guvendemir

We have seen a lot of positive momentum for defense stocks this year and the situation in Ukraine as well as tensions with China are the obvious reasons for that. In this report, I will focus on the defense budgets in North America and Europe to see how strongly defense budgets are trending or not.

For this report, I will be using the evoX Defense Contracts and Budget Monitor which contains over 5,000 defense contracts for 15 companies, including companies that were acquired over the years, and defense budgets for over 70 countries.

How Strong Did Defense Outperform?

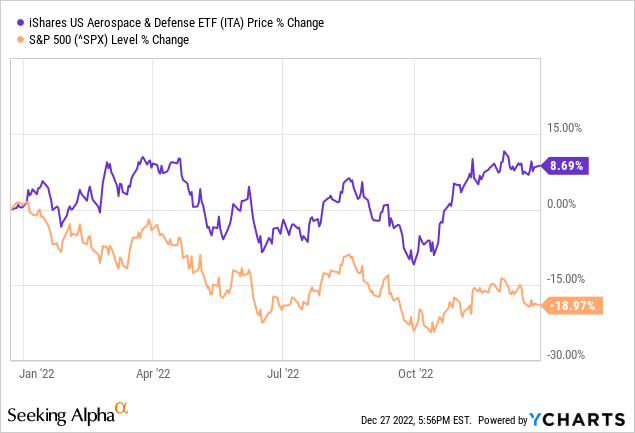

First looking at how Defense names performed, we see that the outperformance is clear. The iShares U.S. Aerospace & Defense ETF (BATS:ITA) returned 8.7% year-to-date while the global markets lost 19%.

|

Ticker |

Name |

Weight (%) |

Covered by evoX Defense Contracts Monitor |

|

RAYTHEON TECHNOLOGIES CORP |

21.23 |

✅ |

|

|

LOCKHEED MARTIN CORP |

16.39 |

✅ |

|

|

BOEING |

7.72 |

✅ |

|

|

TRANSDIGM GROUP INC |

4.55 |

❌ |

|

|

GENERAL DYNAMICS CORP |

4.5 |

✅ |

|

|

HOWMET AEROSPACE INC |

4.46 |

❌ |

|

|

NORTHROP GRUMMAN CORP |

4.43 |

✅ |

|

|

TEXTRON INC |

4.34 |

✅ |

|

|

L3HARRIS TECHNOLOGIES INC |

4.23 |

✅ |

|

|

AXON ENTERPRISE INC |

3.55 |

❌ |

|

|

Total |

75.4 |

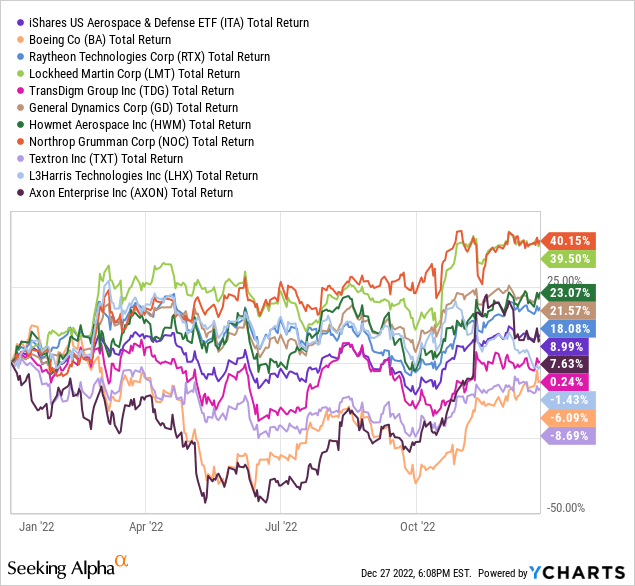

The top 10 of the 35 holdings of ITA represents over 75.4% of weight in the ETF. With some exceptions, these names are also covered in our contracts monitor, so we have a fairly representative base that tracks defense contracts.

Looking at the performance of these 10 names, you could have missed the opportunity if you were invested in the wrong names. However, I believe that Northrop Grumman, Raytheon, Lockheed Martin and General Dynamics should be the core of any Defense Portfolio, and with those names you would have outperformed the ETF easily. So, purchasing the ETF rather than hand picking stocks is something that would significantly lower your year-to-date or 1-year performance. With a weight of nearly 8%, Boeing would be dragging the ETF performance down quite a bit as would Textron and TransDigm, although the latter two companies have lower weights in the ETF.

So, ETFs are nice but you would have been better off analyzing individual companies and make purchases accordingly.

The Defense Budget Expansion Thesis

Right now it is easy to build a thesis for investment in Defense stocks. Add the global tension to the mix with a major role for Russia, China and Taiwan and you can draw the easy conclusion that the US and Europe have to respond with higher defense budgets, especially since Defense budgets have been under pressure in recent years.

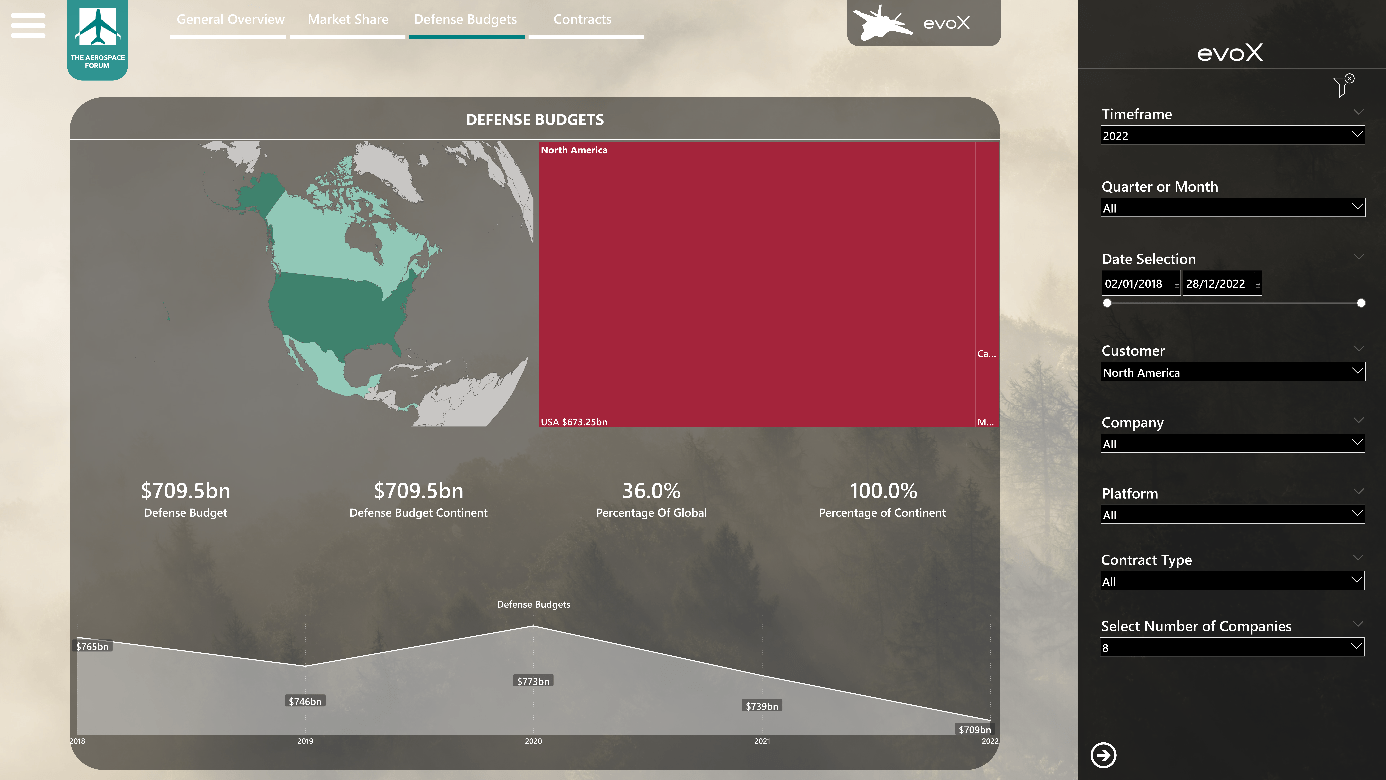

Defense Budgets North America and Europe (The Aerospace Forum)

So, let’s put that to the test. What did we do? Well, very simple. I selected North America as well as Europe in the monitor and selected the year 2022. The results are actually somewhat underwhelming I would say. The defense budget stands on $1.1 trillion representing 55.6% of the global budget. As a reference, in 2018, North America and Europe represented 55.8% of the global budget. So, while it seems defense budgets are exploding in key geographic areas for defense stocks that is really something for next year. Reality is that as threats grow across the globe, North America and Europe have steps to take and a big step should be taken next year, but from that point on it takes a while for budgets to translate to additional sales. So, I would say expect better sales from 2024-2025.

I have also translated the budgets to 2022 dollars and that is where see a painful thing. While in response to the war in Ukraine we were made to believe that defense budgets were growing fast, the fact is they are not. Any hike in defense budgets for 2022 is basically offset by inflationary pressures. That means that as long as budgets are not increasing in line with inflation, expansion of purchasing power is rather limited.

Defense Budgets North America (The Aerospace Forum)

Now let’s look at North America. It’s actually not a pretty picture for North America. Adjusted for inflation, over the past 5 years, purchasing power has contracted by 7.5% and by 8.3% measured from the top and this is something to keep in mind. While defense contracts are expanding, we should not cheer about that because we should be looking for defense budgets expansion at a rate higher than inflation rises and we are not seeing that in North America which mostly reflects the US defense budget.

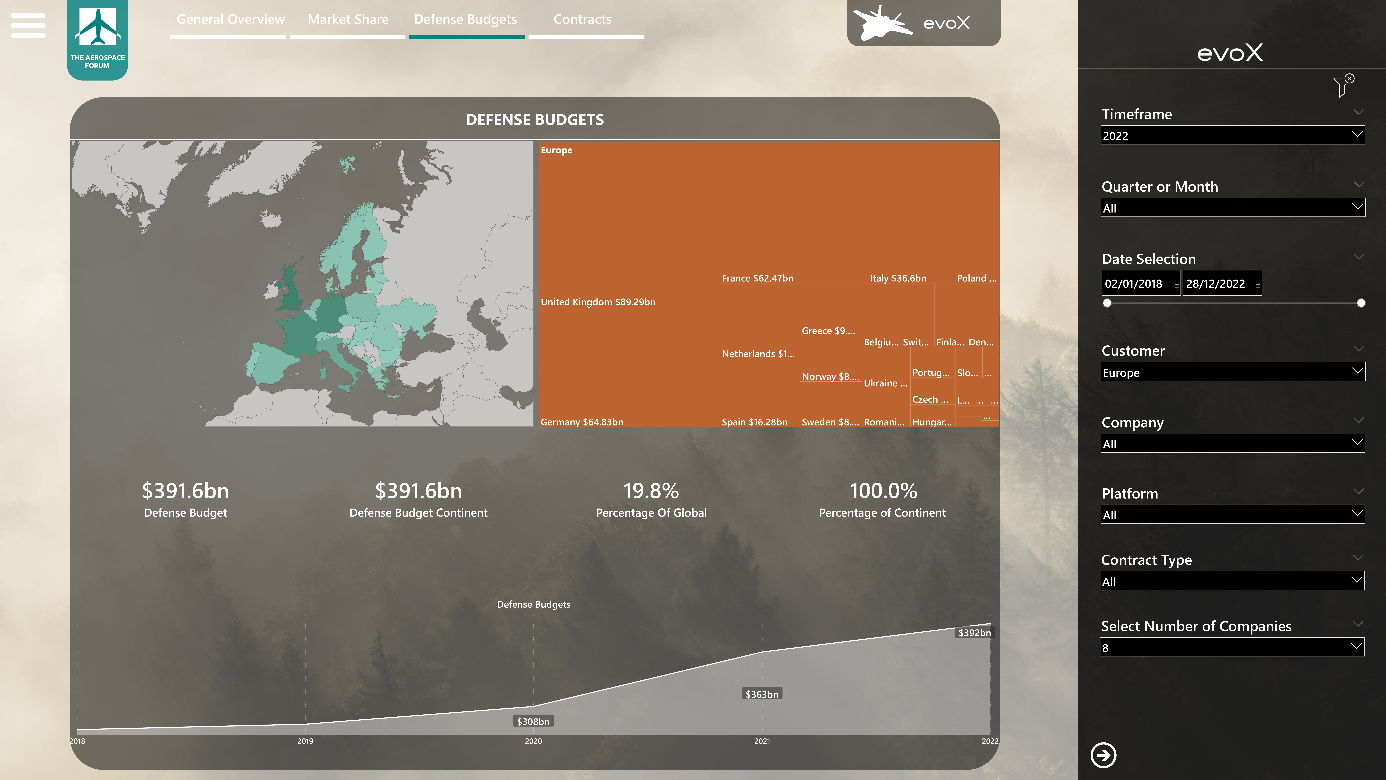

Defense Budgets Europe (The Aerospace Forum)

Now let’s have a look at Europe. There we see a significant increase from $285 billion in 2018 to $391.6 billion now. As global tensions rose not just with China but also with the US, we saw budget expansions in Europe accelerate also driven by former President Trump pushing NATO members to commit to the defense funding targets. Compared to last year, there is an increase of roughly $29 billion to the budget. The guideline that most countries do not meet is that 20% of the budget should be used for equipment expenditure. So 20% of $29 billion gives us $5.8 billion in additional funds for procurement. So looking at just the defense budgets doesn’t tell the real story because a significant portion of the budget goes towards personnel, operations and maintenance. A nearly $6 billion increase is not going to significantly impact defense manufacturers. To give you an idea, it is equivalent to 77 F-35s and Lockheed Martin delivers approximately 150 F-35s per year. So keeping that in mind as well as the fact that $6 billion has to be shared with other contractors, the current budgets are not going to provide significant growth opportunities. We will see sales materializing in 2024-2025, but until that time we also need to see funding for defense increase significantly to provide big and sustained increases in sales for defense contractors.

One thing to also keep in mind is the USD-EUR balance. The dollar is weakening now again, but in October 2022, the currencies hit parity which means that with one euro you could buy less dollars, or said differently, a country could buy less defense equipment. While I believe we are on the way back towards normalized exchange rates, this is something that should be kept in mind.

Conclusion: Defense Budget Hikes Provide Longer Term Value Generation Opportunity

We are seeing that more writers on Seeking Alpha are turning bullish on the defense industry, if they weren’t already. However, what is often not addressed is the fact that hiked defense budgets only partially translate to higher sales and it takes time for those sales to be ending up in the order books and even longer before the value is generated.

Furthermore, we see that the US purchase power for defense equipment has reduced and that is something that you wouldn’t expect if you see how bold the statements are. So, we are facing significant needs to develop new weapon capabilities in quantities that are also useful but the budget has been contracting. In Europe, we see strong improvement in the budgets as NATO members have been urged to commit to the funding guidelines and it has become painfully clear this year that for Europe the times of peace dividend on the budgets are over.

Be the first to comment