mixetto/E+ via Getty Images

Last week I wrote an article titled My Biggest Losers On Full Display and this article was humbling, as it reminded me of something my former business partner used to always tell me, “we all eat crow some of the time”. In fact, he would then say, “I’ve eaten so much crow in my lifetime that it actually tastes good”.

Now, let me be clear, I’ve never eaten crow in the literal sense, and I certainly don’t anticipate chewing on any in the future. Yet, figuratively, I’ve eaten a lot of crow, and hopefully learned from these humbling experiences.

Now, over my thirty-plus year career – as an investor and stock analyst – I can attest that a large majority of my mistakes have been due to overconfidence. I suppose that’s part of being young and not recognizing risk.

Back when I was in my early twenties, I would fly around Georgia in a single engine plane with my girlfriend (at the time). She was a pilot and of course I knew nothing about flying a plane (and landing it).

Looking back in time, I don’t think I would be a passenger in a single engine plane again (even though I trusted my girlfriend). I prefer two propellers as opposed to one. As David Swensen observed (he wrote Unconventional Success),

“Overconfidence contributes to a litany of investor errors, including inadequate diversification, overzealous security selection, and counterproductive market timing.

Misplaced confidence in forecasts of return prospects for broad asset classes and individual securities causes investors to misallocate assets and actively traded securities, thereby incurring higher costs, producing greater risks, and generating lower returns.”

Here’s my point…

I’ve been writing on Seeking Alpha for over twelve years and during that time I have seen stock pickers come and go. One of the reasons that I’ve endured here is because I’ve become a more intelligent investor because I have learned from my mistakes.

Thus, I have no problem highlighting my mistakes and most of the time someone will let me know when I do make one.

Of course, Risk Management 101 is to avoid mistakes and to help steer readers away from dangerous investment strategies to preserve and maintain hard-earned capital.

As you know, a market downturn is the true test of an investment philosophy, and within the mortgage REIT sector, there are quite a few intoxicating picks that investors are gobbling up right now.

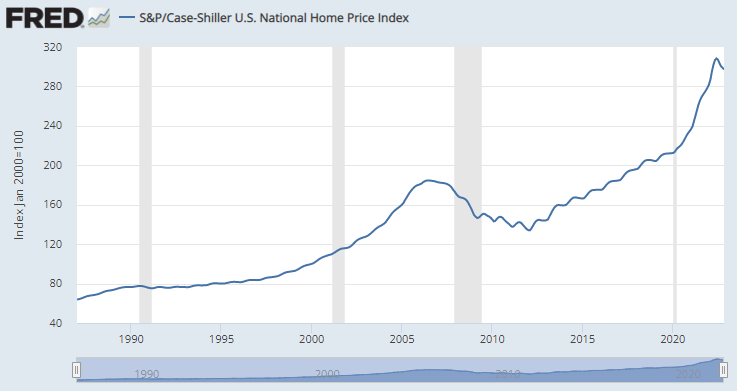

The Housing Sector

The real estate market has been strong for the past decade or so, and the pandemic era saw the meteoric rise of home prices. The large demand, shortage of houses, and easy money policy combined to create an eye-watering 18.8% increase in house prices in 2021.

It was common to see multiple offers on a house within a day in some of the most popular metropolitan areas (e.g., Austin, Seattle, Denver, etc.).

Then, inflation hit the U.S. (and the rest of the world), and the Federal Reserve decided to deflate the money balloon at a record pace. They increased interest rates sharply to tame inflation, and the stock market and real estate market suffered as a result.

Sale volumes of existing houses have been declining over the course of 2022, and the trend is continuing. The stock market overall suffered a great deal over the course of 2022, especially tech companies and growth companies.

Source: FRED

Reflecting this negative sentiment, the stock prices of residential mortgage REITs have suffered quite a bit in the time span. The beat down in prices mean that they are now offering very generous dividend yields.

While market risk is certainly still there, I believe that the opportunity that they now present is attractive, but only for certain investors.

Let me provide a disclaimer here: Residential mREITs are not for everyone and it’s critical that the investor recognize the added risk involved in these financial alternatives.

Let’s take a closer look at the following three residential mortgage REITs.

Annaly (NLY)

Annaly is a leading diversified capital manager company that has investment strategies across mortgage finance and corporate middle market lending.

They have three investment groups under them. Annaly Agency Group invests in agency mortgage-backed securities that are collateralized by residential mortgages. Annaly Residential Credit Group invests in non-agency residential mortgages assets within securitized product and whole loan markets.

Finally, Annaly Middle Market Lending Group provides financing to private equity backed middle market businesses, focusing primarily on senior debt within select industries.

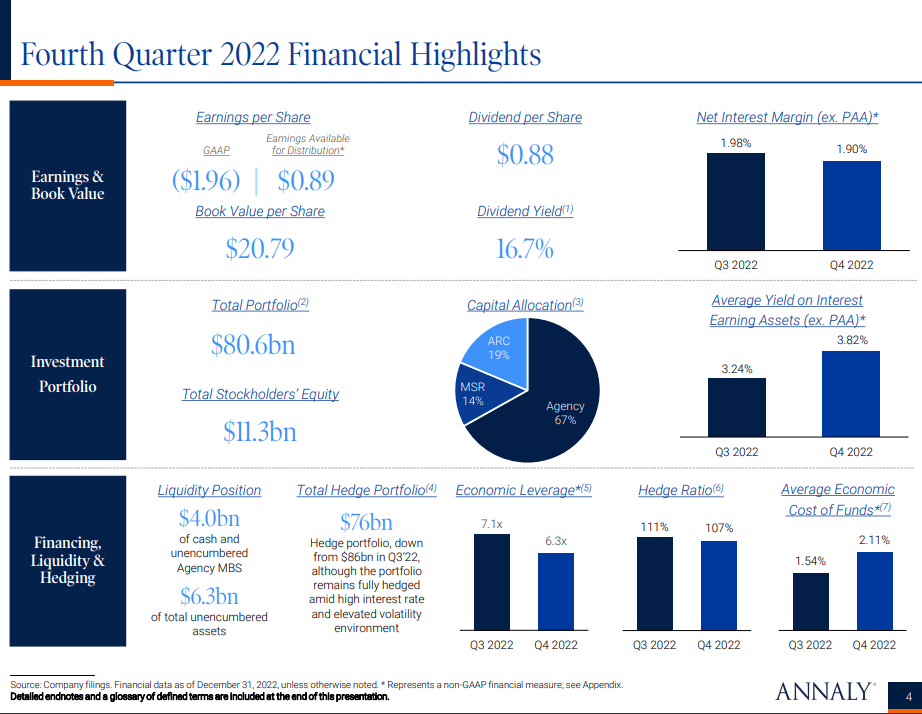

NLY Investor Relations

The size of their total portfolio is upward of $80 B, and the capital allocation among Agency, Annaly Residential Credit, and Middle Market Lending are about 67%, 19%, and 14%, respectively.

Annaly reported solid performance during the latest earnings call. Management mentioned that the mortgage and credit spreads tightened from the peak spreads in October 2022, and Annaly achieved strong 8.7% economic return for the quarter.

Annaly has a strong liquidity position, with $4.0 B of cash and unencumbered agency MBS. The average economic cost of the funds was at 1.54%. Adding to the appeal, the current dividend yield of Annaly is very tempting at 15.23%.

However, the balance sheet is not as strong as it could be, and the leverage is high. The economic leverage ratio is 7.1x, and the hedge ratio is 111%.

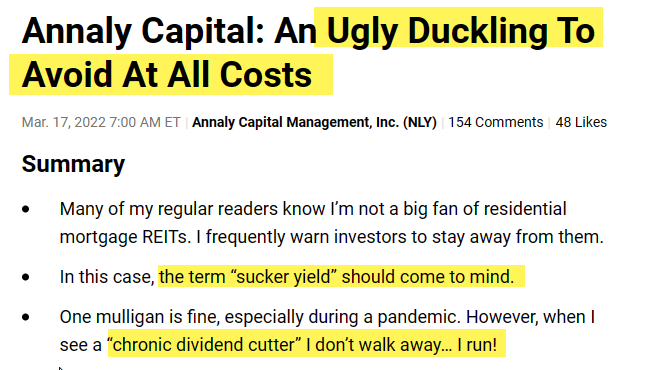

Last week on the Annaly earnings call David Finkelstein announced another dividend cut.

“Subject to determination by our Board, we expect to reduce our quarterly dividend in the first quarter of 2023 to a level closer to Annaly’s historical yield on book value of 11% to 12%, which compares to the approximately 16% yield on book we’re paying today.”

I’ve been waving the yellow flag for quite sometime:

Seeking Alpha (March 2022)

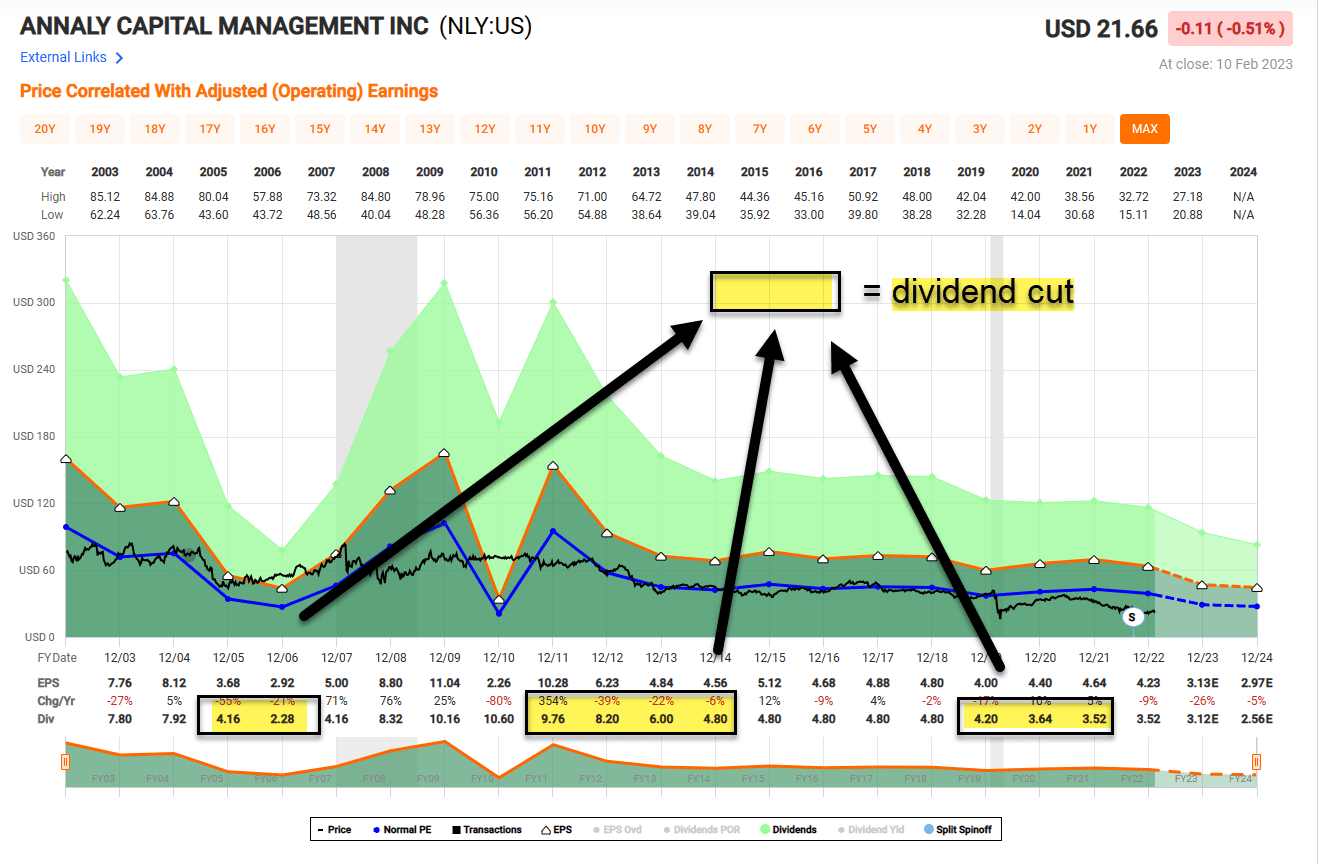

For me, I’m staying away from Annaly as the company has shown a chronic history of dividend cuts, which has of course led to under-performance in the shares.

FAST Graphs

These next two REITs also have nice dividend yields but are backed by stronger balance sheets.

Arbor (ABR)

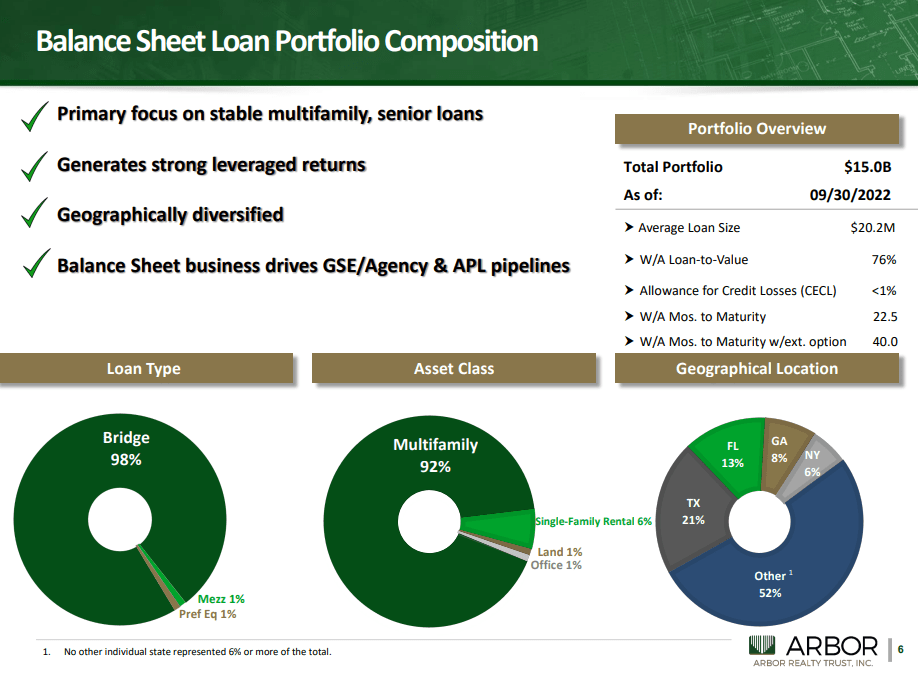

Arbor Realty is a mortgage REIT that operates through two business segments: structured loan origination and agency loan origination. The structured loan segment mostly focuses on originating bridge loans (short-term financing that is typically used for a property acquisition), and the agency loan segment originates, sells and services government backed loans (e.g., Fannie Mae and Freddie MAC) and private label loans.

Abor Realty has a very diversified and differentiated business platform. The premium operating platform has multiple product lines that produce many diverse income streams. The platform primarily focuses on the multifamily asset class with good geographical diversity.

Also, they have very stable liability structures and are well capitalized ($500 M in cash and liquidity on hand).

ABR Investor Relations

Arbor Realty reported very strong results in the latest quarter. Their 17.7% ROE in the first 9 month of 2022 is unmatched in their industry, and they recorded 10 straight years of dividend growth and 10 consecutive quarters of dividend increase (33% over the time period).

Additionally, they continued to strengthen funding sources in 2022. They closed three securitizations totaling $3.6 B and increased warehouse capacity by $1.7 B.

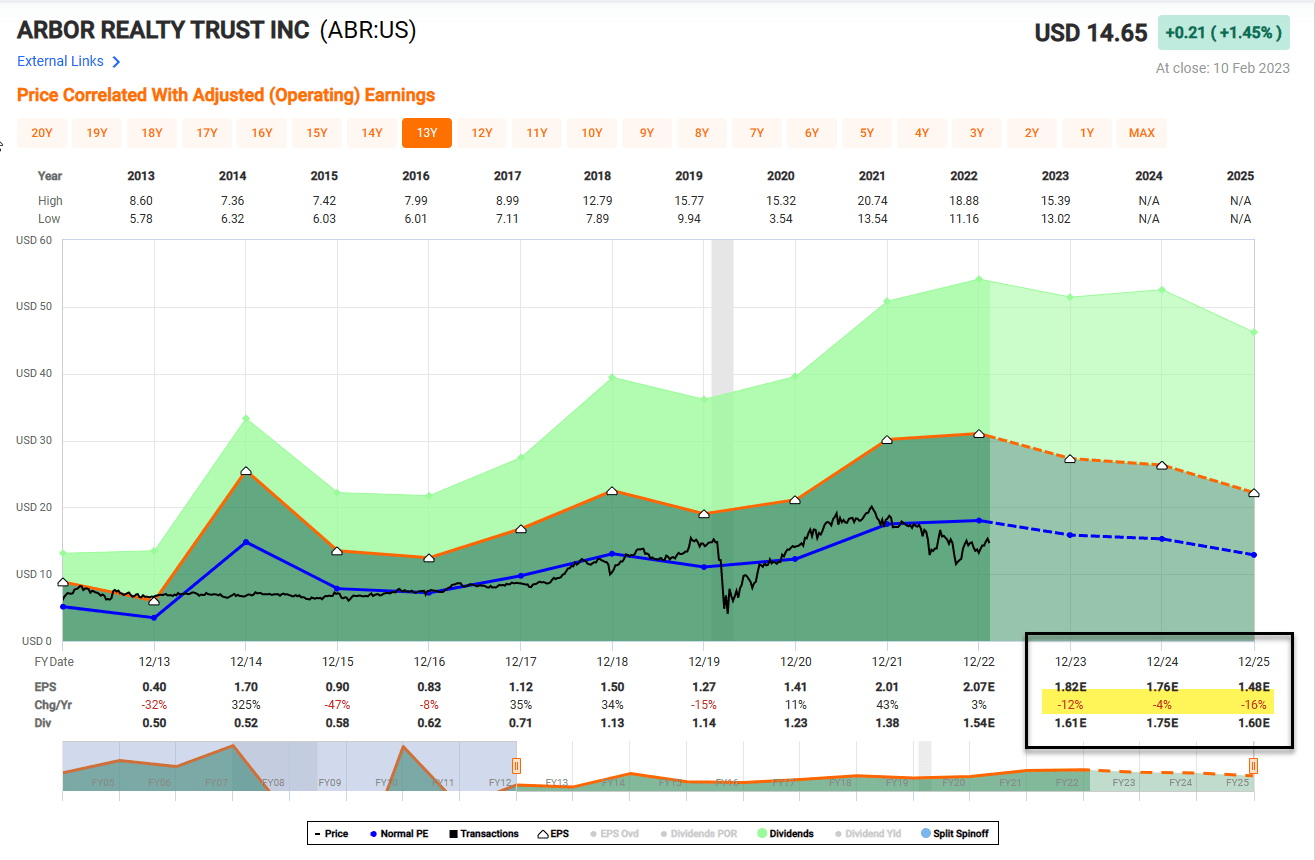

Currently, they are paying a juicy dividend with 10.76% yield. Given their strong performance and solid funding sources, I expect Arbor Realty to achieve their growth plan. Also, I believe their dividend will continue its growth trajectory as the Arbor Realty business grows.

One thing to consider however is that analysts are not as bullish as they’re forecasting negative growth in 2023 (-12%), 2024 (-4%), and 2025 (-16%). Caution is advised and limiting exposure, and of course we will be monitoring the company closely. We recommend as a Buy but maintain responsible diversification.

FAST Graphs

Rithm (RITM)

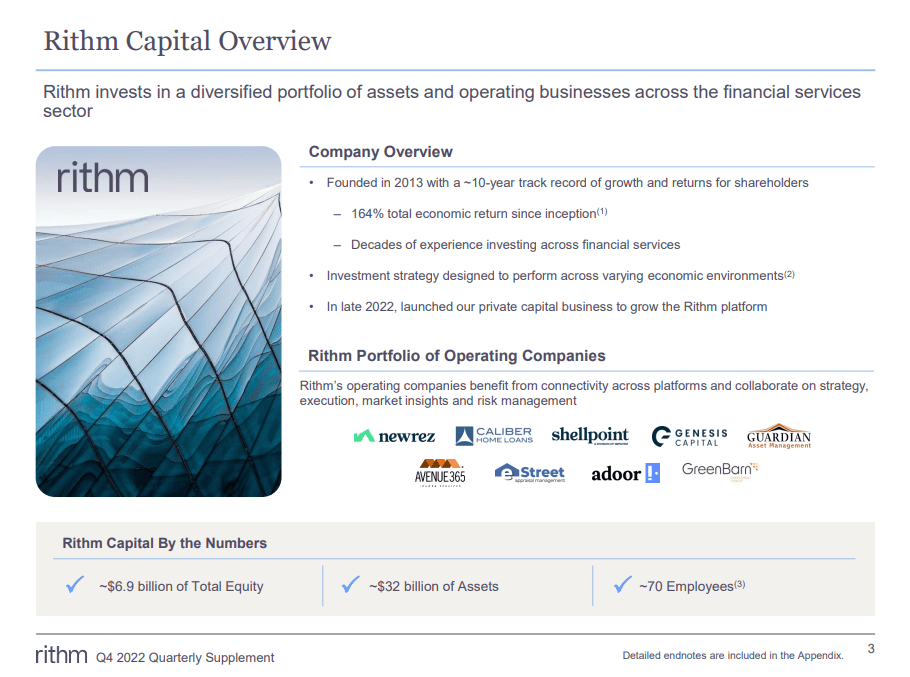

Rithm is a company that provides capital and services to the real estate and financial services sectors in the U.S. They have several operating companies under them: newrez (national mortgage lender & servicer), shellpoint (national mortgage sub-servicer), Genesis Capital (business purpose lender), Guardian Asset Management (field services & property preservation), Avenue 365 (title insurance agency), e-Street (appraisal management company), adoor! (single family rental business), and GreenBarn (investment management firm).

This diversified business portfolio provides great opportunities for Rithm to grow.

rithm Investor Relations

During the latest earnings call, the management mentioned the tough capital environment due to the hawkish Federal Reserve. Michael Nierenberg, the CEO of Rithm, stated,

“With the Federal Reserve raising rates seven times for a total of 425 basis points in 2022, the mortgage basis widening between 70 and 100 basis points, high yield index wider by almost 200 basis points and investment grade bond spreads wider by at least 25 basis points, capital markets essentially shut down during different periods.”

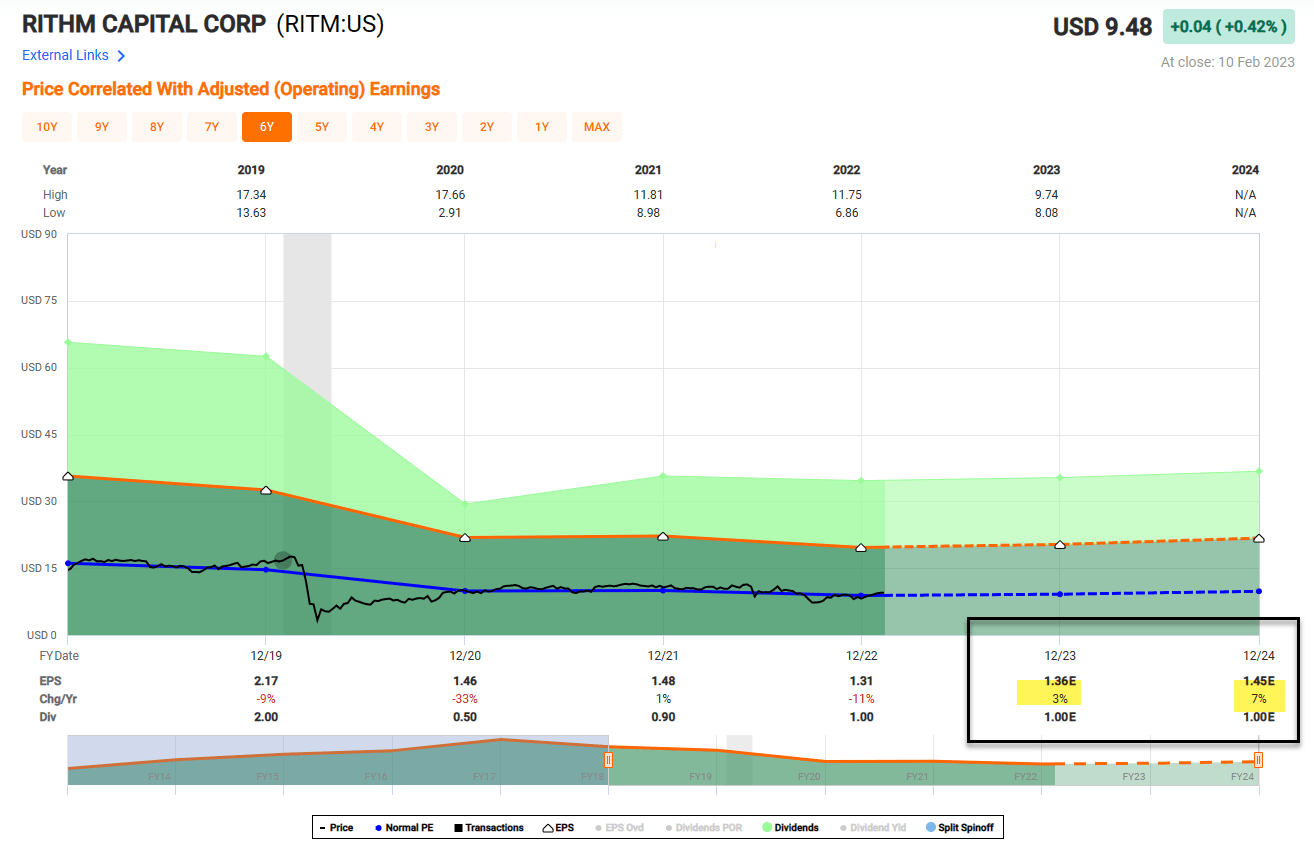

Even with this tough capital environment, Rithm managed to growth their book value by 5% during 2022, generated ROE of 15% and economic return of 14%.

The dividend payment of Rithm is great at this point. Their dividend yield is at 10.49%.

Given their diversified operations and strong portfolio, I believe Rithm will continue their strong performance and have no problem covering their dividend. Unlike ABR, analysts are forecasting positive earnings for RITM in 2023 (+2%) and 2024 (+7%). We recommend as a Buy, but maintain responsible diversification.

FAST Graphs

Risks…

The Federal Reserve plans to maintain or raise the high interest rate for a while, and the high interest rate is keeping mortgage rates at the highest level that we have seen in the past several years.

Due to the high borrowing cost environment, the residential real estate market has been in a precarious position in the past year, and the conditions may continue for a while.

The existing home sale volume has been decreasing over 11 straight months, and the trend will likely continue. Given the struggling real estate market, residential mortgage companies may suffer from declining revenue and profit.

Even though market sentiment has been improving, especially here in January, there is still a large fear over an upcoming recession. The recessionary environment may put constraints on the capital market.

Fewer institutions might be interested in lending money, causing borrowing costs to further increase. This capital scarce environment may put significant pressure on mortgage REIT companies.

Conclusion

One of my favorite quotes related to the investment is from Benjamin Graham,

“Adversity is bitter, but its uses may be sweet. Our loss was great, but in the end, we could count great compensations.”

Like Graham, I can also count great compensations, primarily because I learned from my mistakes. Chasing yield is dangerous, especially in this environment, and that’s why I stick with time-tested SWANs like Realty Income (O), Prologis (PLD), and American Tower (AMT).

Now is not the time to be too cute, because (in the words of my very wealthy friend), “The thrill of victory is not worth the agony of defeat”.

Author’s note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

Be the first to comment