XiXinXing

In March 2013, Jingdong was officially reborn as JD.com. It also then adopted Joy as a corporate mascot symbolizing canine-like loyalty and reliability the brand had come to represent for its then 35 million customers. Today JD is ever more entrenched in the lives of its 588 million active users as a curator of high-quality branded products.

It also has the most paid members, over 30 million at the last count. Though the subscribers shop more frequently, spend more money and buy more expensive items, their non-PLUS peers enjoy many of the same technologically enabled efficiencies like same or next-day delivery, and have been for over a decade.

What made this possible was founder Qiangdong Liu’s decision to create a fully digitalized stand-alone logistics system. The resulting enhanced level of service has become a hallmark of JD and set a high standard for e-commerce in China, and indeed the entire world. For perspective, JD Logistics’ fulfillment infrastructure of 30 million square meters is twice as extensive as that of Amazon (AMZN) and its average days in inventory 10 days shorter.

Scale is not the only point of differentiation. The Chinese market is much more concentrated, with Alibaba (BABA), JD and Pinduoduo (PDD) accounting for nearly all digital merchandise sales: 90% compared to a 50% share of the American troika of leaders (Amazon, Shopify (SHOP) and eBay (EBAY)). A lot of it has to do with structural characteristics such as geography and demographics. But the Western ideation of e-commerce is generally more enterprise-driven whereas the Chinese model is more dynamic and customer-centric.

Competitors: So Different, Yet Alike

|

JD (FY2021) |

Alibaba (FY2021) |

Pinduoduo (FY31.3.2022) |

|

|

Primary business model (over 70% of revenue) |

Direct retailer |

Online marketplace |

Group buying platform |

|

Total revenue |

$149.7b |

$134.5b |

$14.7b |

|

Gross merchandise value |

|||

|

Revenue growth (y-o-y) |

31.6% |

22.90% |

62.1% |

|

Active customers |

588 million |

||

|

New customers |

120 million |

300 million |

80 million |

|

Gross profit |

$11.0b |

$49.6b |

$9.7b |

|

Operating income |

$530m |

$15.2b |

$1.1b |

|

SG&A expenses |

$7.9b |

$23.9b |

$7.3b |

|

Unlevered FCF |

$2b |

$10,343b |

$2.16b |

|

Capital expenditure |

$2.5b |

$8.4b |

$517m |

Source: Statista, company reports

The Original Internet Company

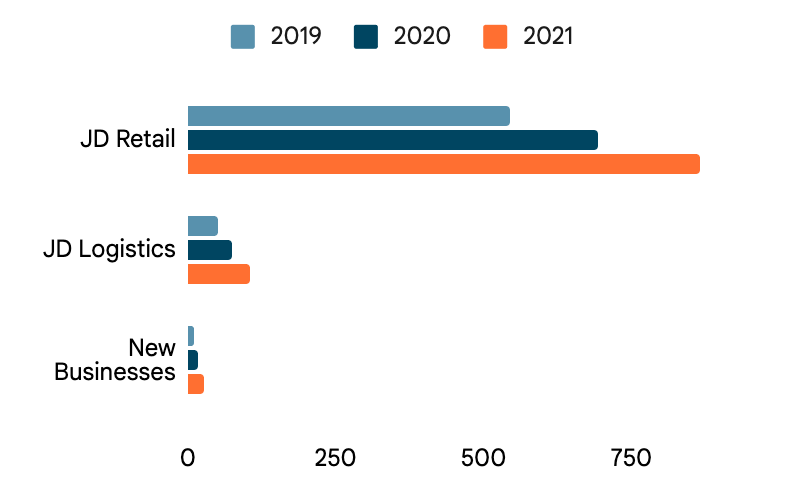

By now the main business, online retail, is a well-oiled machine in nearly every respect. Last year the segment’s net product revenue amounted to 816b yuan ($127b). While it has been growing continually in absolute value, its share of the total keeps decreasing: the contribution to merchandise sales fell from 92% in 2017 to 86% in 2021. Concomitantly gaining a bigger piece of the pie are services encompassing marketplace, marketing and logistics. Logistics, in particular, is the most rapidly growing source of revenue.

JD Logistics, which now trades separately in Hong Kong with JD the group owning 63% of shares, is servicing more external clients than ever, more than 300,000 last year. The proposition it offers is hard to resist: 90% of orders processed through its network are delivered on the same day or the day after the order is placed (or within 30 minutes for JD Health), which in a country as vast and populous as China is a true feat of operational efficiency. Offering the same logistics and supply chain efficiencies to other firms is a fast-growing business with huge potential.

Net revenue, yuan bn

Company reports

Seemingly on the other end of the spectrum are newer ventures spawned from JD’s attempts to capture the undertapped market in farther-flung locales. From this year, the group has started reporting on Dada, a local on-demand delivery and retail platform, of which it owns 52%. Although the Nasdaq-listed company is barely moneymaking at this point, there is reason to believe that it will come through soon enough. One area of growth Dada is helping JD diversify into is e-grocery, a vertical of the offline-to-online trend that has taken off in China. And in that Dada’s own crowdsourced delivery network is supplementing JD Logistics’ and extending instant delivery to ever more categories of products.

Notable among New Businesses is Jingxi, but not for the best of reasons. Jingxi — JD’s group-buying app that targets price-sensitive consumers in smaller, or lower-tier, cities and rural areas (as opposed to JD’s home turf, top Tier 1-2 cities) — is getting reorganized. Competition with the leading incumbent Pinduoduo has proved too much, so it is being downsized from 80 cities originally to just two: Beijing (where it has managed to break even) and Zhengzhou (where it is testing a new distribution model).

However, JD is not abandoning the ship because lower-tier cities are anything but sinking. Fueled by the rise in population and disposable incomes, discretionary spending in these cities has been booming. A boon for JD is the consumers’ growing proclivity to choose quality over value. The company’s strategy is now shifting to upgrading logistics and other product related services, to use fulfillment efficiency and customer experience as differentiation, instead of conventional but unsustainable incentive marketing.

The Fall and Rise of China Inc

Recently, JD has been showing welcome maturity, axing loss-making projects, for the sake of “operating stability”. (Aside from Jingxi, New Businesses has a number of them: last year, they collectively made an operating loss of 11b yuan, or $1.6b, on net revenue of 26b yuan, or $4.1b.) This is a consequence of well-known political and economic dynamics. The government crackdown that started in late 2020 and eased only earlier this year took a serious toll on Chinese big tech. In certain ways, the state is expected to continue directing the development of technologies, albeit covertly — which is a fresh challenge for JD and peers to deal with.

Other forces tempering entrepreneurial ambitions were China’s disruptive zero-covid policy and the homegrown property crisis. Both have come to an end but the economic outlook remains cloudy. For one, the damage has been done. Growth stalled mid-year, GDP barely eked out 0.4% in Q2; the conservative forecast for 2022 is 3.2%, to be the second slowest growth year for China in over four decades. Consumption was one of the hardest hit, plunging to 5.7% in Q1 and then 1.5% in Q3. Retail sales fared worst, recording negative growth in some months.

JD started feeling the pain already in late 2021 which took net margin back into negative territory. The full year closed with a net loss of 4.5b yuan ($701m), down from a positive 49b yuan the previous year. From the beginning of the year to 31 October, the US listed stock fell about 40%; the MSCI China Index slumped to a 10-year low.

However, in the last couple of months Chinese shares have rebounded on foreign investor optimism around economic reopening and policy reforms ranging from COVID to real estate and ties with the US. JD has regained more than 50% (also because of strong Q3 results), making up for the earlier year-to-date loss.

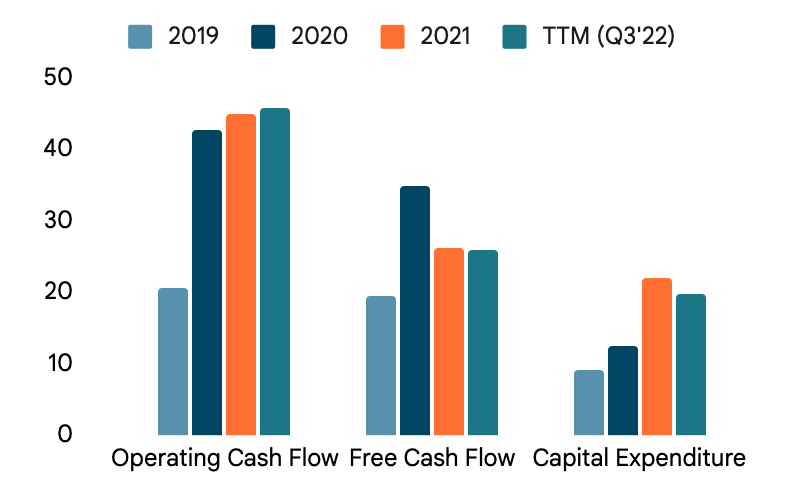

For all the tribulations, the company’s balance sheet has stayed consistent and stable. JD maintains a healthy cash flow and manages its debt prudently. Cash comfortably exceeds total debt and operating cash flow outstrips net income. This cash buffer, which is practical proof of solid metrics, has supported the business during the worst of times. Importantly, JD continues to employ capital in areas which promise the most return: property for pure cash generation as well as expanding logistics infrastructure as a competitive edge.

Cash and capital, yuan bn

Company reports

Is JD a buy?

China’s biggest e-commerce player by revenue, JD is still growing at a brisk pace. The new engines of growth are marketing and logistics. The two in combination, with technology as a binding agent, are being used to attract more customers from the country’s bevy of thriving lower-tier cities.

Online retail there and the rest of China is getting increasingly crowded. It now includes non-retail types like social media and live-stream platforms, so the incumbents like JD and Alibaba have been feeling the pressure. But at least in the case of JD, the expansion strategy is being redesigned — by going back to the basics.

The most salient fact about JD is trust (in brand and quality), still a big sell for consumers in China. The sophisticated logistics network is another compelling draw for savvy shoppers who value efficiency at no extra charge. JD, therefore, wields a winning combination of scale (most surface area), superior quality and low prices.

Although JD, like many others, has experienced a strong recovery in share price at the end of 2022, I believe there is room to grow. Its Price/Sales of 0.6 is below Alibaba’s 1.9 and Pinduoduo’s 6.1. Its Price/Cash Flow, which may be more telling in JD’s case, of 13.6 is below the five-year average of 17.5 and the Consumer Discretionary median.

China’s struggle to work through rampaging COVID in the immediate future and fears of economic overheating further down the road may dampen the enthusiasm somewhat. But neither will change the fundamentals which make JD a long-term holding.

Be the first to comment