fcafotodigital/E+ via Getty Images

John B. Sanfilippo & Son (NASDAQ:JBSS) reported its Q2 earnings results recently. JBSS stock’s upward momentum has stalled for now, but it still has more room to run.

Background

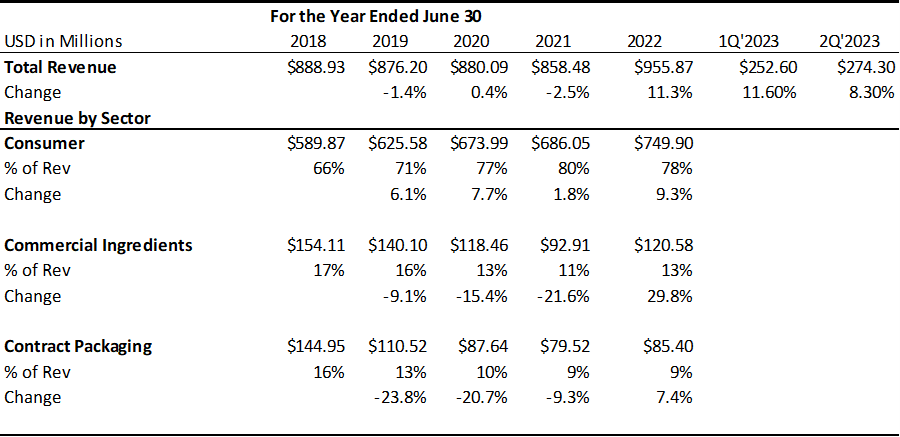

JBSS is a processor of nuts that buys raw nuts from growers, shells and processes them and either sells the processed product or packages and sells them under one of its brands (under the Fisher, Orchard Valley Harvest, Squirrel Brand and Southern Style Nuts labels) or a private label. Currently approximately 50% of its sales in 2022 is derived from Walmart and Target stores. As such, the space is competitive and pricing power with retailers is very limited. The Company is controlled by the founding Sanfilippo family out of Chicago.

Healthy Growth

All sectors have experienced strong growth in 2022. The growth rate of the largest sector, consumer sector, accelerated to 9.3%. Commercial ingredients are especially strong with a close to 30% growth compared to 2021. Contract packaging sector also finally reversed the previous declines and started to grow again. For the first two quarters in fiscal year 2023, though the growth in the second quarter is slowing down from previous double-digit rates, the overall net sales grew at 8.3%, a very solid growth rate.

SEC 10-Q and 10-K

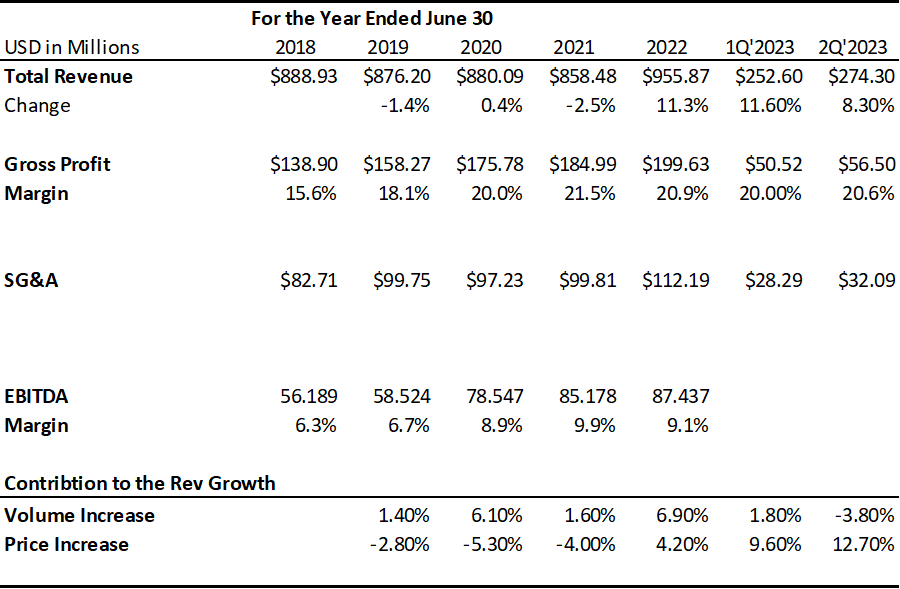

Starting in 2018, the revenue growth of JBSS was mostly contributed by the growth of sales volume, as a year of higher growth was usually followed by a year of lower growth. The prices of nuts actually declined between 2018 and 2021. The price decline changed starting 2022 (4.2%). The strong price increase continued through the first two quarters of 2023 (Fiscal Year). In the 2nd quarter of 2023, the company enjoyed a strong price growth (12.7%) in its nut businesses (even higher than the first quarter), but suffered a 3.8% decrease in sales volume.

SEC 10-Q and 10-K

Financial Implication & Valuation

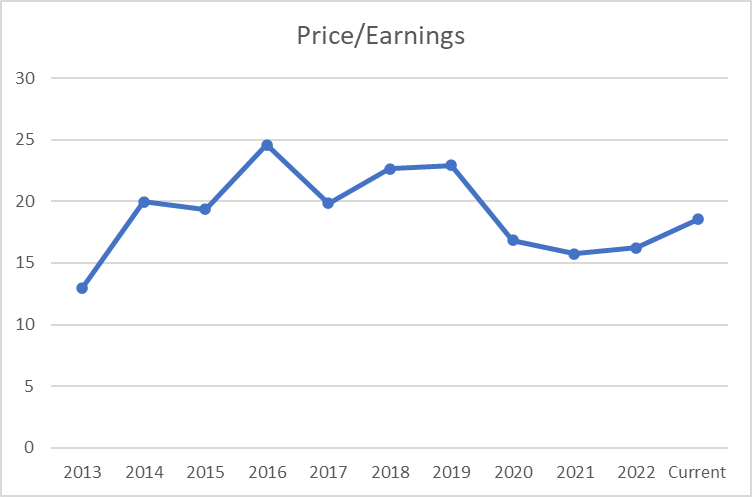

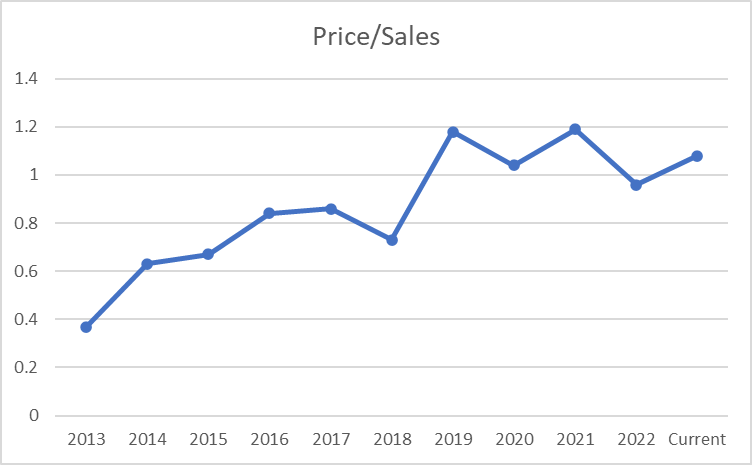

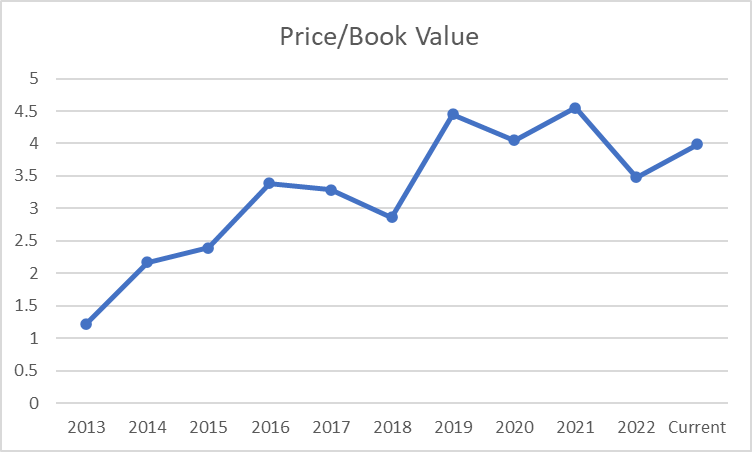

With a strong second quarter, JBSS currently has a Price/Earnings ratios under 20. This is not high compared to its historic P/E ratios, but it is higher than that in the past three years. The PE ratio was higher before 2020, but it was quite stable in the past few years. The Price/Sales ratio and Price/Book Value ratio are elevated but still below its historic heights. After a 10% price jump after the earnings report, the valuation of the company is still looking attractive at this point.

Morningstar

Morningstar

Morningstar

Future growth

In the company’s earnings report for the 2nd quarter 2023, the company mentioned “The weighted average cost per pound of raw nut and dried fruit input stock on hand decreased 24.2% year over year mainly due to lower acquisition costs for all major tree nuts.” This is a significant improvement especially compared with the 20.6% increase in weighted average cost of inventory from the previous quarter. With the company keeping its pricing power, the company’s profit margin should greatly improve in the next few quarters. Given the current trend, the forward gross margin for 2023 is estimated to be above 30% and the EBITDA.

margin is estimated to be above 10%. I assume that the forward P/E is roughly the same as the current P/E. The share price of JBSS could reach the level around $110 in the next few quarters.

Risks

- Venturing in the new sector. The company has just completed the acquisition of the Just the Cheese brand. Although which this acquisition diversified JBSS’s product offerings, it also is going to face fierce competition in the dairy market.

- The disinflation in the goods market may eventually affect JBSS’s pricing power in the consumer market.

Conclusion

The risk reward profile for JBSS seems still attractive at current prices. The company has demonstrated its pricing power in the competitive industry. The average cost of the inventory declined significantly. Its market share is intact, its competitive position is strong, and nuts are not going away. I expect the company’s gross margins and net margins to also rise in the near future. When that happens, its stock price shouldn’t be too far behind.

Be the first to comment