as they relate to the war in Ukraine. I believe that the FERC rules will be quietly shelved or greatly watered-down as the Administration’s foreign policy goals will take precedence. This will allow Kinder and other midstreams to pursue growth capex projects as they had done before. It may also signal a beneficial shift for the industry and we may begin seeing the regulatory pendulum swing the other way.

Geopolitical Backdrop

I had previously written about Kinder Morgan in January, recommending the stock as a good dividend play that had some upside potential given rising hydrocarbon demand. Since then, however, much has happened in the space; most of which reinforces my initial buy recommendation.

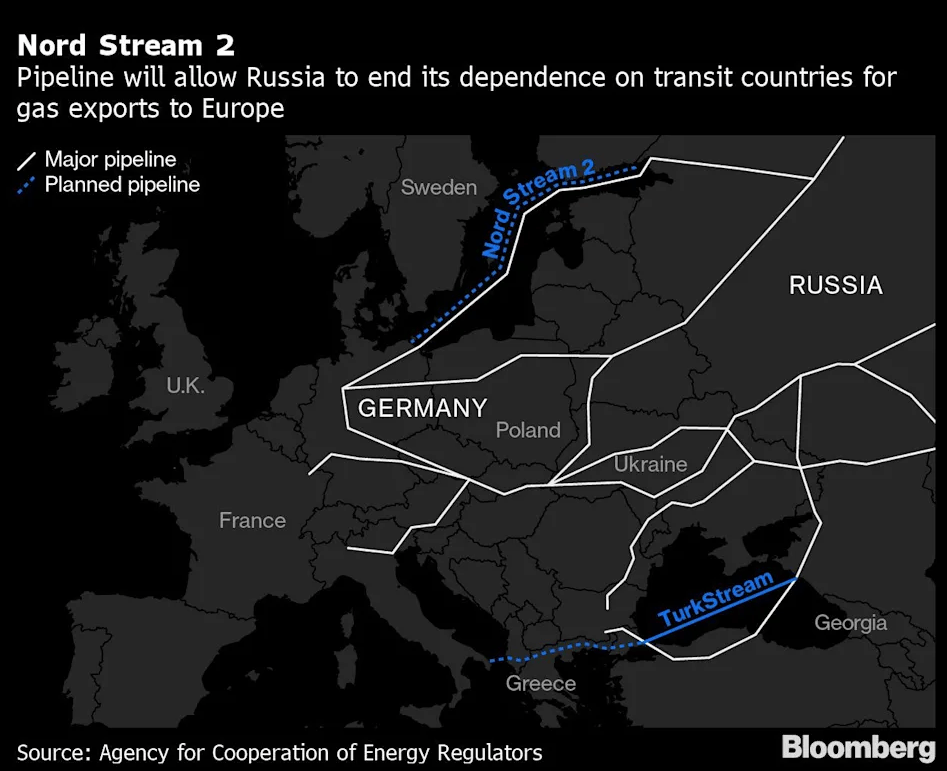

The war in Ukraine and its impact on global commodities prices has highlighted Europe’s chronic underinvestment in the sector and its reliance on Russian oil and gas. What we in the US consider to be a means of transport for hydrocarbons from point A to point B, the Russian government considers geopolitical tools to gain strategic advantage. For that reason, the Nord Stream 2 natural gas pipeline played such a pivotal role in the lead up to the conflict.

Bloomberg

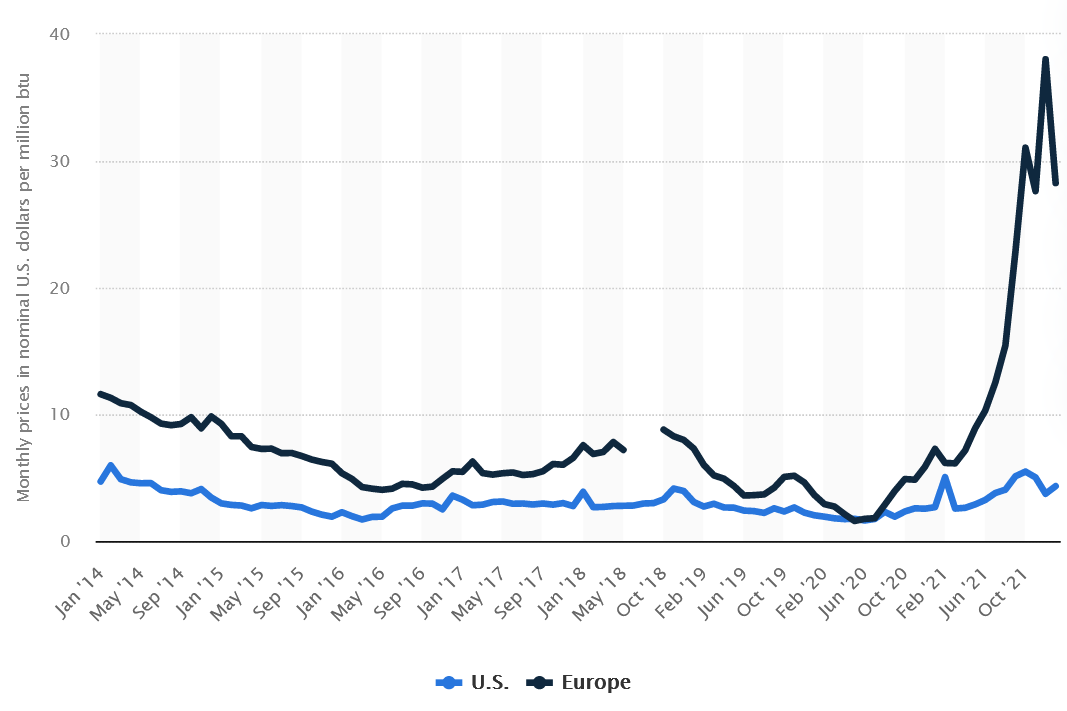

Europe’s, and especially Germany’s, sudden realization of this fact has led them to fast track the construction of LNG terminals and look for gas wherever they can find it. Germany found some success in locating supplies in Qatar but nowhere near enough to replace Russia. But even that supply will take time come online. European governments are feeling the pressure as their citizens have seen price increases that are orders of magnitude higher than have US consumers. Below is a chart of monthly US and European natgas prices from 2014 to January 2022, both expressed in nominal U.S. dollars per million British thermal units.

US and European Natural Gas Prices, USD/mBTU (Statista)

This has created a great market opportunity for US companies but has simultaneously put a tremendous amount of pressure on the Biden Administration to help the US’ NATO allies. Helping them find alternative suppliers would also rob Russia of an important source of funding and put additional pressure on Putin’s regime.

For those reasons, this past Friday the US and EU announced a new partnership explicitly geared towards reducing the continent’s reliance on Russian energy. That occurred less than a day after the cancellation of the new FERC rules. Under the plan the U.S., along with other unspecified nations, will increase LNG exports to Europe by 15 billion cubic meters this year, and increase US shipments to over 50 billion cubic meters in the coming years.

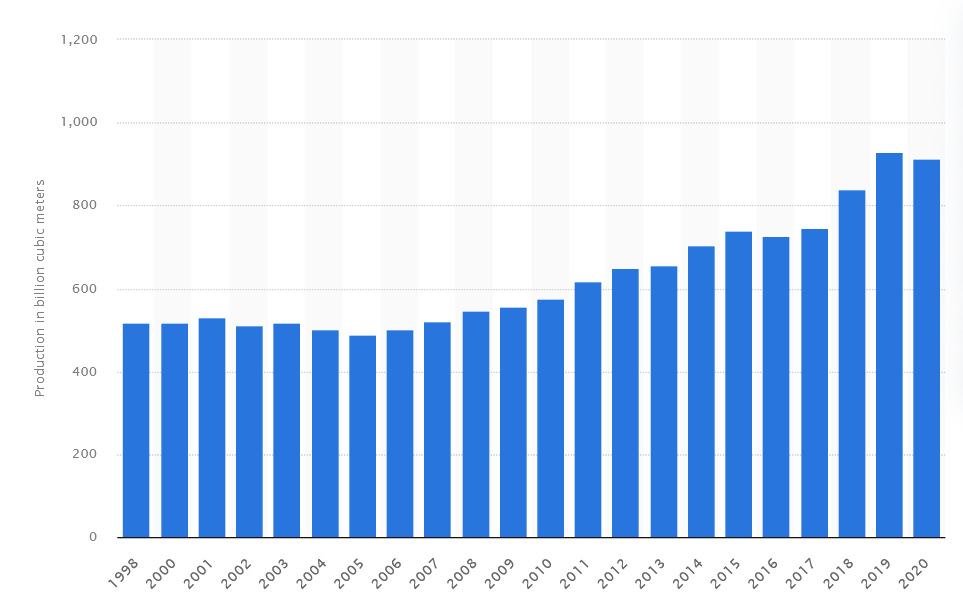

The agreement was more of a statement of intent than a detailed plan and was rather lacking in the who and how. In all likelihood, the task will fall on the US to replace a substantial portion of Russia’s supply. But doing so is currently impossible as Russia’s annual shipments were well in excess of current US spare capacity. Russia shipped about 150 billion cubic meters of gas to Europe through pipelines and another 14-18 billion cubic meters of LNG, before the onset of hostilities. To put that into perspective, total US natural gas production was 915 billion cubic meters in 2020.

US Natural Gas Production by Year (Statista)

Domestic Implications

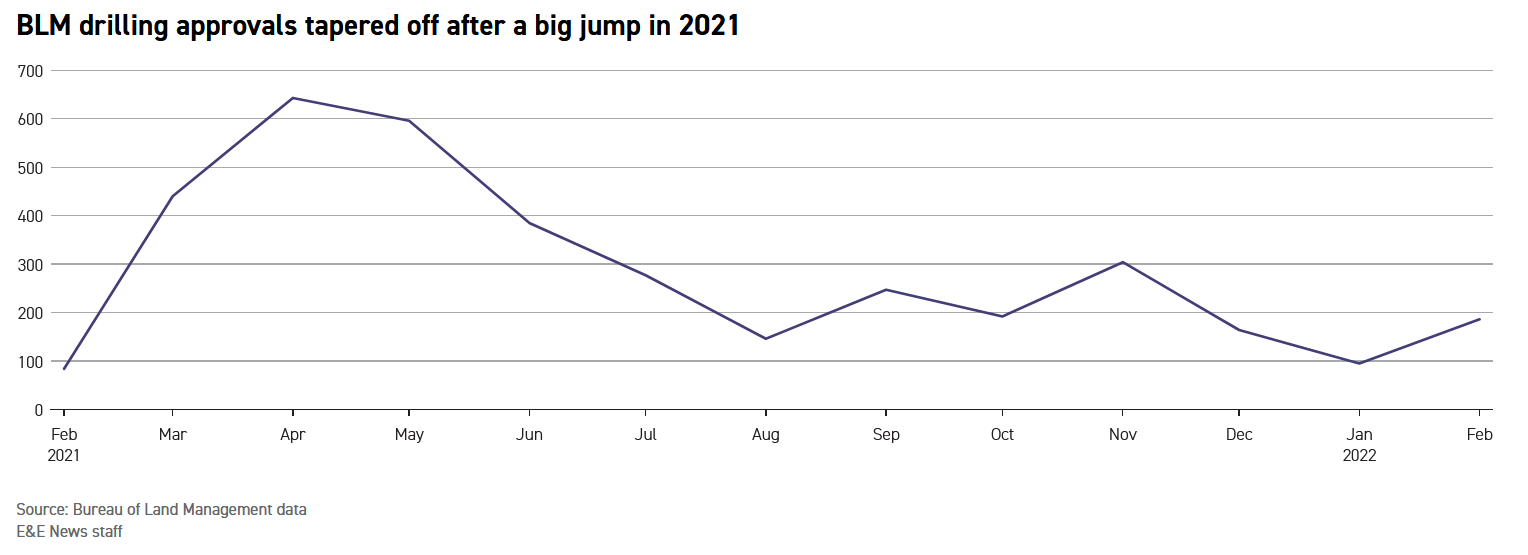

The Biden Administration came to power with the intention of promoting wind and solar energy over oil and gas. This was not a ‘campaign promise’ but rather a genuine policy plank and the Administration was true to its rhetoric as it followed through on numerous promised changes. After assuming power, it paused oil and gas leasing on federal lands until the moratorium was overturned by a judge. But even then, the issuance of drilling permits continued to slow, with the number of APDs (applications for permit to drill) plunging since last summer and remaining low right into February.

BLM Drilling Approvals (eenews.net)

FERC also began taking a much harder line towards the industry as it implemented the aforementioned rules that would apply to both pending and future projects. The rules would force the commission to begin considering how proposed gas projects and the gas that would eventually pass through them could affect climate change. And any project expected to emit 100K metric tons/year of CO2 equivalent emissions would be deemed to have a significant impact on climate change. This was a very negative development for the midstream industry.

But all of this occurred before the war began. A war that has forced the Administration to prioritize foreign geopolitical considerations over its domestic environmental agenda. And as if to go all-in on foreign policy, Biden named Putin a war criminal and this weekend called for his removal as Russian President in a major speech given to European allies.

To ensure this occurs, the Administration will need the energy complex to ramp up production. And luckily for him, midstream companies need to make growth capex investments in order to continue increasing free cash flow. So, as the old saying goes, “politics makes for strange bedfellows”.

And while the Administration will probably continue using the same old rhetoric as before and the opinions of most midstream investors towards the Administration likely won’t change, the interests of both sides are now aligned. Therefore, investors should not focus on what is said but rather the actions that are taken.

The alignment of interests can be seen in how quickly FERC repealed its rules. There was no need for legal challenges or Congress to pass a motion, the rules were simply reclassified as ‘drafts’. It’s also highly unlikely that they’ll be reinstated as doing so would essentially cap US natural gas capacity at 2021 levels; this at a time when the government needs all the capacity it can get.

Kinder Morgan

These changes will undoubtedly benefit the whole industry but I chose to focus on Kinder Morgan partly because of its size and vocal opposition to the measures. But mostly because the company is still open to building out new projects at a time when the industry is heavily focused on returning capital to shareholders. The company has come in for criticism by both analysts and investors for focusing too much on growth and not returning enough cash to shareholders. At times, those criticisms were very valid.

However, in the current environment I look for midstreams that have both a solid yield and share buyback program, but that are also looking to reinvest a portion of FCF into growth capex projects. If a midstream can find project opportunities that can be self-funded and that have an IRR significantly higher than the 6%-7% dividend yield typically paid out by the large players in the sector, then it should consider investing in the project. As long as expansion is done in a measured and reasonable way, it will allow the company to grow shareholder distributions over the longer-term.

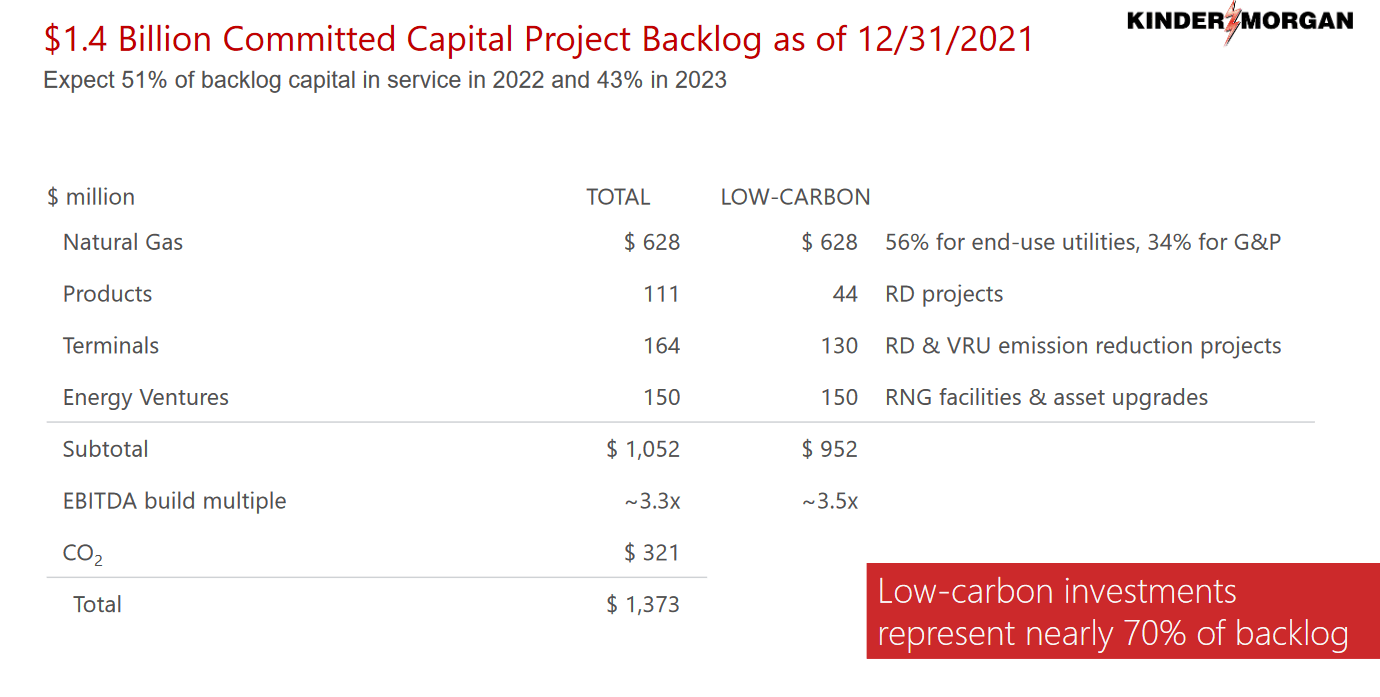

For that reason, I like Kinder as management has consistently stated that finding select high-return expansion capex opportunities is a core part of their capital allocation strategy. The company allocated ~$1.4 billion to capex spend this year and Steven Kean, Kinder’s CEO, has spoken in the past of targeting a range of $1-2 billion per year.

KMI Capex Projects (Investor Presentation)

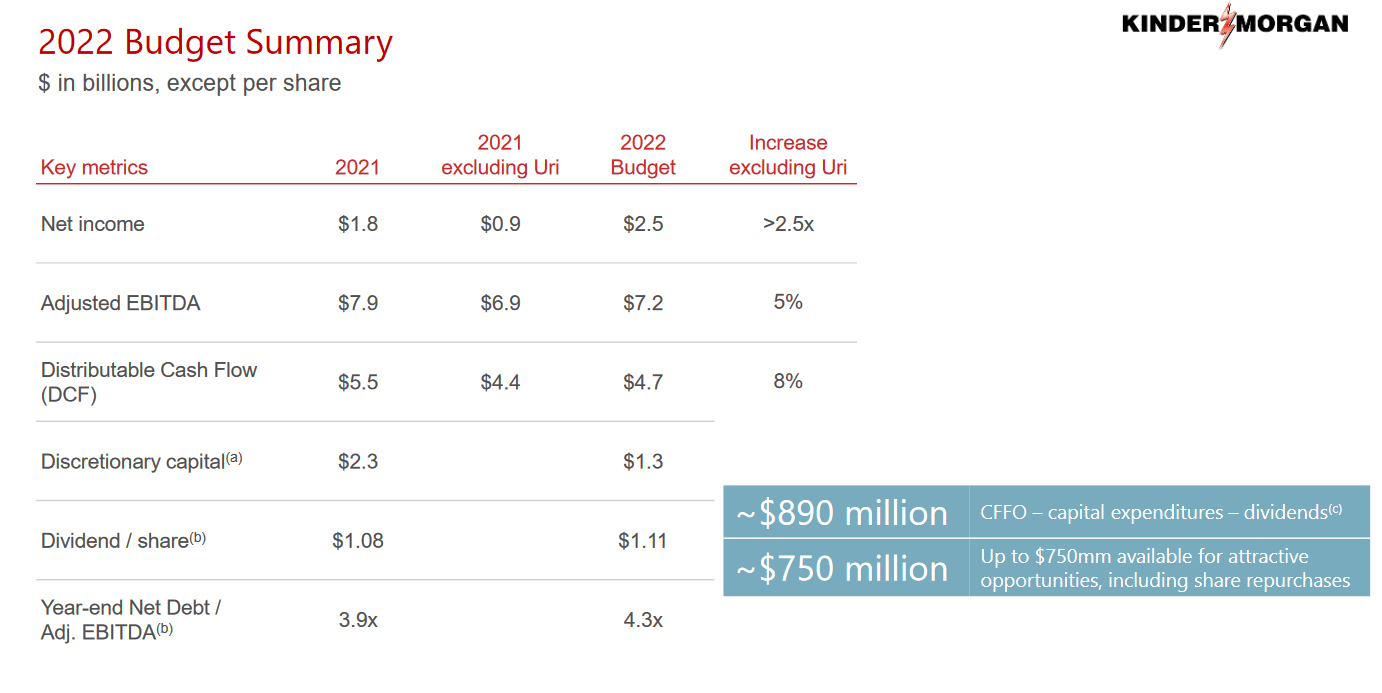

The company is doing this while still planning to increase the dividend by 3% this year, from $1.08/share to $1.11. Net Debt/EBITDA projections are for a reasonable level of 4.3x and the company even anticipates having around $750 million available for opportunities such as share repurchases.

KMI Budget (Investor Presentation)

Conclusion

The company is well-positioned for the current economic environment and as the regulatory pendulum begins to swing the other way, it is well-positioned to take advantage of any opportunities that may emerge.

Risk

The thesis would have to be reconsidered if there were ever a drastic turn in Russia’s internal politics leading to Putin’s overthrow. This is especially the case if he was replaced by a more pro-Western president. Such a turn of events would be very positive and probably help end the war in Ukraine. But the end of sanctions would lead to a shift in the dynamics of world energy markets as sanctions on Russia were dropped and energy prices would fall. This would result in the Administration’s interests no longer being aligned with those of the oil and gas industry.

Be the first to comment