onurdongel/E+ via Getty Images

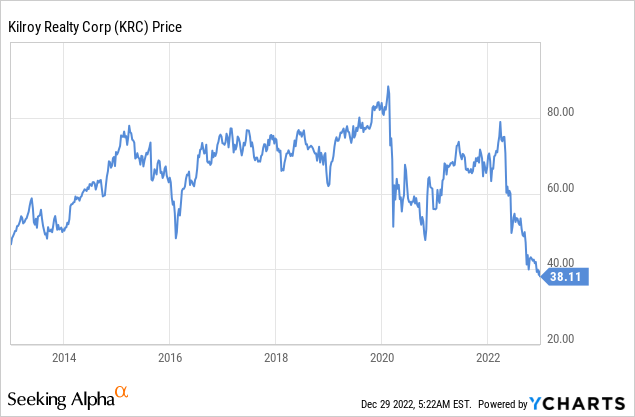

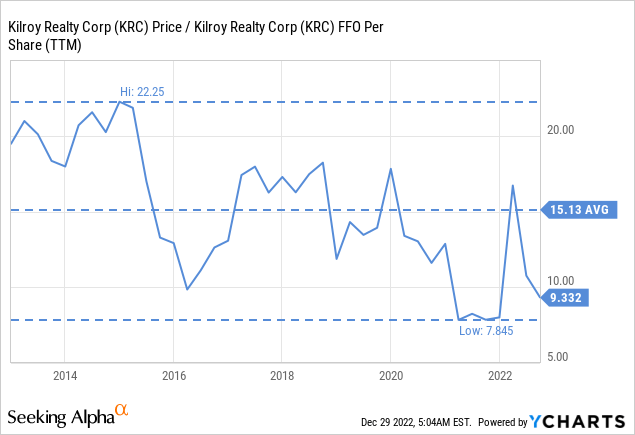

One of the highest quality office REITs in the US is without a doubt Kilroy Realty (NYSE:KRC). This has not prevented its shares, however, from being obliterated by the work-from-home trend. As can be seen below, they are now trading at a lower price than ten years ago. They are even lower than during the worst of the Covid crisis. This is not unique to Kilroy, other high-quality office peers like Boston Properties (BXP) are also trading at multi-year lows. Does this mean that it is time to buy? We are not convinced yet. While the valuation is very attractive, uncertainty remains sky high with office physical occupancy at roughly 50% on average in the main cities in the US.

Kilroy Realty does have some advantages compared to other office peers. Kilroy is a leader in maintaining a young, high quality portfolio with collaborative outdoor workspaces, best-in-class health and wellness amenities, and in general very good locations. It is also diversifying into life sciences and residential properties, but office remains the largest component of its net operating income.

Kilroy Realty Investor Presentation

Its operating metrics are still quite solid, but occupancy and leasing spreads might suffer in the future if companies start reducing their office footprints to adapt to the new work-from-home reality. At the end of the last quarter Kilroy’s stabilized portfolio was 91% occupied and 93% leased. Included in this number were three development and redevelopment properties brought into service during the quarter. These three projects were 59% occupied and leased. Despite some leasing activity taking place, the company expects year end occupancy to be at the low end of their range at approximately 91% occupied for the office portfolio, and residential occupancy is projected to stay around the current level in the mid-90% range.

Work-From-Home Trend

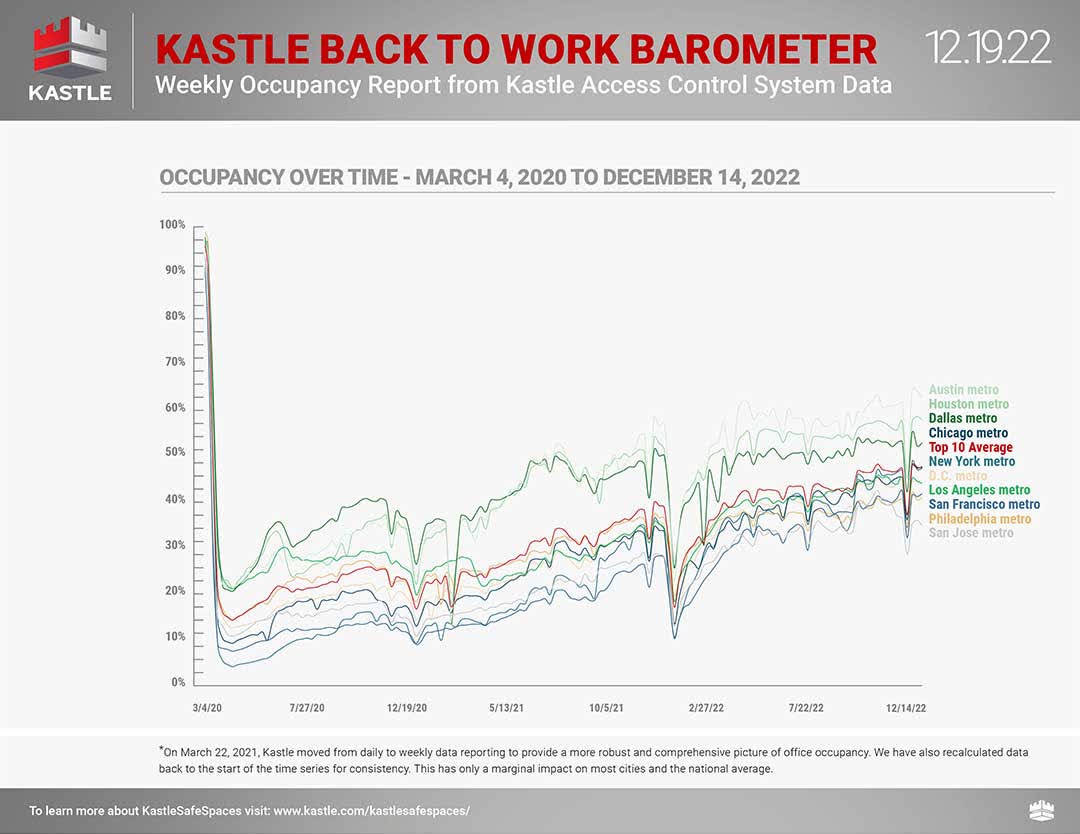

The biggest headwind for office REITs right now is probably the impact that the work-from-home trend is having on office demand. Physical occupancy remains very low compared to pre-pandemic levels, which is making a lot of companies re-think their need for office space. According to the Kastle back-to-work barometer, physical occupancy remains at ~50%, which is much lower than the >90% levels pre-pandemic.

Kastle

During the most recent earnings call analysts asked several questions trying to gauge the level of demand for Kilroy’s product. Management tried to sound optimistic, but did admit that there is a lot of uncertainty. For example, Rob Paratte who is in charge of leasing at the company admitted that things are slower than 2019 in a response to analysts:

So I think the market dynamics are just set for these larger tenants, and again, in specific markets, you are seeing activity, and when you have quality space, you will see activity. Is it slower than 2019? Absolutely. And are some tech companies sitting on the sidelines? Absolutely. But you can’t generalize that all tech is on the sidelines.

Chairman and CEO John Kilroy sounded optimistic that high-quality space will fare better compared to older and less desirable buildings, and that employers will start asking their workforce to go back to the office.

Like many, we believe that softness in the labor market will likely strengthen employers resolve around encouraging work from the office and will also resolve in employees adhering to those plans more closely.

The bifurcation between high quality space and commodity space continues to grow, which bodes well for our young and modern portfolio. According to JLL, in the third quarter, 90% of the space added to the sublease market was in older and less desirable buildings.

Furthermore, throughout 2022, nearly 50% of markets nationally set records for high watermark rents on Premier Class A properties. This includes several of our markets, such as San Diego, Austin, San Francisco. Companies that are making decisions today understand the importance of locating and modern amenitized buildings and we are seeing that.

Operating Metrics

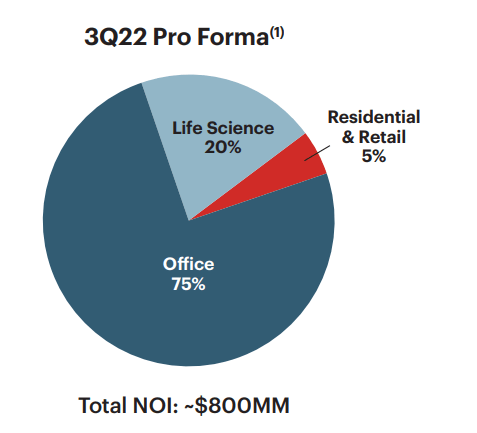

A bright spot for Kilroy has been its 1,000 luxury residential units which continue to perform well, with occupancy at ~94%. Similarly, life science demand, especially in top-tier markets, has been holding up well. Vacancy is roughly 2% in South San Francisco and roughly 2% in the Del Mar Heights and UTC regions, the company’s two biggest clusters. Unfortunately for the company, life science, residential, and retail make up only about a quarter of its total net operating income. This percentage should increase in the future however, as a significant part of the development pipeline is composed of life science projects.

Kilroy Realty Investor Presentation

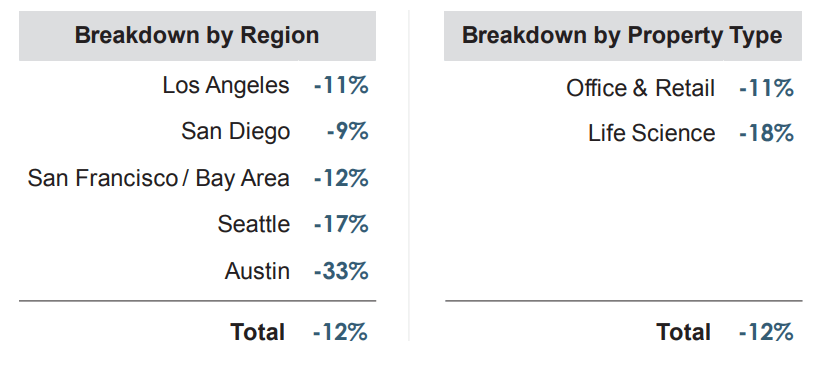

Another factor mitigating the headwinds for Kilroy is that its in-place rents are still below market rates on average. Kilroy’s in-place rents average ~12% below market rate. This is especially true for its life science properties that are on average ~18% below market.

Kilroy Realty Investor Presentation

The company does continue signing leases, having signed 390,000 square feet of leases since the end of the second quarter with an average term of eight years and average rent roll-ups of +7% on a cash basis and +27% on a GAAP basis.

Balance Sheet

Compared to other office REITs Kilroy has a very strong balance sheet. Its net debt to third quarter annualized EBITDA remained at about 6x, and the company has no debt maturities until December of 2024. During the earnings call CFO Eliott Trencher made an interesting comment where he said that the company’s balance sheet is strong enough that it could even debt fund its development pipeline if it chose to do so, although it does not mean it plans to do so:

As far as leverage, we are about 6 times now. I think what we have said in the past is not that we intend on debt funding everything, but if we did debt fund everything just to show a sensitivity that 6 times goes up to 7 times and then once the pipeline is leased, it gets back down to around 6 times.

Sustainability

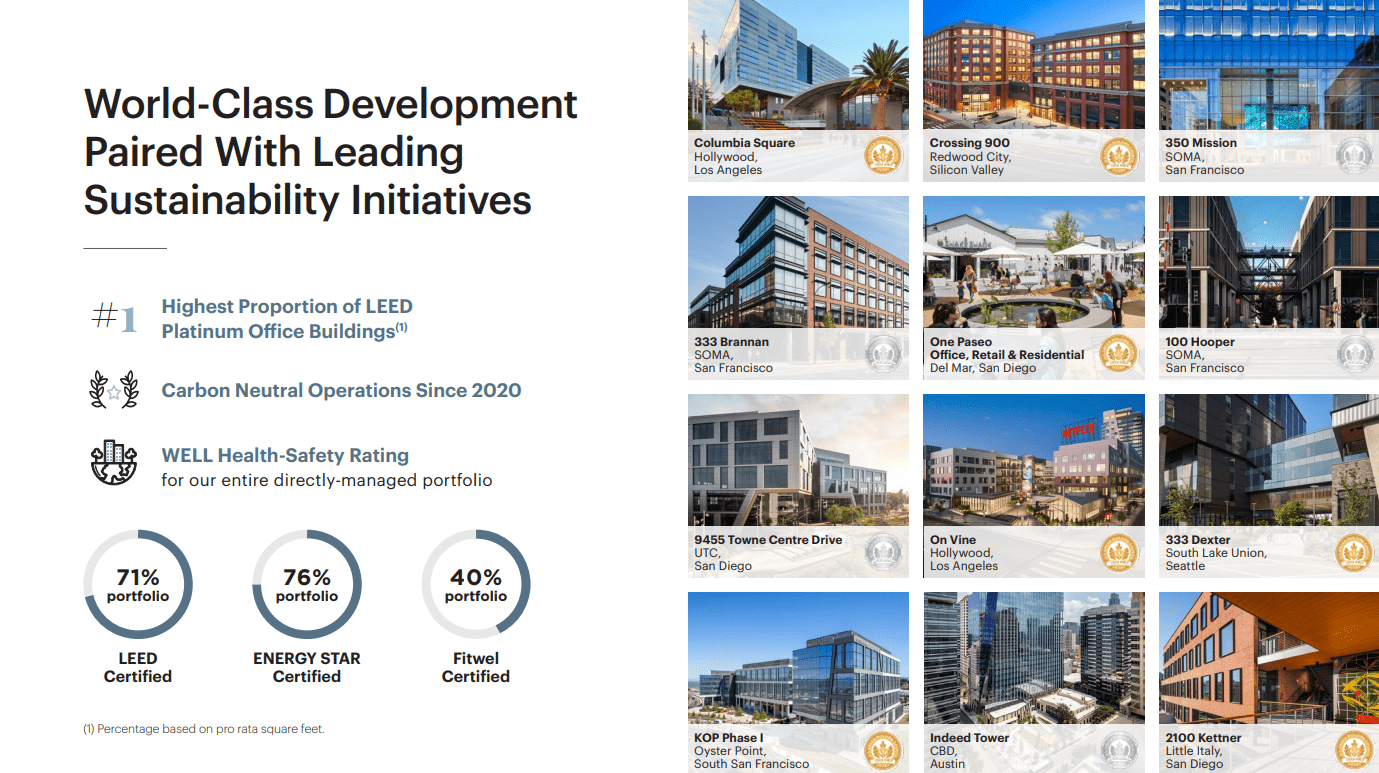

A big selling point for Kilroy is that its buildings have excellent sustainability credentials, with ~71% of its portfolio LEED certified. With increasingly more companies implementing sustainability plans, and the office being a big component of it, this is an important competitive advantage that could help attract more tenants to Kilroy’s buildings.

Kilroy Realty Investor Presentation

Valuation

While the valuation looks incredibly cheap, we would caution that there is significant uncertainty as to how much of an impact the work-from-home trend will have in future results. Updated 2022 FFO guidance is projected to range between $4.62 per share and $4.68 per share with a midpoint of $4.65 per share, which means shares are currently trading at only ~9x FFO. The dividend yield is also quite high at ~5.5%.

Kilroy Realty Investor Presentation

Shares have rarely been this cheap, with price/FFO averaging ~15x over the last ten years, making the current multiple look like a bargain. We still prefer, however, office REITs completely focused on the life science space, such as Alexandria (ARE). The reason for this is that life science is proving much more resilient to the work-from-home trend, as we analyzed in a recent article.

Risks

We believe the biggest risk for Kilroy is currently the work-from-home trend, but a recession could further complicate things for the company. We believe these risks are mitigated by the company’s strong balance sheet and high-quality properties. Still, we do believe uncertainty remains extremely high as to how deep an impact work-from-home will have on future results, and this is likely what’s significantly depressing the company’s valuation.

Conclusion

Shares of Kilroy are trading at a multi-year valuation low, despite the high-quality properties in its portfolio and its diversification into residential and life science buildings. We believe the main reason for the bargain valuation to be the work-from-home trend, with physical office occupancy remaining extremely low on average for most US cities. We are rating shares as ‘Hold’, since we believe the risk and reward are relatively well balanced. If the work-from-home headwind moderates, however, we would not be surprised to see shares quickly move much higher.

Be the first to comment